Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Polaris Industries Inc. (NYSE:PII) presented its second quarter 2025 earnings on July 29, 2025, revealing a company navigating significant challenges while making strategic adjustments to maintain market position. The stock responded positively in premarket trading, up 5.54% to $52.22, suggesting investors found encouraging elements in the presentation despite ongoing pressures.

The recreational vehicle manufacturer reported results that exceeded the high end of its guidance range, though still showing year-over-year declines in most key metrics. The presentation comes against a backdrop of continued macroeconomic uncertainty and significant tariff headwinds that have been pressuring the company’s margins and overall performance.

Quarterly Performance Highlights

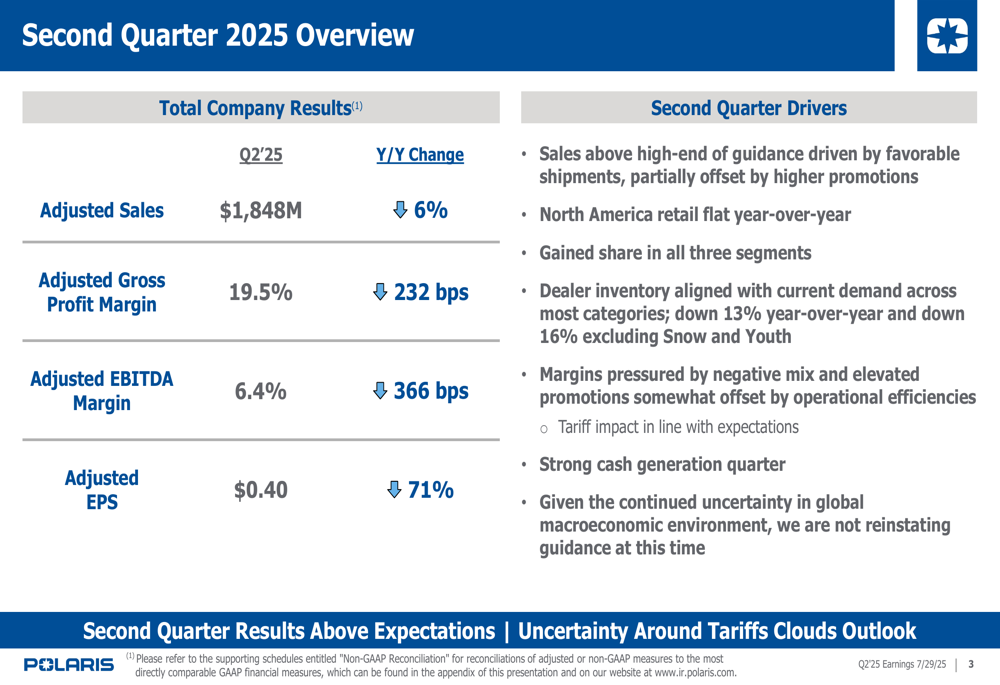

Polaris reported adjusted sales of $1.848 billion for Q2 2025, down 6% year-over-year but above the high end of the company’s guidance. The company achieved flat North America retail sales year-over-year, a notable improvement from the 7% decline reported in Q1 2025, suggesting some stabilization in consumer demand.

As shown in the following quarterly overview:

Adjusted gross profit margin came in at 19.5%, down 232 basis points year-over-year, while adjusted EBITDA margin fell 366 basis points to 6.4%. Adjusted earnings per share declined 71% to $0.40, reflecting the significant margin pressure the company faces.

Despite these challenges, Polaris highlighted several positive developments, including market share gains across all three business segments, dealer inventory that’s now aligned with current demand (down 13% year-over-year), and strong cash generation during the quarter.

Tariff Impact and Mitigation Strategy

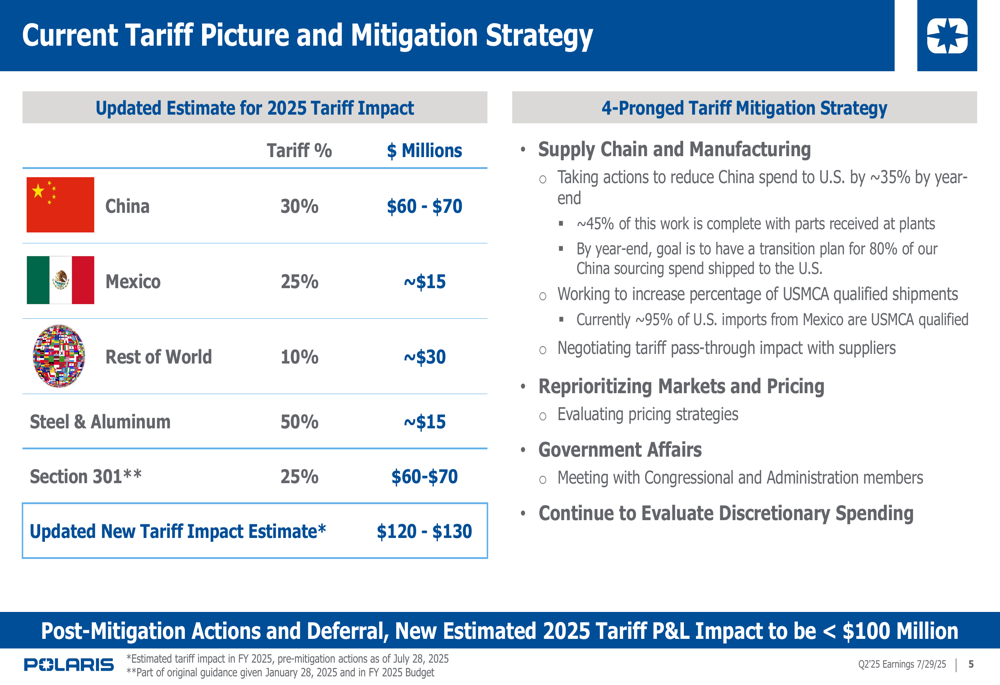

A central focus of the presentation was the impact of tariffs on Polaris’s business and the company’s strategy to mitigate these effects. The company provided a detailed breakdown of the estimated tariff impact for 2025, which totals $120-$130 million before mitigation efforts.

The tariff picture and mitigation strategy are illustrated in this detailed breakdown:

Polaris outlined a four-pronged approach to address these tariffs:

1. Supply chain and manufacturing adjustments, including reducing China spend to the U.S. by approximately 35% by year-end

2. Reprioritizing markets and evaluating pricing strategies

3. Government affairs engagement with Congressional and Administration members

4. Continued evaluation of discretionary spending

Through these mitigation actions and deferrals, Polaris expects to reduce the 2025 tariff P&L impact to less than $100 million, though this still represents a significant headwind for the company’s profitability.

Segment Performance Analysis

Polaris provided detailed breakdowns of performance across its three main business segments, each showing different trends:

Off Road

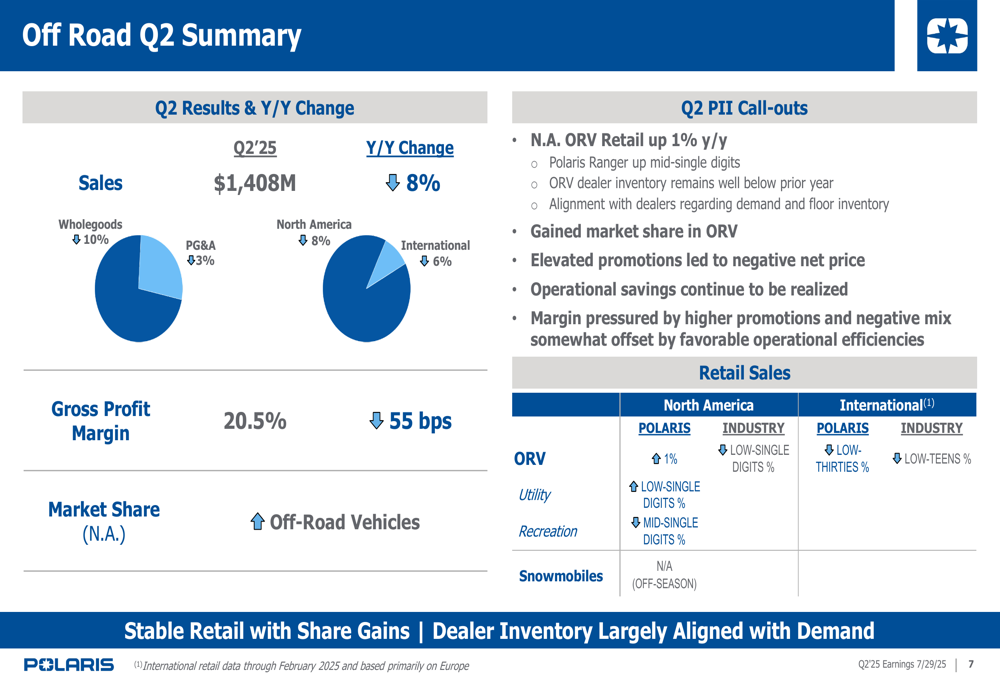

The Off Road segment, which represents the largest portion of Polaris’s business, reported sales of $1.408 billion, down 8% year-over-year. Despite this decline, North American retail sales increased by 1% year-over-year, and the company gained market share in the segment.

The Off Road segment performance is summarized in this chart:

Management noted that elevated promotions led to negative net pricing, though this was partially offset by operational efficiencies. The utility segment showed low-single-digit growth, while the recreation segment faced mid-single-digit declines.

On Road

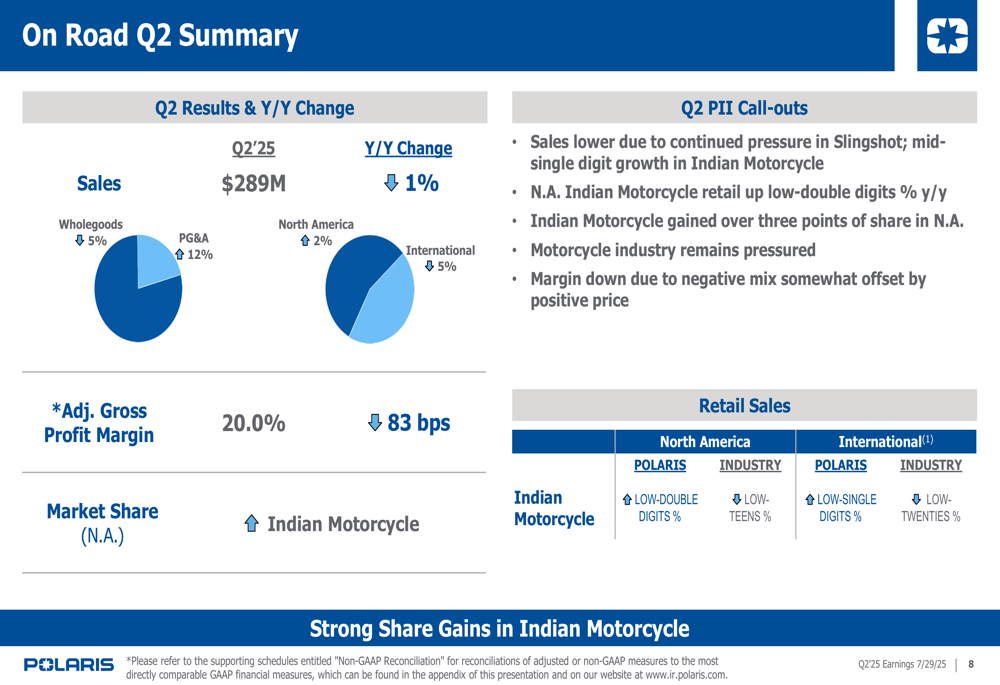

The On Road segment reported sales of $289 million, down 1% year-over-year. The decline was primarily attributed to continued pressure in the Slingshot business, while Indian Motorcycle showed mid-single-digit growth.

As illustrated in the On Road performance summary:

A bright spot was Indian Motorcycle’s retail performance, which grew by low-double digits year-over-year in North America, resulting in a market share gain of over three percentage points. This performance is particularly notable given that the broader motorcycle industry remains under pressure.

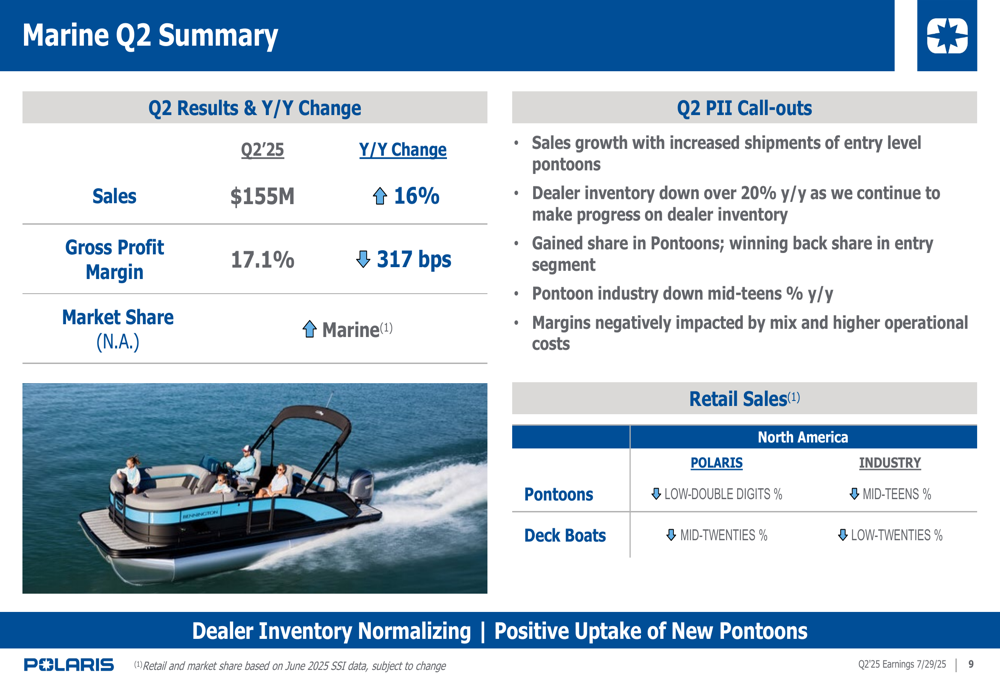

Marine

The Marine segment was the only one to show sales growth, with revenue increasing 16% year-over-year to $155 million. This growth was driven by increased shipments of entry-level pontoons, though margins were negatively impacted by mix and higher operational costs.

The Marine segment’s performance is detailed here:

Despite the sales growth, the broader pontoon industry was down mid-teens percentage year-over-year, highlighting Polaris’s ability to gain share in a challenging market. Dealer inventory in the Marine segment was down over 20% year-over-year as the company continues to align inventory with demand.

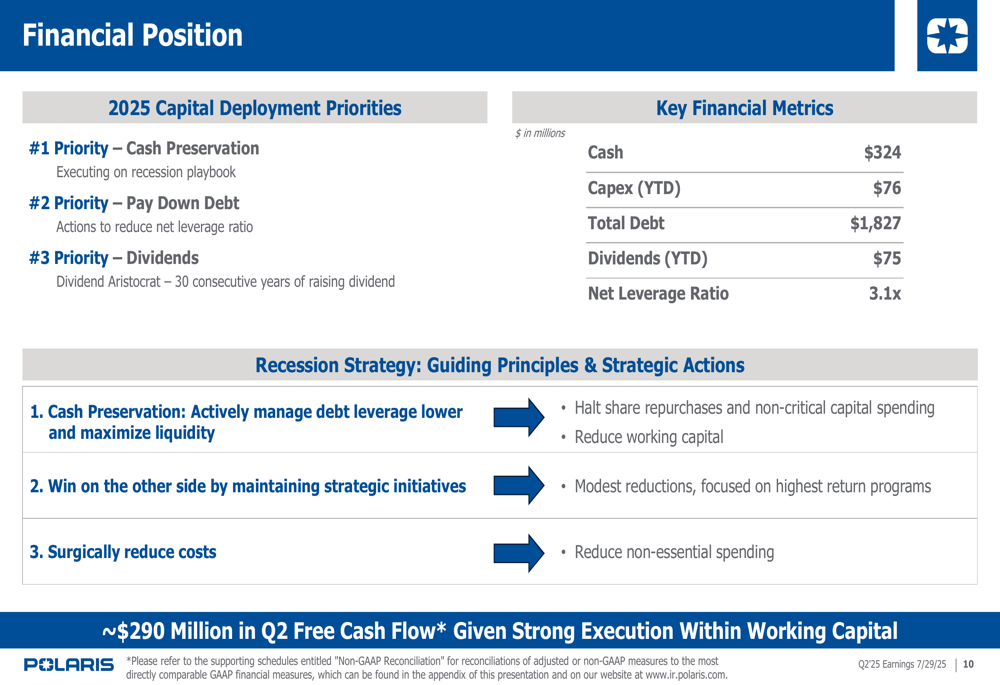

Financial Position and Outlook

Polaris emphasized its focus on financial discipline, with cash preservation as the top priority, followed by debt reduction and dividend payments. The company reported $324 million in cash, total debt of $1.827 billion, and a net leverage ratio of 3.1x.

The financial position and capital deployment priorities are outlined in this summary:

For the third quarter of 2025, Polaris expects sales to be between $1.6 billion and $1.8 billion, with retail demand expected to remain relatively flat in what the company describes as an "elevated promotional environment." The company anticipates a tariff impact of $30-$40 million in Q3 as it continues to execute on its mitigation strategy.

Given the continued uncertainty in the global macroeconomic environment and the evolving tariff situation, Polaris has not reinstated full-year guidance at this time, maintaining the cautious approach it adopted in Q1.

In a positive development for its product lineup, Polaris announced the launch of a new RANGER 500 utility vehicle with an MSRP of $9,999, targeting what the company describes as a significant market opportunity in the utility segment.

Conclusion

Polaris’s Q2 2025 presentation reveals a company making strategic adjustments to navigate significant headwinds, particularly from tariffs and a challenging macroeconomic environment. While sales and margins remain under pressure year-over-year, the stabilization in retail sales and market share gains across all segments suggest the company’s strategies are helping it maintain its competitive position.

The stock’s positive premarket reaction indicates that investors may be focusing on these signs of stabilization and the company’s proactive approach to tariff mitigation rather than the continued year-over-year declines in key financial metrics. As Polaris moves into the second half of 2025, its ability to execute on its tariff mitigation strategy and maintain retail momentum will be critical factors to watch.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.