Nvidia demand continues to outweigh supply, JPMorgan says

Introduction & Market Context

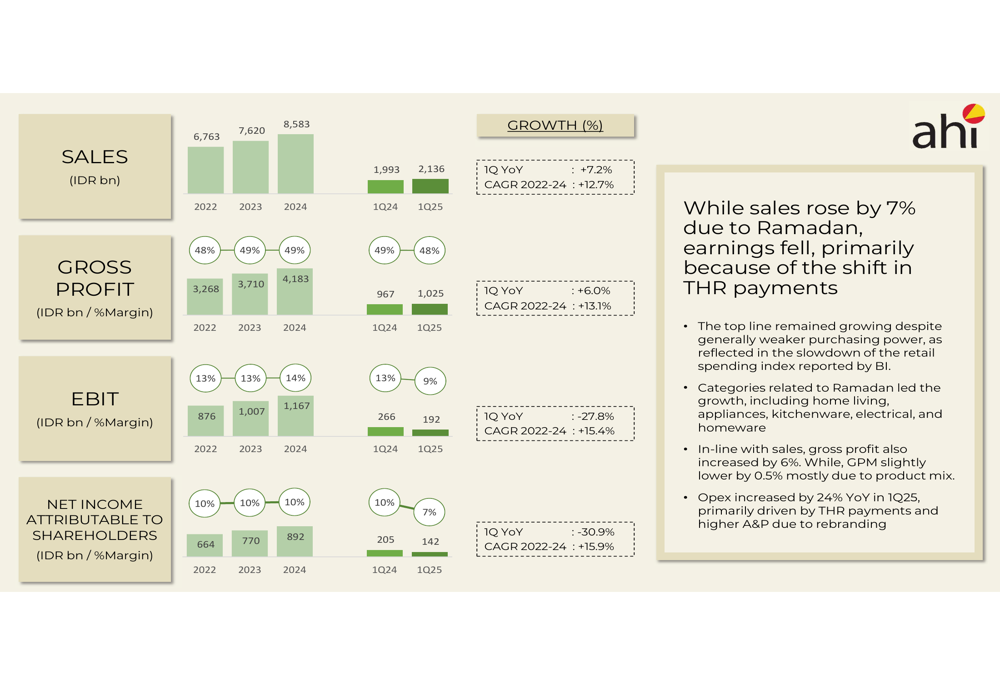

PT Aspirasi Hidup Indonesia Tbk (ACES.IJ), a leading home improvement and lifestyle retailer in Indonesia, presented its Q1 2025 financial results on May 2, 2025, revealing a mixed performance. The company reported sales growth of 7.2% year-over-year, reaching 2.1 trillion IDR, while net profit attributable to shareholders declined by 30.9% to 142 billion IDR. The earnings decline was primarily attributed to the timing of holiday allowance (THR) payments and increased advertising expenses related to the company’s extensive rebranding campaign.

As a member of the Kawan Lama Group with 70 years of industry experience, PT Aspirasi Hidup Indonesia operates 249 stores across 61 cities in 30 Indonesian provinces, offering over 50,000 SKUs through its retail brands Azko, Toys Kingdom (TADAWUL:4280), Ataru, and Pendopo.

Quarterly Performance Highlights

The company’s Q1 2025 financial performance showed continued top-line growth but significant pressure on profitability metrics:

Gross profit increased by 6.0% year-over-year to 1.025 trillion IDR, with gross margin slightly decreasing to 48% from 49% in Q1 2024. However, operating profit (EBIT) declined sharply by 27.8% to 192 billion IDR, resulting in an EBIT margin contraction from 13% to 9%. Net profit attributable to shareholders fell by 30.9% to 142 billion IDR, with net margin decreasing from 10% to 7%.

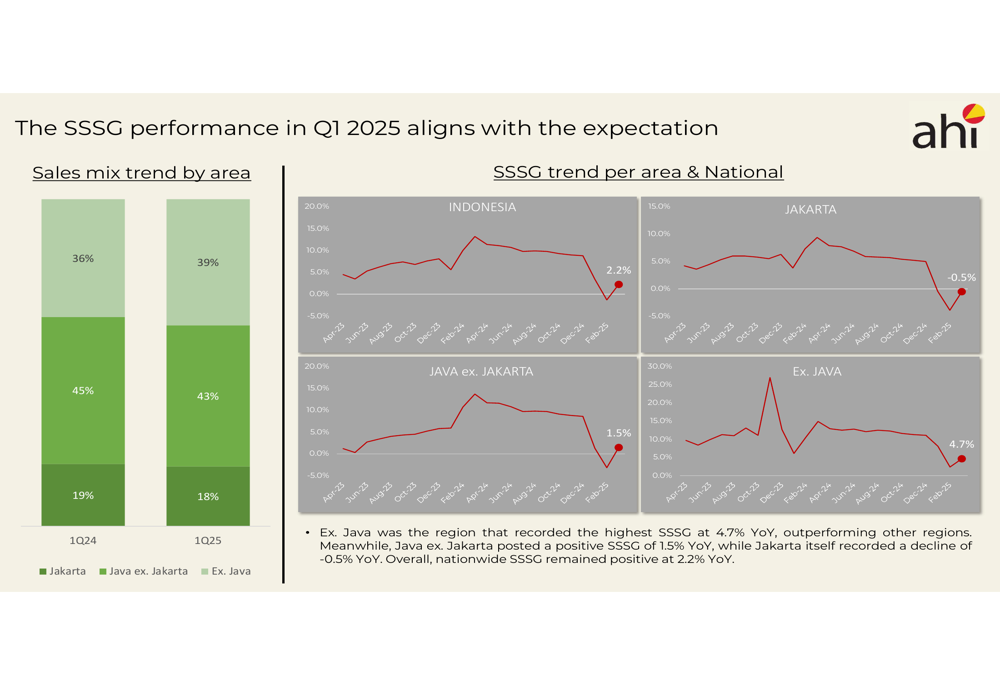

The company’s sales mix remained relatively stable, with Home Improvements accounting for 53% of sales, Lifestyle products at 42%, and Toys at 5%.

Same-Store Sales Growth (SSSG) performance varied significantly by region, with an overall positive nationwide growth of 2.2% year-over-year:

Notably, regions outside Java recorded the highest SSSG at 4.7% year-over-year, outperforming other areas. Java excluding Jakarta posted a positive SSSG of 1.5%, while Jakarta itself experienced a slight decline of 0.5%. The sales mix by region showed Jakarta accounting for 39% of sales in Q1 2025 (up from 36% in Q1 2024), Java excluding Jakarta at 43% (down from 45%), and regions outside Java at 18% (down from 19%).

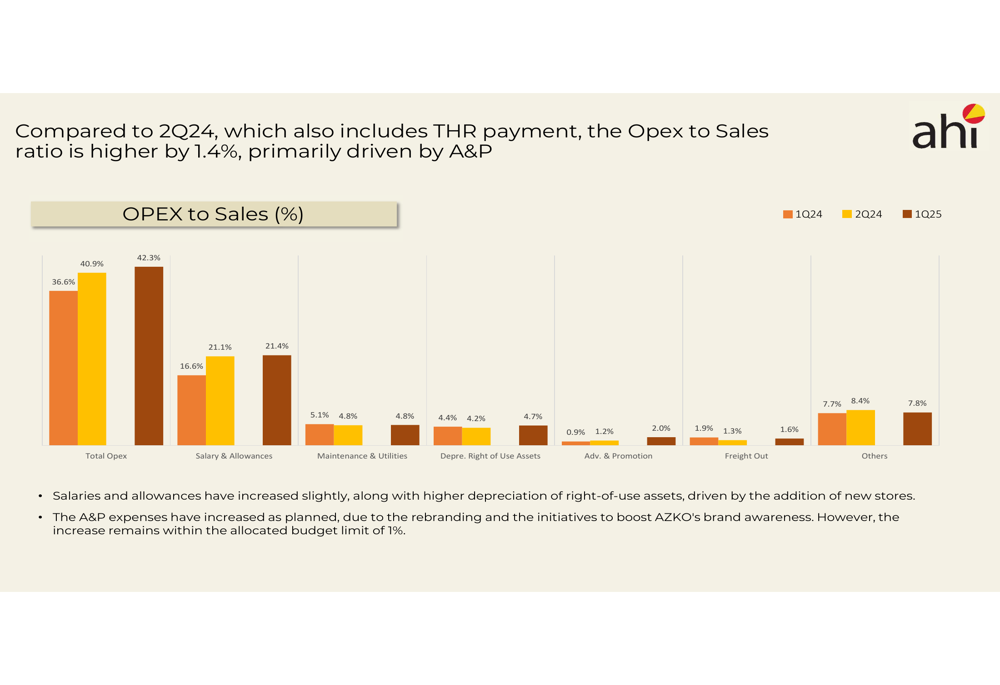

The decline in profitability was largely attributed to increased operating expenses:

The operating expense to sales ratio increased to 42.3% in Q1 2025 from 36.6% in Q1 2024, primarily driven by higher advertising and promotion expenses, which jumped from 1.2% to 4.7% of sales due to the company’s rebranding initiatives. Salary and allowance expenses also increased to 21.4% of sales, compared to 16.6% in the same period last year.

Strategic Initiatives

A central focus of PT Aspirasi Hidup Indonesia’s strategy is the comprehensive rebranding of its Azko stores, aimed at enhancing customer experience and brand awareness:

The rebranding represents the company’s commitment to improving lives with A-Z product collections, comprehensive services, and innovative solutions tailored to Indonesian customers’ needs. The "AZKO Experience Store" introduces a next-generation concept with modern features designed to elevate the shopping experience.

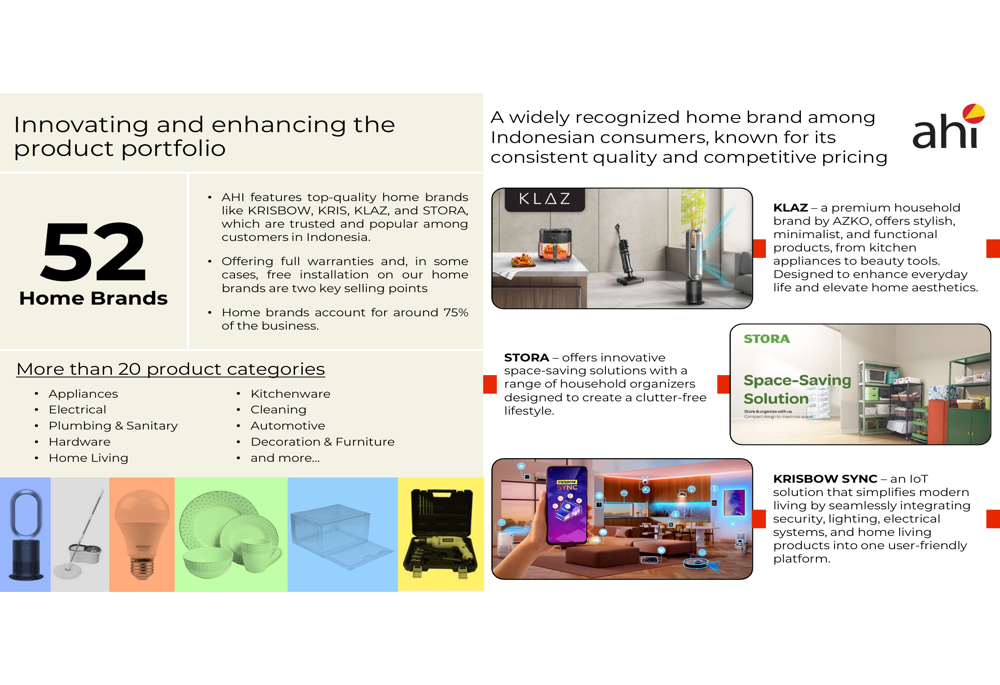

The company is also strengthening its product portfolio, featuring 52 home brands that account for approximately 75% of the business:

Top-quality home brands include KRISBOW, KRIS, KLAZ, and STORA, which are popular among Indonesian consumers. These brands offer full warranties and, in some cases, free installation as key selling points. The product range spans more than 20 categories, including appliances, electrical, plumbing, hardware, home living, kitchenware, and furniture.

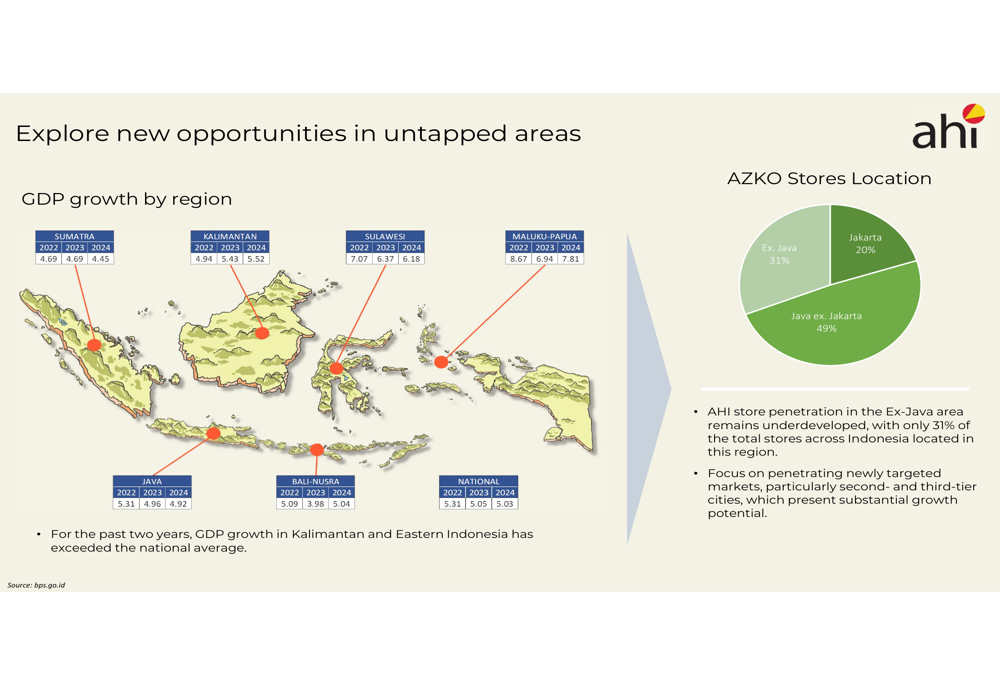

PT Aspirasi Hidup Indonesia is strategically targeting expansion in untapped markets, particularly in regions outside Java:

The company noted that GDP growth in Kalimantan and Eastern Indonesia has exceeded the national average for the past two years, presenting significant growth opportunities. Currently, only 31% of the company’s stores are located outside Java, highlighting substantial room for expansion in these high-potential regions.

Operational Updates

The company continues to enhance its omnichannel approach, integrating physical stores with digital platforms:

Online sales now contribute 11% of total sales, with the company’s integrated e-commerce platform "ruparupa" accounting for approximately 75% of online sales (or about 8% of total sales). The platform has achieved over 2 million downloads and maintains strong ratings on both Apple (NASDAQ:AAPL) (4.6/5) and Android (4.8/5) app stores. The user base is predominantly young, with over 50% of users aged 18-34.

Efficiency metrics show modest improvements despite the challenging quarter:

Employee count increased by 5% year-over-year to 14,471, while sales per employee improved by 2% to 590 million IDR. Employee coverage remained stable at 43 square meters per employee.

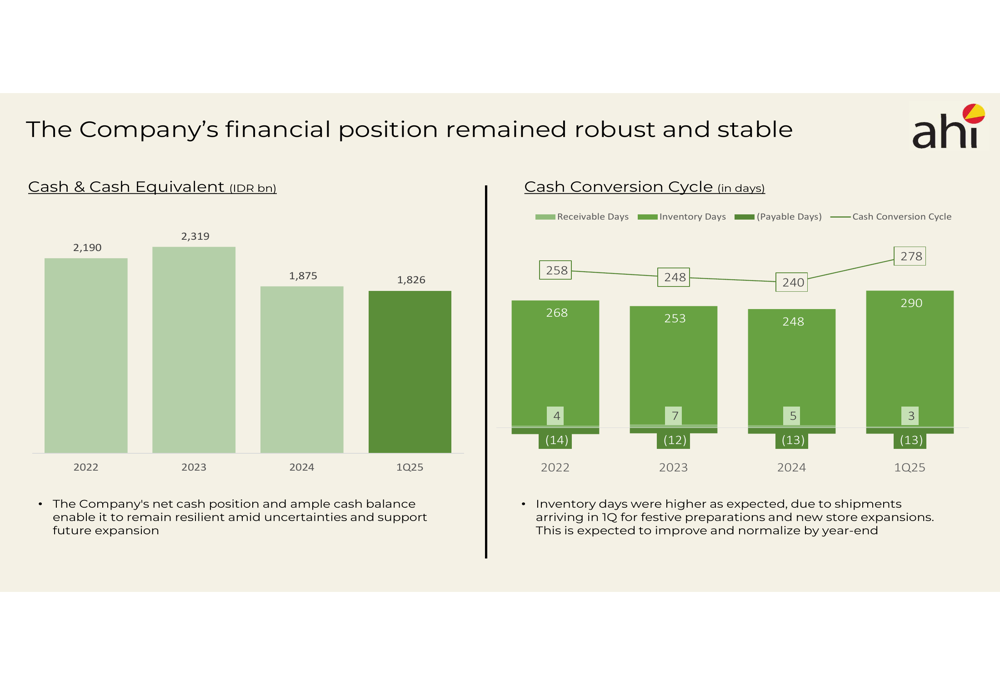

The company’s financial position remains solid, though with some changes in working capital metrics:

Cash and cash equivalents stood at 1.826 trillion IDR at the end of Q1 2025, slightly down from 1.875 trillion IDR at the end of 2024. The cash conversion cycle increased to 290 days from 240 days at year-end 2024, primarily due to higher inventory days (278 vs. 248). The company attributed this increase to shipments arriving in Q1 for festive preparations and new store expansions, expecting normalization by year-end.

Forward Guidance

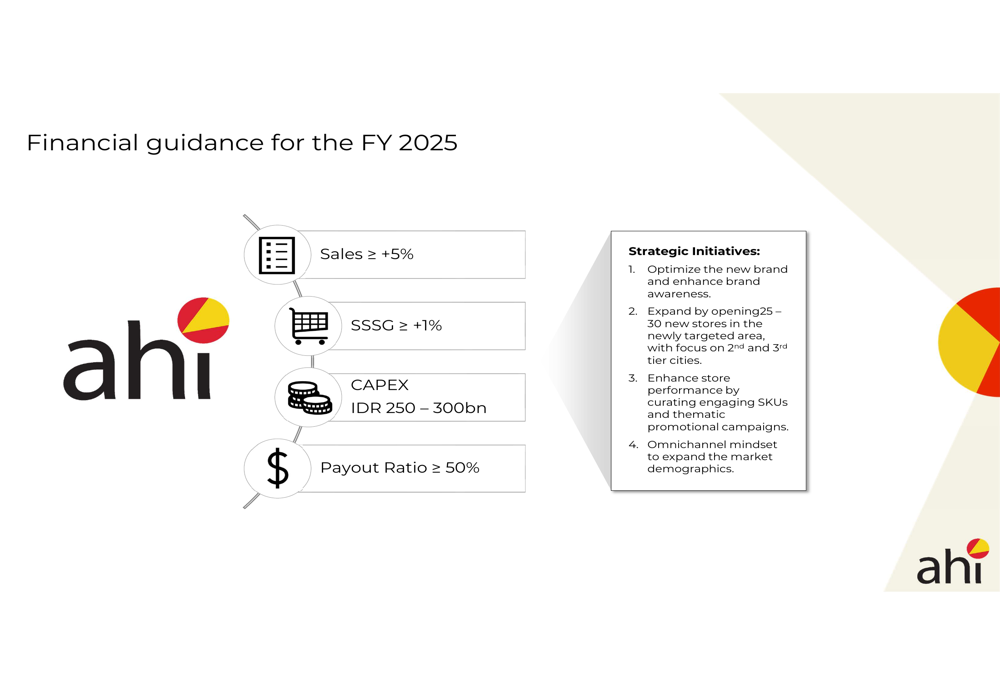

For the full year 2025, PT Aspirasi Hidup Indonesia provided the following guidance:

The company targets sales growth of at least 5%, with same-store sales growth exceeding 1%. Capital expenditure is planned at 250-300 billion IDR, with a dividend payout ratio of at least 50%.

Strategic priorities for 2025 include optimizing the new brand and enhancing brand awareness, expanding with 25-30 new stores in targeted areas (focusing on second and third-tier cities), enhancing store performance through curated SKUs and thematic promotional campaigns, and continuing to develop the omnichannel approach to expand market demographics.

Despite the profit pressure in Q1, management expressed confidence that the investments in rebranding and expansion will position the company for sustainable long-term growth in Indonesia’s evolving retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.