Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Petco Health and Wellness Company Inc (NASDAQ:WOOF) presented its second quarter 2025 earnings results on August 28, showing significant profitability improvements despite ongoing revenue challenges. The pet retailer’s stock closed at $3.20 and gained 0.97% in after-hours trading, reflecting cautious market optimism about the company’s strategic progress.

The company is navigating a challenging retail environment while executing a multi-phase transformation strategy that appears to be yielding results on the bottom line, even as top-line growth remains elusive. This quarter’s presentation highlighted Petco’s focus on strengthening retail fundamentals and improving operational efficiency.

Quarterly Performance Highlights

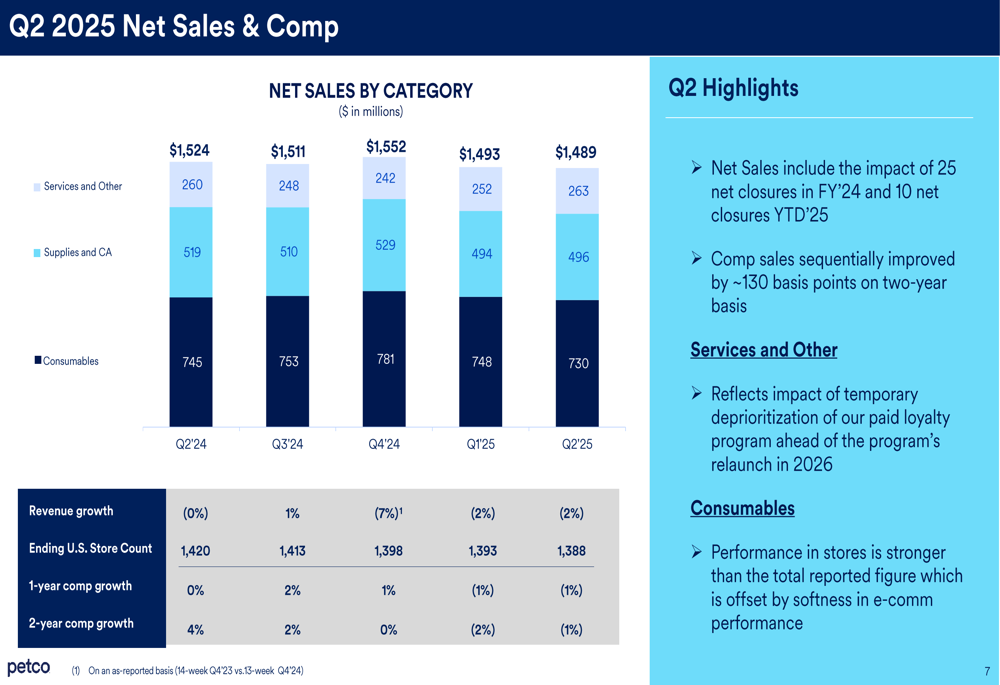

Petco reported total net sales of $1,489 million for Q2 2025, representing a 2% year-over-year decline. Comparable sales decreased 1% on both a one-year and two-year basis, though management noted a sequential improvement of approximately 130 basis points on a two-year basis.

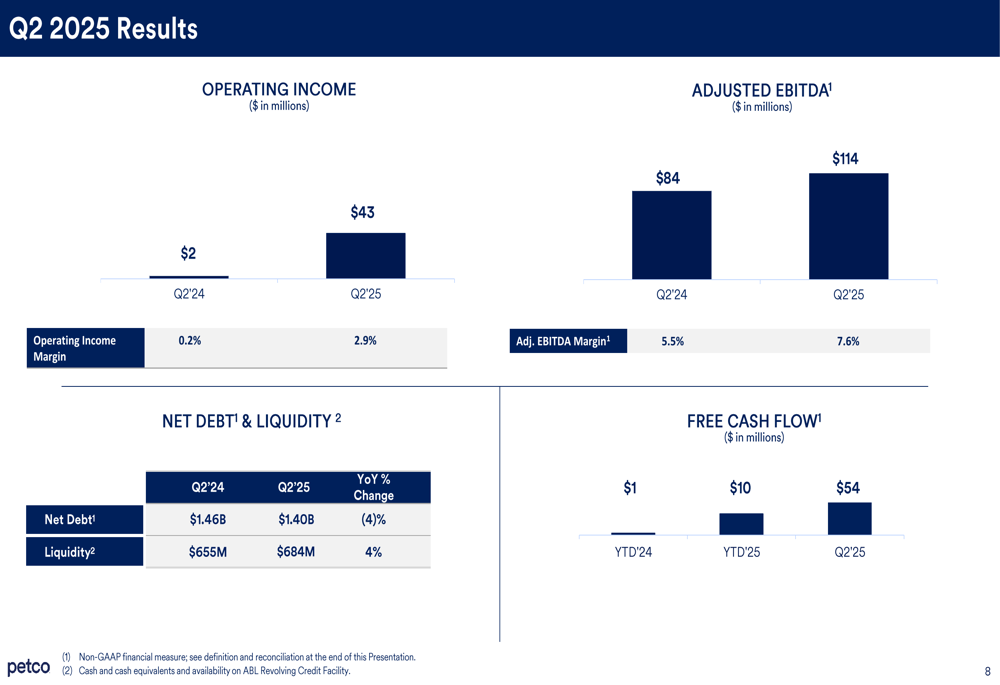

Despite the sales decline, Petco achieved substantial profitability gains. Operating income increased by approximately $41 million to $43 million (2.9% margin), while Adjusted EBITDA rose by approximately $30 million to $114 million (7.6% margin).

As shown in the following chart of quarterly net sales by category:

The sales mix remained relatively stable with Consumables contributing $730 million, Supplies and companion animals at $496 million, and Services and other generating $263 million. The company’s store count stood at 1,388 U.S. locations, reflecting 25 net closures in fiscal year 2024 and 10 net closures year-to-date in 2025.

Petco’s financial results demonstrate significant improvement in profitability metrics compared to previous quarters:

The company generated approximately $54 million in free cash flow during the quarter, while maintaining a net debt position of $1.40 billion and available liquidity of $684 million.

Strategic Initiatives

Petco outlined its three-phase strategic approach for 2025, which includes strengthening fundamentals, implementing and executing operational improvements, and returning to growth. The company indicated it is making progress on all fronts while preparing to shift focus to the growth phase.

A key component of Petco’s strategy to drive store traffic is its "WHERE THE PETS GO" marketing campaign, which includes various promotional events and in-store activities designed to enhance customer engagement and drive sales.

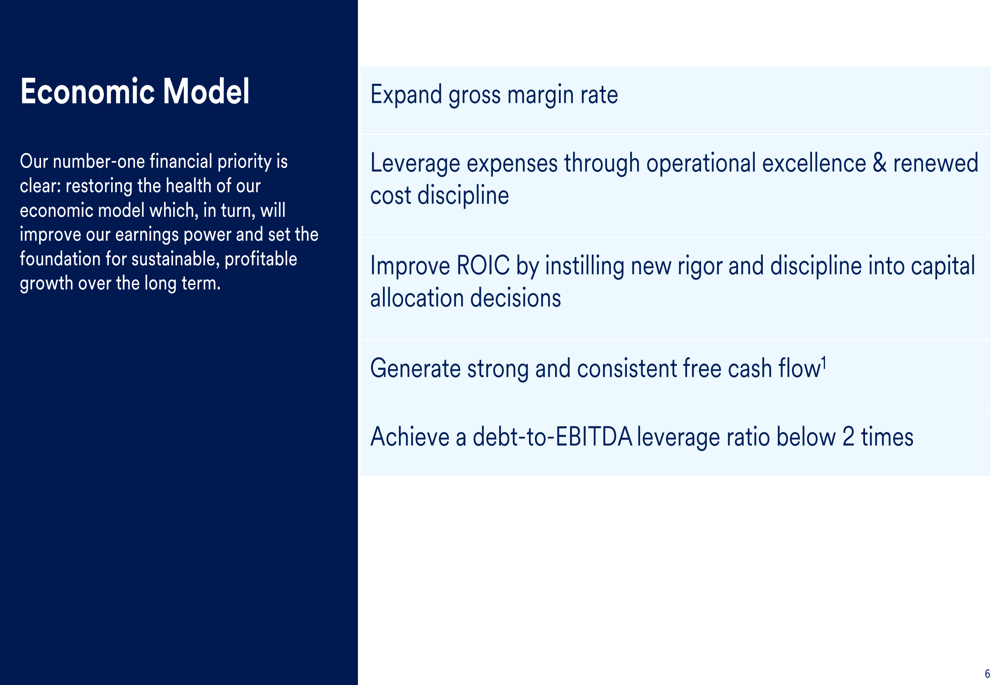

The company’s economic model prioritizes expanding gross margins, leveraging expenses through operational excellence, improving return on invested capital, generating strong free cash flow, and reducing debt. This disciplined approach appears to be yielding results, as evidenced by the significant profitability improvements in Q2.

Forward-Looking Statements

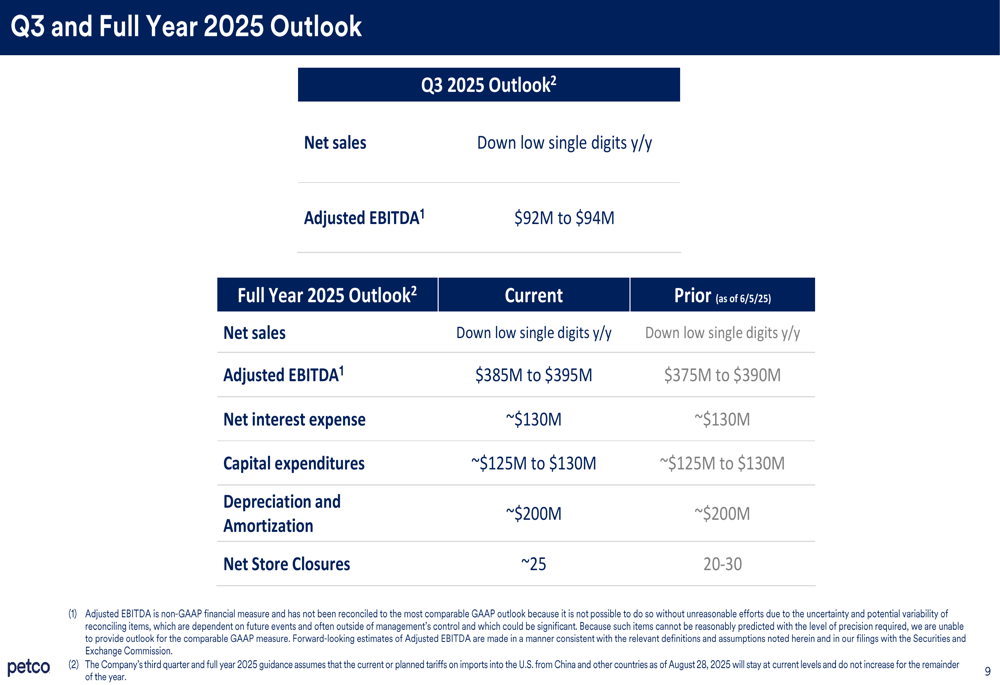

Petco provided guidance for both Q3 and full-year 2025, maintaining a cautious outlook on sales while expressing confidence in continued profitability improvements. For Q3, the company expects net sales to decline in the low single digits year-over-year, with Adjusted EBITDA projected between $92 million and $94 million.

For the full year 2025, Petco raised its Adjusted EBITDA guidance to a range of $385 million to $395 million, while projecting net sales to decline in the low single digits. The company also forecasts net interest expense of approximately $130 million, capital expenditures of $125-130 million, and depreciation and amortization of approximately $200 million.

Notably, this guidance incorporates expected tariff headwinds, indicating management’s confidence in their ability to offset these challenges through operational improvements and cost discipline.

Financial Analysis

Petco’s Q2 results represent a significant improvement from Q1 2025, when the company reported an EPS of -$0.04 and operating profit of $16.4 million. The substantial quarter-over-quarter increase in operating income and Adjusted EBITDA suggests that the company’s focus on margin expansion and cost discipline is gaining traction.

The company’s ability to generate $54 million in free cash flow is particularly noteworthy, as it provides financial flexibility to manage its $1.40 billion net debt position. This cash generation capability, combined with $684 million in available liquidity, should help Petco navigate ongoing challenges in the retail environment.

While the continued sales decline remains a concern, the sequential improvement in comparable sales on a two-year basis offers a glimmer of hope that the company’s strategic initiatives may eventually translate into top-line growth. Management’s raised earnings guidance despite acknowledged tariff headwinds further suggests confidence in their ability to execute on operational improvements.

As Petco transitions to the "Return to Growth" phase of its strategy, investors will be watching closely to see if the company can maintain its profitability momentum while reversing the sales decline trend in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.