Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

Introduction & Market Context

PKO Bank Polski (PKO), Poland’s largest bank, reported strong financial results for the first quarter of 2025, demonstrating resilience in a challenging economic environment. The bank achieved a net profit of 2.5 billion PLN, representing a 20.8% increase year-over-year, despite setting aside nearly 1 billion PLN for Swiss franc mortgage legal provisions.

The results come amid what the bank describes as "favorable economic prospects despite high global uncertainty," with Poland’s economic expansion primarily supported by robust domestic consumption and rising investment activity. According to the presentation, Poland is among the countries least vulnerable to potential adverse effects of U.S. policies, thanks to its limited exposure to the U.S. market and well-diversified export structure.

Quarterly Performance Highlights

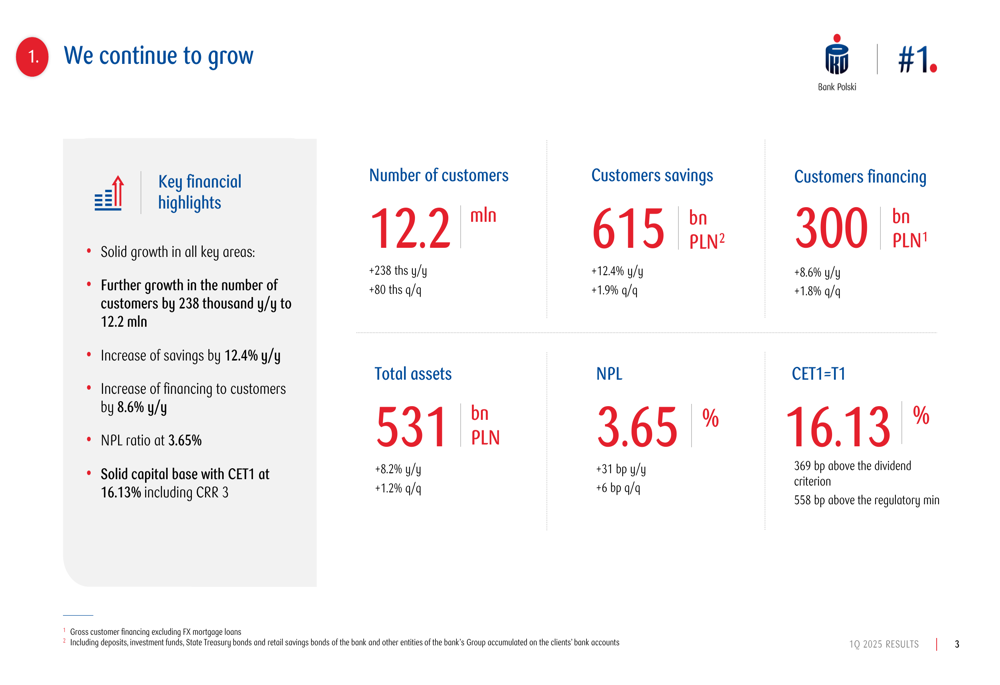

PKO Bank Polski reported impressive growth across key metrics in Q1 2025. Net profit reached 2.5 billion PLN, marking a 20.8% increase year-over-year and a 0.9% increase quarter-over-quarter. This represents the third consecutive quarter with net profit at this level, an achievement the bank highlighted in its presentation.

As shown in the following key financial highlights, the bank continued to expand its customer base and business volumes:

The bank’s return on equity (ROE) stood at 18.6%, up 0.9 percentage points year-over-year, while maintaining a solid capital position with a CET1 ratio of 16.13%, which is 369 basis points above the dividend criterion. The net interest margin remained stable at 4.95%, while the cost-to-income ratio was 33.3%.

PKO Bank Polski demonstrated strong risk management capabilities, with the cost of risk decreasing to 31 basis points, down 16 basis points year-over-year and 13 basis points quarter-over-quarter. This improvement reflects the lack of pressure on asset quality, as explained in the presentation.

The following chart illustrates the bank’s profitability and efficiency metrics:

Detailed Financial Analysis

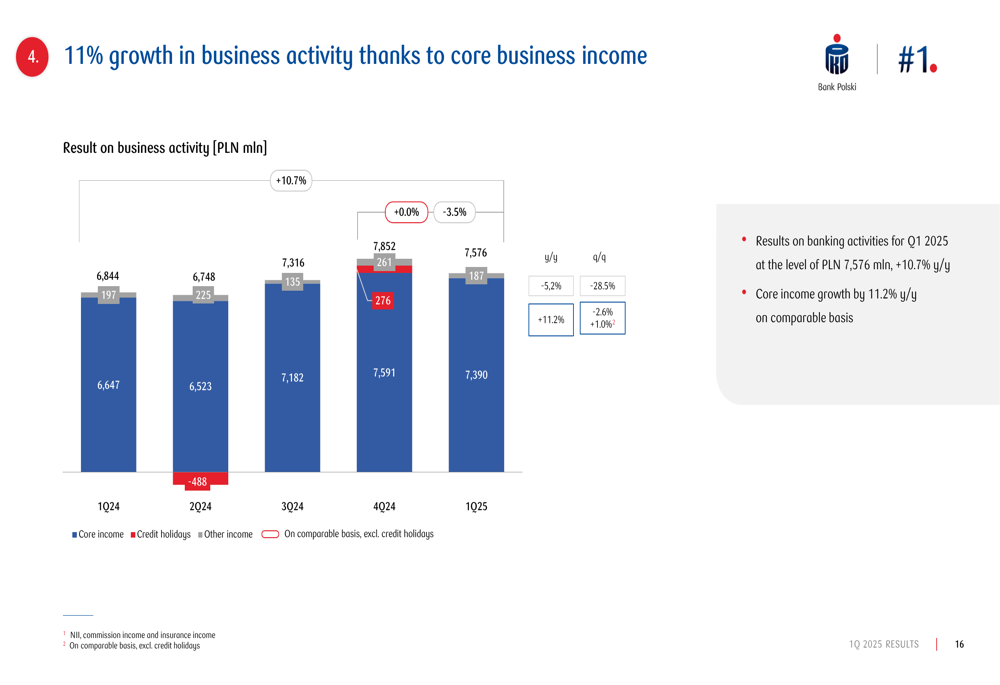

The bank’s core income grew by 11.2% year-over-year, driven primarily by a 15.2% increase in net interest income. This growth resulted from both increased business volumes and an improved interest margin compared to the previous year.

As illustrated in the following chart, the bank’s business activity showed consistent growth:

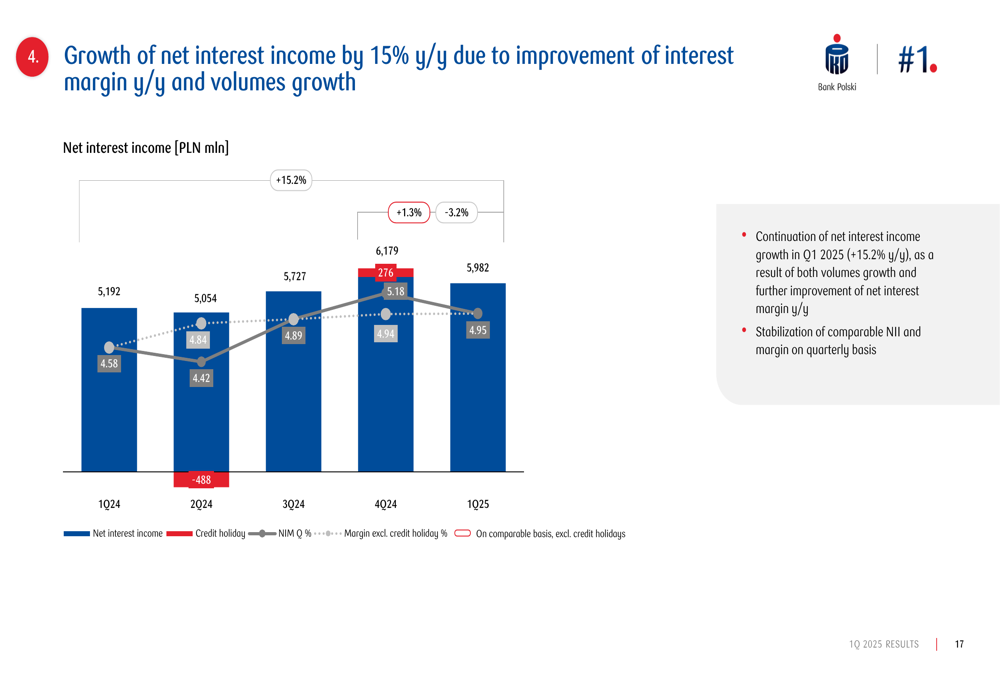

Net interest income, which represents the largest component of the bank’s revenue, continued its upward trajectory with a 15.2% year-over-year increase. This growth outpaced that of competitors, with the presentation noting that the top 4 competing banks averaged only 6% growth in this metric.

The following chart shows the trend in net interest income:

Fee and commission income decreased slightly by 2.0% year-over-year, primarily due to what the bank described as a "high base effect" from card income in Q1 2024. However, this was partially offset by a 17.4% year-over-year increase in income from mutual funds and brokerage activities.

The bank’s total costs increased by 15.7% year-over-year, reflecting higher personnel costs and economic price pressures. Despite this increase, PKO maintained a competitive cost-to-income ratio of 33.3%, although this was impacted by seasonally high Bank Guarantee Fund (BGF) costs.

Competitive Industry Position

PKO Bank Polski emphasized its market leadership throughout the presentation, consistently referring to itself as "#1 Bank Polski." The bank maintained or expanded its market share across key segments, including consumer loans (19.8%, +0.4 percentage points quarter-over-quarter), PLN mortgage loans (26.1%, +0.2 percentage points quarter-over-quarter), and loans for entrepreneurs (14.1%, +0.1 percentage points quarter-over-quarter).

The following chart highlights the bank’s market leadership position:

In corporate financing, PKO Bank Polski reported 6.1% year-over-year growth, reaching 106.8 billion PLN. The bank also highlighted its role in leading major transactions in the Polish economy, including several syndicated loans and green financing initiatives.

Retail lending showed double-digit growth, with the bank maintaining its strong market position. Retail deposits increased by 5.2% to 340.9 billion PLN, while assets under management in mutual funds grew by an impressive 38%.

Strategic Initiatives

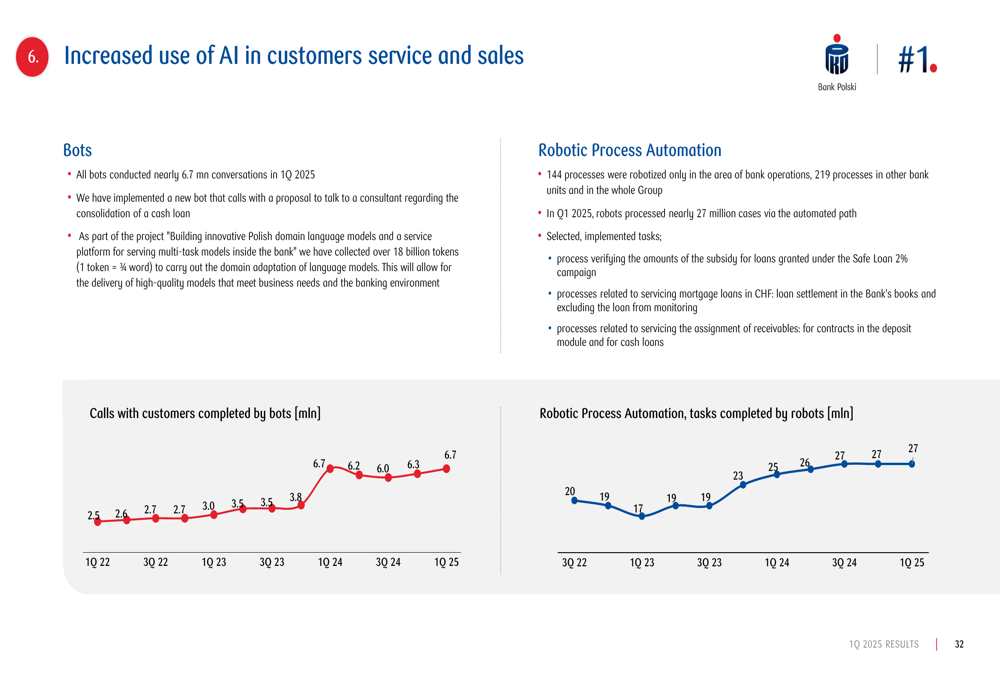

PKO Bank Polski continued to invest in digital innovation, with a particular focus on artificial intelligence and mobile banking. The bank reported increased use of AI in customer service and sales, with millions of customer calls handled by bots and millions of tasks completed through robotic process automation.

As shown in the following chart, the bank has significantly expanded its use of AI technologies:

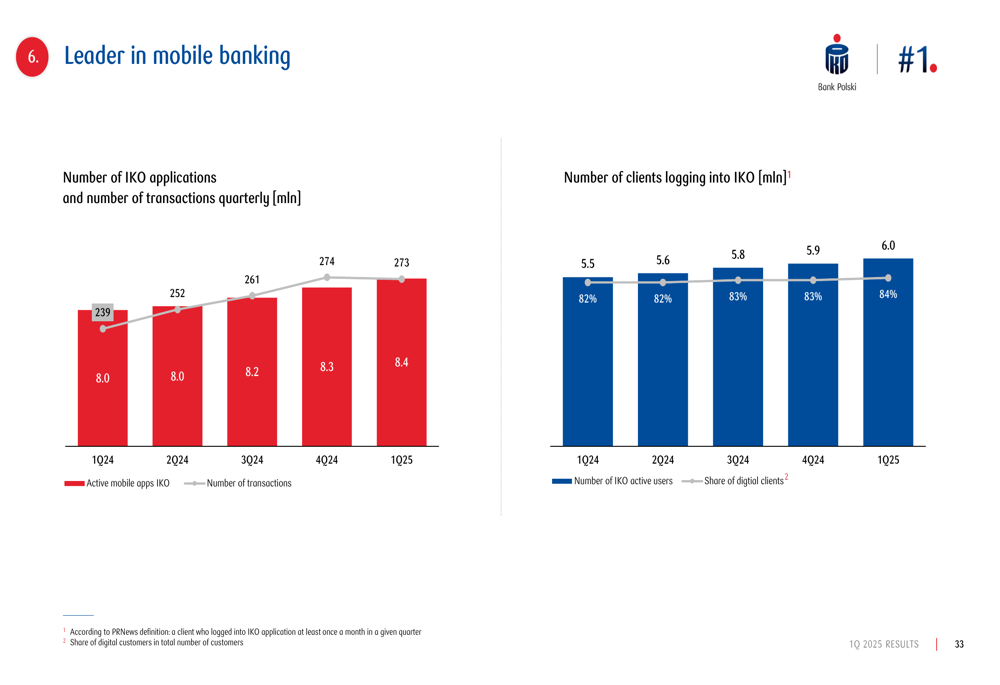

The bank also maintained its leadership position in mobile banking through its IKO application. The number of IKO users and transactions continued to grow, reinforcing the bank’s digital capabilities.

The following chart illustrates the bank’s strength in mobile banking:

Forward-Looking Statements

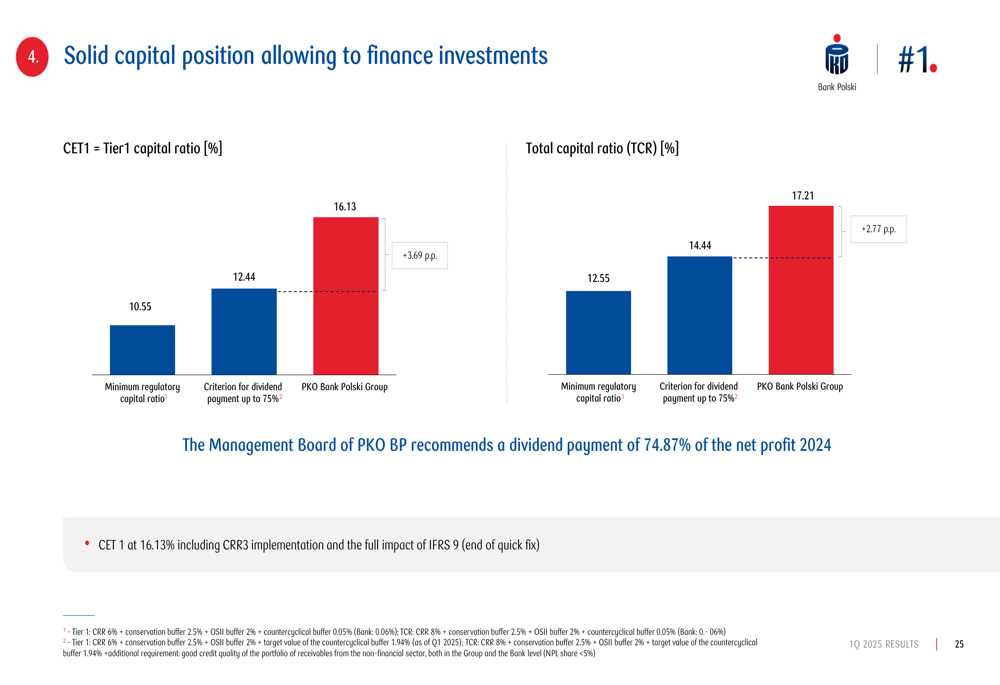

Looking ahead, PKO Bank Polski expressed confidence in its ability to maintain strong performance. The bank’s solid capital position, with a CET1 ratio of 16.13% and a total capital ratio of 17.21%, provides a strong foundation for future growth.

As illustrated in the following chart, the bank’s capital position remains robust:

The Management Board recommended a dividend payment of 74.87% of the 2024 net profit, reflecting confidence in the bank’s financial strength and future prospects.

The bank summarized its Q1 2025 performance as a "solid start of the year," highlighting the 2.5 billion PLN net profit (including 1 billion PLN of CHF legal risk provisions), continued double-digit core income growth, growth in both corporate and retail financing, and strong efficiency metrics with a cost-to-income ratio of 33.3% and cost of risk at 31 basis points.

PKO Bank Polski’s Q1 2025 results demonstrate the bank’s ability to maintain profitability and growth despite ongoing challenges related to Swiss franc mortgage legal issues and economic uncertainties. With its strong market position, solid capital base, and focus on digital innovation, the bank appears well-positioned to continue its growth trajectory in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.