Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Polaris Industries Inc. (NYSE:PII) presented its third-quarter 2025 earnings results on October 28, revealing a company navigating significant challenges while maintaining sales growth and market share gains. Despite beating earnings expectations, Polaris shares fell 6.87% as investors digested the impact of tariffs and strategic changes.

Quarterly Performance Highlights

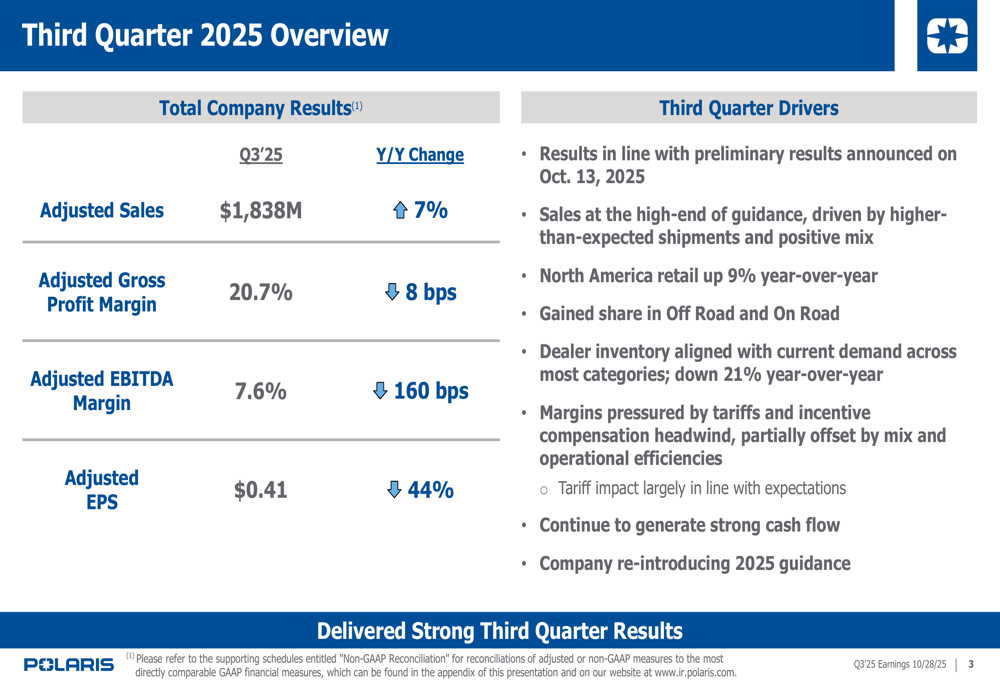

Polaris reported adjusted sales of $1.84 billion for Q3 2025, representing a 7% year-over-year increase and exceeding analyst expectations. The company posted adjusted earnings per share of $0.41, significantly outperforming the forecasted $0.23, though this still represented a 44% decline from the previous year.

"We delivered strong third-quarter results aligned with our preliminary announcement from earlier this month," noted the company in its presentation. "Sales came in at the high-end of guidance, driven by higher shipments and positive mix."

North American retail sales increased by 9% year-over-year, with Polaris gaining share in both Off Road and On Road segments. The company highlighted that dealer inventory is now aligned with current demand across most categories, down 21% compared to the previous year.

As shown in the following overview of Q3 2025 performance:

Segment Performance

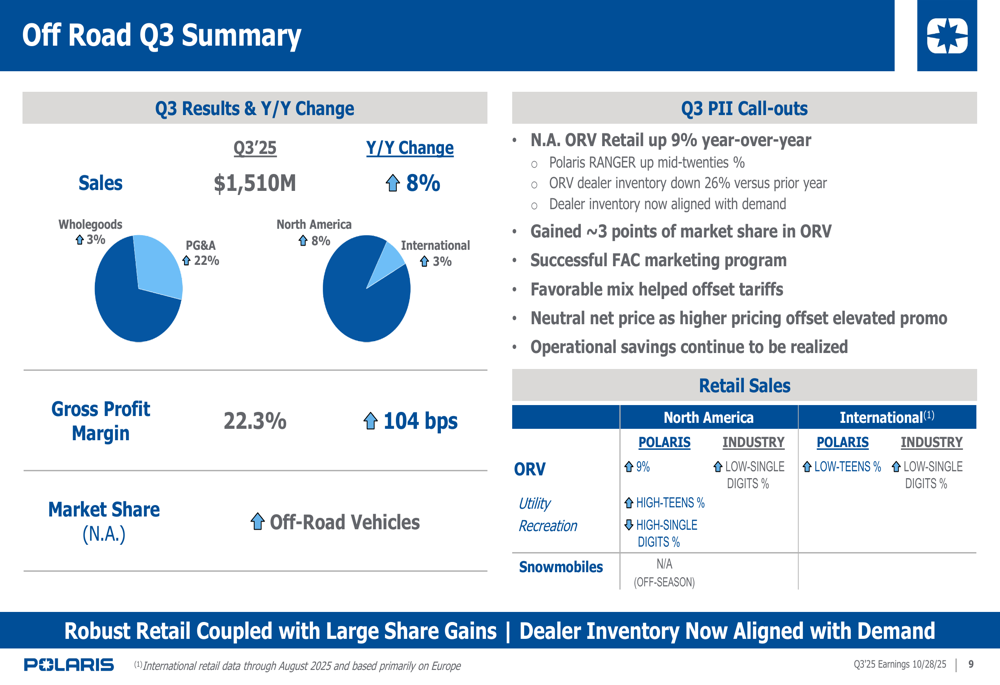

The Off Road segment, Polaris’s largest business unit, delivered sales of $1.51 billion, up 8% year-over-year with an improved gross profit margin of 22.3% (up 104 basis points). The company gained approximately 3 points of market share in ORV, with utility vehicles up by high-teens percentages.

"Robust retail coupled with large share gains and dealer inventory now aligned with demand," the company noted regarding its Off Road segment performance.

The segment breakdown shows strong performance in Off Road while other segments faced challenges:

The On Road segment reported sales of $229 million, down 3% year-over-year with adjusted gross profit margin of 16.6% (down 23 basis points). Market softness drove the revenue decline, though Polaris achieved modest share gains in North America for Indian Motorcycle.

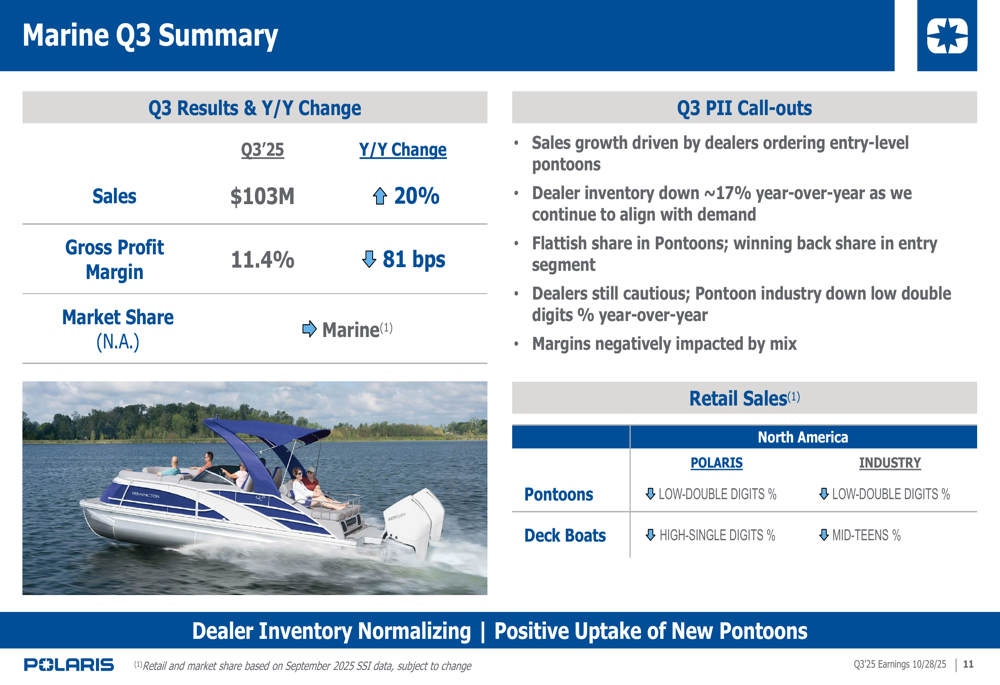

The Marine segment showed sales growth of 20% year-over-year to $103 million, though gross profit margin declined by 81 basis points to 11.4%. The growth was primarily driven by dealers ordering entry-level pontoons, while the broader marine industry continues to experience softness.

Tariff Impact and Mitigation Strategy

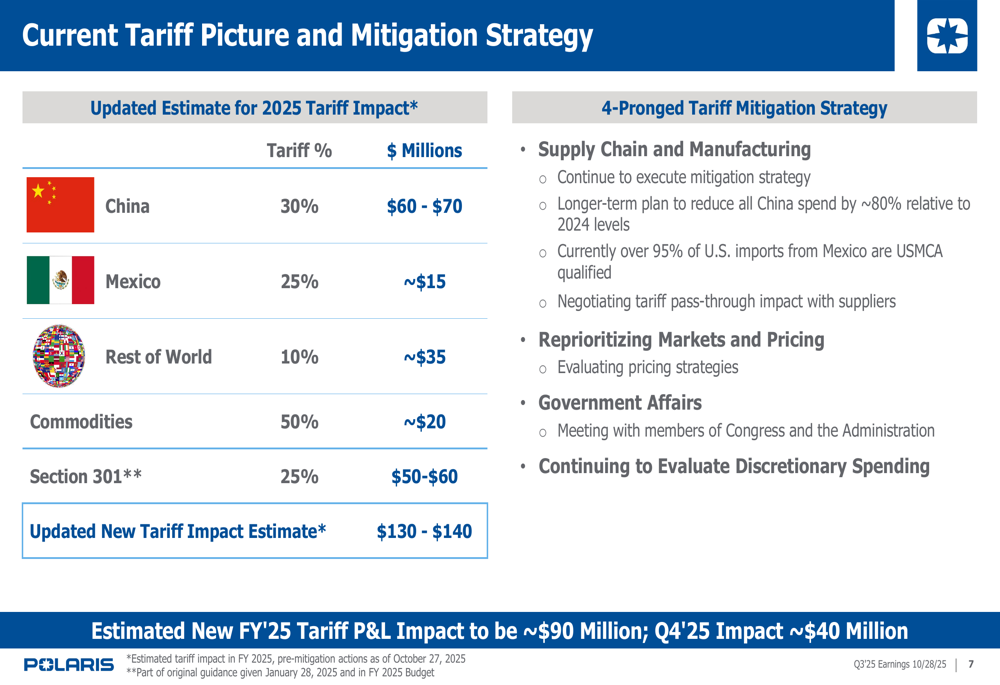

A significant focus of the presentation was on tariffs, which are creating substantial headwinds for Polaris. The company detailed its updated estimate for 2025 tariff impact, totaling $130-$140 million across various categories including China (30% tariff), Mexico (25% tariff), and commodities (50% tariff).

Polaris outlined a four-pronged mitigation strategy focusing on supply chain adjustments, market prioritization, government affairs engagement, and discretionary spending evaluation. The company expects the net P&L impact for fiscal year 2025 to be approximately $90 million, with about $40 million impacting Q4 2025.

The detailed tariff impact and mitigation strategy is illustrated here:

Strategic Initiatives

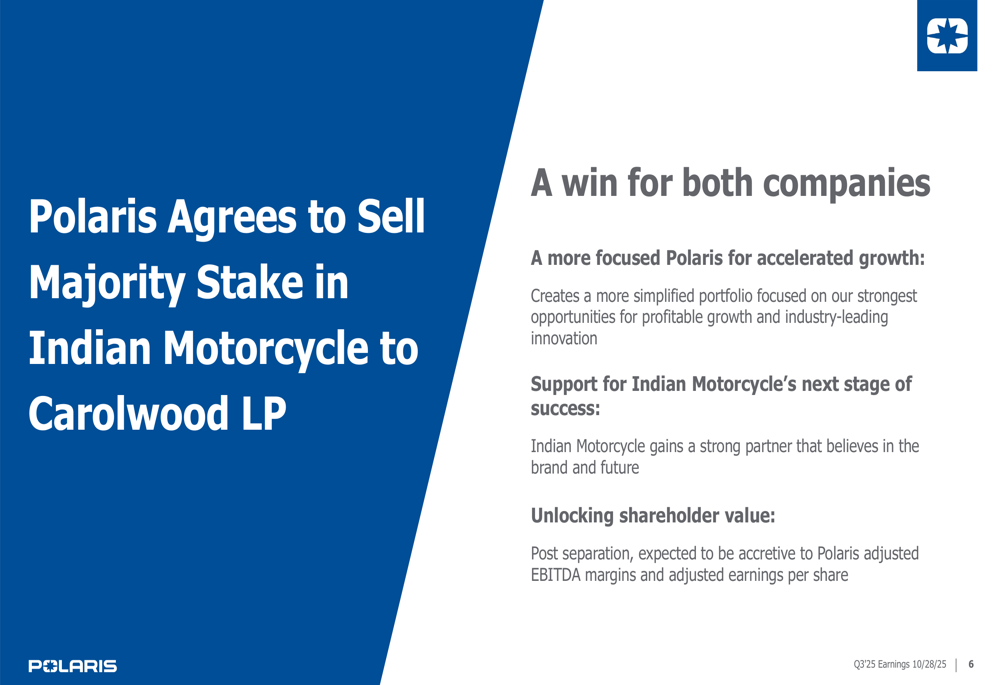

In a major strategic move, Polaris announced an agreement to sell a majority stake in Indian Motorcycle to Carolwood LP. This decision aims to create "a more focused Polaris for accelerated growth through a simplified portfolio" while supporting "Indian Motorcycle’s next stage of success with a strong partner."

The company expects this transaction to be accretive to Polaris’s adjusted EBITDA margins and adjusted earnings per share post-separation.

Polaris continues to position itself as a global leader in powersports, highlighting innovations and new product launches for 2026. The presentation emphasized the company’s "Think Outside" slogan and showcased its diverse vehicle portfolio.

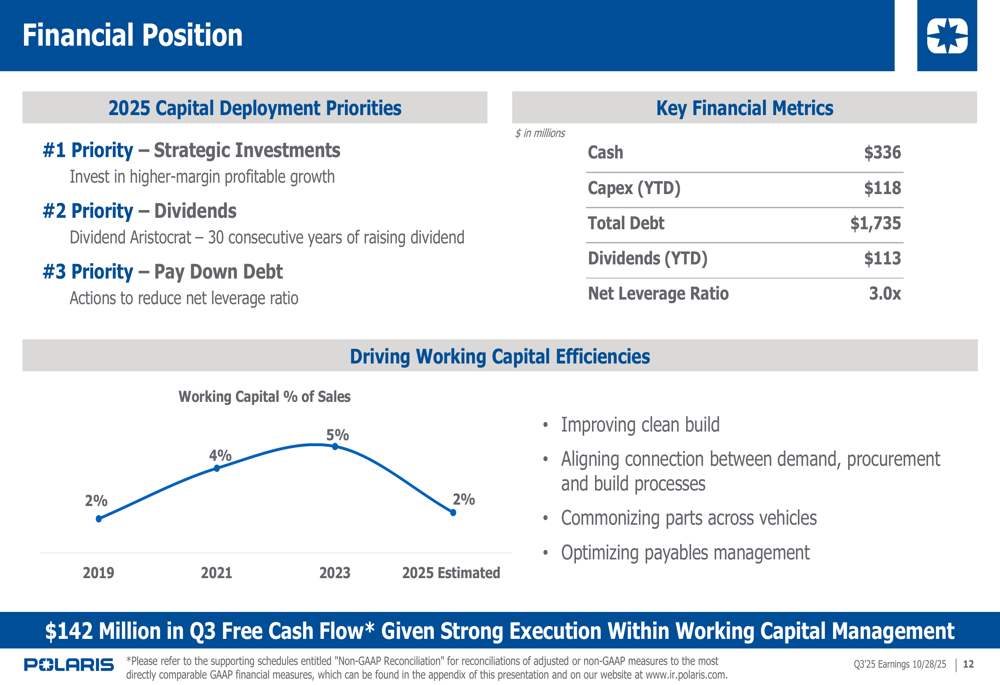

Financial Position and Outlook

Polaris maintains a solid financial position with $336 million in cash and $1.735 billion in total debt, resulting in a net leverage ratio of 3.0x. The company’s capital deployment priorities focus first on strategic investments, followed by dividends and debt reduction.

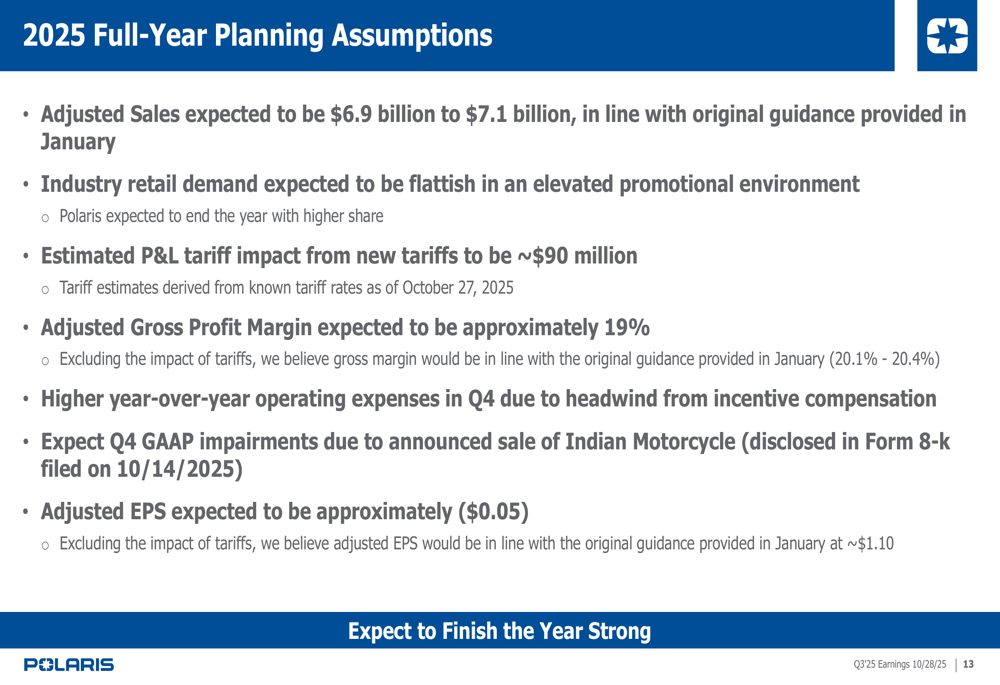

For full-year 2025, Polaris reintroduced guidance with expected adjusted sales of $6.9-$7.1 billion, in line with its original guidance. However, the company now anticipates an adjusted EPS loss of approximately $0.05 for the year. This outlook assumes relatively flat industry retail demand in an elevated promotional environment.

The company also warned investors to expect Q4 GAAP impairments related to the announced sale of Indian Motorcycle.

Despite the challenges from tariffs and market conditions, Polaris emphasized its continued focus on innovation, operational efficiencies, and strategic positioning to drive long-term growth. The company’s ability to gain market share in key segments while navigating significant external pressures demonstrates resilience, though investors remain cautious as reflected in the stock’s performance following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.