Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Primoris Services (NYSE:PRIM) Corporation (NASDAQ:PRIM) released its first quarter 2025 earnings presentation on May 6, showcasing substantial year-over-year growth across key financial metrics. The infrastructure construction company reported a 16.7% increase in revenue and more than doubled its earnings per share compared to the same period last year.

The company’s stock closed at $67.07 on the day of the presentation, down slightly by 0.88% from the previous close. Despite this minor dip, Primoris continues to trade well above its 52-week low of $45.92, reflecting overall positive market sentiment following several quarters of strong performance.

Quarterly Performance Highlights

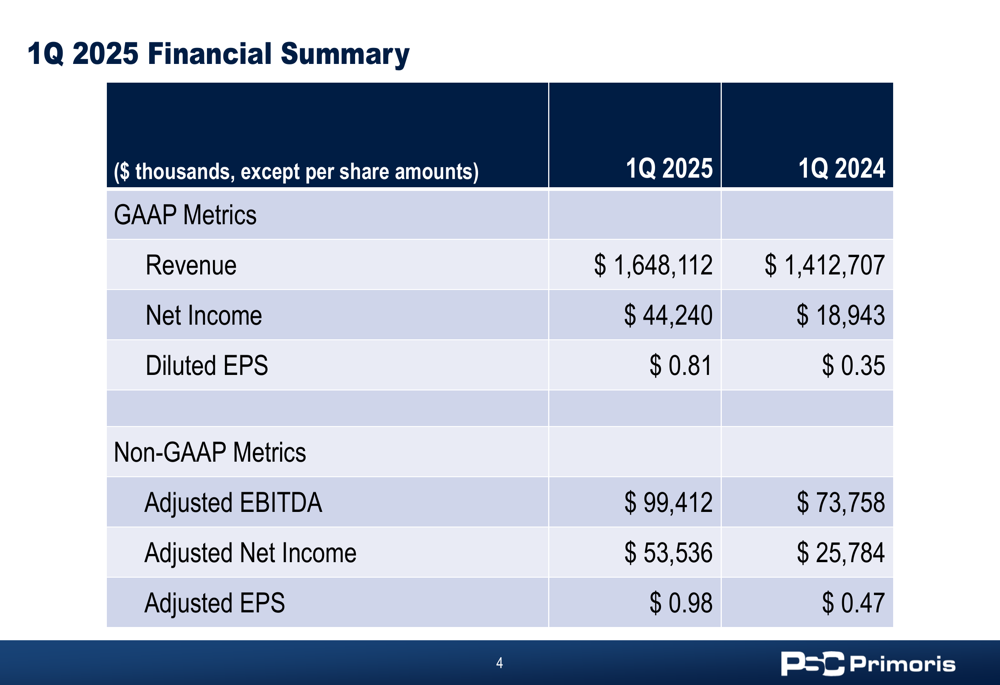

Primoris delivered exceptional financial results for the first quarter of 2025, with significant improvements across both GAAP and non-GAAP metrics compared to Q1 2024.

As shown in the following comprehensive financial summary:

Revenue reached $1.65 billion, a 16.7% increase from $1.41 billion in Q1 2024. Net income more than doubled to $44.2 million compared to $18.9 million in the prior year period, while diluted earnings per share jumped to $0.81 from $0.35, representing a 131.4% increase.

Non-GAAP metrics also showed robust growth, with Adjusted EBITDA increasing by 34.8% to $99.4 million and Adjusted EPS rising to $0.98 from $0.47 in Q1 2024.

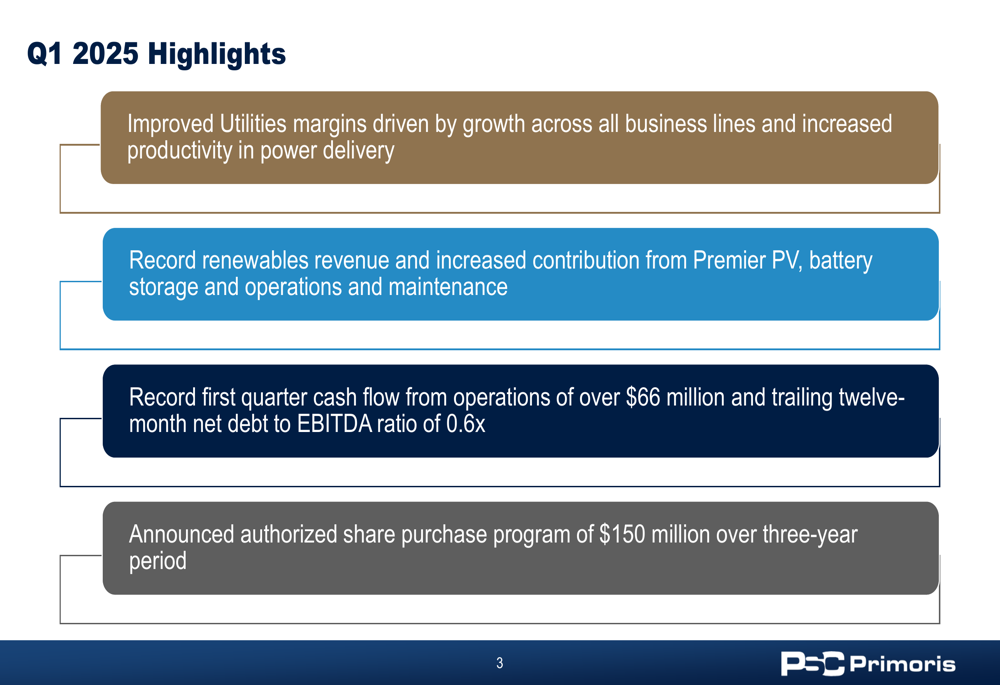

The company highlighted several key achievements that contributed to these strong results:

Particularly notable was the record first quarter cash flow from operations exceeding $66 million, which helped maintain a healthy balance sheet with a trailing twelve-month net debt to EBITDA ratio of just 0.6x. The company also announced a $150 million share repurchase program spread over a three-year period, signaling confidence in its financial position and commitment to returning value to shareholders.

Segment Analysis

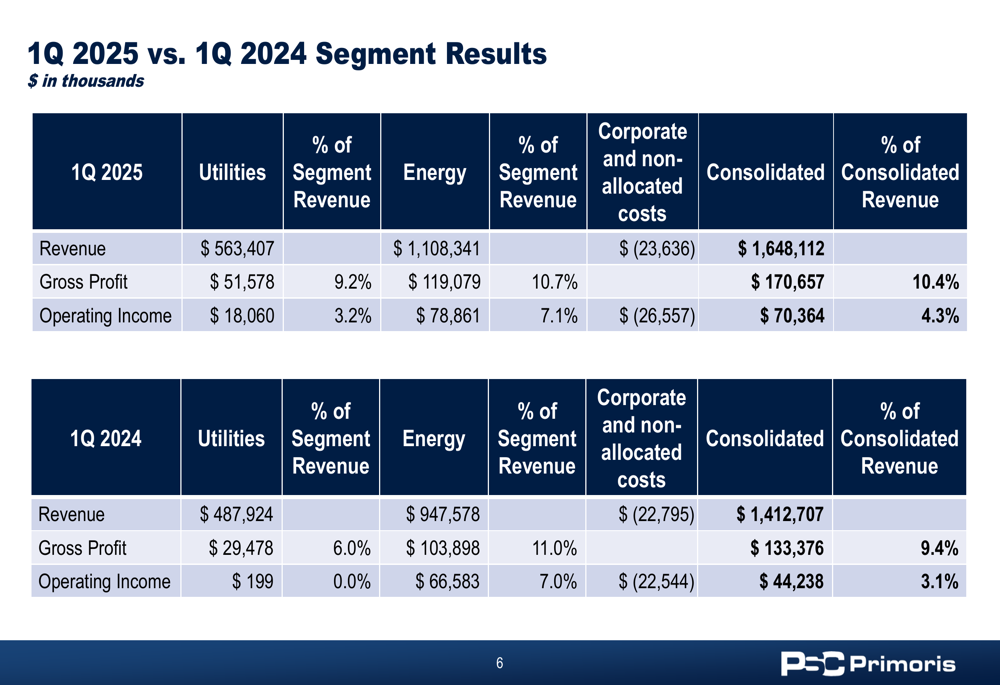

Primoris operates through two primary segments: Utilities and Energy. Both segments contributed to the company’s overall growth, with particularly impressive margin improvements in the Utilities segment.

The detailed segment breakdown reveals the following performance metrics:

The Utilities segment saw revenue increase by 15.5% to $563.4 million, while its operating income surged dramatically from just $199,000 in Q1 2024 to $18.1 million in Q1 2025. This improvement was driven by growth across all business lines and increased productivity in power delivery operations, resulting in gross profit margin expansion from 6.0% to 9.2%.

The Energy segment, which accounts for the larger portion of Primoris’s business, grew revenue by 17.0% to $1.11 billion. Operating income in this segment increased by 18.4% to $78.9 million, maintaining a strong operating margin of 7.1%. The company specifically highlighted record renewables revenue with increased contributions from Premier PV, battery storage, and operations and maintenance services.

Backlog and Revenue Stability

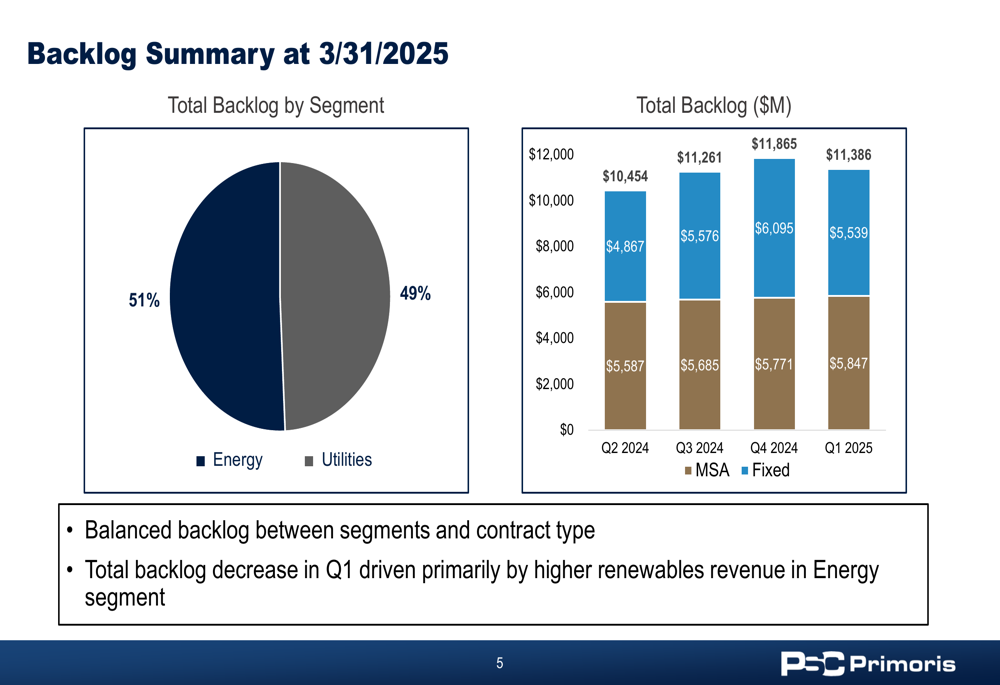

Primoris’s backlog provides insight into future revenue potential and business stability. As of March 31, 2025, the company maintained a well-balanced backlog between its two segments.

The following chart illustrates the backlog composition and recent trends:

Total (EPA:TTEF) backlog stood at $11.39 billion, showing a slight decrease from $11.87 billion at the end of Q4 2024. This reduction was primarily attributed to higher renewables revenue execution in the Energy segment during Q1. The backlog remains evenly distributed between Energy (51%) and Utilities (49%) segments, providing balanced exposure to both markets.

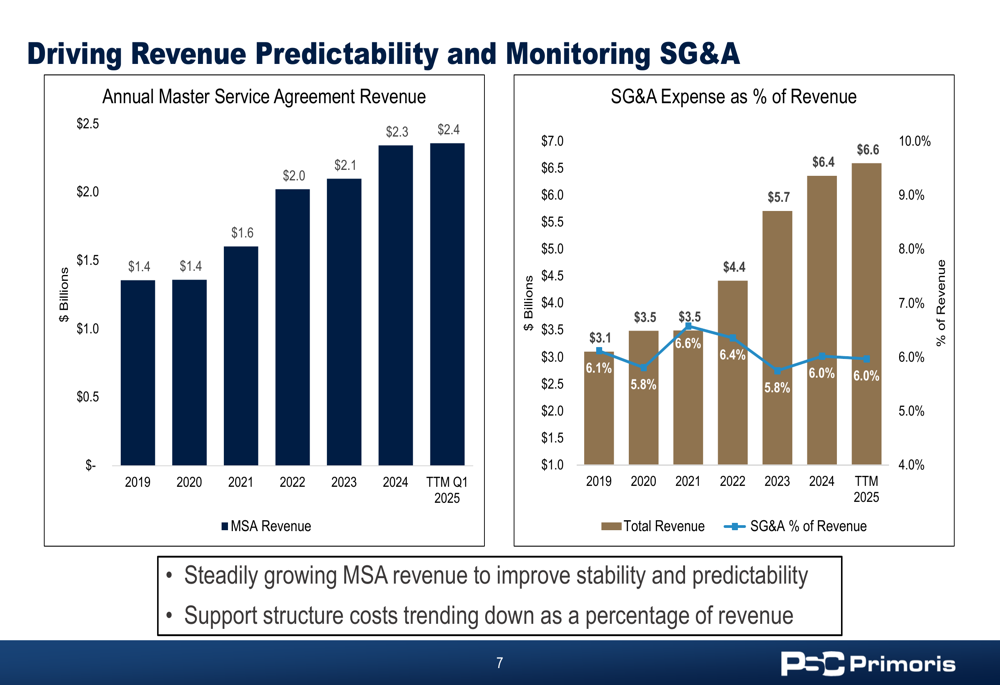

A key element of Primoris’s business strategy has been growing its Master Service Agreement (MSA) revenue to improve stability and predictability. The company has made significant progress in this area over recent years:

Annual MSA revenue has grown steadily from $1.4 billion in 2019 to $2.4 billion for the trailing twelve months ending Q1 2025. This growth in recurring revenue streams provides greater visibility into future performance. Meanwhile, the company has maintained disciplined cost control, with SG&A expenses consistently hovering around 6% of revenue despite the significant business expansion.

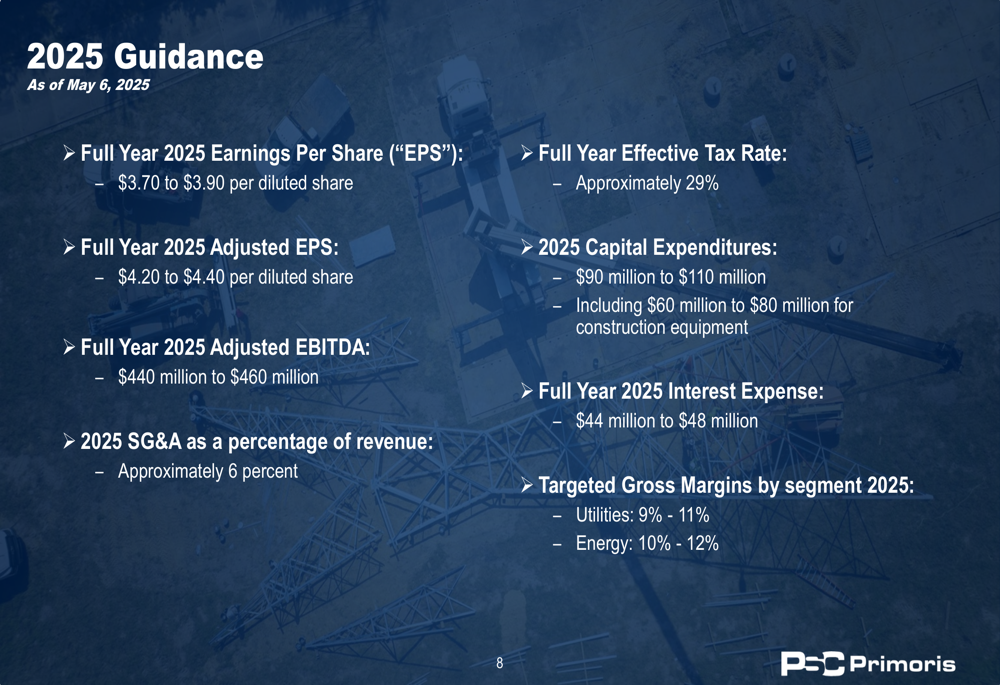

2025 Guidance and Outlook

Looking ahead, Primoris provided detailed financial guidance for the full year 2025:

The company expects full-year earnings per share between $3.70 and $3.90, with adjusted EPS ranging from $4.20 to $4.40. Adjusted EBITDA is projected to reach between $440 million and $460 million.

Primoris anticipates maintaining its SG&A expenses at approximately 6% of revenue while targeting gross margins of 9-11% in the Utilities segment and 10-12% in the Energy segment. Capital expenditures are expected to range from $90 million to $110 million, including $60-80 million specifically for construction equipment.

This guidance aligns with the company’s previous outlook shared during its Q4 2024 earnings report, suggesting management remains confident in its growth trajectory despite the slight dip in backlog during Q1. The continued expansion in renewable energy projects and power delivery services, combined with the stability provided by growing MSA revenue, positions Primoris to potentially deliver another year of strong financial performance in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.