Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

PROG Holdings, Inc. (NYSE:PRG) presented its third-quarter 2025 earnings results on October 22, 2025, revealing a mixed performance characterized by slightly lower revenue but improved profitability metrics. Despite beating earnings expectations with a Non-GAAP EPS of $0.90 (exceeding forecasts by 21.62%), the company’s stock experienced a 3.76% decline in pre-market trading, reflecting investor concerns about future growth prospects amid challenging market conditions.

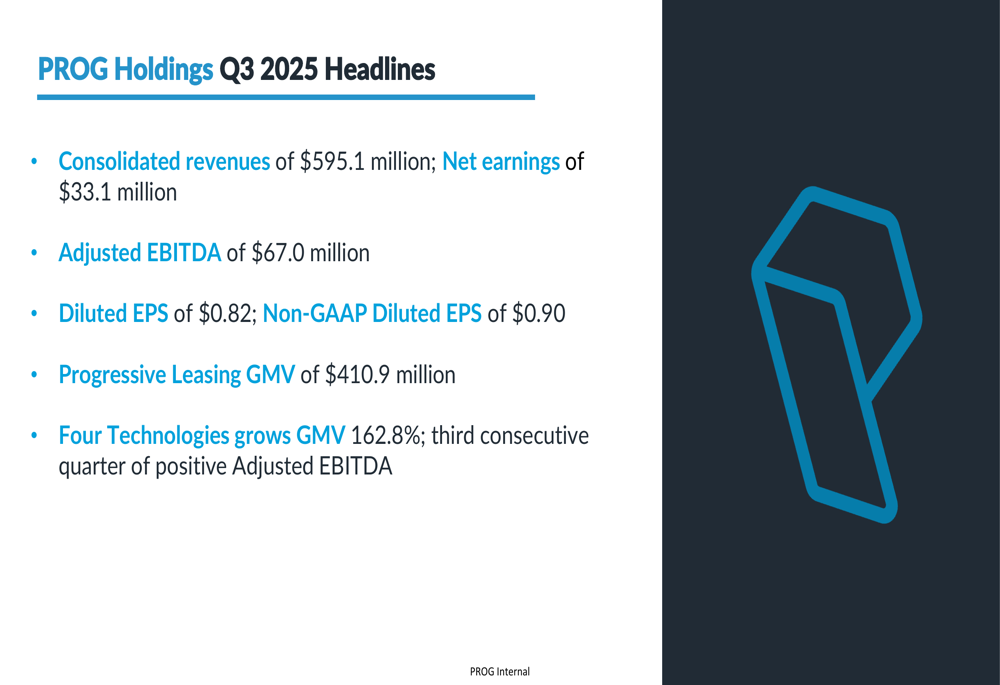

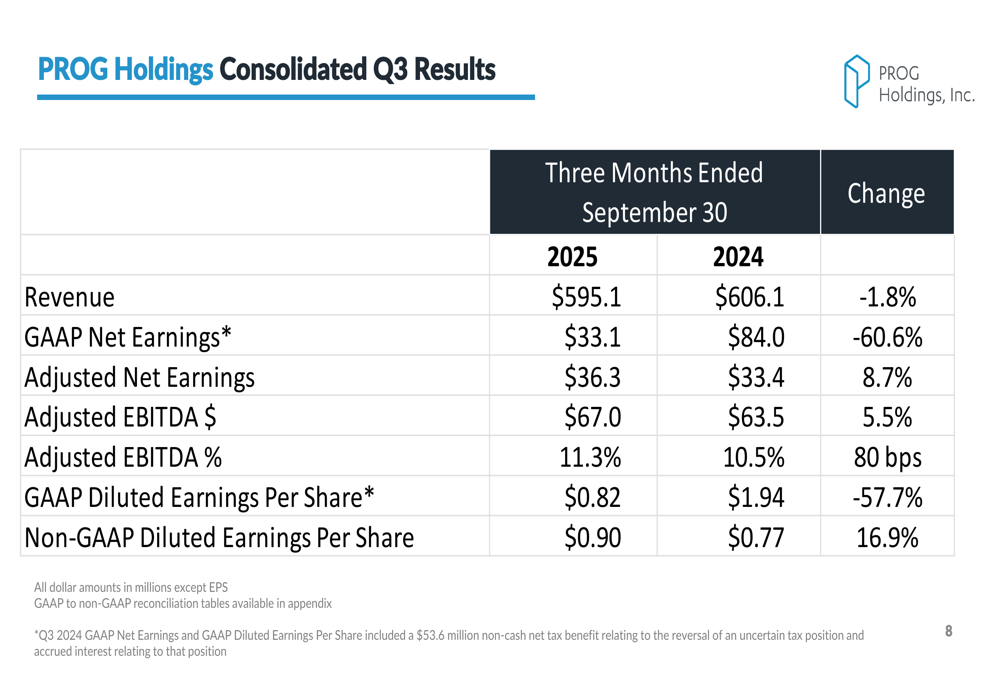

The company reported consolidated revenues of $595.1 million, representing a 1.8% year-over-year decline, while delivering net earnings of $33.1 million and adjusted EBITDA of $67.0 million. The presentation highlighted the company’s strategic shift, including the divestiture of its Vive Financial portfolio and continued focus on its core Progressive Leasing business alongside the rapidly growing Four Technologies segment.

Quarterly Performance Highlights

PROG Holdings delivered solid profitability improvements despite revenue headwinds in the third quarter. The company achieved a 16.9% year-over-year increase in Non-GAAP diluted earnings per share, reaching $0.90 compared to $0.77 in Q3 2024. Adjusted EBITDA grew by 5.5% to $67.0 million, with margins expanding from 10.5% to 11.3% of consolidated revenues.

As shown in the following key financial highlights from Q3 2025:

The company’s GAAP net earnings of $33.1 million represented a significant decline from the $84.0 million reported in Q3 2024. However, this comparison is skewed by a one-time $53.6 million non-cash tax benefit recorded in the prior-year period. When adjusted for this and other non-recurring items, adjusted net earnings actually increased by 8.7% year-over-year.

The detailed quarterly comparison reveals the company’s ability to improve profitability metrics despite revenue challenges:

Segment Analysis

Progressive Leasing

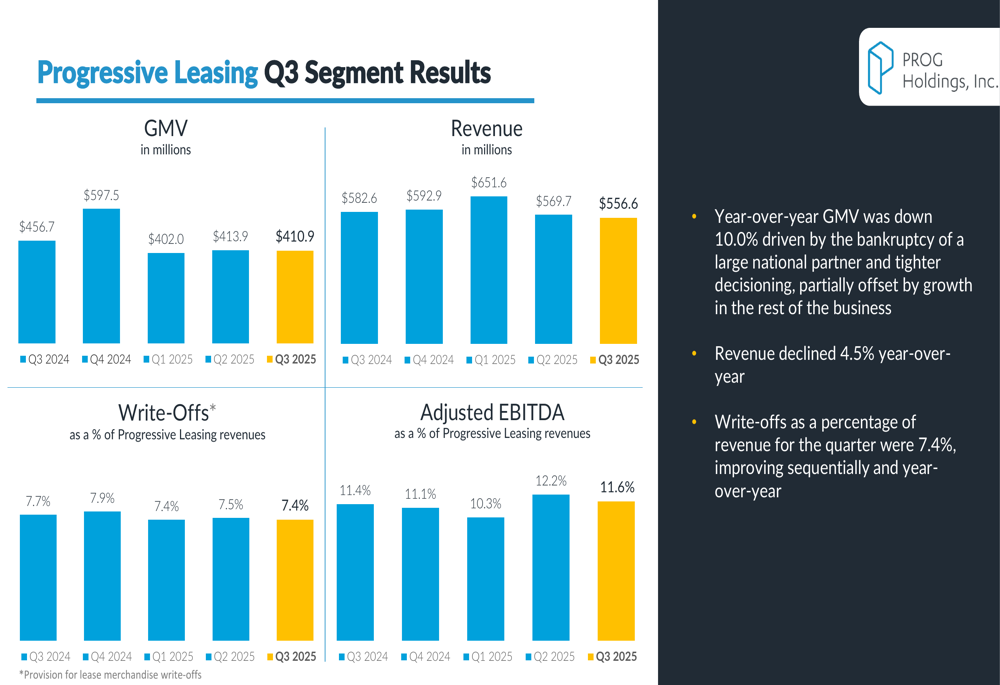

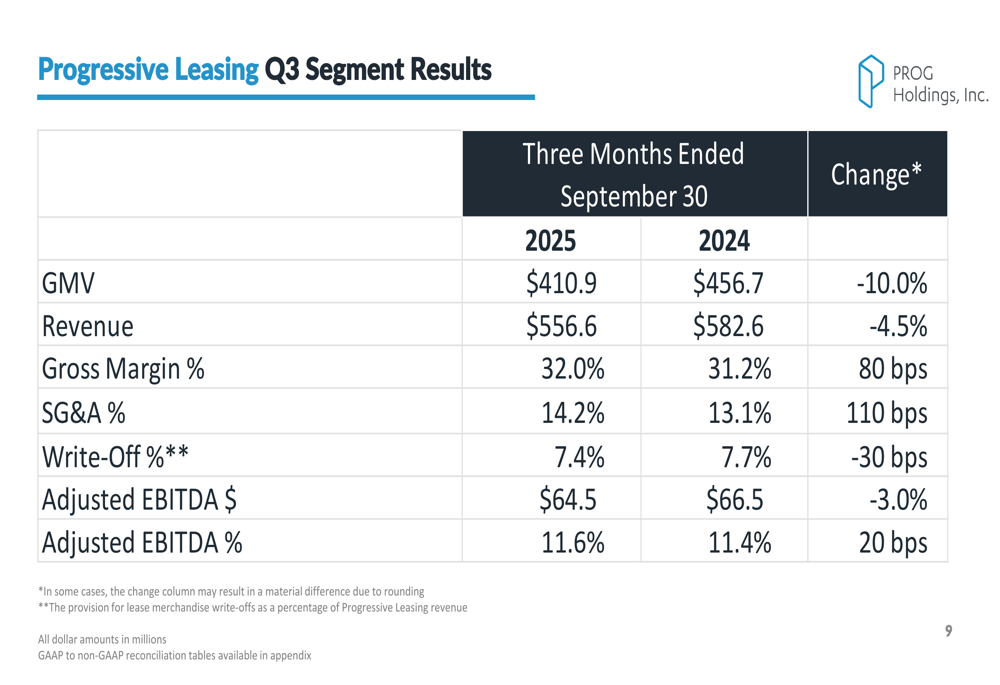

The company’s core Progressive Leasing segment faced headwinds in Q3 2025, with gross merchandise value (GMV) declining 10.0% year-over-year to $410.9 million. This decrease was primarily attributed to the bankruptcy of a large national partner and tighter decisioning criteria, partially offset by growth in the rest of the business. Segment revenue fell 4.5% to $556.6 million.

Despite these challenges, Progressive Leasing demonstrated improved operational efficiency, with write-offs as a percentage of revenue improving to 7.4% from 7.7% in the prior year. The segment also achieved gross margin expansion of 80 basis points to 32.0% and a slight improvement in Adjusted EBITDA margin to 11.6%.

The following chart illustrates Progressive Leasing’s quarterly performance trends:

A detailed breakdown of the segment’s financial performance shows the balance between revenue challenges and margin improvements:

Four Technologies

A bright spot in the company’s portfolio was Four Technologies, which achieved impressive growth with GMV increasing 162.8% year-over-year. The presentation highlighted that this was the third consecutive quarter of positive Adjusted EBITDA for this segment, demonstrating its increasing contribution to the company’s overall performance.

CEO Steve Michaels emphasized the segment’s momentum in his commentary: "Four Technologies delivered triple-digit GMV and revenue growth, continuing its strong performance trajectory." This growth helps offset some of the challenges faced by the Progressive Leasing segment and supports the company’s diversification strategy.

Financial Position and Capital Allocation

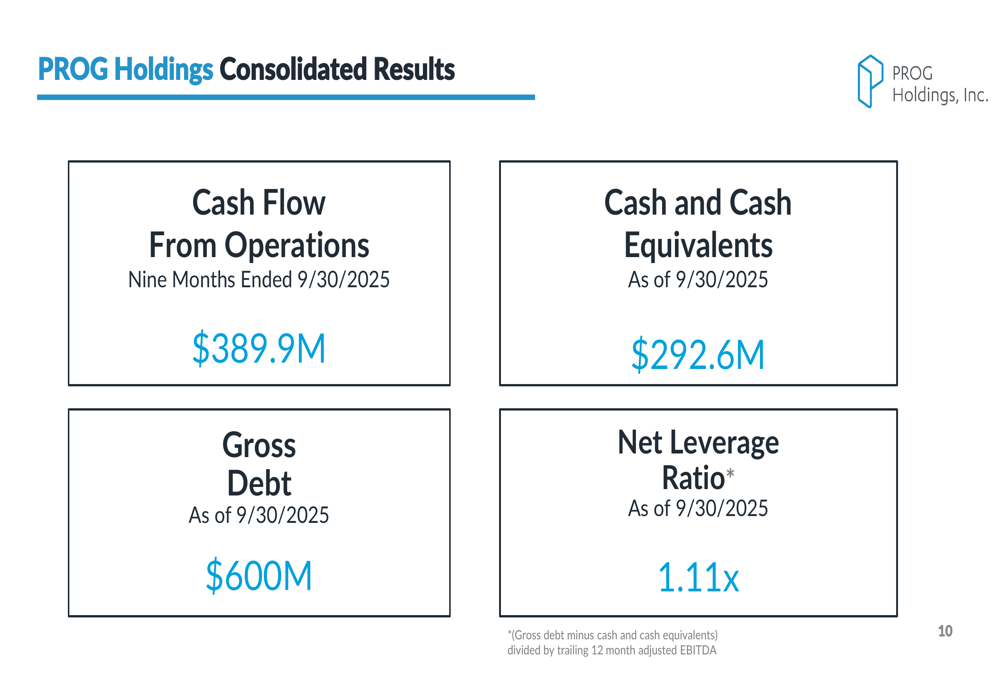

PROG Holdings maintained a strong financial position at the end of Q3 2025, with substantial cash flow generation and a conservative leverage profile. The company reported $389.9 million in cash flow from operations for the nine months ended September 30, 2025, and held $292.6 million in cash and cash equivalents.

The company’s balance sheet metrics reflect its financial strength:

With a gross debt of $600 million and a net leverage ratio of 1.11x, PROG Holdings maintains significant financial flexibility to pursue strategic initiatives, including potential share repurchases. The company’s strong cash position and cash flow generation capability provide a solid foundation for navigating the challenging operating environment while continuing to invest in growth opportunities.

Strategic Initiatives

A key strategic development highlighted in the presentation was the completion of the sale of the Vive Financial portfolio. This divestiture aligns with the company’s stated focus on "high-impact businesses and products" and its capital allocation strategy.

CEO Steve Michaels commented on the company’s strategic direction: "We are focused on high-impact businesses and products and capital allocation strategy. Our team is well positioned to deliver sustainable growth in 2026 and beyond."

The strategic shift toward the company’s core Progressive Leasing business and the rapidly growing Four Technologies segment reflects management’s efforts to optimize the portfolio and concentrate resources on the most promising growth opportunities.

Forward-Looking Statements

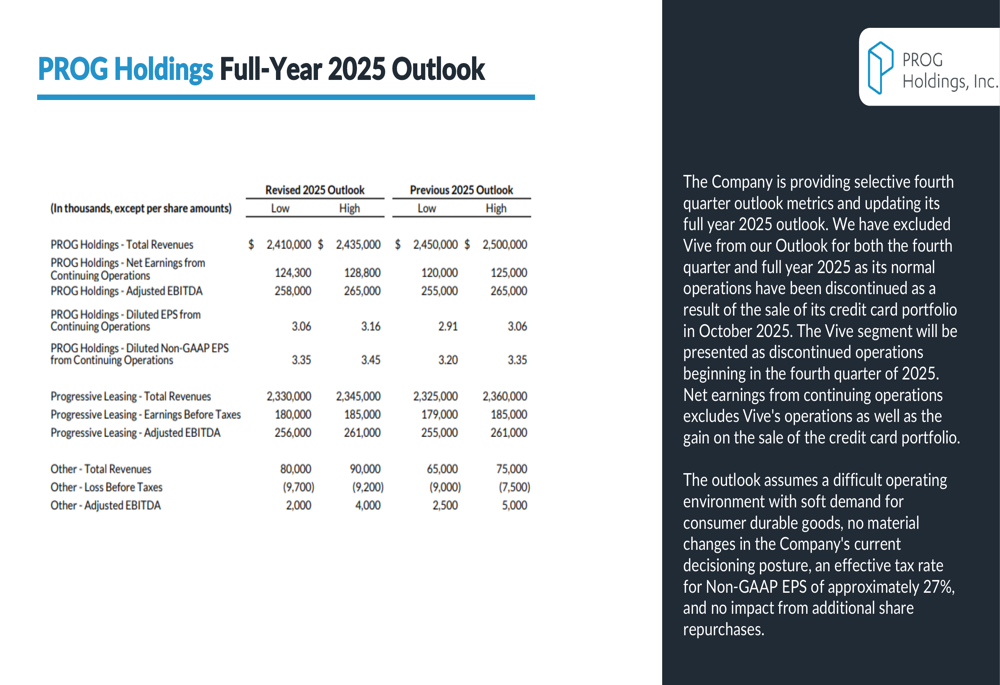

PROG Holdings provided an updated outlook for the remainder of 2025, projecting full-year revenues between $2.41 billion and $2.435 billion, with adjusted EBITDA expected to range from $258 million to $265 million. The company anticipates diluted non-GAAP EPS from continuing operations to be between $3.35 and $3.45.

The detailed outlook for full-year 2025 shows the company’s expectations across key metrics:

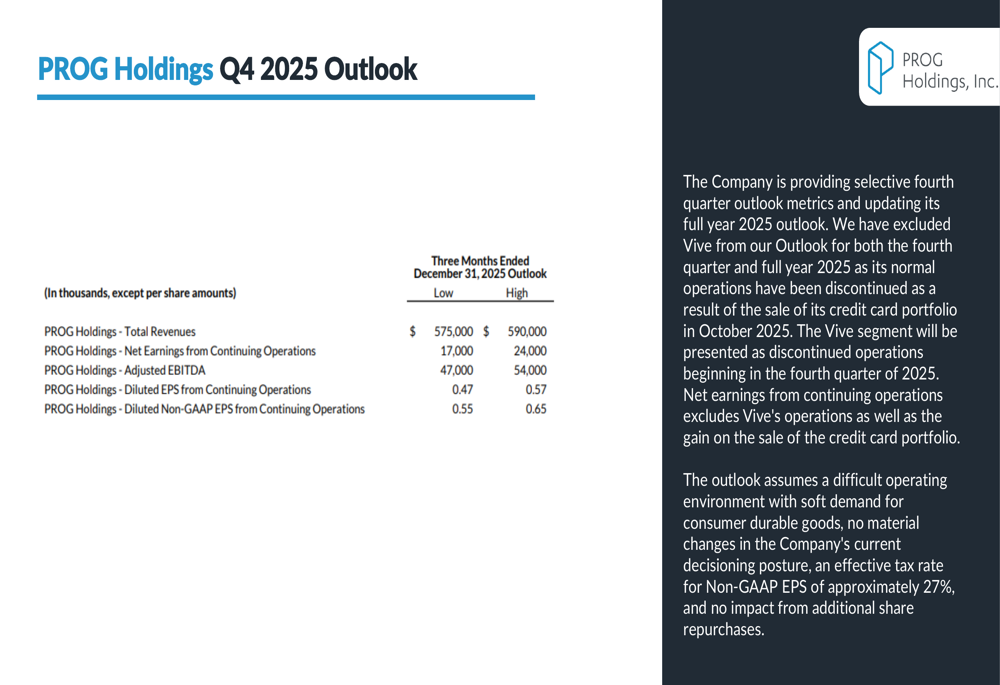

For the fourth quarter of 2025, the company projects total revenues between $575 million and $590 million, with diluted non-GAAP EPS from continuing operations expected to range from $0.55 to $0.65.

Management noted that this outlook assumes a continued difficult operating environment, no material changes in decisioning posture, and an effective tax rate for non-GAAP EPS of approximately 27%. The guidance also excludes any impact from additional share repurchases, suggesting potential upside if the company continues its buyback program.

Despite near-term challenges, CEO Steve Michaels expressed confidence in the company’s positioning, stating that the team is "well positioned to deliver sustainable growth in 2026 and beyond," reflecting a longer-term optimistic outlook beyond the current challenging environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.