European stocks retreat on tech valuation concerns; U.K. economic woes

Introduction & Market Context

Proact IT Group AB (STO:PACT) presented its Q1 2025 interim results on May 6, 2025, revealing a mixed performance with modest revenue growth but declining profitability. The company’s stock price has responded negatively, falling 5.31% to SEK 110.6 following the presentation, extending the decline that began after the initial earnings release.

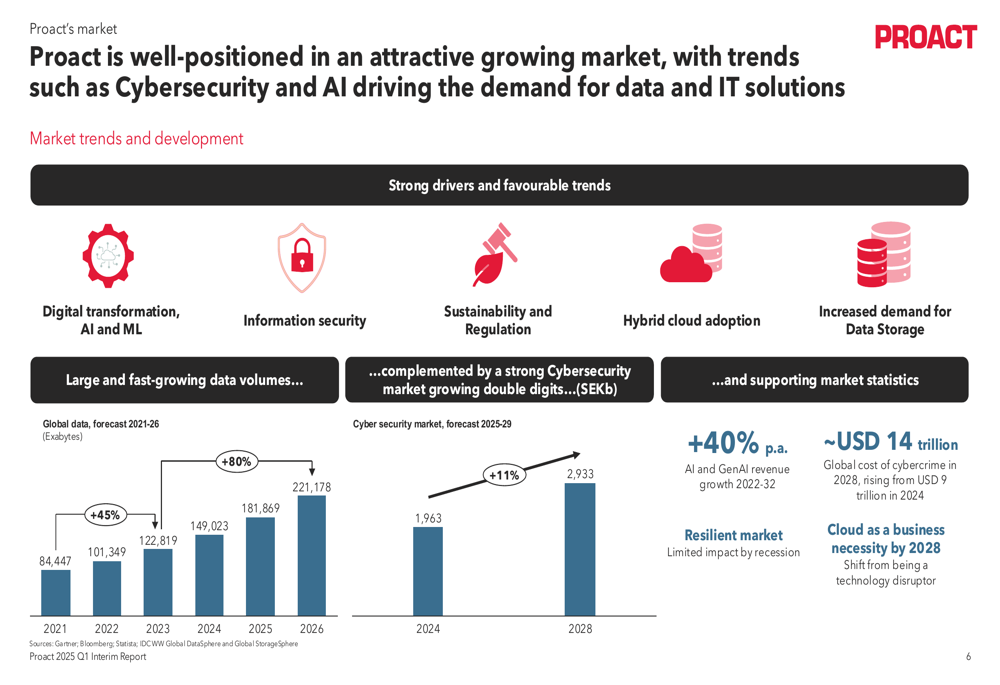

As a leading European IT services provider specializing in data management and hybrid cloud solutions, Proact operates in a growing market driven by digital transformation, AI adoption, and increasing cybersecurity concerns. The company highlighted that global data volume is forecast to grow by 80% from 2021 to 2026, while the cybersecurity market is expected to expand by 11% from 2024 to 2028.

As shown in the following market growth chart from the presentation:

Quarterly Performance Highlights

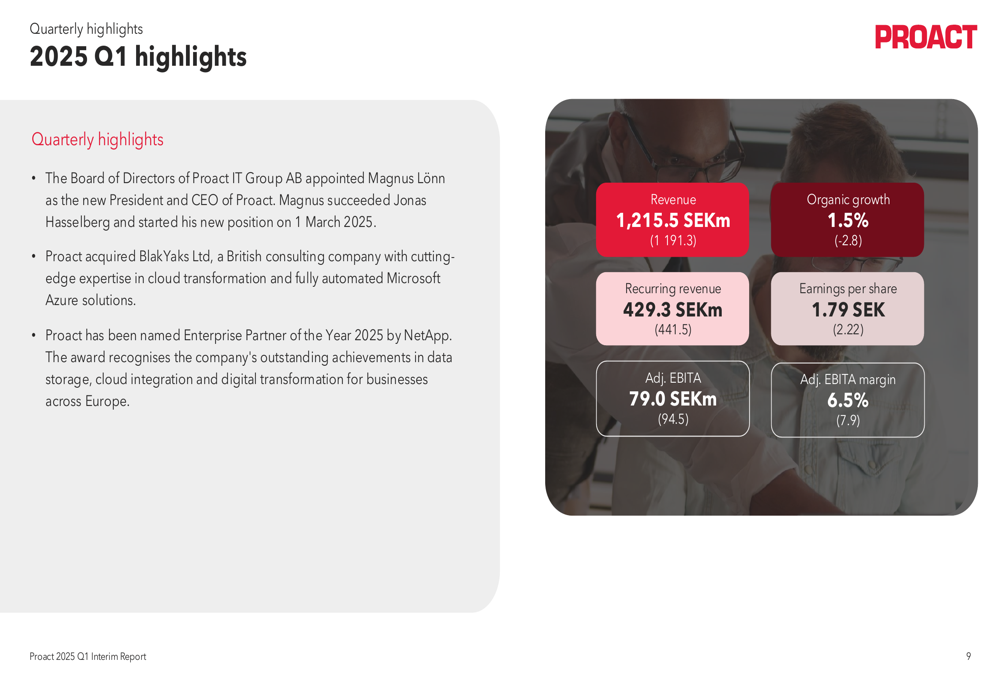

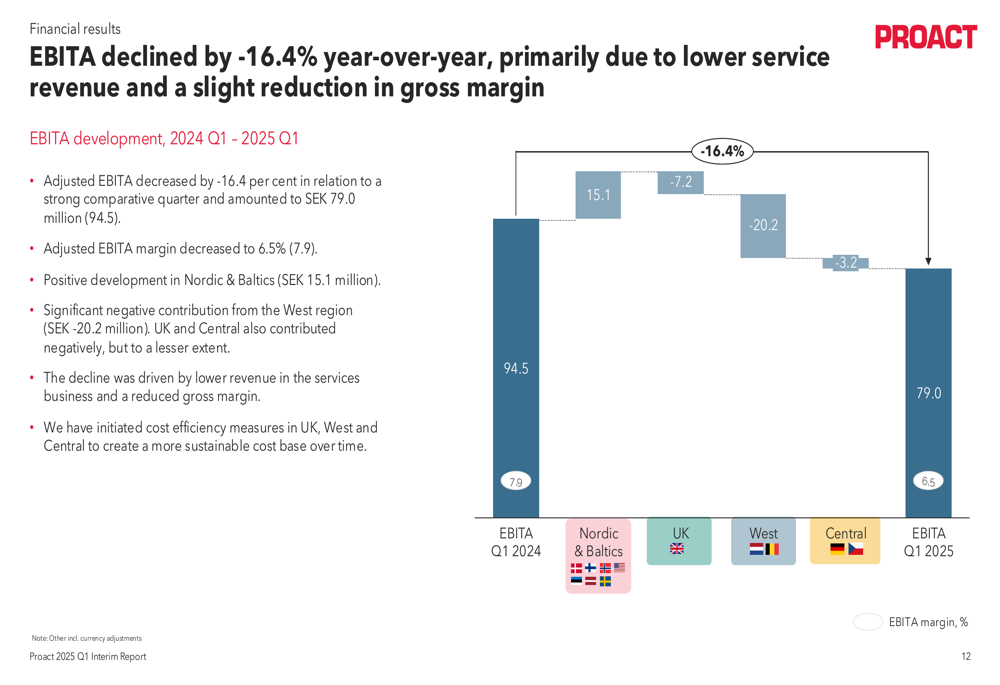

Proact reported Q1 2025 revenue of SEK 1,215.5 million, representing a 2.0% year-over-year increase, with organic growth of 1.5%. However, adjusted EBITA declined by 16.4% to SEK 79.0 million, resulting in an adjusted EBITA margin of 6.5%, which falls short of the company’s long-term target of 8%.

The quarter was marked by several notable developments, including the appointment of Magnus Lönn as President and CEO, the acquisition of BlakYaks Ltd in the UK to strengthen cloud transformation capabilities, and recognition as NetApp (NASDAQ:NTAP)’s Enterprise Partner of the Year 2025.

The following slide summarizes the key highlights from the quarter:

Detailed Financial Analysis

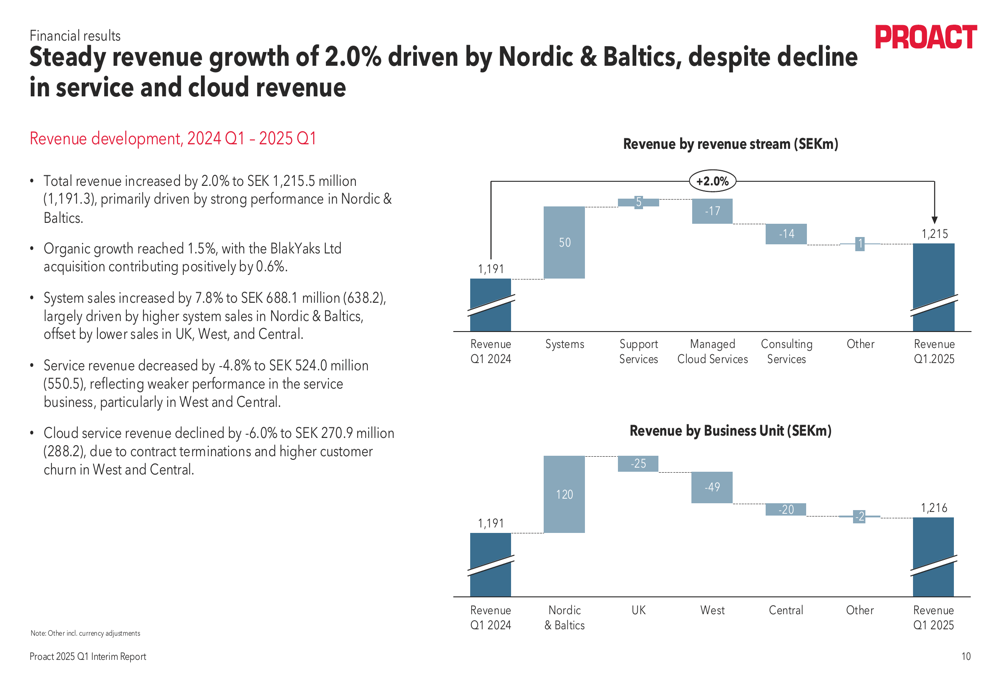

Proact’s revenue growth was primarily driven by a 7.8% increase in system sales to SEK 688.1 million, which offset a 4.8% decline in service revenue to SEK 524.0 million. Cloud service revenue, a strategic focus area for the company, decreased by 6.0% to SEK 270.9 million.

The company’s revenue breakdown by stream shows systems accounting for 57% of total revenue, followed by managed cloud services (22%), support services (13%), and consulting services (8%). This breakdown is illustrated in the following chart:

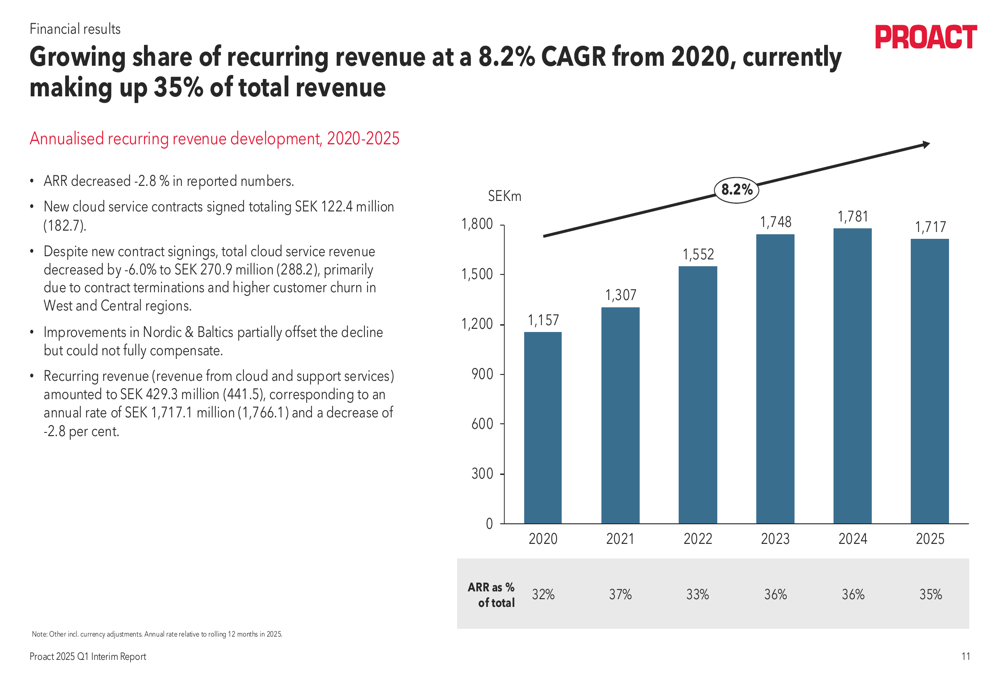

Annualized recurring revenue (ARR), a key metric for software and service companies, decreased by 2.8% to SEK 1,717 million, representing 35% of total revenue, down from 36% in the previous year. This decline in recurring revenue is concerning as it represents a reversal of the positive trend observed from 2020 to 2024.

The following chart illustrates the ARR development over time:

The decline in adjusted EBITA was primarily attributed to poor performance in the West and Central business units, which offset strong results in the Nordic & Baltics region. The waterfall chart below provides a clear visualization of these regional contributions to the overall EBITA decline:

Net cash position decreased significantly from SEK 330 million in Q4 2024 to SEK 101 million in Q1 2025. This reduction was largely due to M&A activities (SEK -206 million), working capital changes (SEK -57 million), and foreign exchange impacts (SEK -28 million).

Regional Performance Disparities

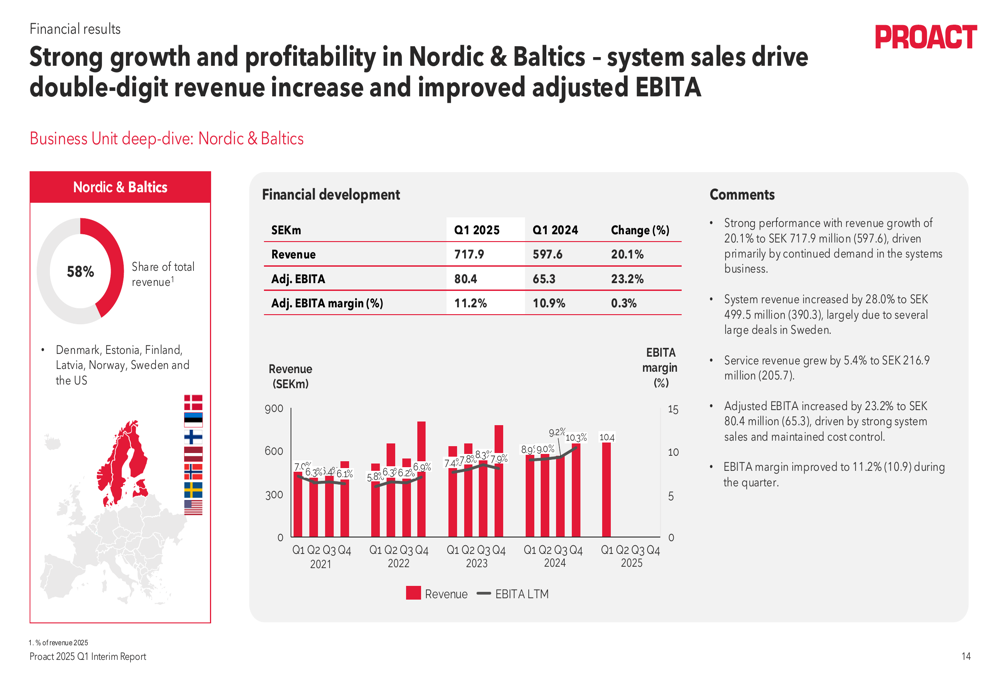

Proact’s performance varied dramatically across its four business units, with the Nordic & Baltics region delivering exceptional results while the other regions struggled.

The Nordic & Baltics business unit, which accounts for approximately 59% of total revenue, grew by 20.1% to SEK 717.9 million, with adjusted EBITA increasing by 23.2% to SEK 80.4 million. The adjusted EBITA margin improved to 11.2%, significantly above the company’s target of 8%.

The strong performance in the Nordic & Baltics region is illustrated in the following chart:

In stark contrast, the UK business unit saw revenue decline by 13.7% to SEK 158.8 million, with adjusted EBITA plummeting by 88.7% to just SEK 0.9 million. The adjusted EBITA margin fell to 0.6% from 4.4% in the previous year.

The West business unit, covering the Netherlands, Belgium, and Spain, experienced the most severe downturn, with revenue decreasing by 21.3% to SEK 180.5 million and adjusted EBITA turning negative at SEK -4.2 million, compared to a positive SEK 16.0 million in Q1 2024.

Similarly, the Central business unit, covering Germany, Austria, and Switzerland, reported a 9.7% revenue decline to SEK 182.5 million and a negative adjusted EBITA of SEK -1.1 million, down from a positive SEK 2.1 million in the previous year.

Strategic Initiatives and Outlook

Despite the challenging quarter, Proact remains focused on its long-term strategy centered around AI infrastructure, cloud transformation, and cybersecurity solutions. The company emphasized the growing importance of AI as a key technology reshaping IT infrastructure, noting that AI is driving a new wave of infrastructure investments.

Proact highlighted its comprehensive technology portfolio, which includes core infrastructure, data management, modern infrastructure, cybersecurity & resilience, and professional services. The company’s delivery models range from technology-only offerings to fully managed "as a service" solutions.

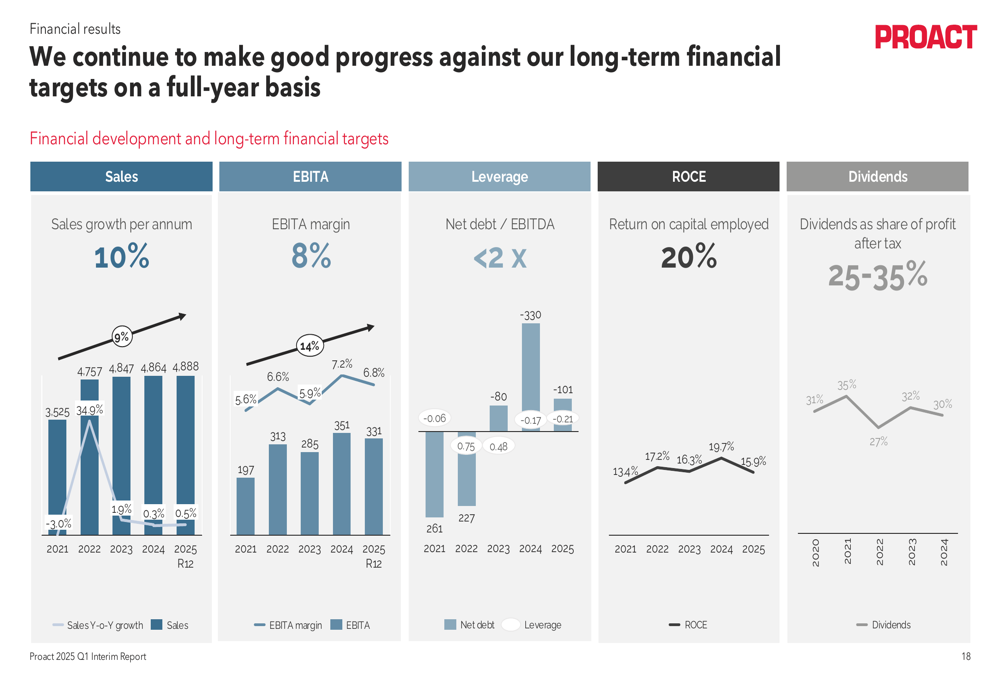

The company’s long-term financial targets remain unchanged: sales growth of 10% per annum, EBITA margin of 8%, net debt to EBITDA ratio below 2x, return on capital employed of 20%, and dividends representing 25-35% of profit after tax.

The following chart illustrates Proact’s progress toward these targets:

In summary, Proact’s Q1 2025 results reveal a company facing significant regional challenges despite overall revenue growth. The strong performance in the Nordic & Baltics region demonstrates the potential of the company’s business model, but the struggles in other regions highlight the need for operational improvements. As Proact continues to focus on high-growth areas like AI infrastructure and cloud services, investors will be watching closely to see if the company can address its profitability challenges and return to a trajectory that aligns with its long-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.