BofA: Investors pour into bonds, pull back from crypto

Introduction & Market Context

Owens & Minor Inc (NYSE:OMI) presented its first quarter 2025 earnings on May 8, 2025, maintaining its full-year outlook amid continued operational momentum. The healthcare solutions company’s stock responded positively, trading up 9.54% to $8.50 in premarket activity, building on recent gains that have helped the company recover from its 52-week low of $6.07.

The presentation comes after Owens & Minor reported better-than-expected Q4 2024 results, which saw the company beat EPS estimates while slightly missing revenue targets. The healthcare logistics and medical supply distributor continues to navigate a challenging but improving market environment.

2025 Financial Outlook

In its Q1 2025 presentation, Owens & Minor maintained the full-year guidance it had previously outlined, providing investors with a comprehensive view of its financial expectations for the year.

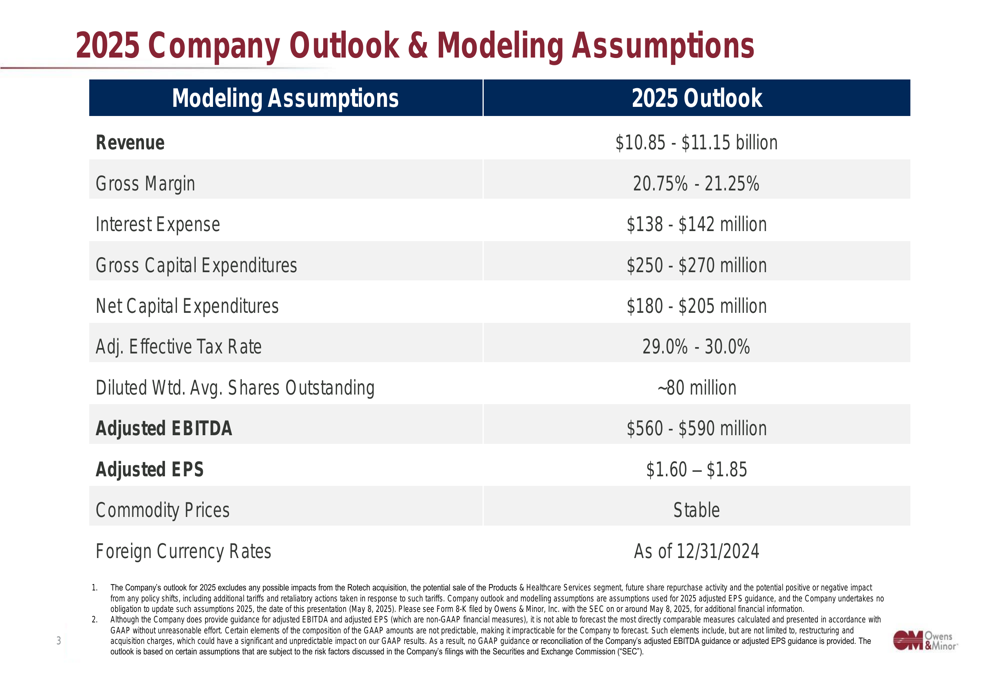

The company projects 2025 revenue between $10.85 billion and $11.15 billion, with adjusted EBITDA ranging from $560 million to $590 million. Adjusted earnings per share are expected to fall between $1.60 and $1.85, representing potential growth from 2024 performance when the company reported full-year adjusted EPS growth of 13%.

As shown in the following detailed outlook slide:

The presentation highlights several key modeling assumptions, including a gross margin range of 20.75% to 21.25% and interest expenses between $138 million and $142 million. The company also forecasts significant capital expenditures, with gross capital expenditures of $250-$270 million and net capital expenditures of $180-$205 million, suggesting continued investment in growth initiatives.

Owens & Minor’s outlook is based on stable commodity prices and foreign currency rates as of December 31, 2024, indicating the company has factored in current market conditions while providing this guidance.

Strategic Initiatives & Growth Drivers

While specific strategic initiatives weren’t detailed in the available slides, the company’s recent performance suggests continued focus on its two primary segments. The Patient Direct segment, which showed mid-single-digit growth in Q4 2024, remains a key driver for the company, benefiting from demographic tailwinds and innovations like the Byram Connect digital health coach for diabetes patients.

The company’s debt reduction strategy also appears to remain a priority, following the $244 million reduction achieved in 2024, which brought the total debt reduction to $647 million over two years. This focus on strengthening the balance sheet positions Owens & Minor to pursue strategic growth opportunities while improving financial flexibility.

Market Reaction & Analyst Perspectives

The market’s positive reaction to Owens & Minor’s Q1 2025 presentation, with shares climbing 9.54% in premarket trading to $8.50, suggests investors are encouraged by the company’s performance and outlook. This builds on the 15.54% surge that followed the Q4 2024 earnings report, indicating growing confidence in the company’s strategic direction.

Despite this optimism, Owens & Minor’s stock remains well below its 52-week high of $21.02, suggesting potential upside if the company continues to execute on its strategic initiatives and meet or exceed its financial targets.

Forward-Looking Statements

As noted in the company’s safe harbor statement, Owens & Minor’s outlook contains forward-looking statements that involve risks and uncertainties:

The company emphasizes that its non-GAAP financial measures, which exclude certain items management doesn’t consider reflective of core business operations, are used for internal evaluation, financial planning, and incentive compensation. These measures should be considered supplementary to GAAP results rather than substitutes.

Investors should continue to monitor Owens & Minor’s performance throughout 2025 to assess whether the company can deliver on its financial targets and strategic objectives in an evolving healthcare market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.