BofA update shows where active managers are putting money

Introduction & Market Context

Premium Brands Holdings Corporation (TSX:PBH) presented its first quarter 2025 results during a conference call on May 7, 2025, highlighting record quarterly sales and adjusted EBITDA despite ongoing market challenges. The company’s stock has shown resilience, trading at $82.60 as of July 14, 2025, down slightly by 0.64% but well above its 52-week low of $72.57.

The specialty food producer reported revenue of $1.68 billion for Q1 2025, exceeding analyst expectations of $1.59 billion by 5.66%, while EPS came in at $0.68, slightly below the forecasted $0.7211. The company’s performance reflects its successful execution of U.S.-focused growth initiatives, particularly in protein, sandwich, and bakery segments, while navigating a stabilizing Canadian market.

Quarterly Performance Highlights

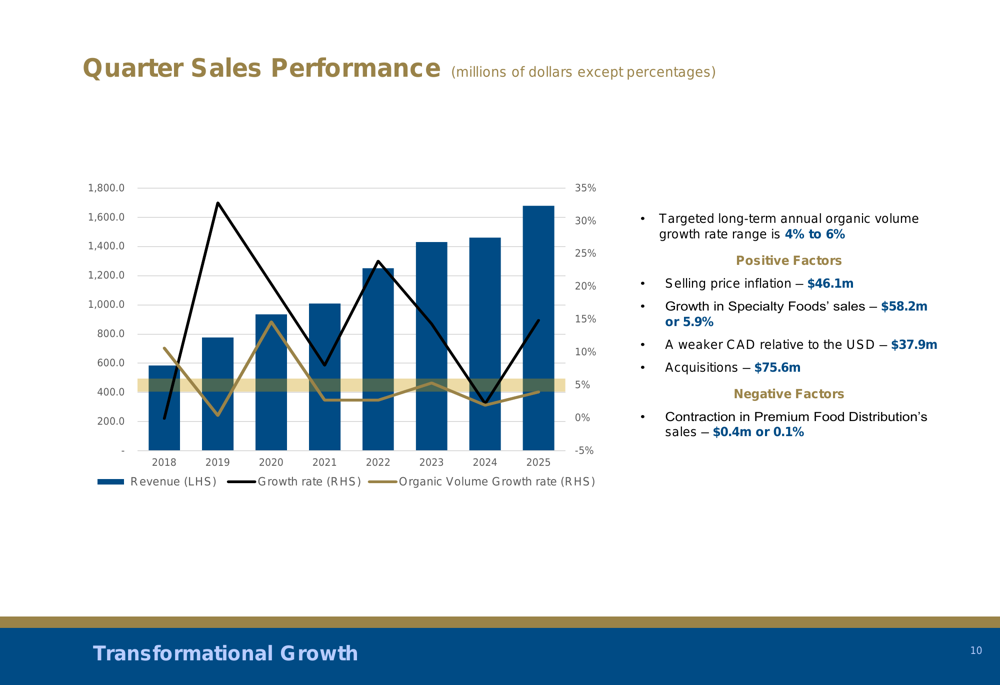

Premium Brands achieved record first quarter sales and adjusted EBITDA, maintaining its 2025 guidance while declaring a quarterly dividend of $0.85 per share. The company highlighted several positive factors driving its performance, including selling price inflation ($46.1 million), growth in Specialty Foods sales ($58.2 million or 5.9%), favorable currency exchange rates ($37.9 million), and contributions from acquisitions ($75.6 million).

As shown in the following chart of quarterly sales performance, the company has maintained a strong growth trajectory:

Despite this impressive revenue growth, the company experienced slight margin compression, with Specialty Foods’ adjusted EBITDA margin declining to 9.1% from 9.5% in the previous year, and Premium Food Distribution’s margin decreasing to 4.8% from 5.1%. Major drivers affecting profitability included positive impacts from organic sales volume growth and plant efficiency gains, offset by commodity cost inflation and wage pressures.

U.S. Expansion Strategy

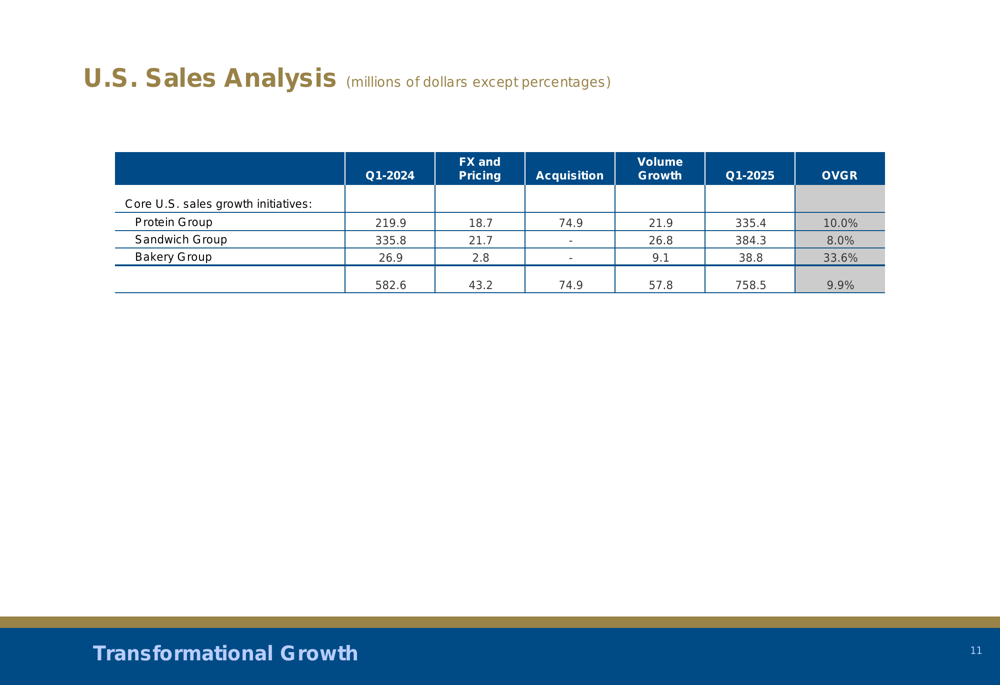

The company’s U.S. expansion strategy has been particularly successful, with significant growth across key product categories. The U.S. sales analysis reveals substantial year-over-year increases in all segments:

This strong performance in the U.S. market aligns with CEO George Paliologo’s statement from the earnings call that "We’re in the early innings in terms of our U.S. business," highlighting the significant growth potential that remains. The bakery segment showed particularly impressive growth of over 30%, confirming the company’s strategic focus on this category.

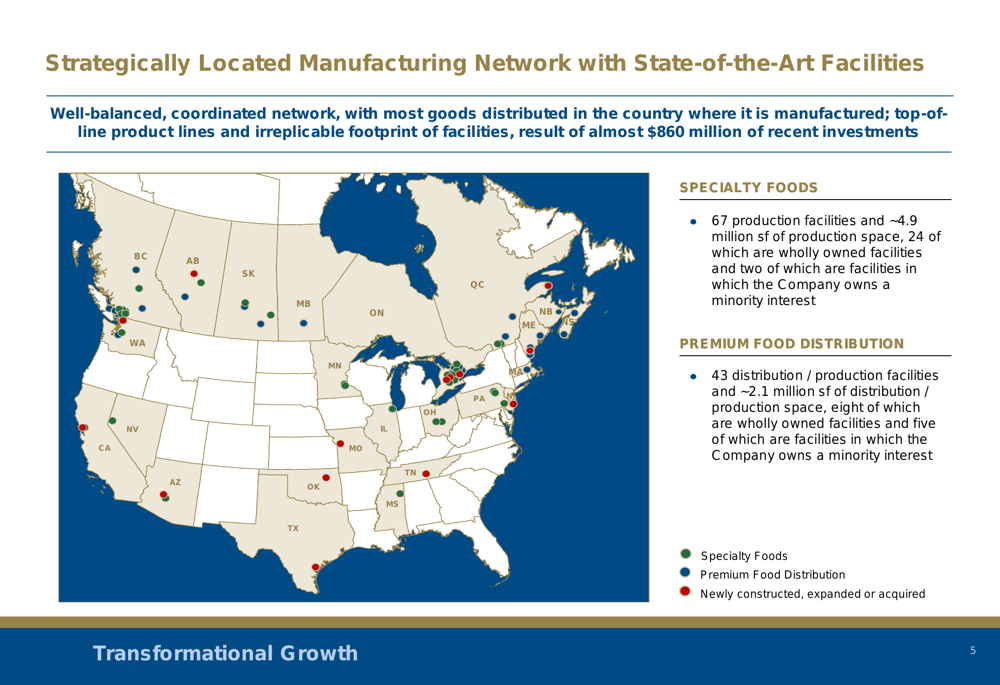

Premium Brands has built a comprehensive manufacturing and distribution network across North America, creating a competitive advantage through its strategic footprint:

With 67 production facilities totaling approximately 4.9 million square feet and 43 distribution/production facilities comprising about 2.1 million square feet, the company has established a well-balanced network that minimizes cross-border logistics challenges. This infrastructure represents nearly $860 million in recent investments, positioning the company for continued growth.

Acquisition Pipeline and Growth Initiatives

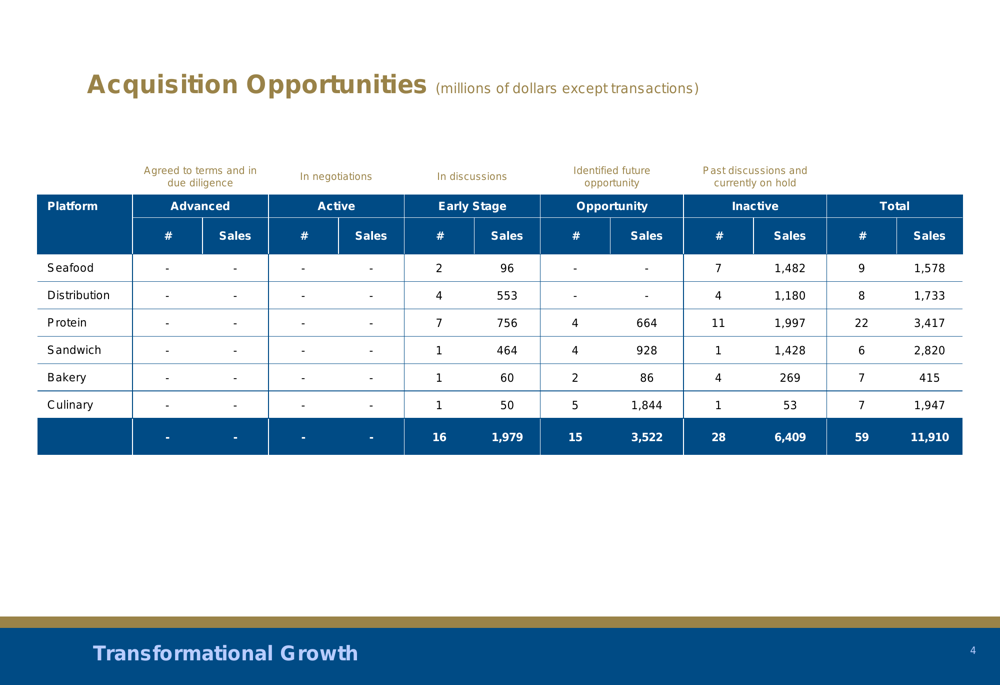

Premium Brands continues to pursue an active acquisition strategy, with a robust pipeline of potential targets across various platforms. The following table illustrates the breadth and scale of these opportunities:

With 59 potential acquisition targets representing combined sales of $11.91 billion, the company has significant runway for inorganic growth. The protein segment represents the largest opportunity with 22 potential acquisitions totaling $3.42 billion in sales, followed by the sandwich segment with 6 opportunities worth $2.82 billion.

The company recently completed the acquisition of Denmark Sausage, further expanding its protein portfolio. Management noted during the earnings call that the company plans to accelerate organic growth in the latter half of the year, complementing its acquisition strategy.

Capital Allocation and Financial Position

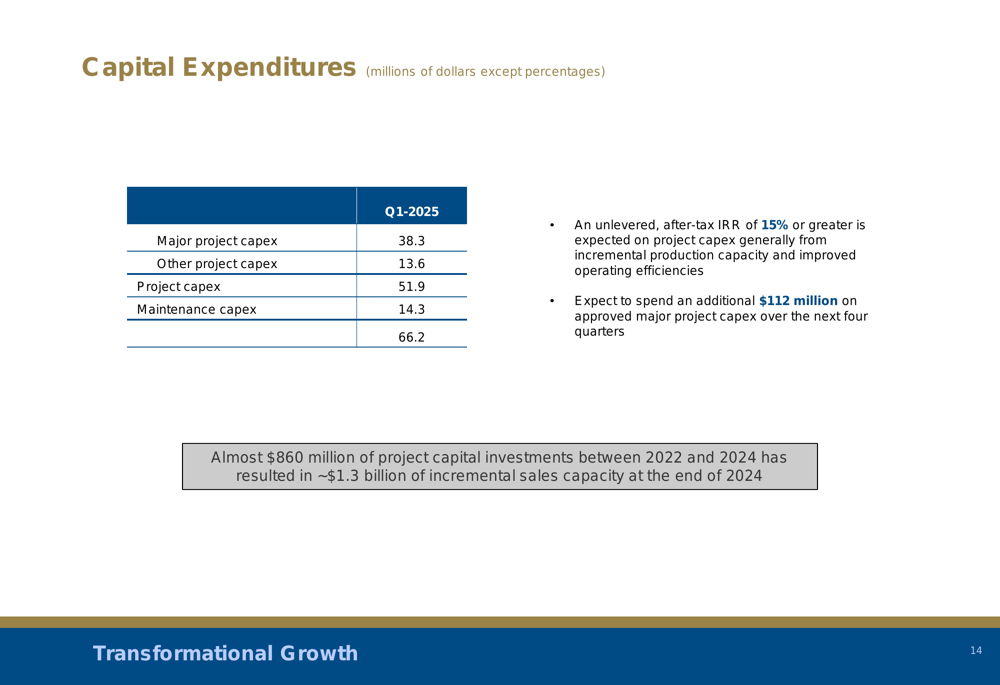

Premium Brands is investing heavily in growth initiatives, with capital expenditures totaling $66.2 million in the quarter. The company expects these investments to generate an unlevered, after-tax IRR of 15% or greater, primarily through incremental production capacity and improved operating efficiencies.

The company plans to invest an additional $112 million in approved major projects over the next four quarters, supporting its ambitious growth targets. These investments align with the company’s capacity expansion strategy, including new facilities in Tennessee and the Greater Toronto Area that are expected to add $1.7 billion in capacity.

Premium Brands maintains a disciplined approach to debt management, with long-term targets for senior debt to EBITDA ratio of 2.5:1 to 3.0:1 and total debt to EBITDA ratio of 3.5:1 to 4.0:1. The company recently completed a convertible debenture offering resulting in net proceeds of $165 million, enhancing its financial flexibility.

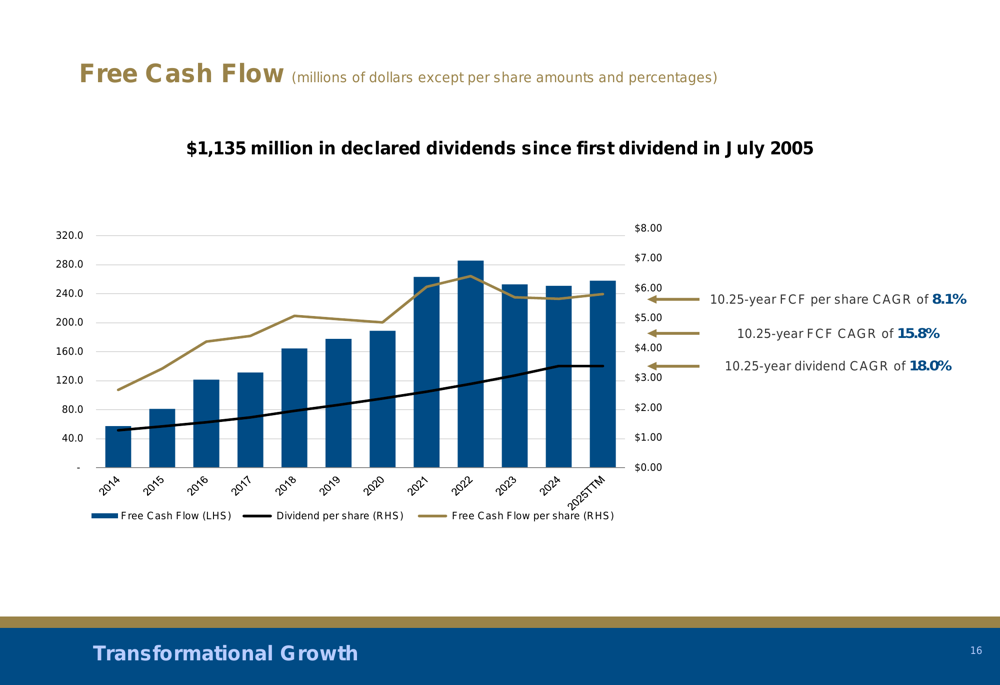

The company’s free cash flow generation has supported consistent dividend growth, with $1.135 billion in declared dividends since July 2005:

With a 10.25-year dividend CAGR of 18.0% and free cash flow CAGR of 15.8%, Premium Brands has demonstrated a strong commitment to shareholder returns while funding its growth initiatives.

Forward-Looking Statements

Looking ahead, Premium Brands has maintained its 2025 sales and adjusted EBITDA guidance, targeting revenue of $7.2-$7.4 billion for the full year. The company expects to face continued challenges from commodity cost inflation and wage pressures, though these are anticipated to stabilize later in the year.

Management remains confident in the company’s growth strategy, particularly in the U.S. market where demand for protein products remains strong. The company’s extensive acquisition pipeline and capital investment program provide multiple avenues for growth, supporting its long-term financial targets.

While the company faces execution risks associated with its capacity expansion and new product launches, as well as temporary financial challenges noted in the earnings call, its diversified product portfolio and geographic footprint provide resilience against market fluctuations. Premium Brands reported no material impacts from the Canada/U.S. trade dispute, further supporting its outlook for continued growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.