UnitedHealth tests AI system to streamline medical claims processing - Bloomberg

Introduction & Market Context

Prologis Inc (NYSE:PLD), the global leader in logistics real estate, released its third quarter 2025 supplemental information on October 15, revealing strong financial performance that exceeded analyst expectations. The company, which owns or has investments in properties totaling approximately 1.3 billion square feet across 20 countries, saw its stock price surge 6.59% following the announcement, reflecting positive investor sentiment.

With a market capitalization of $115.7 billion, Prologis continues to leverage its dominant position in high-barrier, high-growth markets while expanding strategically into data centers and renewable energy. The company’s portfolio serves approximately 6,500 customers, with operations heavily concentrated in the United States, which accounts for 85% of its net operating income (NOI).

As shown in the following company profile breakdown, Prologis maintains a significant global footprint while deriving the majority of its revenue from U.S. operations:

Quarterly Performance Highlights

Prologis reported total revenues of $2.21 billion for Q3 2025, slightly above the $2.05 billion reported in the earnings announcement. Net earnings attributable to common stockholders reached $763 million, with earnings per share of $0.82, exceeding analyst expectations of $0.67 by 22.39%.

The company’s core funds from operations (FFO), a key metric for REITs, totaled $1.43 billion ($1.49 per share), while adjusted funds from operations (AFFO) reached $1.06 billion. These results demonstrate Prologis’ continued ability to generate substantial cash flow from its extensive portfolio.

The following chart illustrates the company’s detailed financial performance for the quarter:

Prologis’ performance shows consistent growth over recent years, with net earnings, core FFO, and AFFO all trending upward. The company’s dividend distributions have also increased steadily, reflecting its commitment to returning value to shareholders.

Operational Performance

While Prologis maintains a strong operational position, its occupancy rate slightly decreased to 94.7% in Q3 2025 compared to 96.1% in Q3 2024. This represents a minor decline but remains within the company’s guided range. However, the earnings announcement reported portfolio occupancy at 95.3%, up 20 basis points, suggesting a potential discrepancy or different measurement methodology.

Despite this slight occupancy fluctuation, Prologis demonstrated robust leasing activity with 62 million square feet signed during the quarter, according to the earnings call. The company continues to maintain strong pricing power, as evidenced by positive rent changes on both a net effective and cash basis.

The following chart shows Prologis’ occupancy trends and rent change metrics:

Customer diversification remains a strength for Prologis, with its largest tenant, Amazon, accounting for 4.9% of net effective rent. Other major customers include Home Depot (1.8%), FedEx (1.4%), DHL (1.2%), and DSV (1.1%). This diversified tenant base helps mitigate concentration risk while providing stable rental income.

As illustrated in the following breakdown of top customers and lease expirations:

Strategic Initiatives

Prologis continues to invest in development activities, with $169 million in value creation from development stabilizations during Q3 2025. The company maintains a substantial land bank with an estimated build-out value of $42.3 billion, providing significant runway for future growth.

A notable strategic focus is the company’s expansion into data centers and renewable energy. During the earnings call, the company’s President emphasized strong demand for their data center capabilities, stating, "Every megawatt we can deliver over the next three years is already in dialogue with customers."

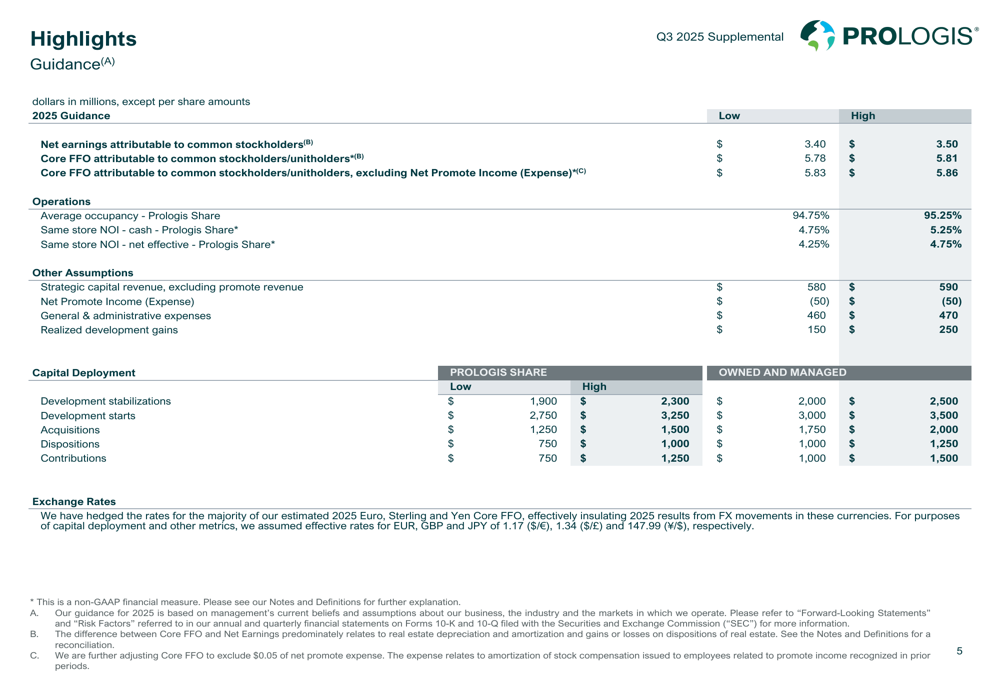

The company’s guidance for 2025 reflects confidence in its strategic direction:

Prologis expects development stabilizations between $2.0-2.5 billion and development starts of $3.0-3.5 billion for 2025, indicating continued investment in growth opportunities. Acquisitions are projected at $1.75-2.0 billion, while dispositions and contributions are expected to total $2.0-2.75 billion, suggesting a balanced approach to portfolio management.

Capital Structure and Financial Position

Prologis maintains a strong financial position with a well-structured debt profile and ample liquidity. The company’s capitalization strategy focuses on maintaining investment-grade ratings while optimizing its capital structure to support growth initiatives.

The following overview highlights Prologis’ debt metrics and capital allocation:

With $5.1 billion in liquidity and a weighted average interest rate of 2.7%, Prologis is well-positioned to navigate the current interest rate environment while pursuing strategic opportunities. The company’s debt-to-market capitalization ratio stands at 18.5%, reflecting a conservative leverage profile.

Forward-Looking Statements

Prologis’ management expressed optimism about the company’s future prospects during the earnings call. The outgoing CEO emphasized that "the best years of Prologis are still ahead of it," highlighting the company’s growth potential and strategic positioning.

For full-year 2025, Prologis expects net earnings per share between $3.40-$3.50 and core FFO per share of $5.78-$5.81. Average occupancy is projected at 94.75%-95.25%, with same-store NOI growth of 4.75%-5.25% on a cash basis.

The company anticipates continued strength in rental rates, with guidance suggesting rent changes in the low 50% range according to the earnings call. This outlook reflects confidence in Prologis’ ability to maintain pricing power despite macroeconomic uncertainties.

While the company faces potential challenges including supply chain disruptions, market saturation in key regions, and increased competition in the data center space, its diversified portfolio, strong balance sheet, and strategic focus on high-growth sectors position it well for sustained performance.

As Prologis continues to execute its growth strategy while maintaining operational excellence, investors appear to be responding positively, as evidenced by the stock’s 6.59% increase following the earnings announcement and its current trading near the 52-week high of $127.65.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.