US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

Park Hotels & Resorts Inc. (NYSE:PK) released its second quarter 2025 supplemental data presentation on July 31, 2025, revealing a mixed financial performance that prompted a downward revision to its full-year outlook. Despite the challenges, investors responded positively, with the stock rising 2.36% to $10.80 following the earnings announcement, suggesting confidence in the company’s long-term strategy despite near-term headwinds.

As one of the largest publicly-traded lodging REITs, Park Hotels maintains a portfolio of 39 premium-branded hotels with approximately 25,000 rooms, primarily located in prime city center and resort locations. The company continues to execute its strategy of reshaping its portfolio to focus on core assets while divesting non-core properties.

Quarterly Performance Highlights

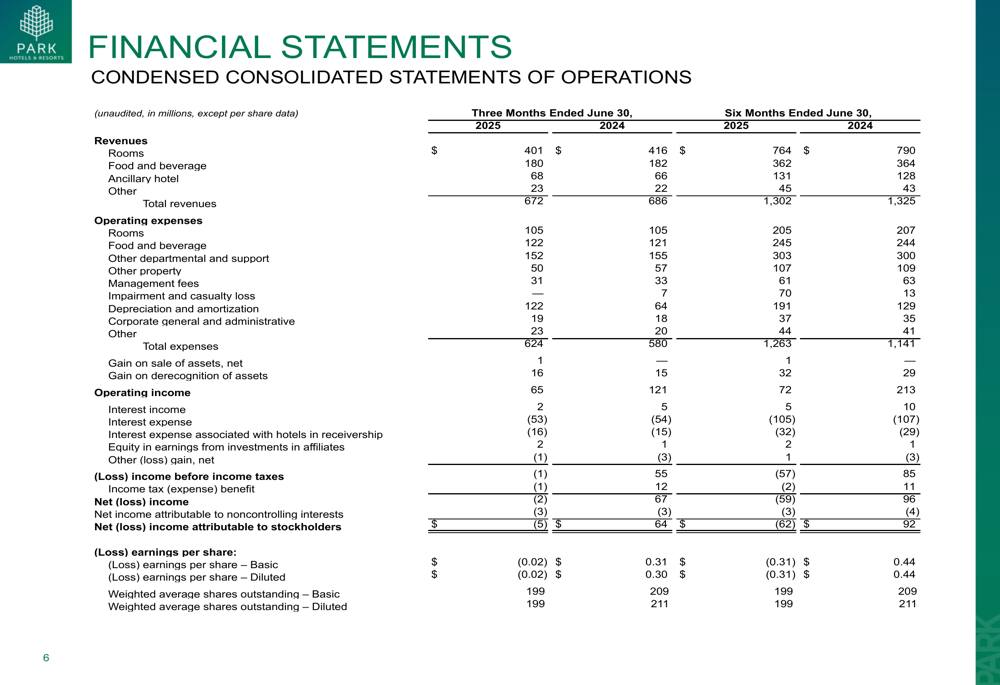

Park Hotels reported total revenues of $672 million for Q2 2025, representing a slight decline from $686 million in the same period last year. The company posted a net loss attributable to stockholders of $5 million, a significant drop from the $64 million net income reported in Q2 2024.

As shown in the following consolidated statements of operations, the company maintained relatively stable adjusted FFO per share at $0.64 compared to $0.65 in the prior year period, despite the revenue challenges:

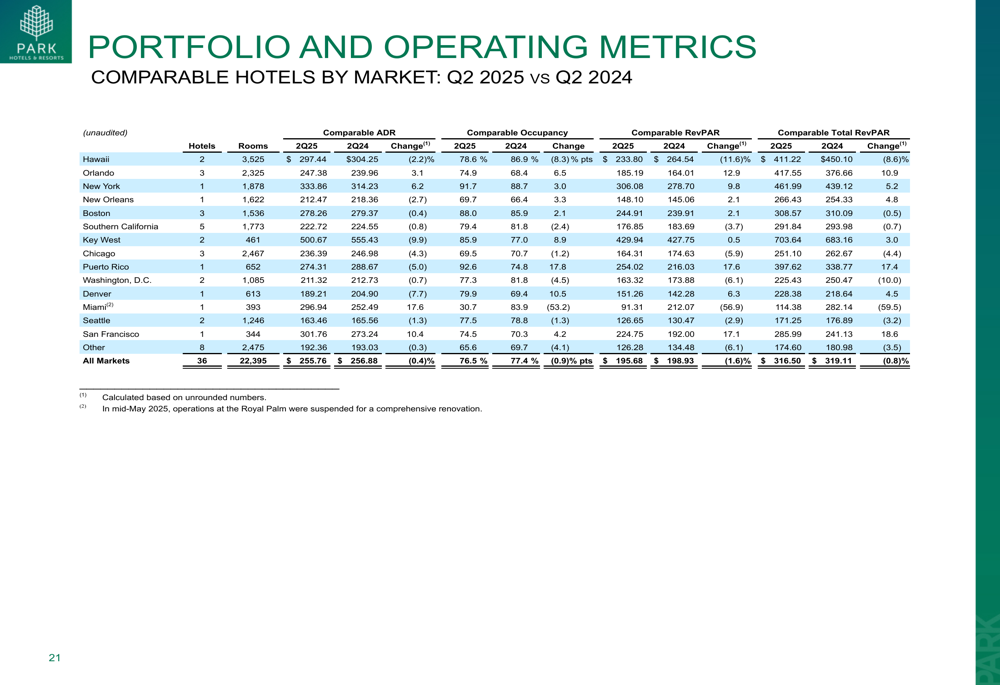

The company’s comparable RevPAR (Revenue Per Available Room) declined to $195.68 in Q2 2025 from $198.93 in Q2 2024, representing a 1.6% year-over-year decrease. This aligns with the earnings report which noted a 160 basis point decline in RevPAR.

Performance varied significantly by market, with Hawaii showing weakness while Orlando demonstrated strength. The following chart breaks down the company’s performance by key markets:

Detailed Financial Analysis

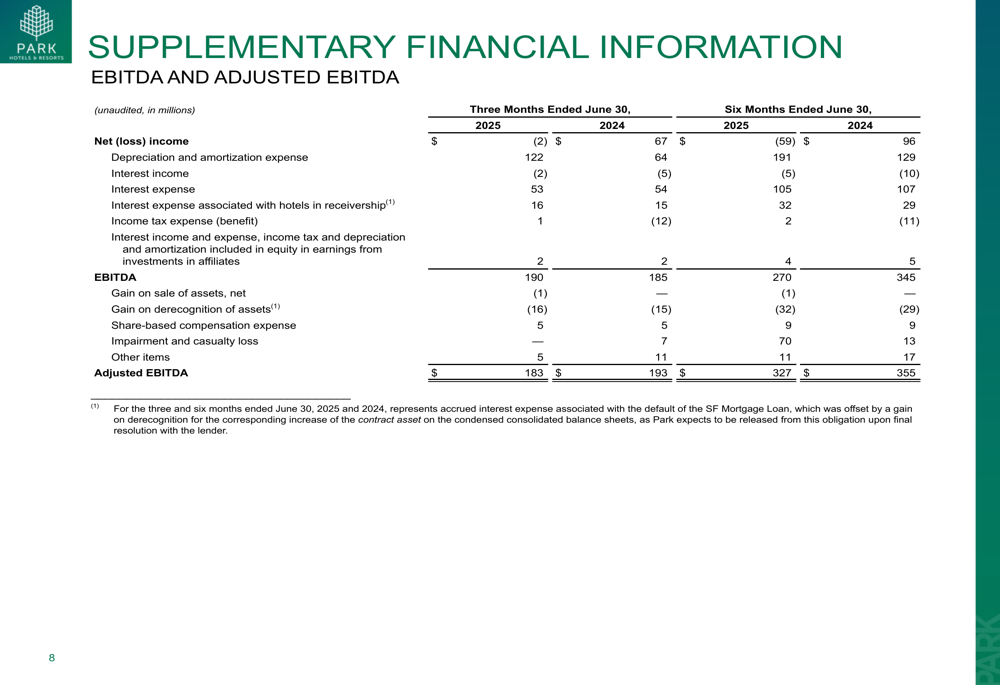

Park Hotels’ Adjusted EBITDA decreased to $183 million in Q2 2025 from $193 million in Q2 2024, while Comparable Hotel Adjusted EBITDA came in at $191 million compared to $197 million in the prior year period. The following table provides a detailed breakdown of these key metrics:

The company’s Hotel Adjusted EBITDA margin remained relatively strong at 29.6%, as confirmed in both the presentation and earnings report. This indicates that despite revenue challenges, Park Hotels has maintained operational efficiency.

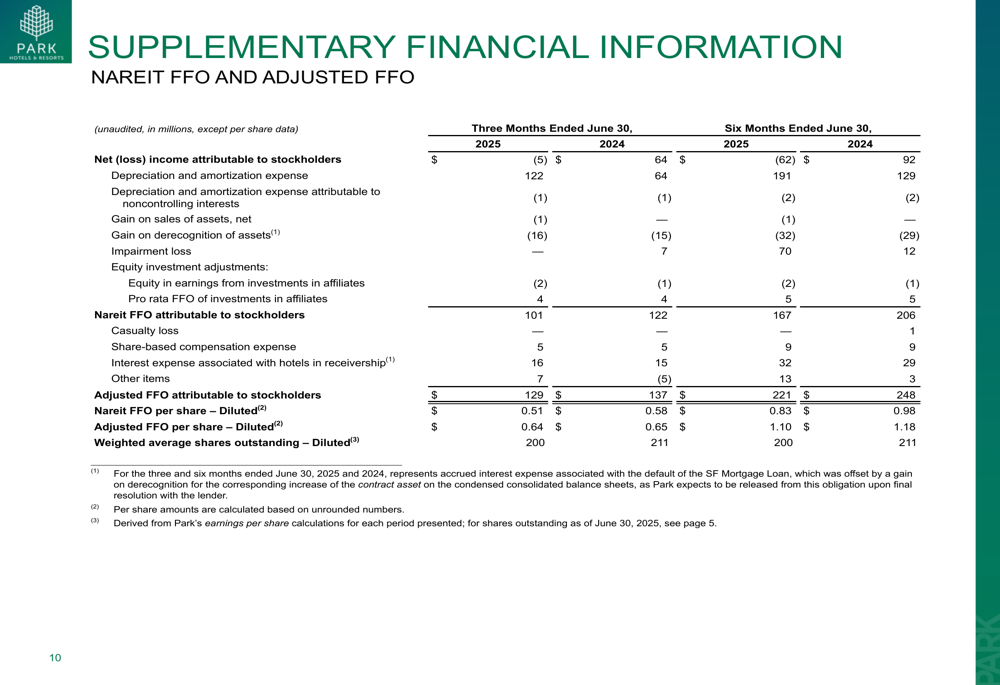

The NAREIT FFO (Funds From Operations) and Adjusted FFO metrics, which are key performance indicators for REITs, showed some resilience despite the overall challenging environment:

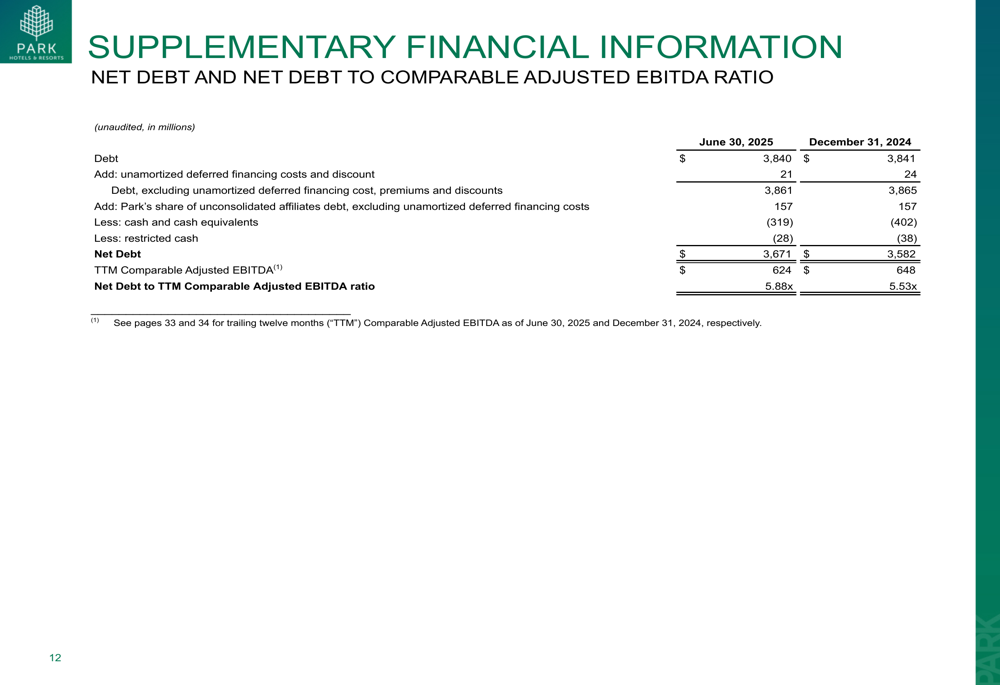

Park’s leverage position has slightly deteriorated, with Net Debt to TTM Comparable Adjusted EBITDA ratio increasing to 5.88x as of June 2025 from 5.53x in December 2024:

Strategic Initiatives

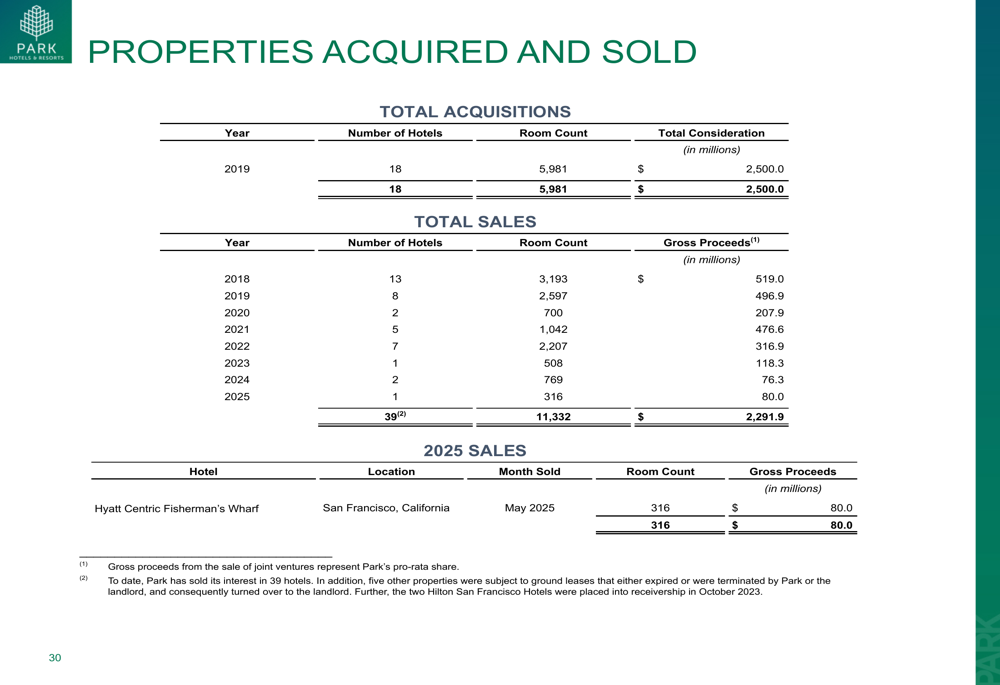

Park Hotels continues to execute its portfolio optimization strategy, focusing on its core properties while divesting non-core assets. The company has sold 39 properties since 2018 for a total consideration of approximately $2.3 billion, including the recent sale of Hotel at Fisherman’s Wharf in San Francisco (316 rooms) for $80 million in 2025.

The following slide summarizes the company’s acquisition and disposition activities:

This strategic reshaping aligns with CEO Thomas Baltimore’s comments from the earnings call, where he emphasized, "We are laser focused on reshaping the portfolio and getting down to that core portfolio." The company’s core portfolio, which represents approximately 90% of its value, continues to be the primary focus for future growth and investment.

Forward-Looking Statements

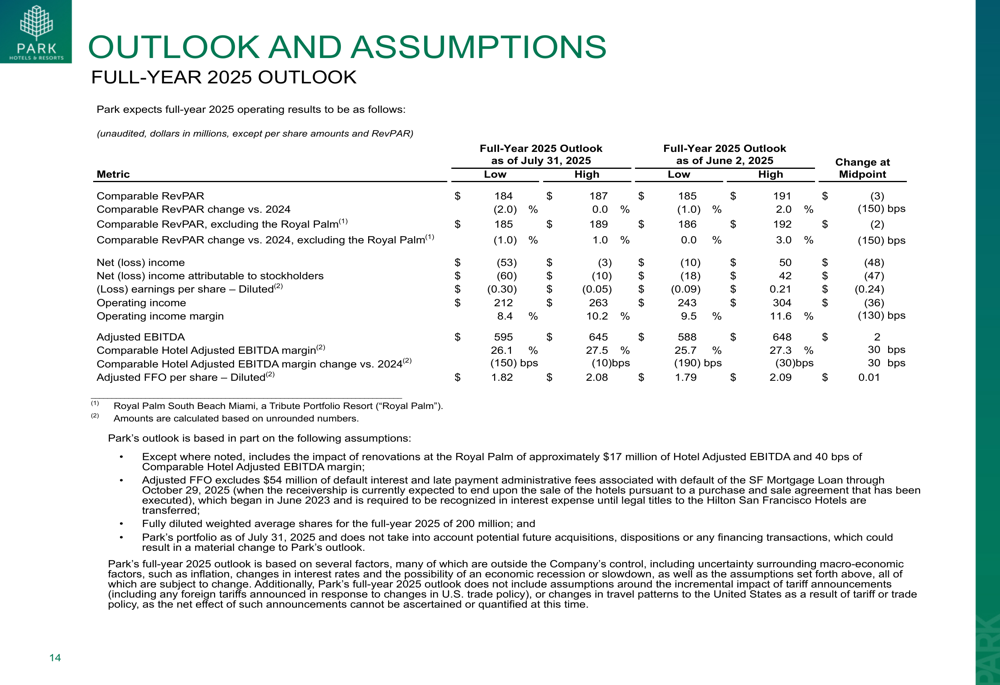

Park Hotels revised its full-year 2025 outlook downward compared to previous guidance provided on June 2, 2025. The updated outlook, as of July 31, 2025, projects:

- Comparable RevPAR of $184-$187, representing a -2.0% to 0.0% change versus 2024

- Net loss of $(53) million to $(3) million

- Adjusted EBITDA of $595 million to $645 million

- Adjusted FFO per share of $1.82 to $2.08

The following slide details the revised outlook and the changes from previous guidance:

Despite the overall cautious outlook, the company anticipates Q4 RevPAR growth of 3-5%, indicating potential recovery in certain markets as noted in the earnings report. This suggests that while near-term challenges persist, particularly in Hawaii, the company sees potential improvement in the latter part of the year.

Market Challenges and Opportunities

Park Hotels faces several challenges, including continued weakness in the Hawaii market, where Hotel Adjusted EBITDA declined to $45 million in Q2 2025 from $56 million in Q2 2024. This aligns with the earnings report’s mention of sluggish recovery in international travel to Hawaii.

Conversely, the Orlando market has shown strength, with Hotel Adjusted EBITDA increasing to $30 million in Q2 2025 from $25 million in Q2 2024. The company’s resort markets, including Orlando and Key West, continue to perform well despite broader market challenges.

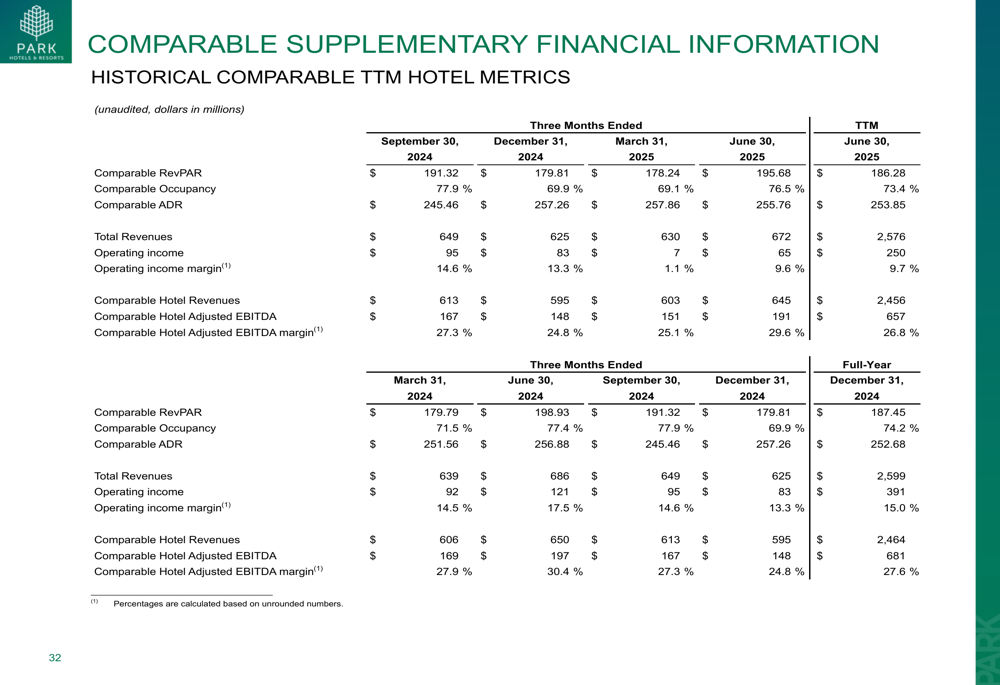

The historical performance metrics provide context for the company’s trajectory over recent quarters:

Market volatility remains a concern, with uncertainty around tariffs and geopolitical issues potentially impacting business travel and international tourism. The stock’s beta of 1.82 indicates higher volatility compared to the broader market, as noted in the earnings report.

Despite these challenges, Park Hotels’ focus on operational efficiency, strategic portfolio reshaping, and targeted investments in core properties positions the company to navigate the current environment while preparing for potential recovery in key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.