Trump to appeal tariff ruling, warns of economic consequences

Introduction & Market Context

Photocure ASA (OB:PHO), the self-described "bladder cancer company," presented its second quarter 2025 results on July 30, showcasing record revenue performance and strategic growth initiatives. The company’s stock closed at NOK 61.6 the day prior to the presentation, down slightly by 0.32%, and has been trading in a 52-week range of NOK 47.0 to NOK 66.7.

The presentation comes after a challenging first quarter where Photocure missed revenue forecasts, leading to a 4.58% stock decline. However, Q2 results indicate a significant rebound with all-time high product revenue, suggesting the company has successfully navigated earlier headwinds.

Quarterly Performance Highlights

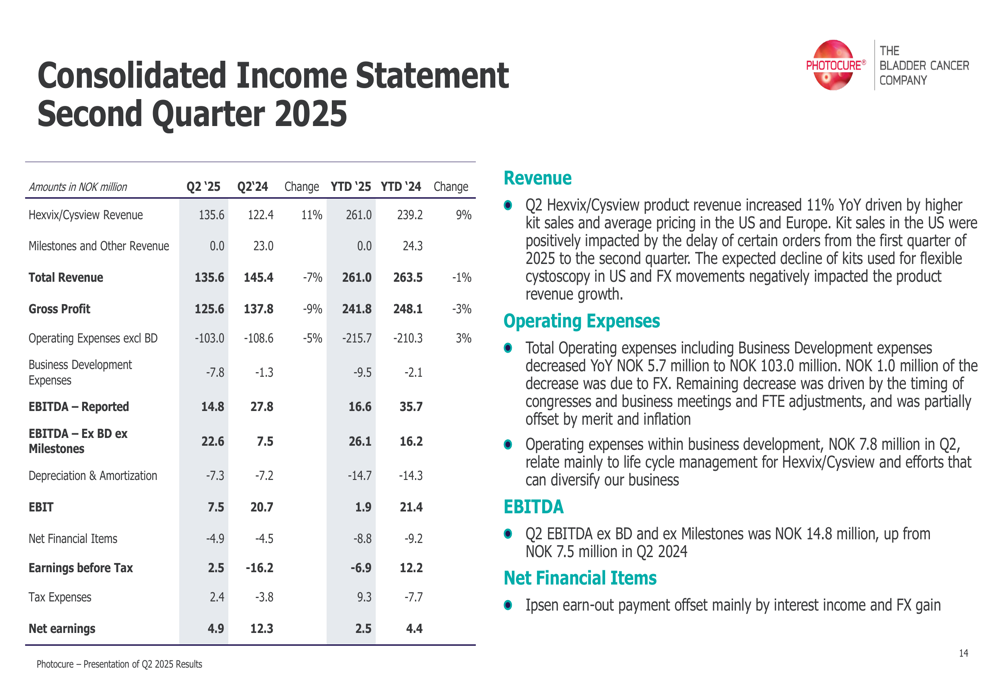

Photocure reported product revenue of NOK 135.6 million in Q2 2025, representing an 11% year-over-year increase and marking an all-time high for the company. This performance demonstrates a substantial improvement from Q1 2025, when the company reported a revenue miss against forecasts.

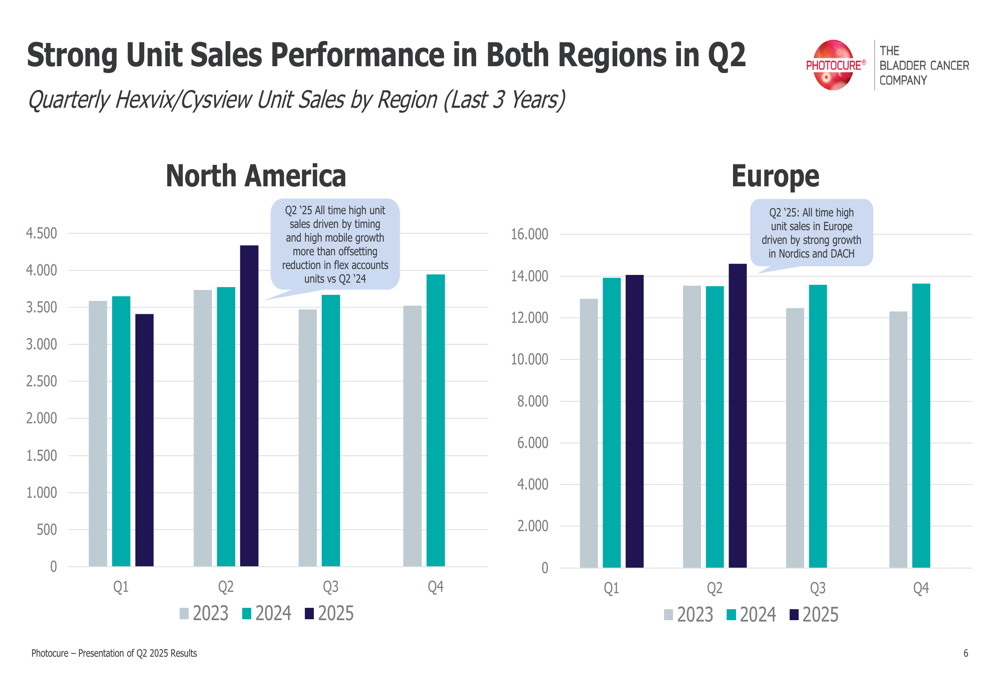

Regional performance showed strong growth across markets, with North America revenue increasing 14% and unit sales up 15% year-over-year. European operations delivered 8% growth in both revenue and unit sales, with particularly strong performance in the Nordic (11% growth) and DACH (8% growth) regions.

As shown in the following chart of unit sales performance across regions:

The company’s U.S. market presence continues to expand significantly, with active accounts growing approximately 24% year-over-year to reach 359 in Q2 2025. This growth trajectory is clearly illustrated in the following chart showing the consistent upward trend in U.S. accounts actively using Cysview:

Detailed Financial Analysis

Photocure reported EBITDA of NOK 14.8 million for Q2 2025, or NOK 22.6 million when excluding business development and milestone expenses. This represents the company’s continued focus on improving operating leverage while investing in growth opportunities.

The consolidated income statement reveals the company’s financial performance across key metrics:

Segment performance showed notable differences between regions. North America delivered a contribution of NOK 9.2 million, more than doubling the contribution margin versus Q2 2024, despite continued challenges in the flexible cystoscopy segment. European operations generated a contribution of NOK 42.0 million, representing 54% of regional revenue.

The segment breakdown provides further insight into regional performance dynamics:

Photocure maintained a strong balance sheet with NOK 239.1 million in cash and equivalents at the end of Q2, having completed a share buy-back program of 500,000 shares. The company carries no term debt, providing financial flexibility for continued investments in growth initiatives.

Strategic Initiatives

Photocure outlined several key strategic initiatives aimed at driving continued growth and market expansion. The company is accelerating Blue Light Cystoscopy (BLC) adoption through its mobile capability partnership with ForTec in the U.S., which has already gained traction with 70 accounts and over 100 medical doctors using the service since its launch in mid-2024.

The company’s growth strategy is illustrated in this detailed breakdown:

In Europe, Photocure has executed on its expansion plans with 36 Olympus BLC Visera Elite-III systems installed since launch in Q1 2025. The company also initiated commercial operations in Spain in June, building collaborations with three major BLC equipment suppliers.

European market developments are highlighted in the following summary:

A significant strategic partnership with Richard Wolf aims to develop and commercialize a next-generation 4K LED HD reusable flexible blue light cystoscope, addressing the global surveillance market with an estimated total addressable market of $1.3 billion. This initiative is particularly important given the 71% decline in flexible cystoscopy kit sales in the U.S. reported in Q1 2025.

Forward-Looking Statements

Photocure maintained its financial guidance for 2025, projecting 7-11% product revenue growth and year-over-year EBITDA improvement. The company continues to focus on increasing Hexvix/Cysview kit throughput and tower upgrades while collaborating with ForTec on the mobile tower national rollout in the U.S.

The company’s partnership with Asieris represents another growth avenue, with Hexvix receiving market authorization in China on November 5, 2024, ahead of schedule. Regulatory approval for BL equipment in China is still pending, after which commercialization can begin.

The comprehensive summary of Q2 2025 results provides a clear overview of the company’s current position and outlook:

Photocure anticipates minimal impact from potential pharmaceutical tariffs in the U.S. due to its high gross margin, addressing a concern that was raised during the Q1 earnings call. The company remains focused on advancing its partnership with Richard Wolf to develop and commercialize a next-generation flexible BLC system for global markets as soon as possible, which could help address the decline in flexible cystoscopy kit sales.

With continued investment in growth initiatives balanced against improving operating leverage, Photocure appears positioned to maintain its momentum through the remainder of 2025, building on the record revenue performance achieved in Q2.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.