Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Phillips 66 (NYSE:PSX) presented its first quarter 2025 financial results on April 25, revealing a mixed performance with positive earnings but adjusted losses. The oil refining and midstream company reported earnings of $487 million while posting an adjusted loss of $368 million, highlighting the challenging market conditions in its refining and renewable fuels segments.

The company continues to execute its strategic transformation, focusing on its midstream business while rationalizing refining operations and maintaining shareholder returns despite headwinds.

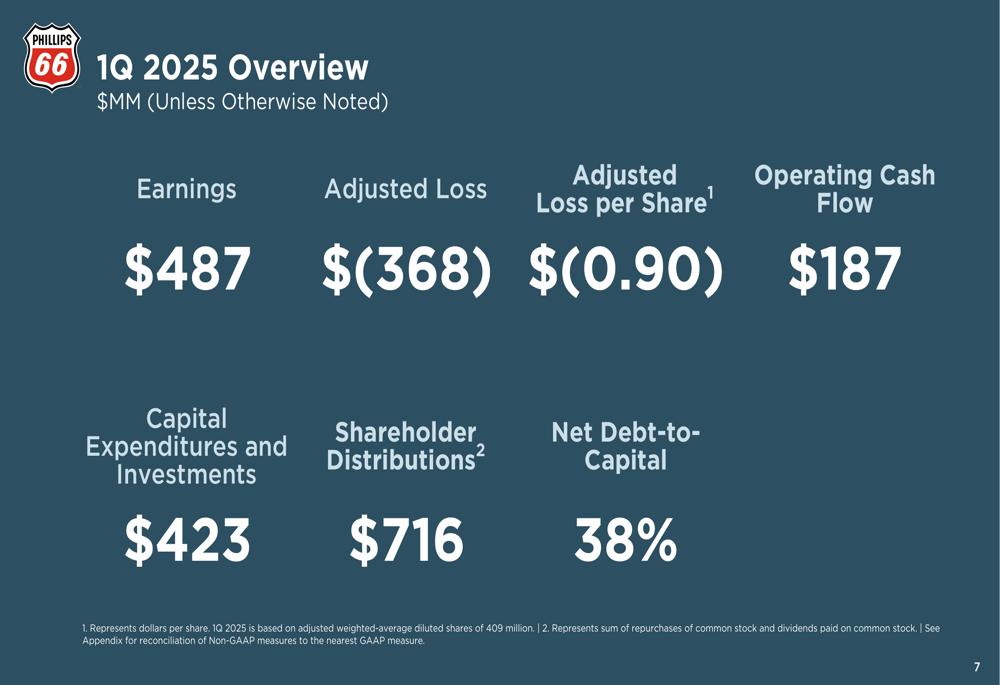

As shown in the following overview of Q1 2025 financial performance:

Quarterly Performance Highlights

Phillips 66 reported Q1 2025 earnings of $487 million, or $1.18 per share, while adjusted loss stood at $368 million, or $0.90 per share. Operating cash flow reached $187 million, with capital expenditures and investments totaling $423 million. The company maintained its commitment to shareholder returns, distributing $716 million to shareholders during the quarter.

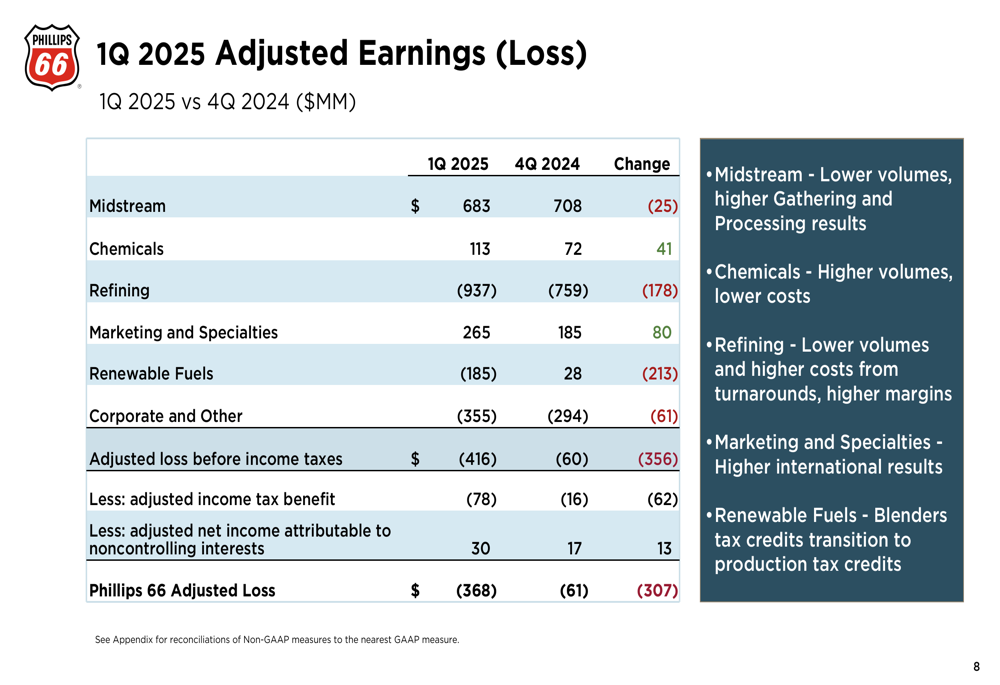

The breakdown of adjusted earnings by segment reveals significant variances in performance across the company’s business lines, with refining and renewable fuels facing substantial challenges while chemicals and marketing showed improvement:

Midstream remained the strongest performer with $683 million in adjusted earnings, though slightly down from $708 million in Q4 2024. The chemicals segment improved to $113 million from $72 million in the previous quarter, while marketing and specialties rose to $265 million from $185 million.

The refining segment’s challenges deepened with an adjusted pre-tax loss of $937 million, compared to a $759 million loss in Q4 2024. Most concerning was the renewable fuels segment, which swung from a $28 million profit to a $185 million loss, primarily due to the transition from blenders tax credits to production tax credits.

Segment Analysis

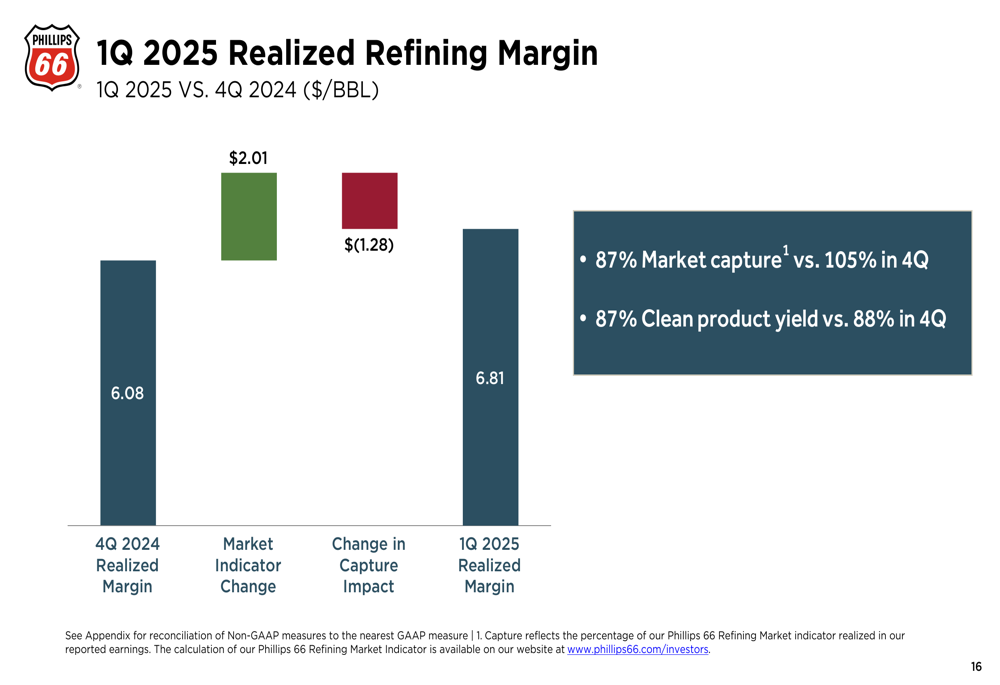

The refining segment continued to face significant headwinds, with crude utilization at 80%, clean product yield at 87%, and market capture at 87%. Regional performance varied considerably, with the West Coast and Central Corridor showing improvement while the Gulf Coast and Atlantic Basin/Europe regions deteriorated.

The realized refining margin increased to $6.81 per barrel from $6.08 in Q4 2024, benefiting from improved market indicators but offset by lower capture rates:

The company attributed the lower capture rate to seasonally reduced butane blending and the impacts of turnaround activity during the quarter. Despite these challenges, Phillips 66 completed the Sweeny Crude Flex (NASDAQ:FLEX) Project during a Q1 turnaround, which is expected to provide additional heavy/light switching capability of approximately 40 MBD and improve market capture by about 0.3%.

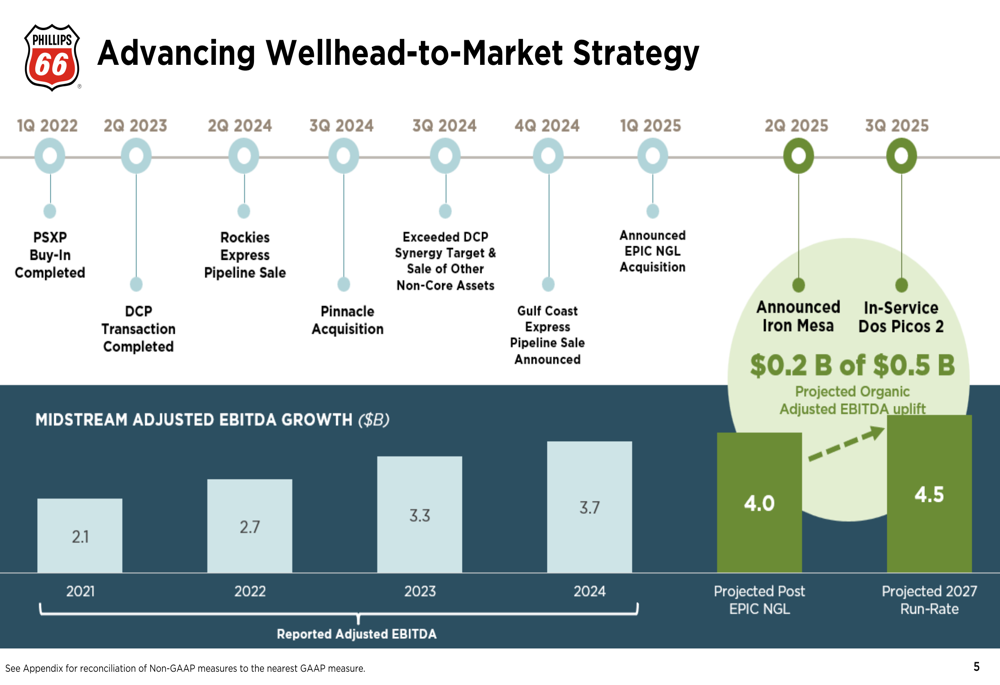

The midstream segment continues to be the cornerstone of Phillips 66’s strategy, with a clear progression in its wellhead-to-market approach:

Midstream adjusted EBITDA has shown consistent growth from $2.1 billion in 2021 to $3.7 billion in 2024, with projections reaching $4.0 billion post-EPIC NGL acquisition and $4.5 billion by 2027. This growth trajectory underscores the company’s strategic shift toward midstream operations.

Strategic Initiatives & Portfolio Changes

Phillips 66 has undertaken significant portfolio reshaping over the past three years, including strategic acquisitions, refinery rationalizations, and non-core asset divestitures. The company has returned over $14 billion to shareholders since July 2022 while completing $3.5 billion in asset sales.

Key strategic initiatives include the completed conversion of the San Francisco Refinery, announced cessation of operations at the Los Angeles Refinery, and expansion of the NGL value chain through Pinnacle and EPIC acquisitions. The company has also focused on reducing refining costs while improving utilization and clean product yield.

Looking ahead, Phillips 66 has established clear strategic priorities for 2027:

These priorities include achieving world-class operations with refining annual adjusted controllable costs of approximately $5.50 per barrel, disciplined growth with $2.0 billion per year in organic capital spending, and returning more than 50% of net cash flow from operations to shareholders.

Financial Position & Capital Allocation

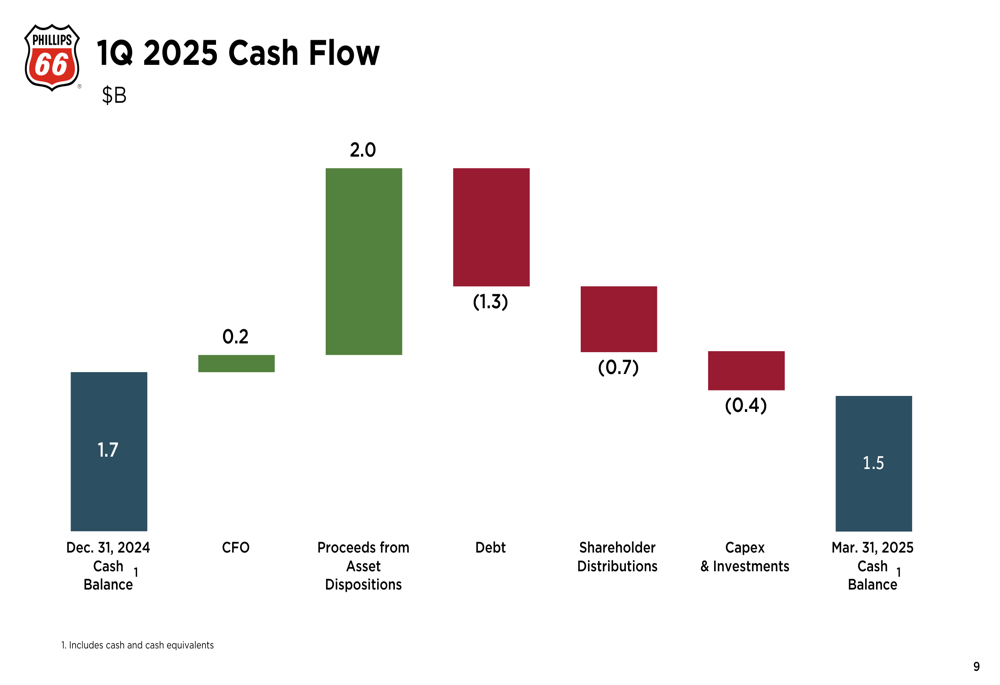

Phillips 66’s cash flow for Q1 2025 reflects both operational challenges and strategic execution:

The company started the quarter with $1.7 billion in cash, generated $0.2 billion from operations, and received $2.0 billion from asset dispositions. After debt reduction of $1.3 billion, shareholder distributions of $0.7 billion, and capital expenditures of $0.4 billion, the ending cash balance stood at $1.5 billion.

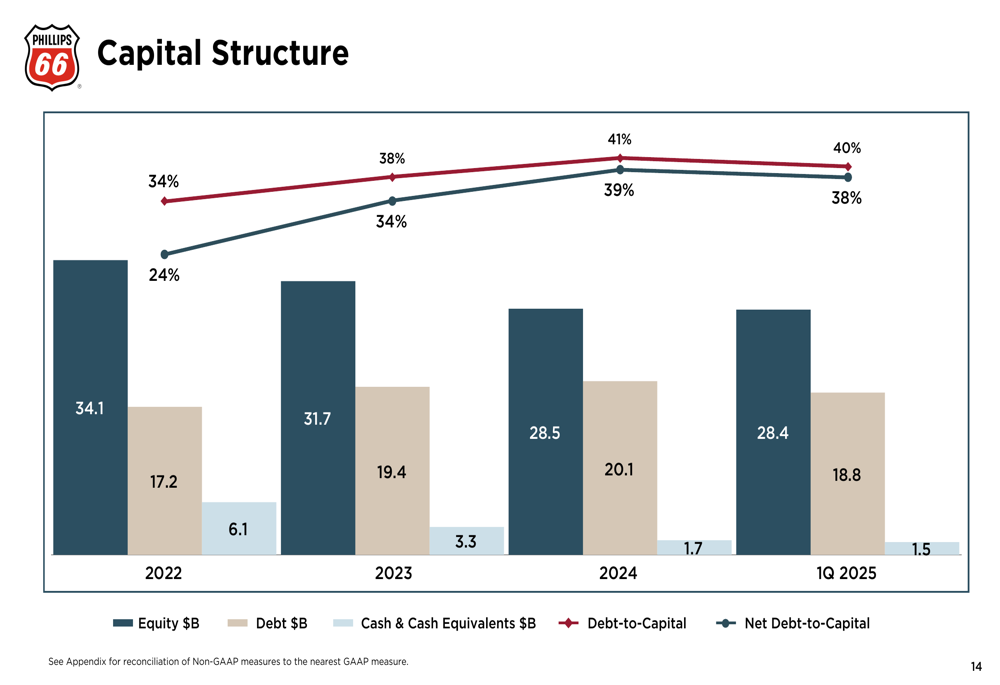

The company’s capital structure has evolved significantly since 2022, with equity declining from $34.1 billion to $28.4 billion, while debt has increased from $17.2 billion to $18.8 billion:

This has resulted in a net debt-to-capital ratio of 38% in Q1 2025, up from 24% in 2022 but slightly improved from 39% at the end of 2024. The company’s 2027 strategic priorities include reducing this ratio to below 30% with a target total debt of $17 billion.

Forward-Looking Statements

For Q2 2025, Phillips 66 expects refining crude utilization and global olefins & polyolefins utilization to be in the mid-90% range. Refining turnaround expenses are projected at $65-75 million, with corporate and other costs estimated at $340-360 million.

The company’s long-term strategy focuses on creating value through three key pillars:

These pillars include leveraging a differentiated portfolio in highly attractive markets, implementing a transformational strategy driving clear operational and commercial benefits, and delivering consistent and compelling value for shareholders.

Phillips 66 remains committed to its strategic transformation despite near-term challenges in refining and renewable fuels. With strong midstream performance, ongoing portfolio optimization, and disciplined capital allocation, the company aims to strengthen its competitive position while continuing to return value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.