Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Oshkosh Corporation (NYSE:OSK) presented its second quarter 2025 earnings results on August 1, 2025, revealing a mixed performance across its business segments. The heavy-duty vehicle manufacturer reported a 4% year-over-year revenue decline while maintaining stable margins and slightly improving earnings per share. In premarket trading following the presentation, Oshkosh shares were down 1.21% to $125.00, suggesting investors had mixed reactions to the results.

The company’s performance shows signs of stabilization following a challenging first quarter, when Oshkosh missed both EPS and revenue forecasts. The Q2 results indicate the company is navigating ongoing market challenges while maintaining its full-year guidance.

Quarterly Performance Highlights

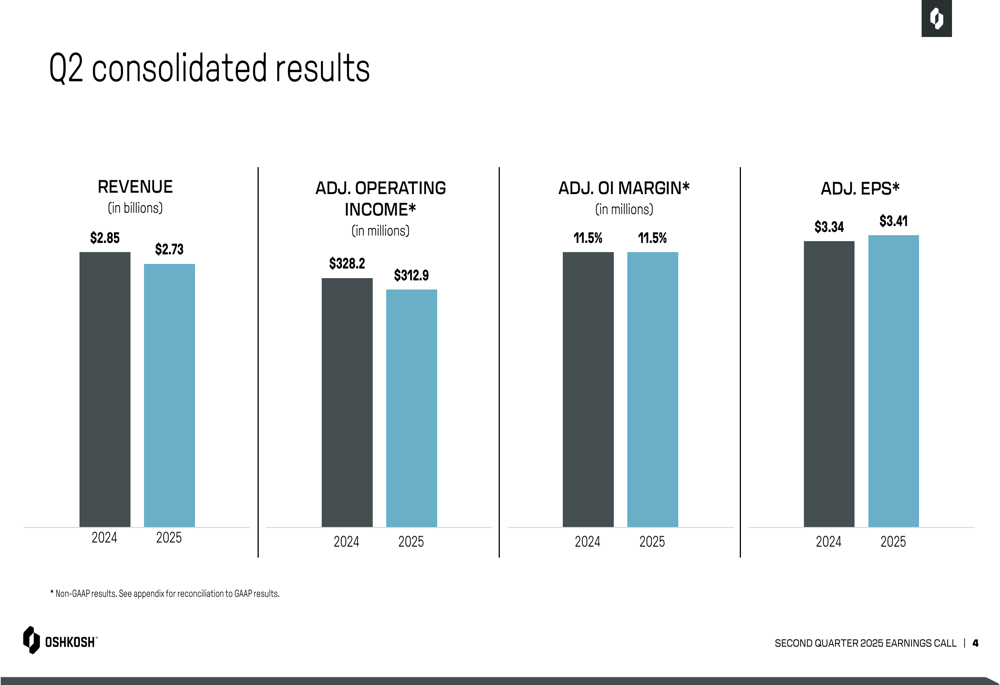

Oshkosh reported Q2 2025 revenue of $2.73 billion, down 4.0% from $2.85 billion in the same period last year. Despite the revenue decline, the company maintained its adjusted operating income margin at 11.5% and improved its adjusted earnings per share to $3.41, a 2.1% increase from $3.34 in Q2 2024.

As shown in the following consolidated results chart:

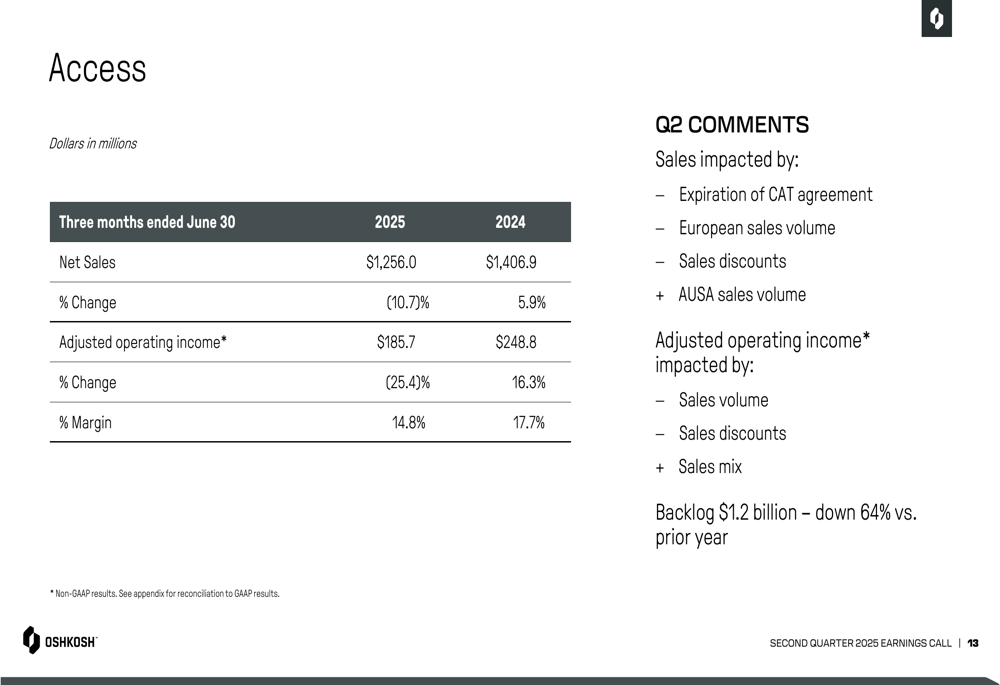

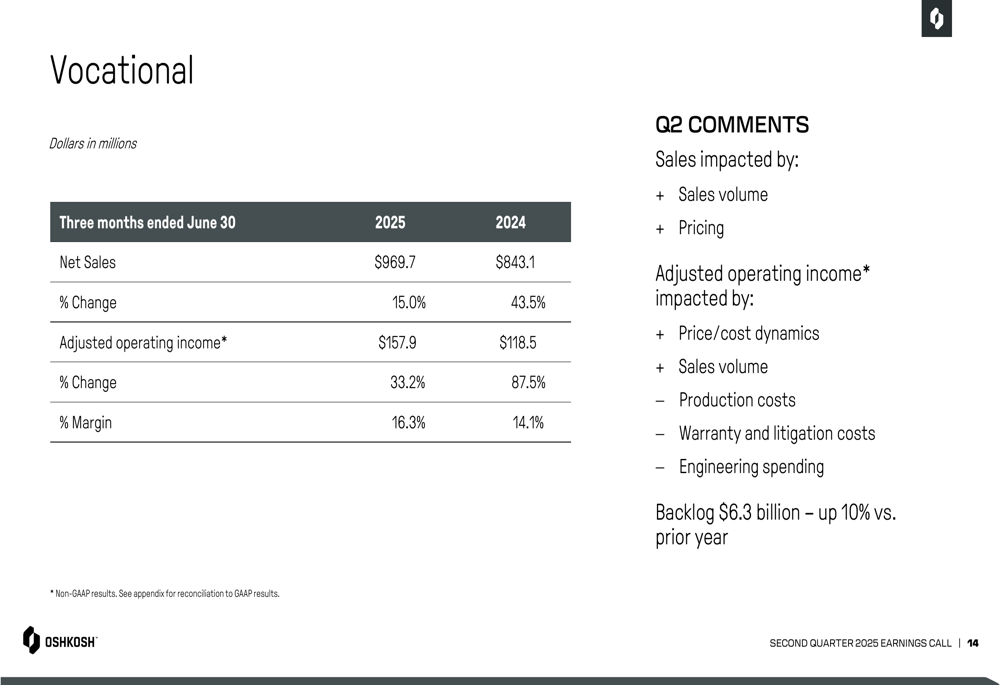

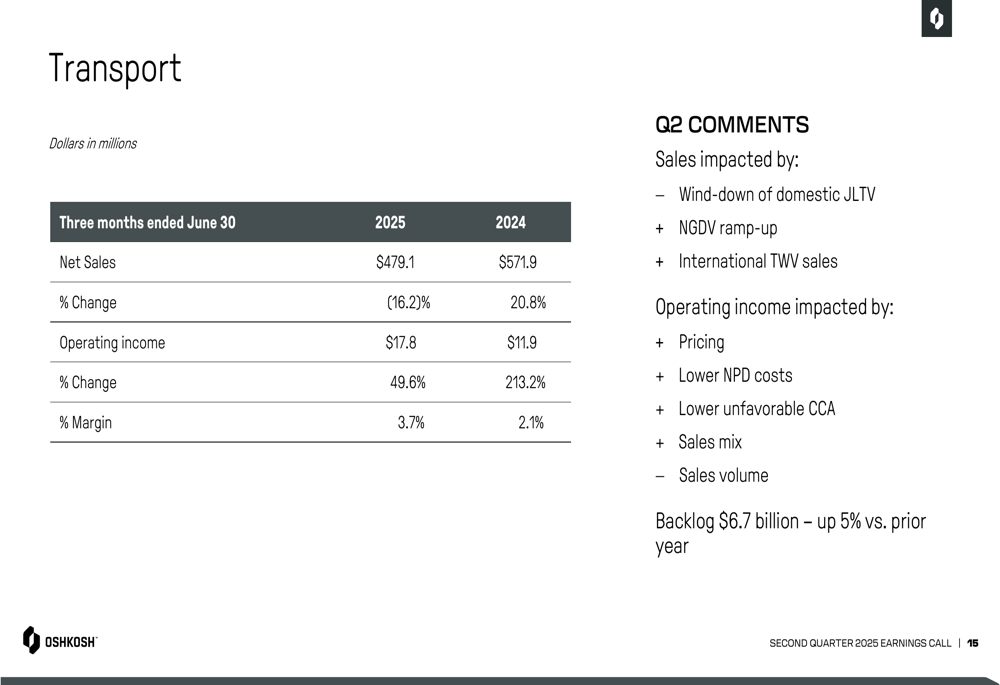

The company’s performance varied significantly across its three business segments. The Vocational segment emerged as the standout performer with 15.0% revenue growth and a 33.2% increase in adjusted operating income. Meanwhile, the Access segment faced headwinds with a 10.7% revenue decline and a 25.4% drop in adjusted operating income. The Transport segment showed mixed results with a 16.2% revenue decline but a 49.6% improvement in operating income.

The segment breakdown reveals the divergent performance trajectories:

A closer examination of the Access segment shows concerning trends, particularly in its backlog, which declined 64% year-over-year to $1.2 billion. The segment was negatively impacted by the expiration of the CAT agreement, lower European sales volume, and increased sales discounts.

In contrast, the Vocational segment demonstrated robust performance with revenue of $969.7 million, up 15.0% year-over-year, and an adjusted operating income margin of 16.3%, up from 14.1% in the prior year. The segment’s backlog increased 10% to $6.3 billion, indicating continued strong demand.

The Transport segment, despite a 16.2% revenue decline to $479.1 million, improved its operating margin to 3.7% from 2.1% in the prior year. The revenue decline was primarily attributed to the wind-down of domestic JLTV production, partially offset by the ramp-up of NGDV ( Next (LON:NXT) Generation Delivery Vehicle) production and international tactical wheeled vehicle sales. The segment’s backlog increased 5% to $6.7 billion.

Strategic Initiatives

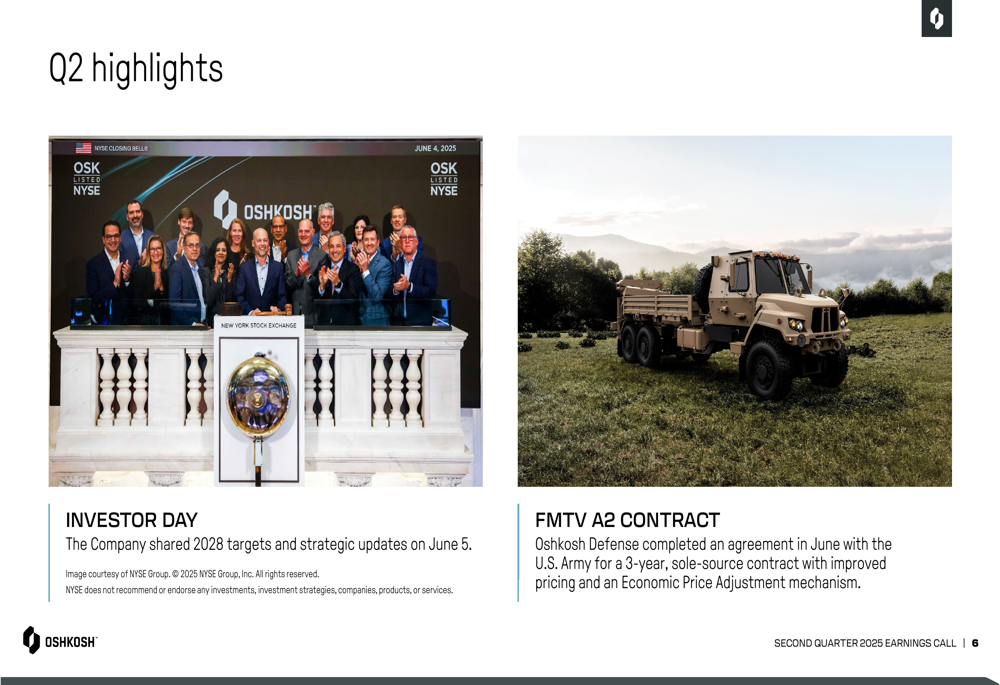

During the quarter, Oshkosh highlighted several strategic developments that align with its long-term growth strategy. The company held an Investor Day on June 5, 2025, where it shared its 2028 targets and strategic updates. The Oshkosh team also rang the closing bell at the New York Stock Exchange, symbolizing its commitment to shareholder value.

A significant win for the Defense division was the completion of a three-year, sole-source contract with the U.S. Army for the FMTV A2 (Family of Medium Tactical Vehicles) program. The new agreement includes improved pricing terms and an Economic Price Adjustment mechanism, which should provide better margin stability.

The following image highlights these key Q2 developments:

On the innovation front, JLG launched a new line of micro-sized scissor lifts targeting the growing data center market, with plans to expand the product line further. Additionally, the company’s Pierce brand delivered 13 custom pumpers and two aerial units to Kansas City, Missouri, as part of its strategy to expand fire apparatus capacity.

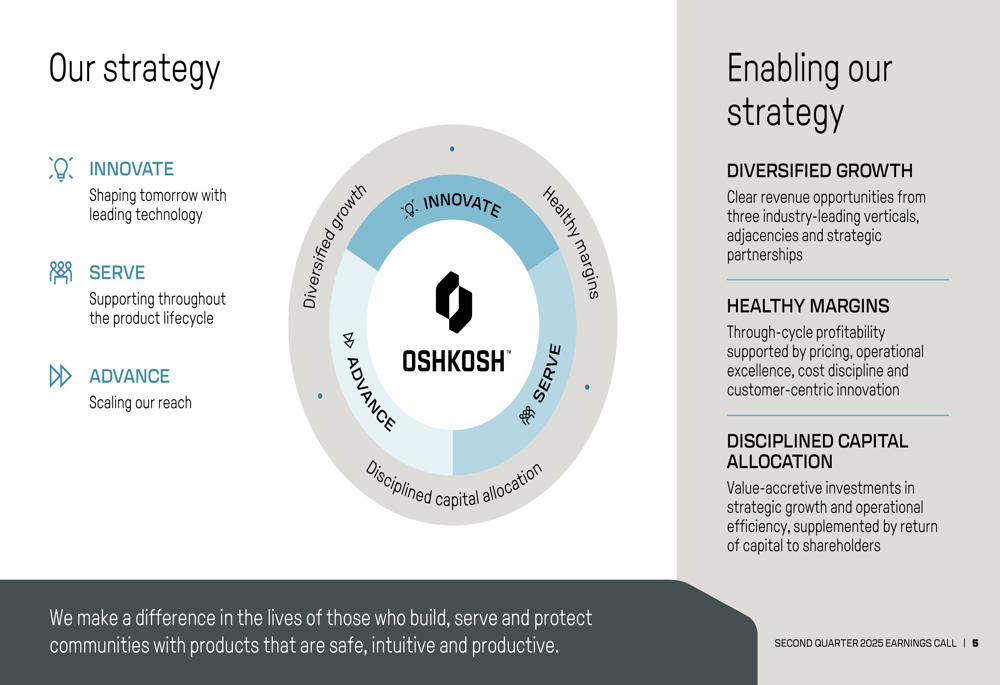

Oshkosh’s overall business strategy continues to focus on three key pillars: Innovate, Serve, and Advance. This approach aims to deliver diversified growth, healthy margins, and disciplined capital allocation, as illustrated in the company’s strategy framework:

Forward-Looking Statements

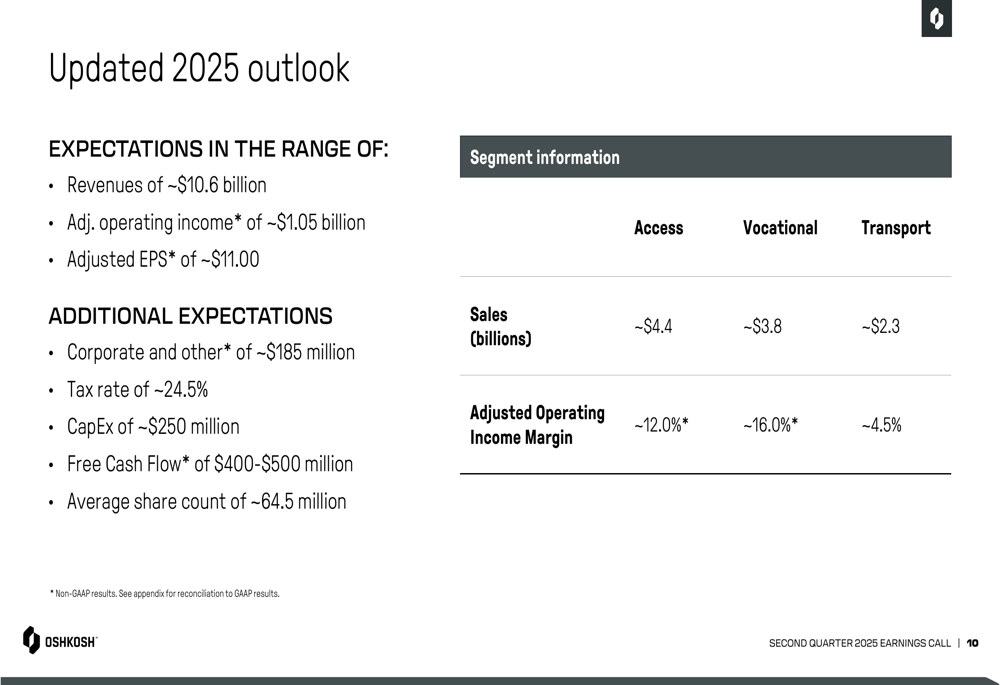

Oshkosh maintained its full-year 2025 guidance, projecting revenues of approximately $10.6 billion, adjusted operating income of around $1.05 billion, and adjusted EPS of approximately $11.00. The company expects free cash flow between $400-$500 million and capital expenditures of about $250 million.

The detailed outlook for 2025 is presented in the following slide:

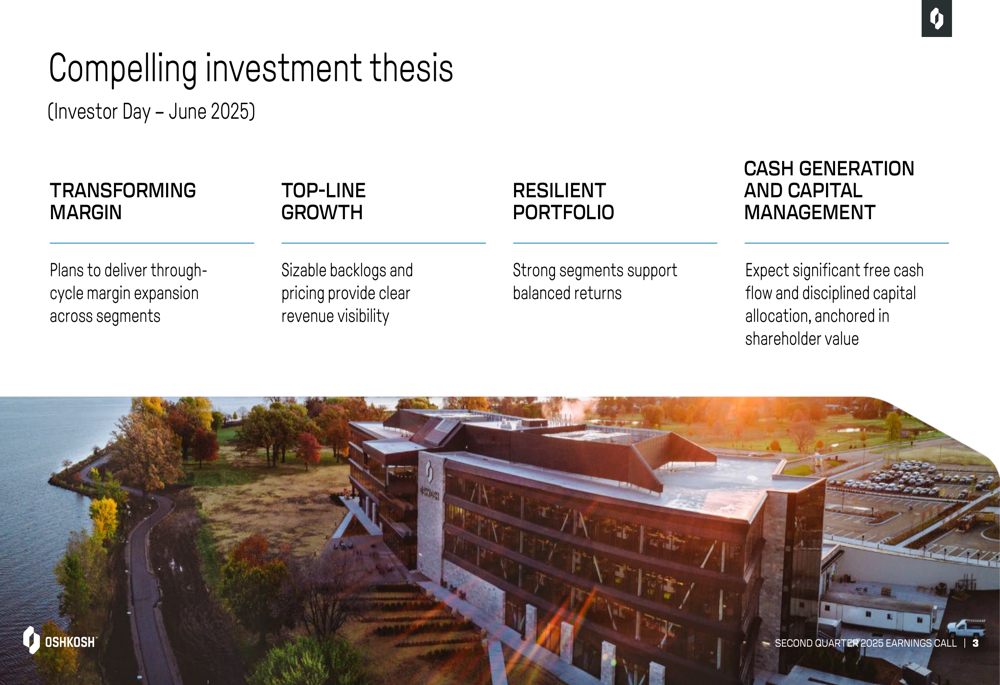

The company’s investment thesis emphasizes margin transformation, top-line growth supported by sizable backlogs, a resilient portfolio with strong segments supporting balanced returns, and significant free cash flow generation with disciplined capital allocation.

Conclusion

Oshkosh’s Q2 2025 results demonstrate the company’s ability to navigate challenging market conditions while maintaining profitability. The stark contrast between segment performances highlights both risks and opportunities in Oshkosh’s diversified business model. The strong performance in the Vocational segment and improving margins in the Transport segment are helping to offset weakness in the Access segment.

While the significant decline in the Access segment’s backlog raises concerns about future revenue streams, the company’s maintained full-year guidance suggests confidence in its ability to execute on its strategic initiatives and potentially improve performance in the second half of the year. Investors will likely focus on whether Oshkosh can sustain its margin improvements and successfully navigate the ongoing challenges in the Access Equipment market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.