Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Phibro Animal Health Corporation (NASDAQ:PAHC) presented its third-quarter fiscal 2025 results on May 8, showcasing exceptional performance across all business segments. The company’s stock surged 13% following the announcement, reaching $21.91, as investors responded positively to results that significantly exceeded analyst expectations.

The animal health company reported adjusted earnings per share of $0.63, beating the forecasted $0.53 by 19%, while revenue of $347.8 million outpaced expectations of $309.5 million by 12.4%. This strong performance comes amid continued integration of the Zoetis (NYSE:ZTS) MFA portfolio, which has substantially expanded Phibro’s market presence.

Quarterly Performance Highlights

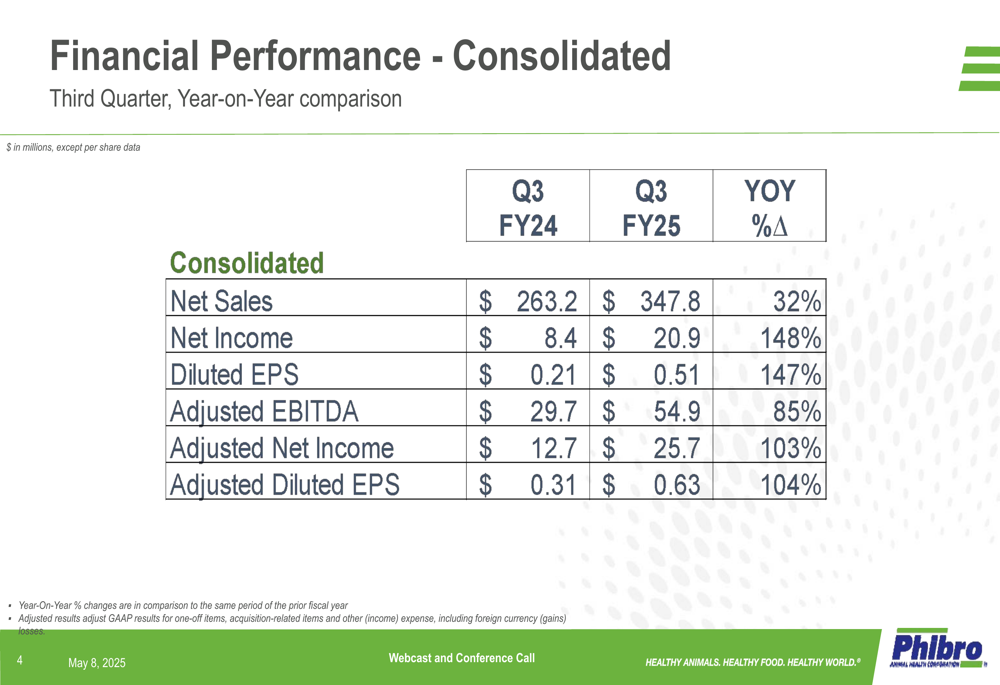

Phibro’s third quarter showed remarkable growth across all key financial metrics. The company achieved a 32% increase in consolidated net sales, rising from $263.2 million in Q3 FY2024 to $347.8 million in Q3 FY2025. Even more impressive was the 85% jump in adjusted EBITDA, which reached $54.9 million compared to $29.7 million in the prior year period.

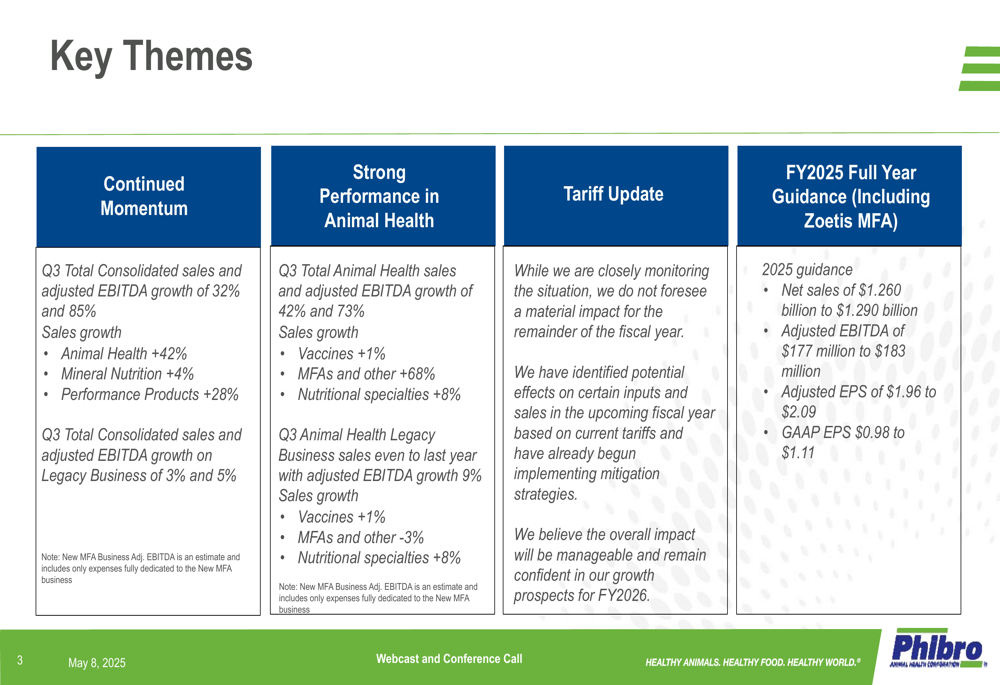

As shown in the following consolidated financial performance overview:

Net income more than doubled, increasing 148% to $20.9 million, while diluted EPS rose 147% to $0.51. On an adjusted basis, net income grew 103% to $25.7 million, with adjusted diluted EPS up 104% to $0.63.

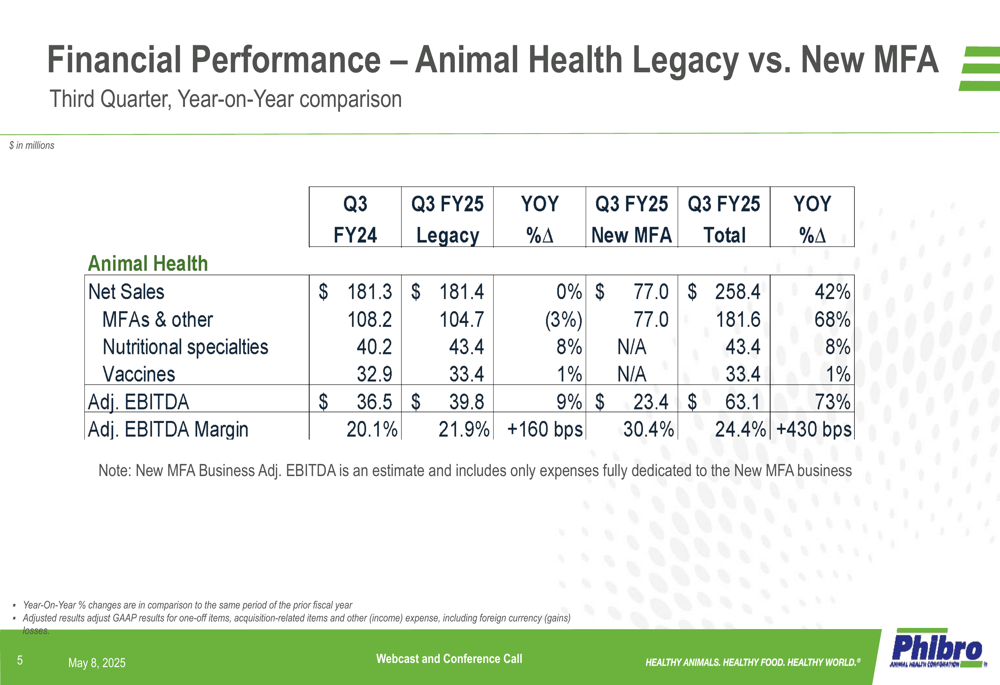

The Animal Health segment, Phibro’s largest business unit, led the company’s growth with a 42% sales increase. This segment’s performance was particularly noteworthy, with adjusted EBITDA surging 73% and margins expanding by 430 basis points to 24.4%.

The detailed breakdown of the Animal Health segment performance reveals the significant impact of the Zoetis MFA acquisition:

Detailed Financial Analysis

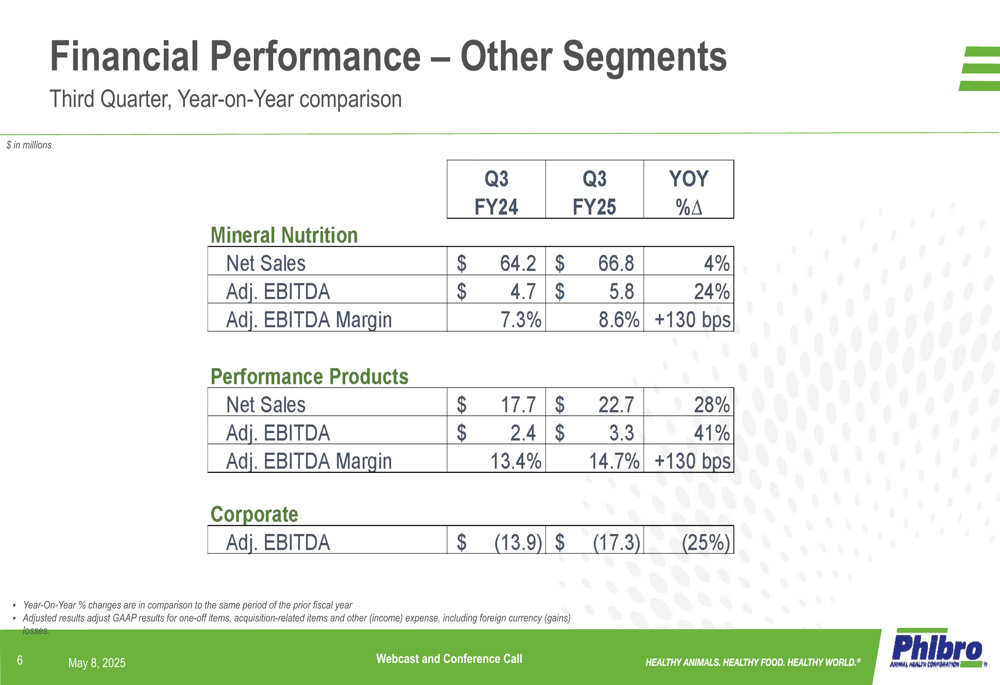

Beyond the Animal Health segment, Phibro’s other business units also delivered solid results. The Mineral Nutrition segment saw a 4% sales increase to $66.8 million, while its adjusted EBITDA grew 24% to $5.8 million, improving margins by 130 basis points to 8.6%. The Performance Products segment posted even stronger growth, with sales up 28% to $22.7 million and adjusted EBITDA increasing 41% to $3.3 million.

These segment performances are illustrated in the following financial breakdown:

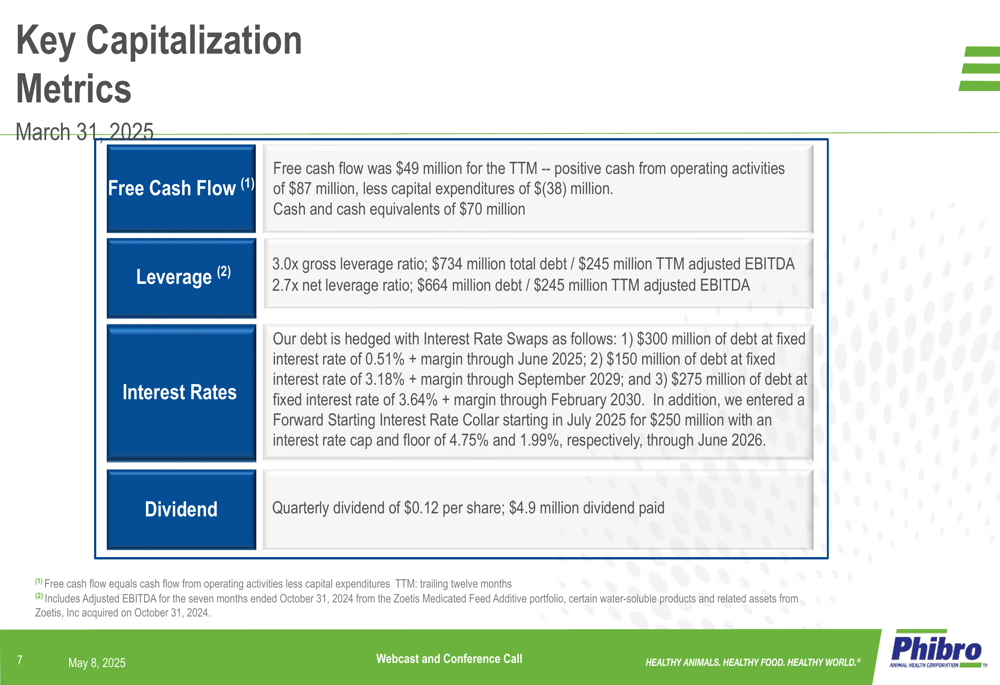

From a capital structure perspective, Phibro maintained a solid financial position despite its acquisition activities. The company generated $49 million in free cash flow for the trailing twelve months ended March 31, 2025, with $70 million in cash and cash equivalents on hand. The leverage ratio stands at 3.0x gross and 2.7x net, which management considers manageable given the company’s growth trajectory and cash generation capabilities.

The key capitalization metrics provide further insight into Phibro’s financial health:

Strategic Initiatives & Acquisitions

The integration of the Zoetis MFA portfolio has been a transformative strategic move for Phibro, significantly expanding its market reach and product offerings. This acquisition has been the primary driver behind the company’s exceptional growth in the MFAs & other category, which saw a 68% increase in sales.

During the earnings presentation, management highlighted that while they are closely monitoring potential tariff impacts, they do not anticipate any material effect for the remainder of fiscal year 2025. However, they acknowledged that some pressure might emerge in fiscal 2026, with analysts in the earnings call suggesting a potential 5-10% impact.

The company’s key strategic themes for the quarter demonstrate both the acquisition impact and organic growth:

Forward-Looking Statements

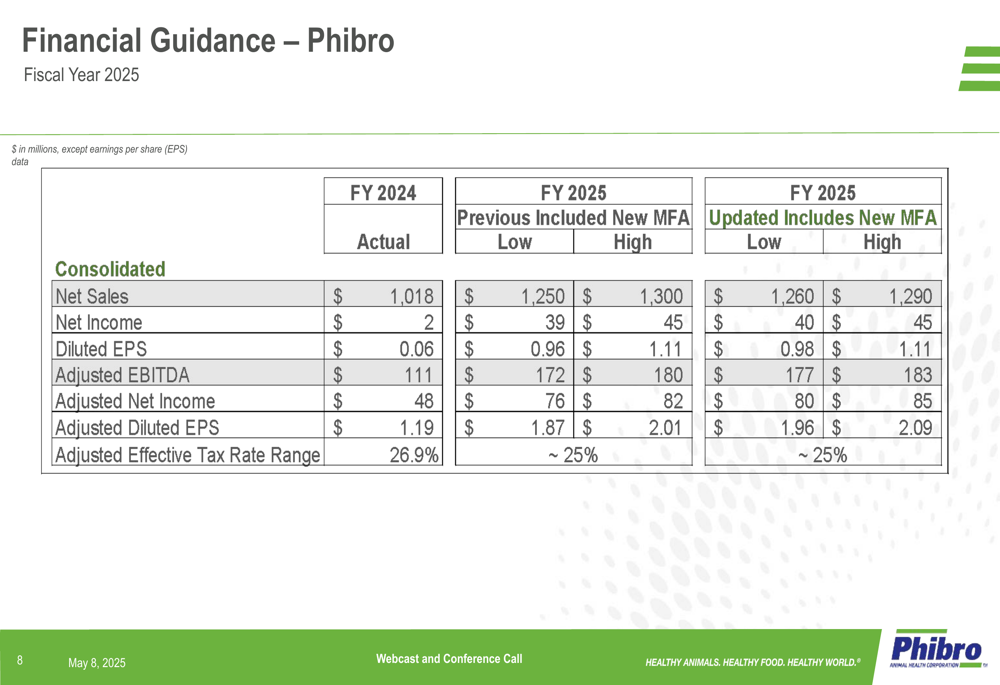

Based on the strong performance in the first three quarters, Phibro has raised its full-year guidance for fiscal 2025. The company now expects net sales between $1.260 billion and $1.290 billion, representing a 24-27% increase over fiscal 2024. Adjusted EBITDA is projected to reach $177-$183 million, up from the previous guidance of $172-$180 million.

Similarly, adjusted diluted EPS guidance has been raised to $1.96-$2.09, compared to the previous range of $1.87-$2.01. This updated outlook reflects management’s confidence in continued strong performance through the fiscal year’s final quarter.

The detailed financial guidance provides a comprehensive view of Phibro’s expectations:

CEO Jack Bantine expressed confidence during the earnings call, attributing the company’s performance to strategic investments in procurement and supply chain resilience. CFO Glenn David reinforced this sentiment, highlighting Phibro’s ability to drive strong income growth in the coming year.

With its stock trading near its 52-week high of $26.55, Phibro appears well-positioned to capitalize on its expanded product portfolio and market presence. However, investors should monitor potential challenges including future tariff pressures, ongoing supply chain dynamics, and competitive pressures in the animal health sector as the company continues its growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.