Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Introduction & Market Context

Philips (AMS:PHIA) reported its second quarter 2025 results on July 29, showing modest sales growth but significant margin improvement as the company continues to focus on operational efficiency and innovation-led growth. The healthcare technology giant achieved 1% comparable sales growth, driven primarily by its Personal Health segment, while order intake increased by 6% and the order book grew 7% year-on-year.

The company operates in a global healthcare market showing varied regional dynamics, with North America demonstrating solid demand driven by productivity and consolidation, Europe showing slight improvement, and Greater China exhibiting strong underlying demand despite regulatory challenges.

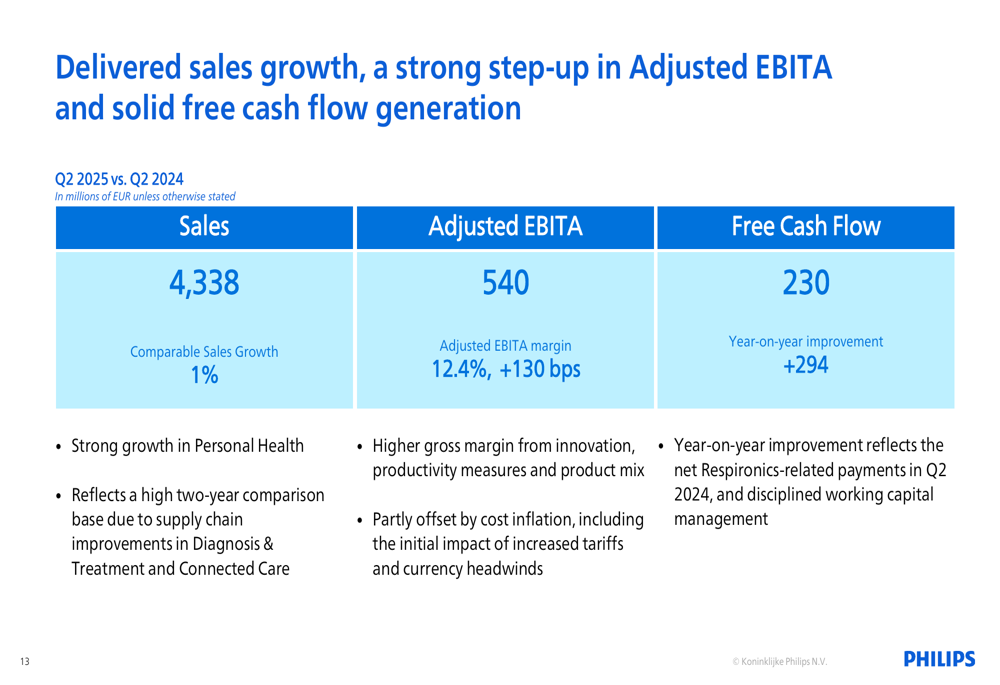

As shown in the following chart of key financial metrics, Philips delivered meaningful improvements in profitability despite modest top-line growth:

Quarterly Performance Highlights

Philips reported sales of €4,338 million in Q2 2025, representing 1% comparable growth year-on-year. The company’s adjusted EBITA reached €540 million with a margin of 12.4%, improving 130 basis points compared to Q2 2024. Free cash flow was €230 million, representing a substantial year-on-year improvement of €294 million.

Performance varied significantly across business segments. The Personal Health division was the standout performer with 6% comparable sales growth, while both the Diagnosis & Treatment and Connected Care segments experienced 1% sales declines but improved their profitability.

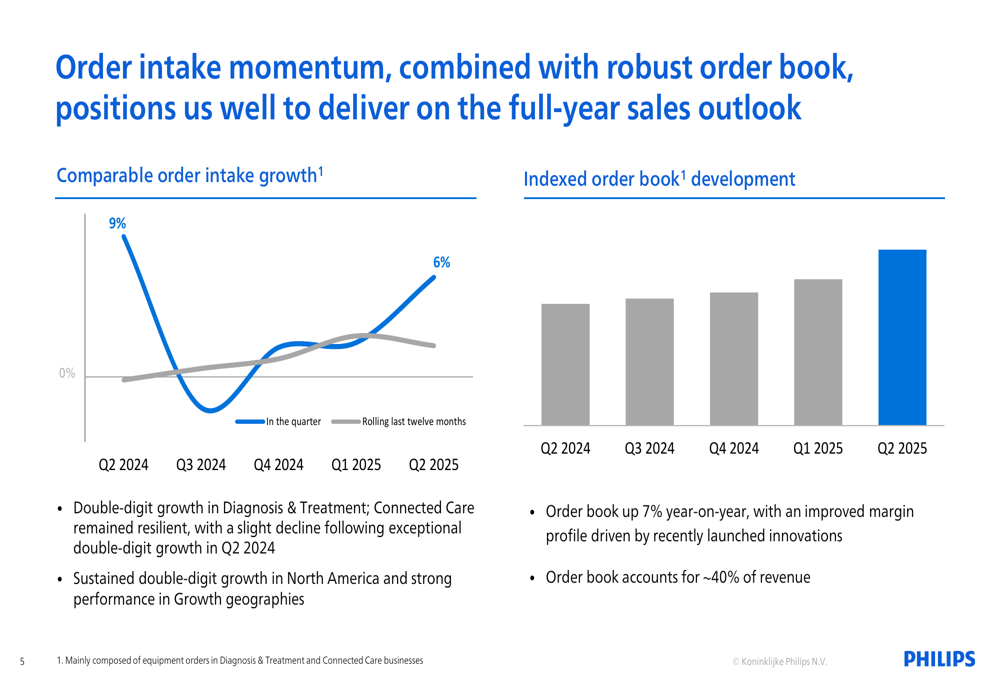

The company’s order intake momentum has been building throughout 2025, with Q2 showing 6% growth after a weak period in late 2024. This positive trend is visualized in the order intake and order book development chart:

Detailed Financial Analysis

Diagnosis & Treatment Segment

The Diagnosis & Treatment segment reported sales of €2,084 million in Q2 2025, down 1% on a comparable basis from €2,174 million in Q2 2024. Despite the sales decline, the segment improved its adjusted EBITA margin to 13.5%, up from 12.2% in the prior year. Income from operations increased to €226 million from €211 million.

The segment continues to focus on innovation, showcasing leading products including the Azurion platform for cardiac care, EPIQ and Affinity Ultrasound systems with over 20 AI tools, and the helium-free BlueSeal MR technology. These innovations are illustrated in the company’s presentation:

Connected Care Segment

Connected Care reported sales of €1,272 million in Q2 2025, down 1% on a comparable basis from €1,332 million in Q2 2024. Despite the sales decline, the segment improved its adjusted EBITA margin to 10.4% from 8.8% in the prior year. Income from operations decreased significantly to €67 million from €558 million, though this appears to be related to one-time factors.

The segment highlighted strategic partnerships with leading U.S. health systems, including Rush University System for Health, focusing on patient monitoring solutions that enhance clinical outcomes and productivity through automation and interoperability.

Personal Health Segment

Personal Health was the growth driver for Philips in Q2 2025, with sales of €862 million representing 6% comparable growth from €834 million in Q2 2024. However, the adjusted EBITA margin declined to 15.2% from 16.9% in the prior year. Income from operations slightly increased to €122 million from €120 million.

The segment’s growth was driven by innovation across multiple product lines, including the i9000 Shaver, OneBlade 360, IPL Lumea, AI-powered Avent baby monitors, and Sonicare oral healthcare products. The company noted strong underlying growth across most geographies for these consumer-focused products:

Strategic Initiatives

A key driver of Philips’ improved profitability has been its comprehensive productivity initiatives, which generated €197 million in savings during Q2 2025 alone. Since Q1 2023, these initiatives have delivered cumulative savings of €2,052 million. The savings come from multiple sources, including a simplified operating model (€40 million in Q2), procurement initiatives (€53 million), and other productivity measures (€104 million).

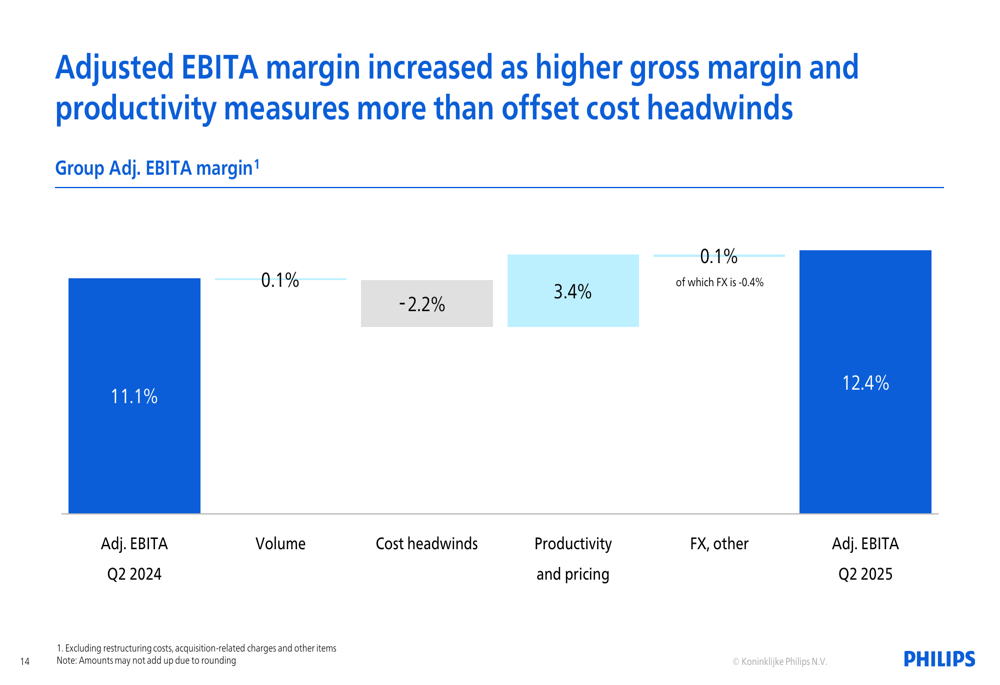

The company’s margin improvement can be attributed to several factors, as illustrated in the adjusted EBITA margin analysis:

Productivity and pricing contributed a substantial 3.4 percentage points to the margin improvement, which more than offset cost headwinds of 2.2 percentage points. This resulted in the overall margin expansion from 11.1% in Q2 2024 to 12.4% in Q2 2025.

Forward-Looking Statements

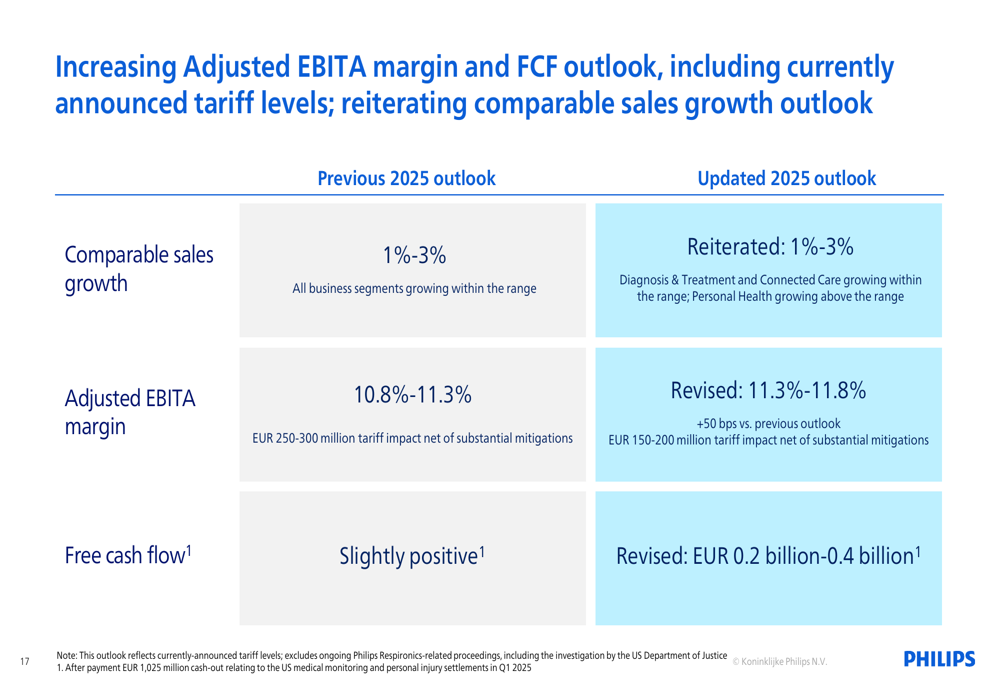

Philips has maintained its 2025 comparable sales growth outlook at 1-3%, but has increased its adjusted EBITA margin guidance by 50 basis points to 11.3-11.8%. The company also raised its free cash flow outlook from "slightly positive" to €0.2-0.4 billion, reflecting improved operational performance and working capital management.

The following chart details the company’s updated outlook for 2025:

The improved outlook comes despite an expected €150-200 million impact from tariffs, highlighting management’s confidence in the company’s operational improvements and growth trajectory.

Financial Position

As of June 30, 2025, Philips reported a total net debt position of €6.6 billion. The company recently issued €1 billion of bonds for repayment of existing debt and to finance eligible green projects. The average tenor of long-term debt is 6.2 years, with maturities extending to 2042.

Working capital management has shown improvement, with group working capital (excluding insurance receivable) at 11.9% in Q2 2025, down from 14.5% in Q2 2024. Similarly, group inventories as a percentage of LTM sales decreased to 18.1% from 17.8% in the same period last year.

Free cash flow reached €230 million in Q2 2025, a significant improvement from the negative €64 million reported in Q2 2024. This improvement reflects the company’s focus on operational efficiency and working capital optimization.

Executive Commentary

During the earnings call, CEO Roy Jakobs emphasized the company’s focus on margin expansion and strategic growth initiatives. "We are building on momentum and delivery today, with a clear focus on driving underlying margin expansion," Jakobs stated. He also highlighted the company’s trajectory towards mid-single-digit growth and mid-to-high-teens margins.

The company plans to hold a Capital Markets Day in February 2026 to outline its strategic vision for the future, which will likely build on the operational improvements and innovation-led growth strategy currently being implemented.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.