Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Parkland Corporation (TSX:PKI) unveiled its May 2025 investor presentation outlining ambitious growth targets despite recent earnings challenges. The fuel retailer and distributor, which operates across 26 countries with approximately 5,400 employees, is pursuing a strategy focused on resilience through diversification, organic growth, and disciplined capital allocation.

The presentation comes shortly after Parkland’s Q4 2024 earnings report, which saw the company miss analyst expectations with an EPS of $0.57 (below the forecasted $0.68) and revenue of $6.73 billion (below the anticipated $7.64 billion). Despite these challenges, Parkland’s stock has recovered, with fundamentals showing a 5.51% increase to $38.28 as of May 5, 2025.

Financial Performance Highlights

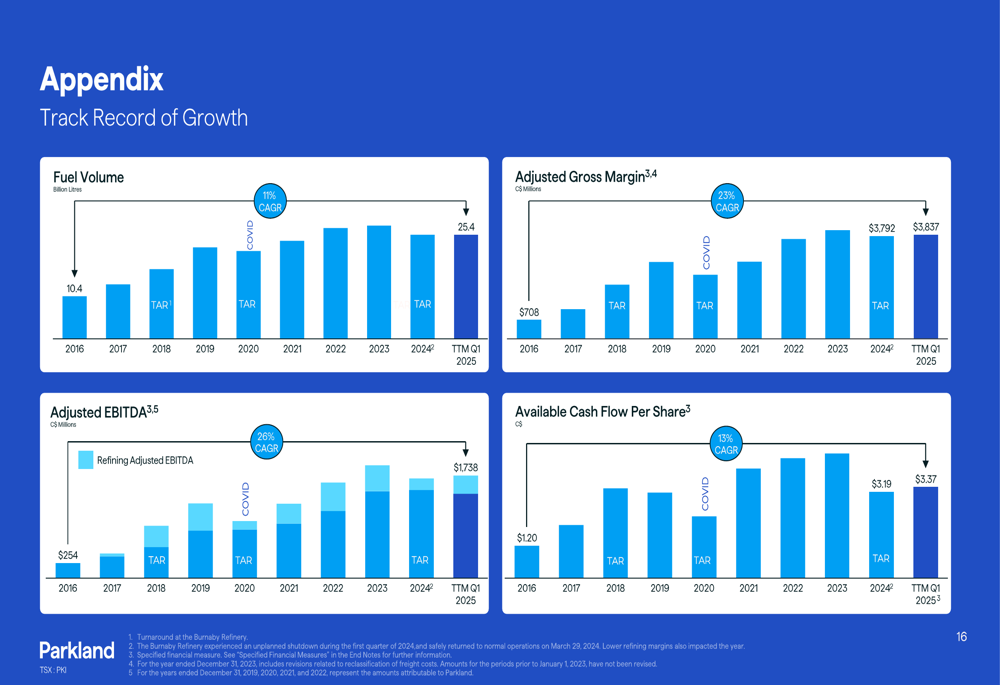

Parkland reported trailing twelve months (TTM) Q1 2025 Adjusted EBITDA of approximately $1.7 billion on fuel volumes of 25 billion liters. The company highlighted its impressive long-term growth trajectory, with a 26% compound annual growth rate (CAGR) in Adjusted EBITDA from 2016 to TTM Q1 2025.

As shown in the following chart of Parkland’s growth metrics:

The company has demonstrated consistent growth across multiple financial metrics, including a 23% CAGR in adjusted gross margin and a 13% CAGR in available cash flow per share over the same period. This growth has supported Parkland’s dividend, which has increased from $1.02 per share in 2012 to $1.44 in 2025, representing a 3% CAGR.

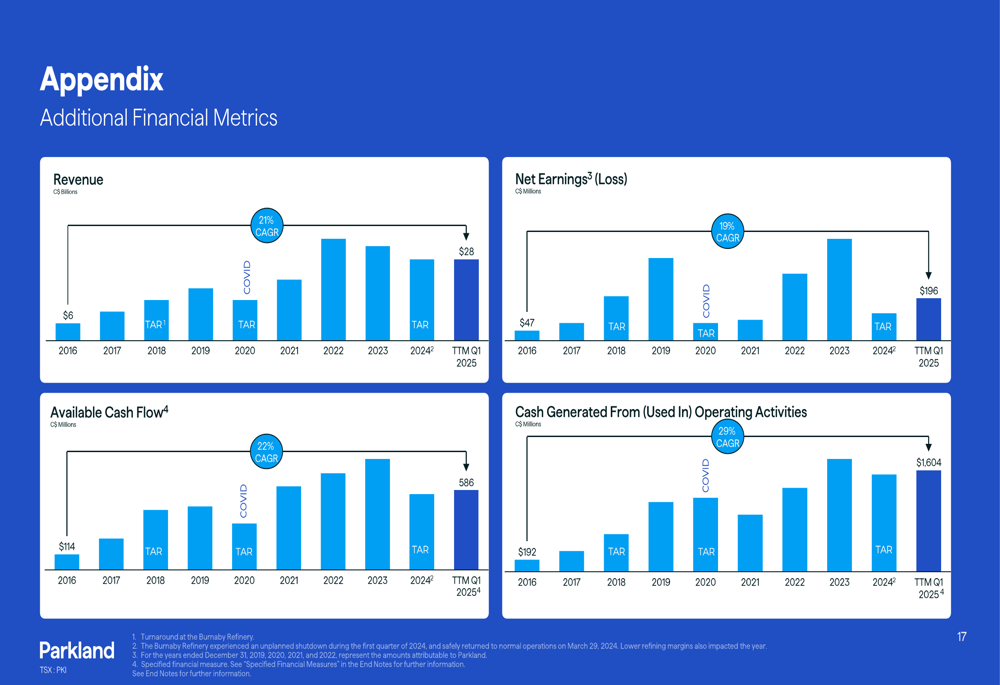

Additional financial metrics further illustrate Parkland’s expansion:

Strategic Growth Initiatives

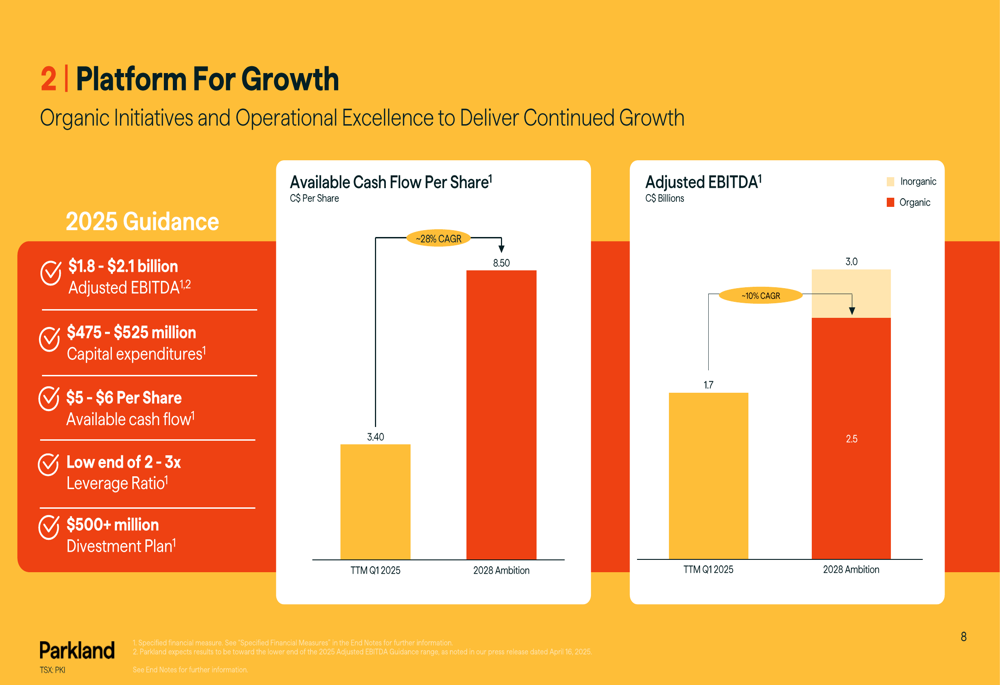

Parkland’s presentation outlined ambitious growth targets, with 2025 guidance projecting Adjusted EBITDA of $1.8-$2.1 billion and a longer-term ambition to reach $3.0 billion by 2028, representing a 10% CAGR from current levels. The company also expects available cash flow per share to grow from $3.40 (TTM Q1 2025) to $8.50 (2028 Ambition), an impressive 28% CAGR.

The company’s growth strategy is illustrated in this forward-looking projection:

To achieve these targets, Parkland is focusing on accretive organic initiatives across its retail, commercial, and supply segments. In retail, the company plans to expand its ON the RUN convenience store brand with enhanced food offerings and digital platforms. The commercial segment will focus on growing fuel volumes through multi-product offerings and expanding renewable business lines. Supply initiatives aim to leverage scale for purchasing power and optimize logistics capabilities.

Business Diversification

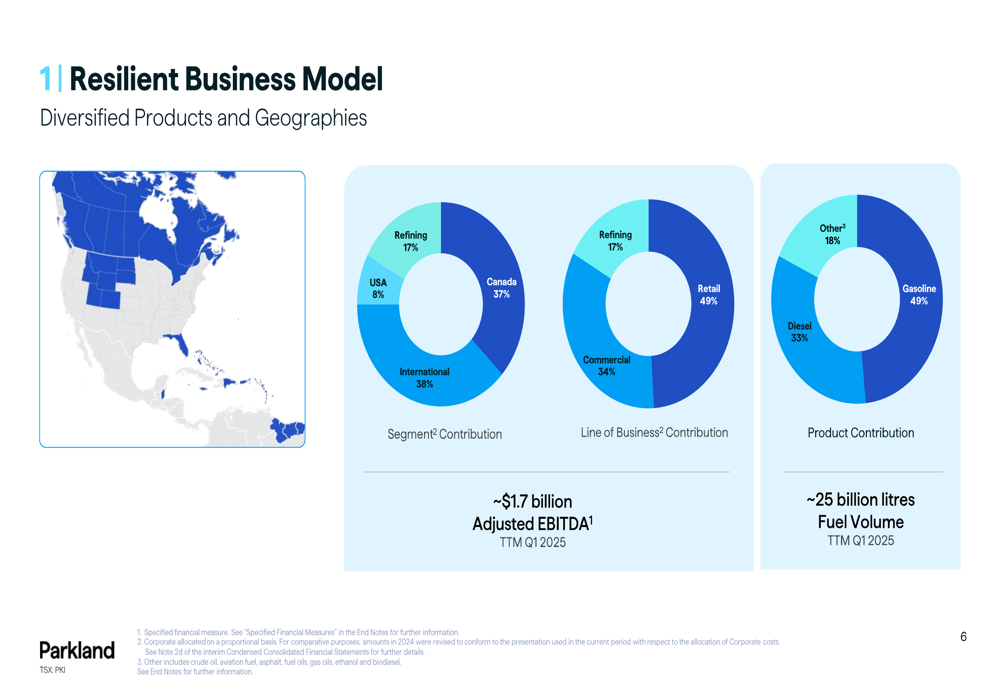

A key strength highlighted in Parkland’s presentation is its diversified business model, which provides resilience against market fluctuations. The company’s operations span Canada (37% of segment contribution), USA (8%), International (38%), and Refining (17%).

The following visualization demonstrates Parkland’s diversification across geographies and business segments:

This diversification extends to Parkland’s retail network, which includes 3,700 service stations across Canada (2,320), USA (645), and International markets (735). The company’s commercial operations encompass terminals, bulk plants, transloaders, marine/aviation facilities, and commercial cardlock sites.

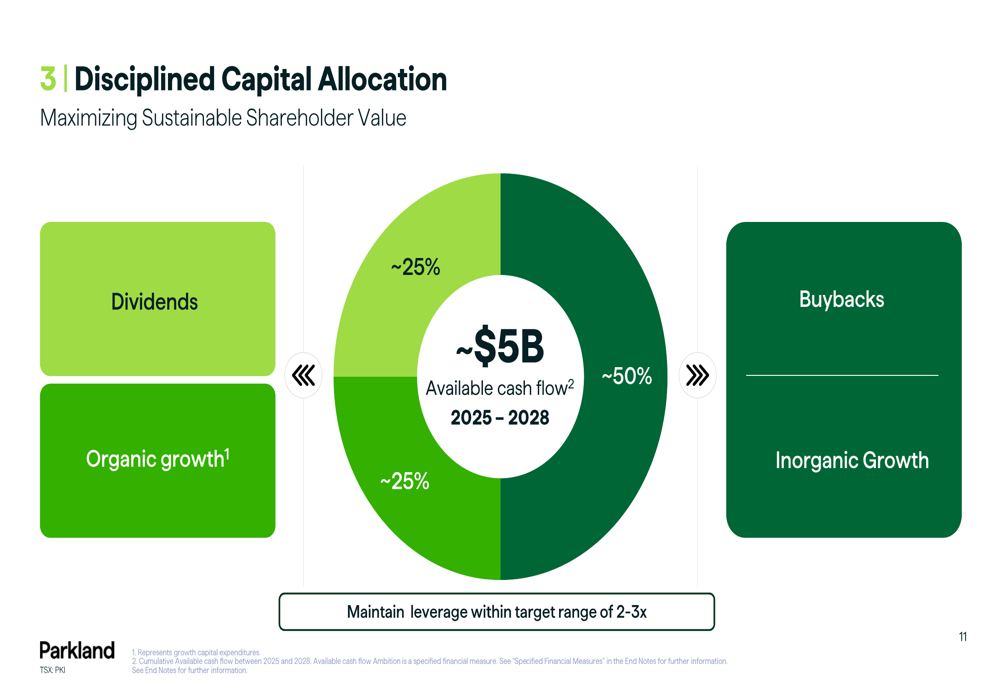

Capital Allocation Strategy

Parkland outlined a disciplined capital allocation strategy for 2025-2028, planning to distribute its projected $5 billion in available cash flow across dividends (~25%), organic growth (~25%), share buybacks (~50%), and inorganic growth (~50%).

The company’s capital allocation priorities are illustrated in this breakdown:

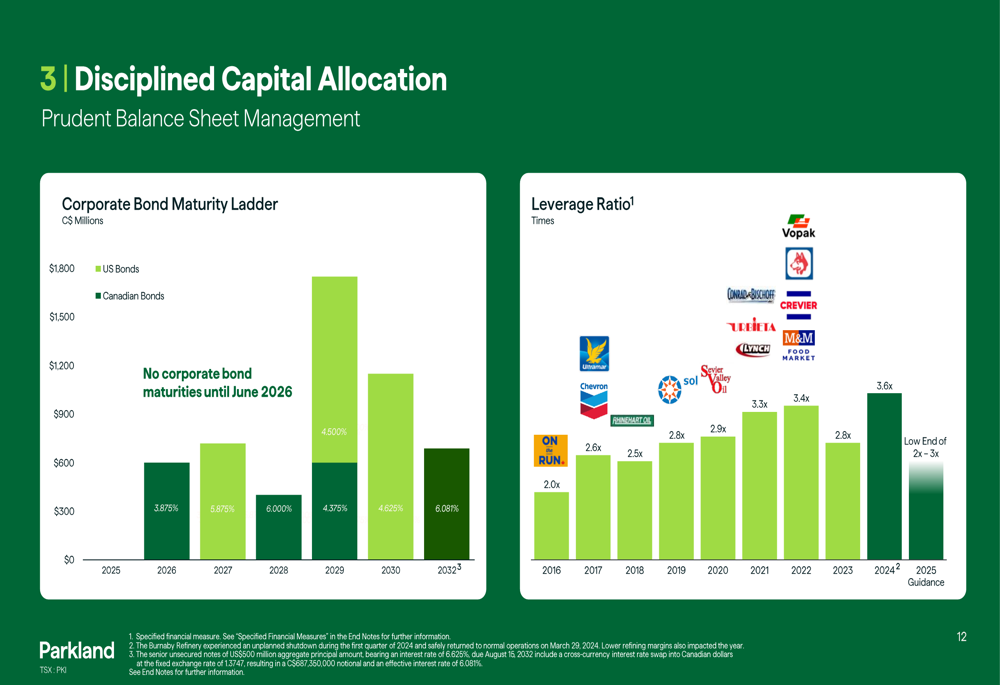

Balance sheet management remains a priority, with Parkland targeting a leverage ratio at the low end of its 2-3x range. This represents an improvement from the 3.6x leverage ratio reported in the Q4 2024 earnings. The company’s bond maturity ladder shows no maturities until June 2026, providing financial flexibility.

The following chart shows Parkland’s leverage ratio trend and bond maturity schedule:

Forward-Looking Statements & Challenges

While Parkland’s presentation paints an optimistic picture of future growth, the company faces several challenges. Recent earnings misses suggest potential headwinds in achieving the ambitious targets. The strategic review initiated on March 5, 2025, and a proposed acquisition announced on May 5, 2025 (details not disclosed in the presentation), indicate potential structural changes ahead.

The company’s divestment plan of $500+ million suggests a focus on portfolio optimization. Additionally, Parkland is investing in future energy transition through its ultra-fast EV charging network, with 58 sites already deployed in high EV adoption markets.

Parkland’s sustainability initiatives include goals to reduce Scope 1 and 2 GHG emissions by 40% per site by 2030 and help customers reduce emissions by 1 million tonnes, positioning the company for long-term resilience in a changing energy landscape.

In conclusion, Parkland’s investor presentation outlines an ambitious growth strategy despite recent performance challenges. The company’s diversified business model and disciplined capital allocation approach will be crucial in achieving its 2028 targets of $3 billion in Adjusted EBITDA and $8.50 in available cash flow per share. Investors will be watching closely to see if Parkland can overcome recent headwinds to deliver on these promises.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.