United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

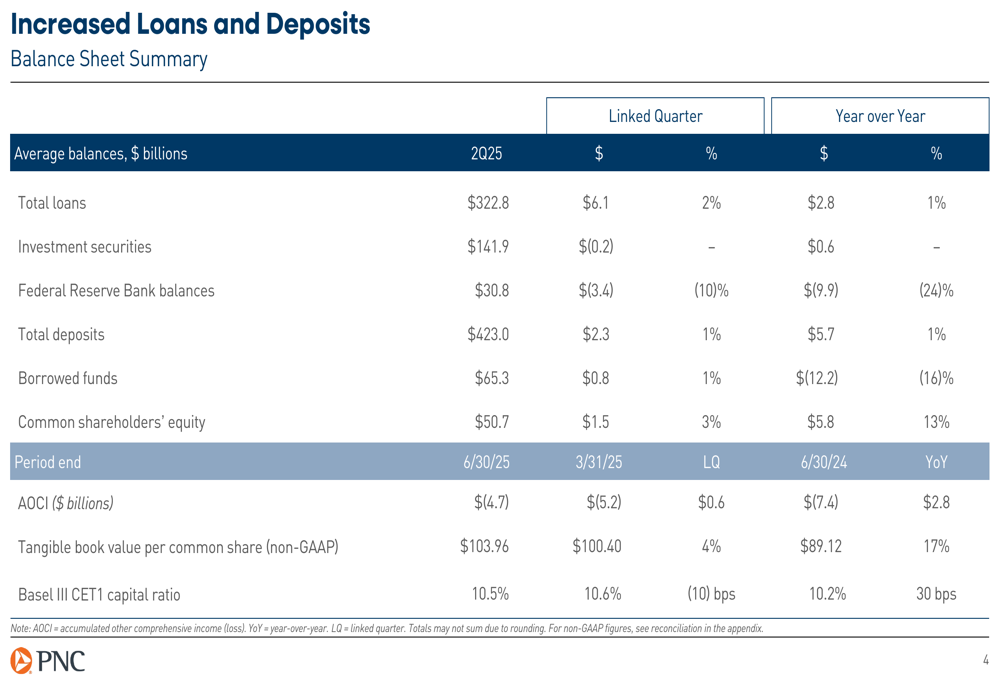

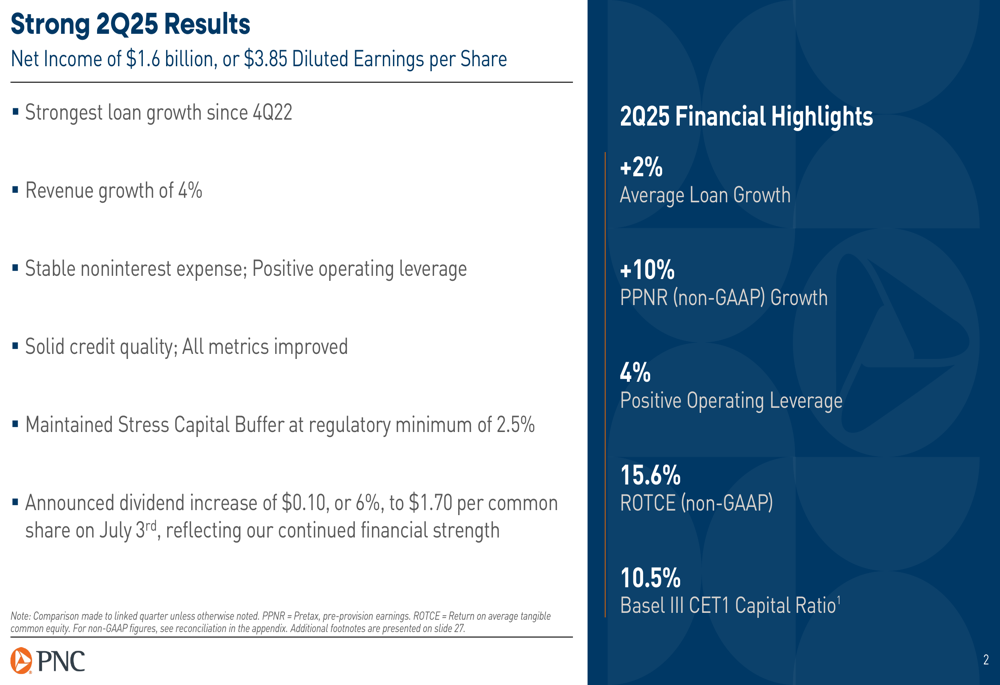

PNC Financial Services Group Inc (NYSE:PNC) released its second quarter 2025 earnings presentation on July 16, showcasing accelerated revenue growth and the strongest loan expansion since late 2022. The bank reported net income of $1.6 billion, or $3.85 per diluted share, representing a 10% increase from the first quarter and 11% year-over-year growth.

The stock responded positively in premarket trading, rising 2.35% to $196.65, according to market data, as investors reacted to results that exceeded expectations. This performance builds on PNC’s first quarter momentum, when the company reported EPS of $3.51.

Quarterly Performance Highlights

PNC delivered strong second quarter results across multiple metrics, with revenue growth of 4% compared to the linked quarter, driven by both higher net interest income and fee revenue. The bank maintained stable noninterest expenses while generating 4% positive operating leverage.

As shown in the following comprehensive overview of quarterly performance:

Average loan growth reached 2%, marking the strongest expansion since the fourth quarter of 2022. The bank also reported a return on tangible common equity (ROTCE) of 15.6% and maintained its Basel III CET1 capital ratio at 10.5%.

PNC announced a dividend increase of $0.10, or 6%, to $1.70 per common share on July 3, reflecting its continued financial strength and commitment to shareholder returns.

Detailed Financial Analysis

Revenue increased to $5.66 billion in the second quarter, up 4% from the first quarter and 5% year-over-year. This growth was driven by a 2% increase in net interest income to $3.56 billion and a 7% rise in noninterest income to $2.11 billion compared to the linked quarter.

The bank’s income statement reveals strong performance across key metrics:

Net interest margin improved to 2.80%, up from 2.78% in the first quarter and 2.60% a year ago, reflecting effective balance sheet management in the current interest rate environment. Fee income grew 3% from the linked quarter and 7% year-over-year to $1.89 billion, with particularly strong performance in capital markets and advisory services (up 5% linked quarter and 18% year-over-year) and card and cash management (up 7% linked quarter).

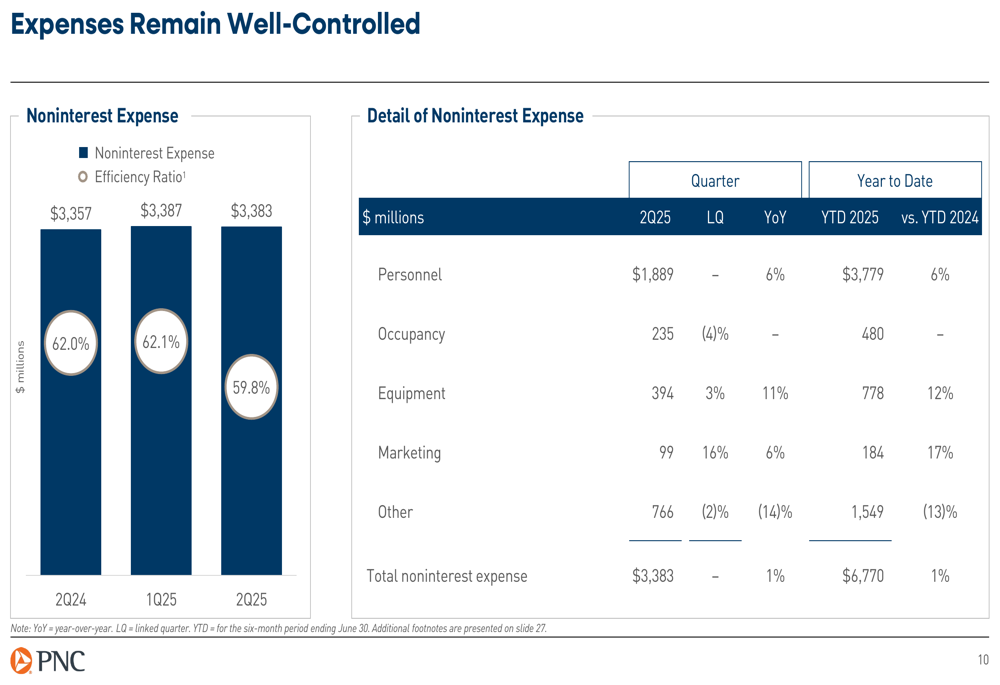

Expenses remained well-controlled at $3.38 billion, essentially flat compared to the first quarter and up only 1% year-over-year, demonstrating PNC’s disciplined approach to cost management while investing in growth initiatives.

Balance Sheet Strength and Credit Quality

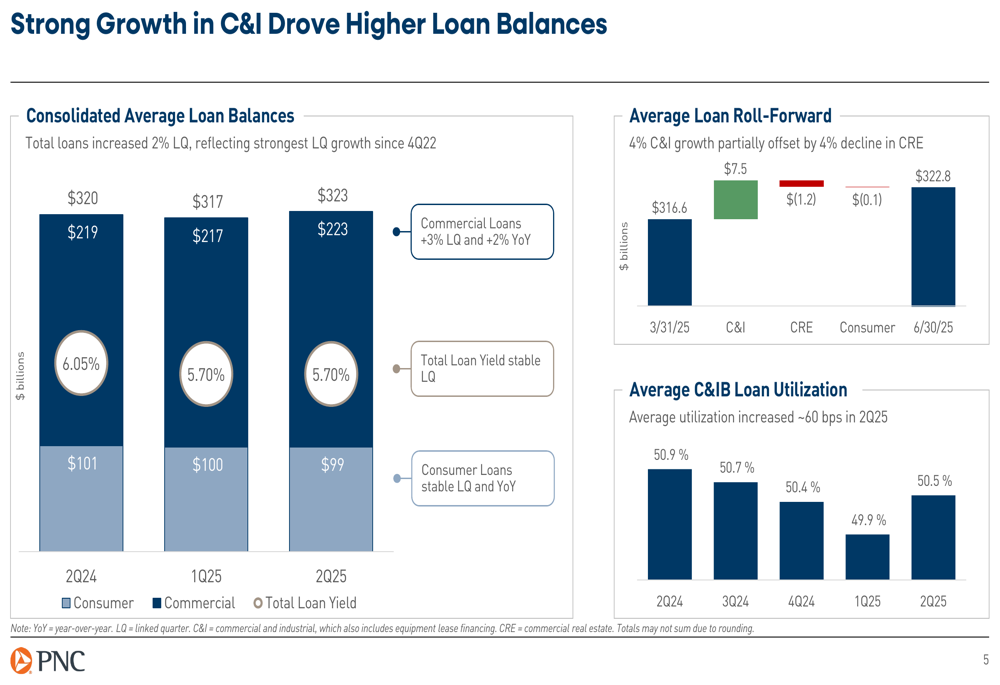

PNC’s loan growth was primarily driven by Commercial & Industrial (C&I) lending, which increased 4% and more than offset a 4% decline in Commercial Real Estate loans. The following chart illustrates this dynamic:

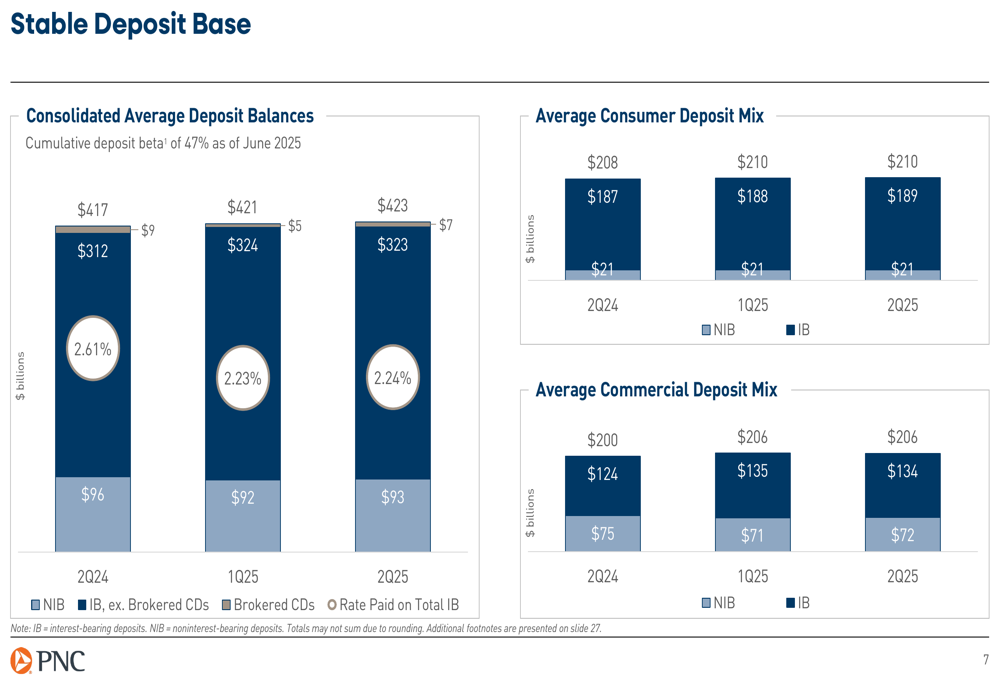

The bank’s deposit base remained stable at $423 billion, up 1% from the first quarter, with a consistent mix of interest-bearing and non-interest-bearing deposits. The cumulative deposit beta stood at 47% as of June 2025, indicating disciplined deposit pricing.

Credit quality showed improvement across all metrics, with nonperforming loans, delinquencies, and net charge-offs all declining from the previous quarter:

Nonperforming loans decreased to $2.11 billion as of June 30, 2025, down from $2.29 billion at the end of the first quarter. Net charge-offs declined to $198 million, representing 0.25% of average loans, compared to $205 million or 0.26% in the first quarter.

Strategic Initiatives and Business Segment Performance

PNC continues to execute on its strategy of diversified business growth across segments. The Corporate & Institutional Banking unit reported a 3% increase in average loans linked quarter, driven by growth in Corporate Banking and Business Credit. The segment also achieved record quarterly Treasury Management revenue.

The following slide details performance across business segments:

In Retail Banking, PNC grew net consumer checking accounts by 2% year-over-year, with 6% growth in the Southwest markets. Brokerage assets increased by 7% year-over-year to a record $87 billion. The bank also introduced new credit and debit card offerings, driving record transaction volume.

The Asset Management Group saw new client acquisition increase by 16% from the linked quarter, with year-to-date asset management fees up 5% year-over-year to a record first-half level.

Forward-Looking Statements

PNC updated its full-year 2025 guidance, now projecting average loan growth of approximately 1% compared to 2024, an improvement from its previous guidance of "stable" loan growth. The bank maintained its outlook for net interest income, noninterest income, and total revenue growth.

For the third quarter of 2025, PNC expects average loans to increase by approximately 1% from the second quarter, with net interest income projected to be up 1-2% and fee income up 1-3%. Noninterest expense is expected to increase 1-2% in the third quarter.

The bank’s investment securities portfolio and swap strategy are positioned to benefit from asset repricing, as illustrated in the following chart:

PNC continues to focus on its strategic priorities of growing its client base nationally, leveraging technology to enhance client service and ensure safety and soundness, and strengthening its brand by serving all stakeholders.

With a solid capital position, improving credit metrics, and continued revenue growth, PNC appears well-positioned to navigate the current economic environment while pursuing its long-term strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.