Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Progress Software Corporation (NASDAQ:PRGS) released its Q2 2025 financial results on June 30, 2025, showcasing solid performance with revenue in line with guidance and earnings per share exceeding expectations. The company’s stock rose 2.24% in after-hours trading to $65.19, reflecting positive investor sentiment toward the results and raised full-year outlook.

The infrastructure software provider continues to demonstrate the success of its acquisition strategy, particularly with ShareFile integration proceeding ahead of schedule. This quarter’s results build on the momentum seen in Q1 2025, when the company reported a 48% year-over-year increase in ARR and significantly beat earnings expectations.

Q2 2025 Performance Highlights

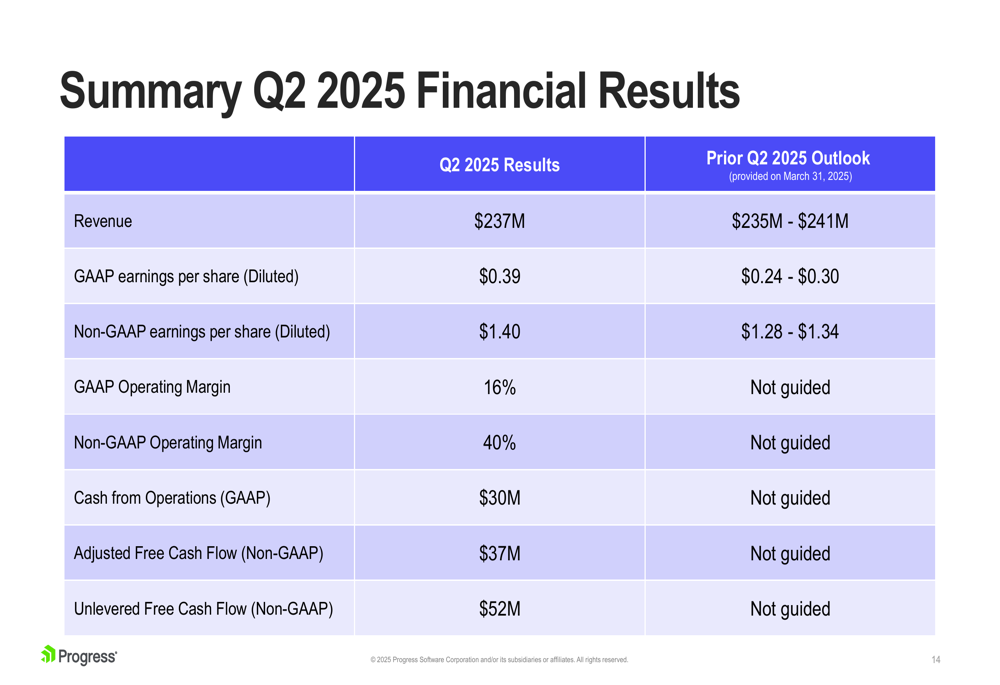

Progress reported Q2 2025 revenue of $237 million, within the company’s prior guidance range of $235-$241 million. Non-GAAP earnings per share reached $1.40, exceeding the high end of previous guidance of $1.28-$1.34. The company maintained its strong profitability with a non-GAAP operating margin of 40%.

As shown in the following summary of Q2 2025 financial results:

The company’s GAAP earnings per share came in at $0.39, also above the prior outlook of $0.24-$0.30. Cash from operations totaled $30 million for the quarter, while adjusted free cash flow reached $37 million and unlevered free cash flow hit $52 million.

ARR Growth and ShareFile Integration

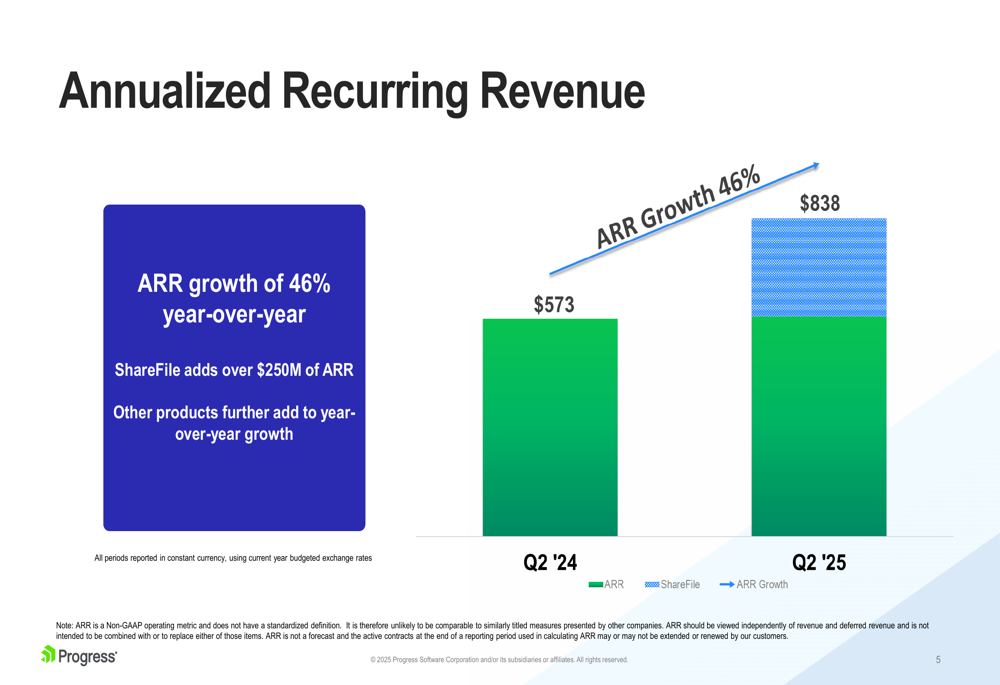

The most notable achievement in Q2 was the 46% year-over-year growth in Annualized Recurring Revenue (ARR), which reached $838 million. This growth was largely driven by the ShareFile acquisition, which contributed over $250 million in ARR. The company maintained a net retention rate of 100%, indicating stable customer relationships.

The following chart illustrates the significant impact of ShareFile on Progress’s ARR growth:

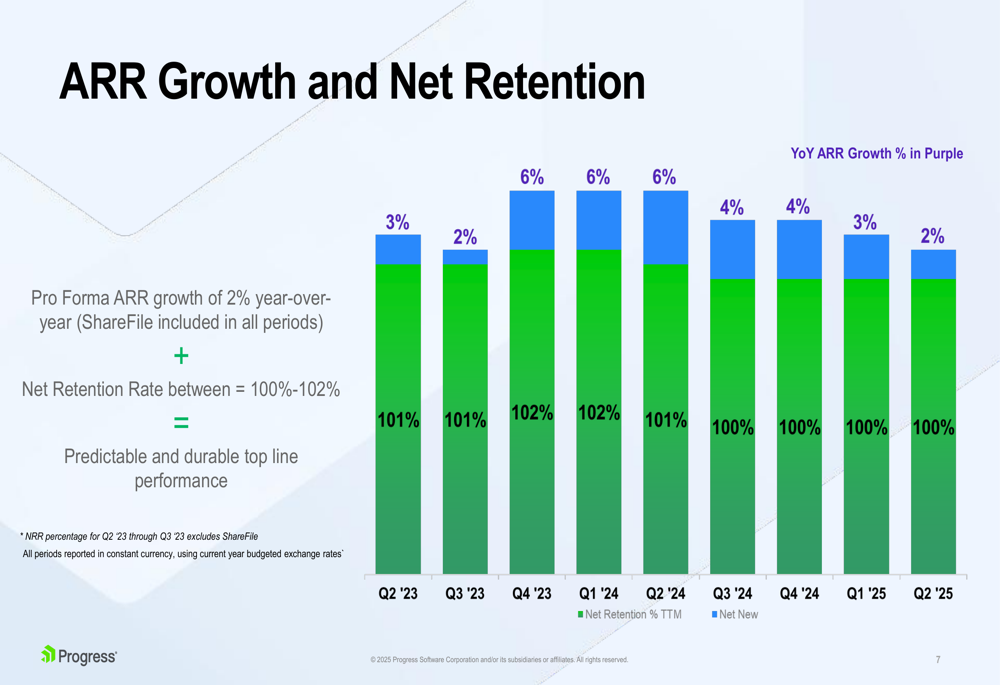

When examining ARR on a pro forma basis (with ShareFile included in all periods), Progress achieved 2% year-over-year growth. The company has maintained consistent ARR growth over multiple quarters, as shown in this trend chart:

The relationship between ARR growth and net retention rate provides insight into the company’s ability to both retain existing customers and expand its customer base:

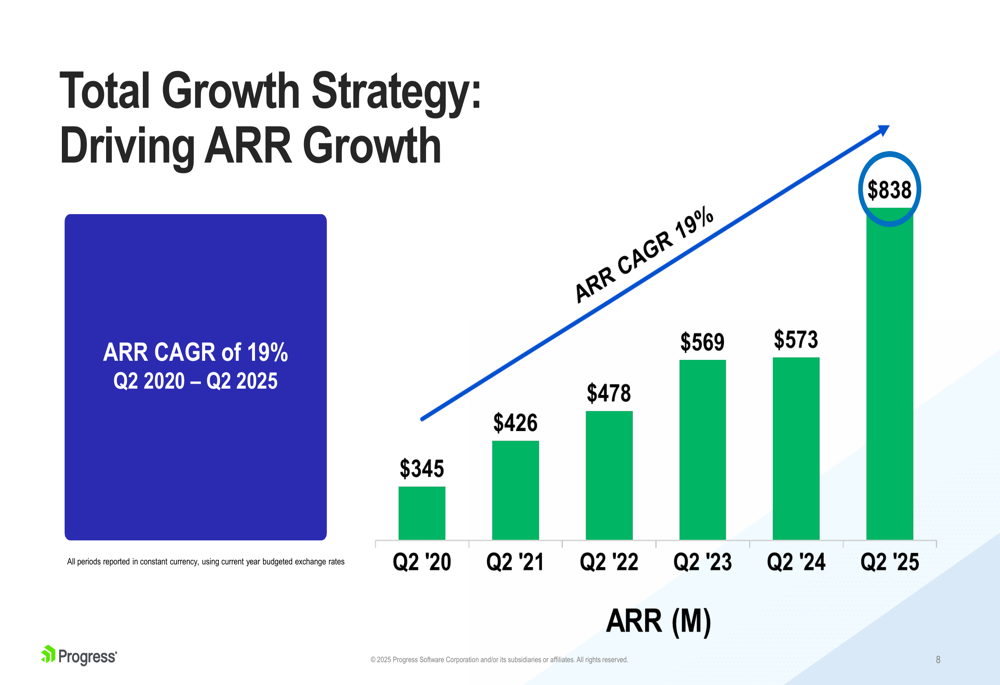

Looking at a longer time horizon, Progress has achieved an impressive 19% CAGR in ARR from Q2 2020 through Q2 2025, demonstrating the effectiveness of its growth strategy:

Long-Term Growth Strategy

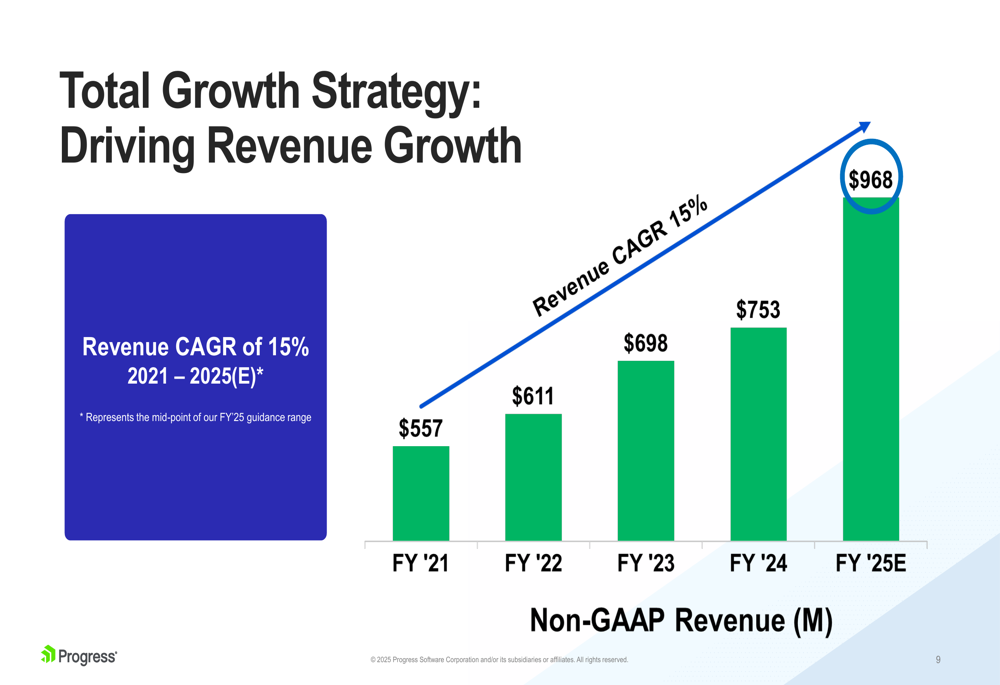

Progress’s long-term growth strategy has delivered consistent results across multiple financial metrics. The company has achieved a 15% revenue CAGR from 2021 to 2025 (estimated), as illustrated in the following chart:

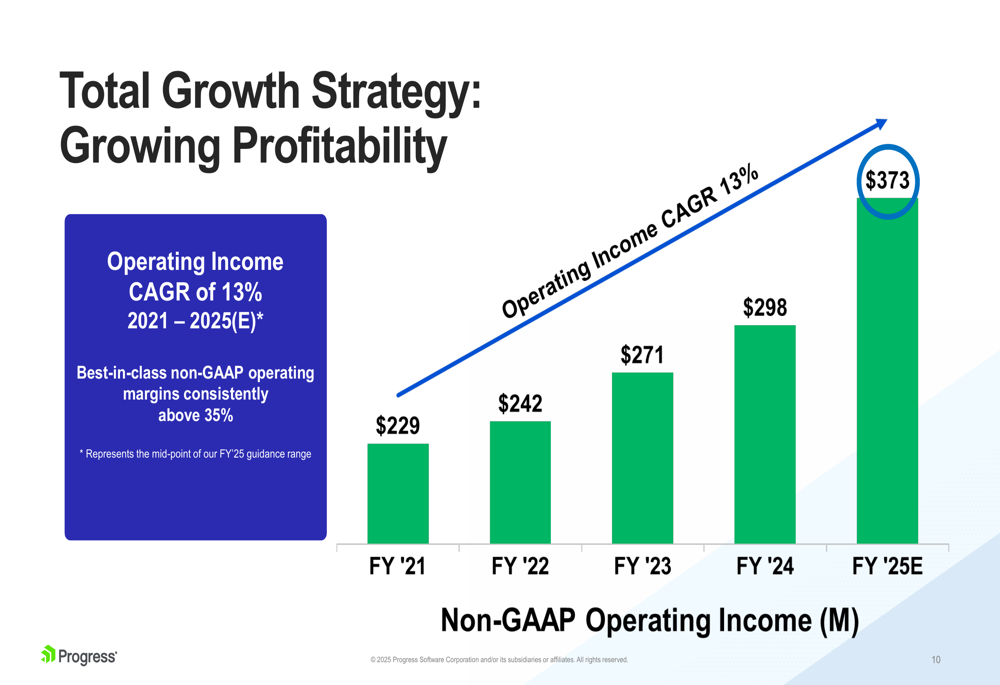

This revenue growth has translated into strong profitability, with operating income growing at a 13% CAGR over the same period. The company highlights its "best-in-class" non-GAAP operating margins, which have consistently remained above 35%:

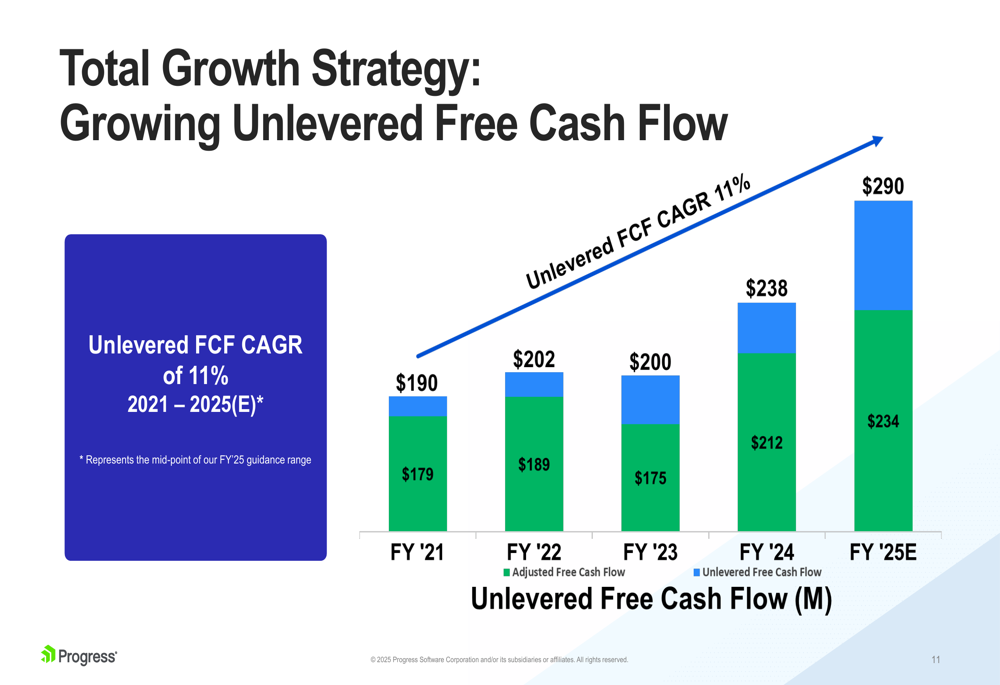

The growth in revenue and operating income has also driven an 11% CAGR in unlevered free cash flow from 2021 to 2025 (estimated):

Updated Guidance and Outlook

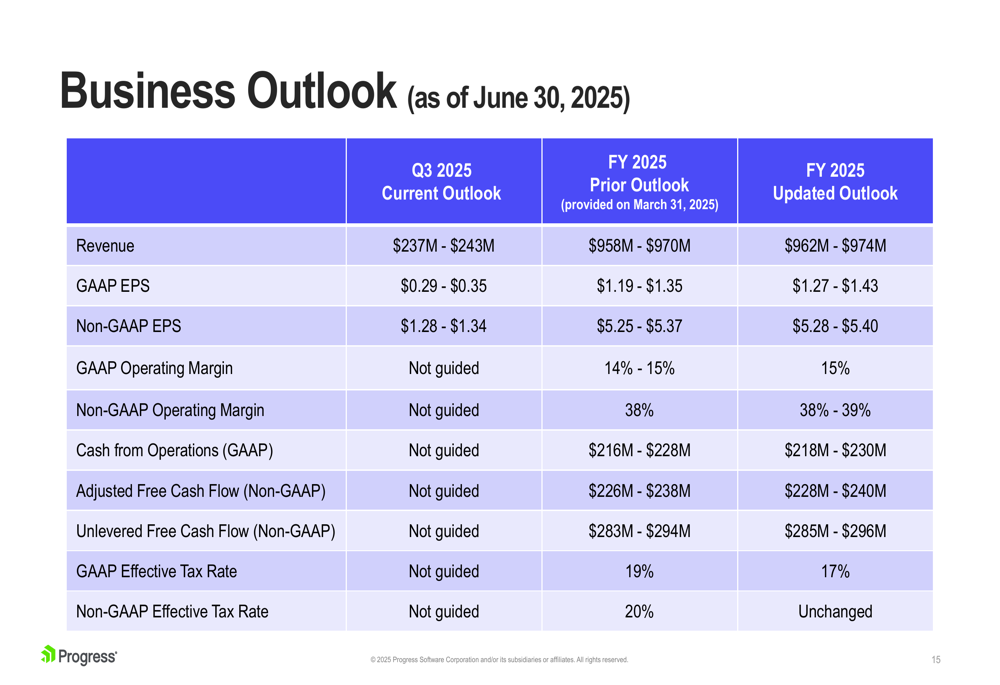

Based on its strong Q2 performance, Progress has raised its full-year 2025 guidance for both revenue and earnings per share. The company now expects FY 2025 revenue between $962-$974 million, up from the previous range of $958-$970 million. Non-GAAP EPS guidance has been increased to $5.28-$5.40, compared to the prior outlook of $5.25-$5.37.

For Q3 2025, Progress expects revenue between $237-$243 million and non-GAAP EPS of $1.28-$1.34. The company also raised its non-GAAP operating margin guidance for the full year to 38-39%, up from 38% previously.

The following table provides a comprehensive view of the updated business outlook:

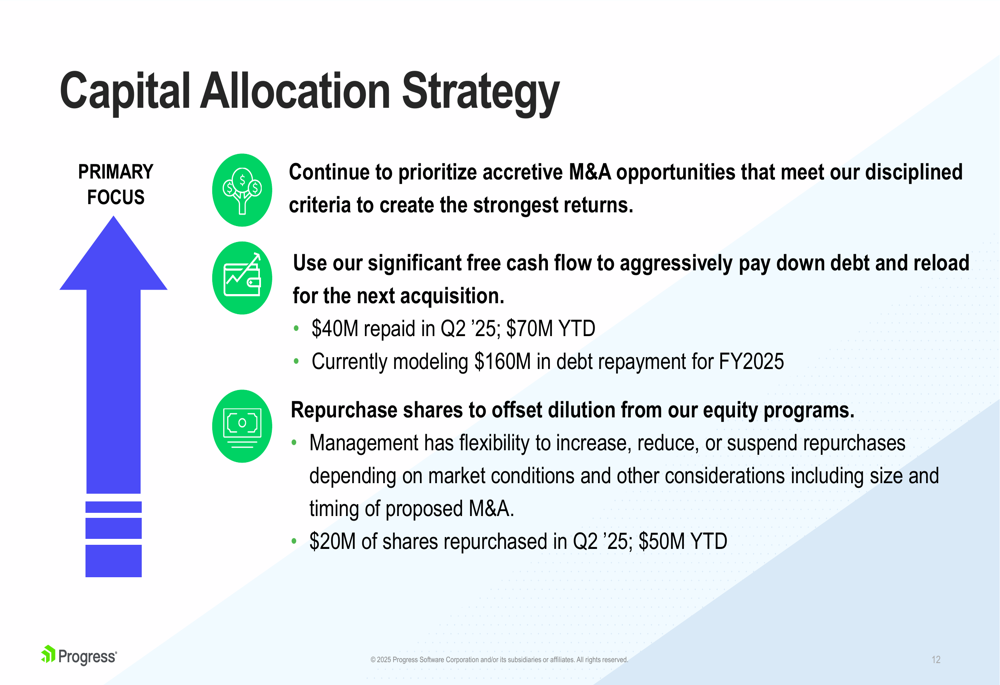

Capital Allocation Strategy

Progress continues to execute its disciplined capital allocation strategy, focusing on three key areas: accretive M&A opportunities, debt repayment, and share repurchases. In Q2 2025, the company repaid $40 million in debt (bringing the year-to-date total to $70 million) and repurchased $20 million in shares (year-to-date total of $50 million).

For the full fiscal year 2025, Progress is modeling approximately $160 million in debt repayment, demonstrating its commitment to strengthening its balance sheet while maintaining flexibility for future acquisitions.

The company’s M&A framework remains focused on end market alignment, appropriate sizing (targeting acquisitions representing 10-25% of current revenues), strong financial characteristics, and ensuring returns on invested capital exceed weighted average cost of capital.

As shown in the company’s capital allocation strategy slide:

Supplemental Revenue Information

Progress’s revenue mix continues to evolve, with SaaS revenue showing significant growth. In Q2 2025, SaaS revenue reached $72.1 million, compared to just $6.0 million in Q2 2024, reflecting the impact of the ShareFile acquisition. Maintenance revenue remained stable at $103.5 million, while license revenue declined slightly to $50.8 million.

From a geographic perspective, North America continues to be the largest market, accounting for $147.3 million in Q2 2025 revenue, followed by EMEA at $73.0 million. The Asia Pacific region showed strong year-over-year growth, reaching $12.1 million in Q2 2025 compared to $10.0 million in Q2 2024.

These results reinforce Progress Software’s position as a stable performer in the infrastructure software space, with its acquisition strategy continuing to drive growth in recurring revenue while maintaining strong profitability and cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.