Fed Governor Adriana Kugler to resign

Introduction & Market Context

PTC Inc (NASDAQ:PTC) released its third-quarter fiscal year 2025 results on July 30, 2025, showing solid performance across key metrics. The company, which specializes in product lifecycle management (PLM), computer-aided design (CAD), and service lifecycle management (SLM (NASDAQ:SLM)) solutions, continues to leverage its diverse portfolio and AI capabilities to drive growth despite macroeconomic uncertainties.

PTC’s stock closed at $204.19 on the day of the announcement, down 0.72% from the previous session, but still trading significantly above its 52-week low of $133.38. The company’s results come amid ongoing digital transformation initiatives across manufacturing and engineering sectors, with particular strength in automotive, aerospace, and medical technology verticals.

Quarterly Performance Highlights

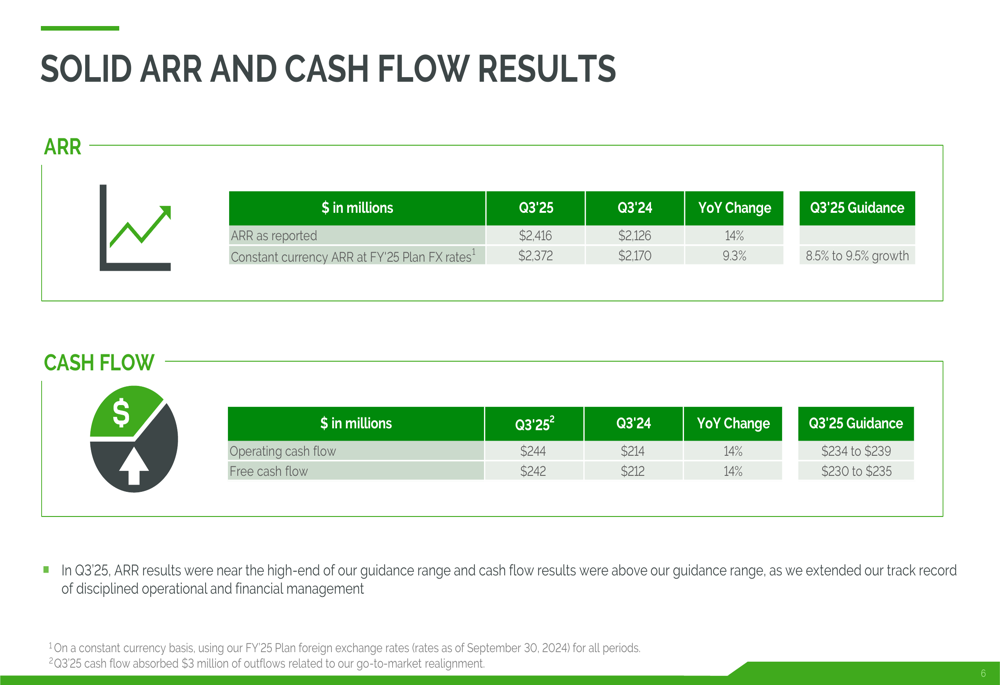

PTC reported Annual Run Rate (ARR) of $2,416 million as reported, or $2,372 million at constant currency, representing a 9.3% year-over-year growth. This performance landed near the high end of the company’s guidance range of 8.5% to 9.5%. Cash flow results exceeded guidance, with operating cash flow reaching $244 million and free cash flow hitting $242 million, both representing 14% year-over-year growth.

As shown in the following chart detailing PTC’s Q3’25 ARR and cash flow performance:

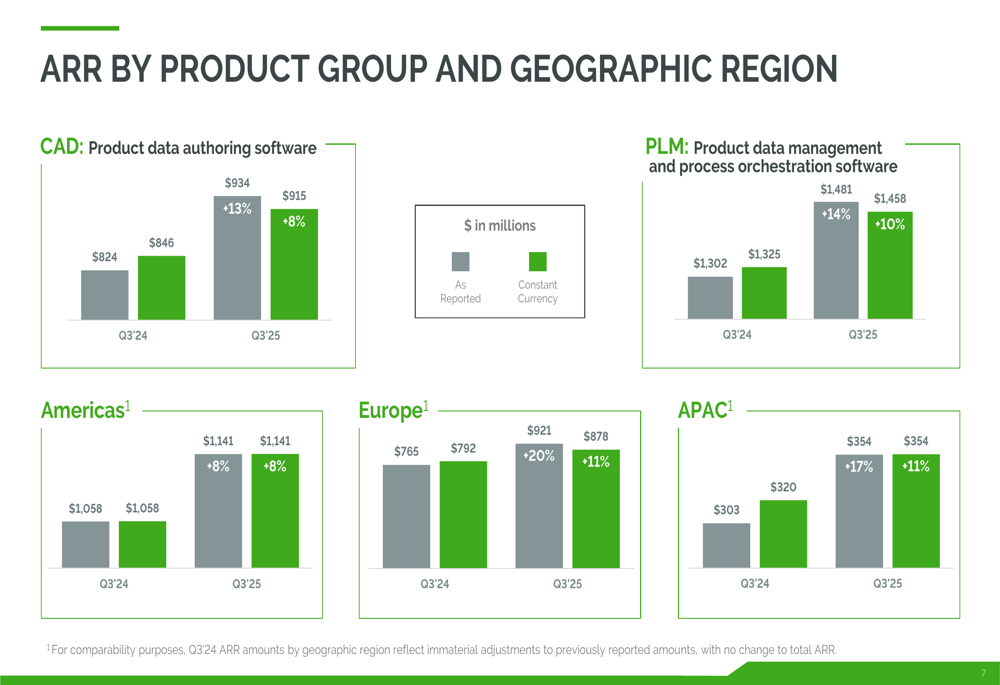

The company’s ARR growth was balanced across geographic regions, with the Americas growing 8% year-over-year to $1,141 million, Europe growing 11% to $878 million, and Asia-Pacific growing 11% to $354 million. From a product perspective, PLM solutions led growth at 10% year-over-year to reach $1,458 million in ARR, while CAD solutions grew 8% to $915 million.

The following breakdown illustrates PTC’s ARR distribution by product group and geographic region:

Detailed Financial Analysis

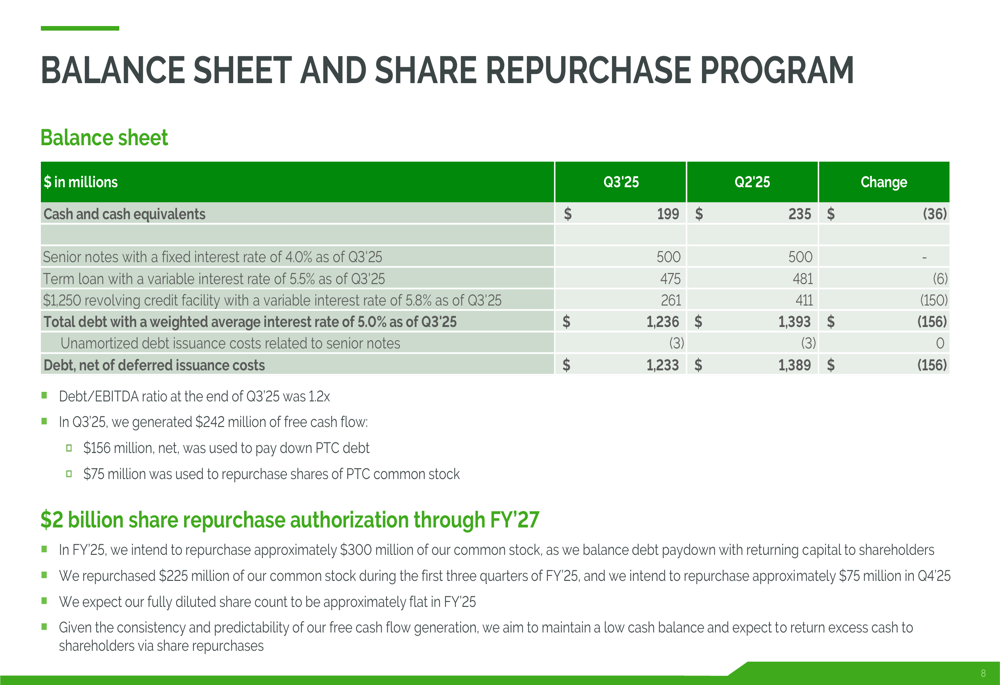

PTC’s balance sheet remains solid with $199 million in cash and cash equivalents. The company reported total debt of $1,236 million with a weighted average interest rate of 5.0%, including $500 million in senior notes at a fixed 4.0% rate. During Q3’25, PTC generated $242 million in free cash flow, allocating $156 million toward debt reduction and $75 million for share repurchases.

The company’s capital allocation strategy is detailed in the following slide:

PTC continues to execute on its $2 billion share repurchase authorization, which extends through FY’27. The company intends to repurchase approximately $300 million of common stock in FY’25, demonstrating confidence in its long-term business outlook despite near-term market uncertainties.

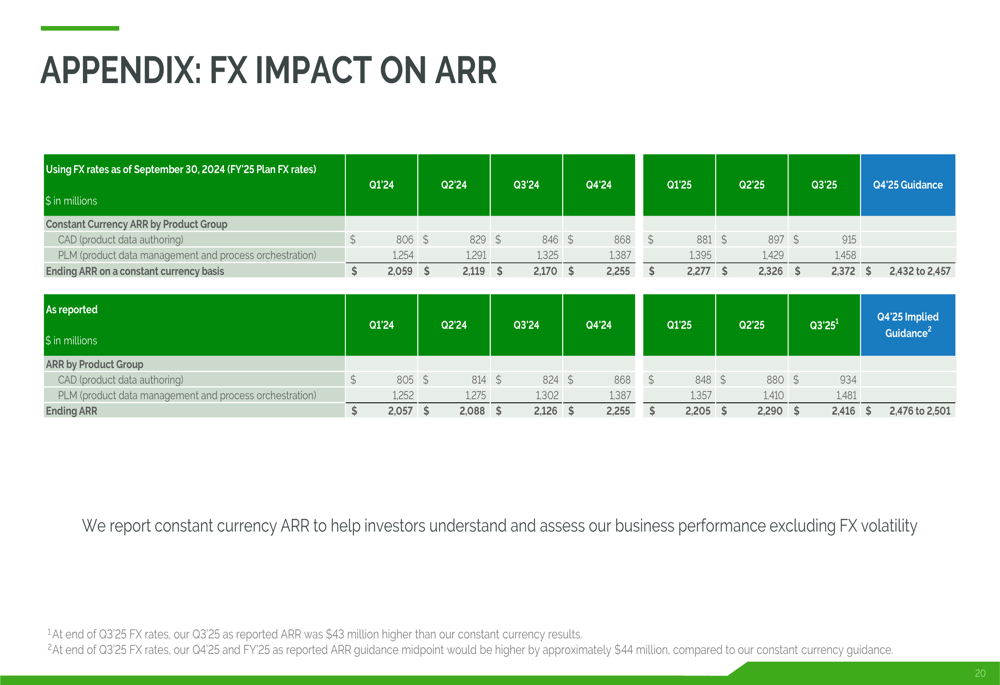

Foreign exchange movements had a notable impact on reported results, with Q3’25 as-reported ARR coming in $43 million higher than constant currency figures. This currency effect has been consistent across recent quarters, as illustrated in the following analysis:

Strategic Initiatives & Customer Wins

PTC highlighted several strategic customer wins across key verticals during the quarter. In the automotive sector, a major European supplier expanded its relationship with PTC by adding Codebeamer ALM to its existing Windchill PLM implementation, aiming to achieve comprehensive end-to-end development traceability and efficient software reuse.

The following case study demonstrates PTC’s cross-selling success:

In the medical technology space, PTC secured a significant expansion of its ServiceMax SLM solution with a global leader in medical solutions. The customer is leveraging ServiceMax to improve revenue generation and provide field clinicians with modern tools for faster response times, while ensuring regulatory compliance through end-to-end traceability with Windchill.

PTC’s ServiceMax expansion in the medical technology sector is illustrated here:

The company also highlighted its success with Windchill+ SaaS PLM, winning a competitive displacement at a global leader in diagnostics and life sciences. This customer, already using ServiceMax, selected Windchill+ over competitive offerings to improve time to market and quality through a modern SaaS-based PLM system.

The following slide details this competitive win:

Forward-Looking Statements

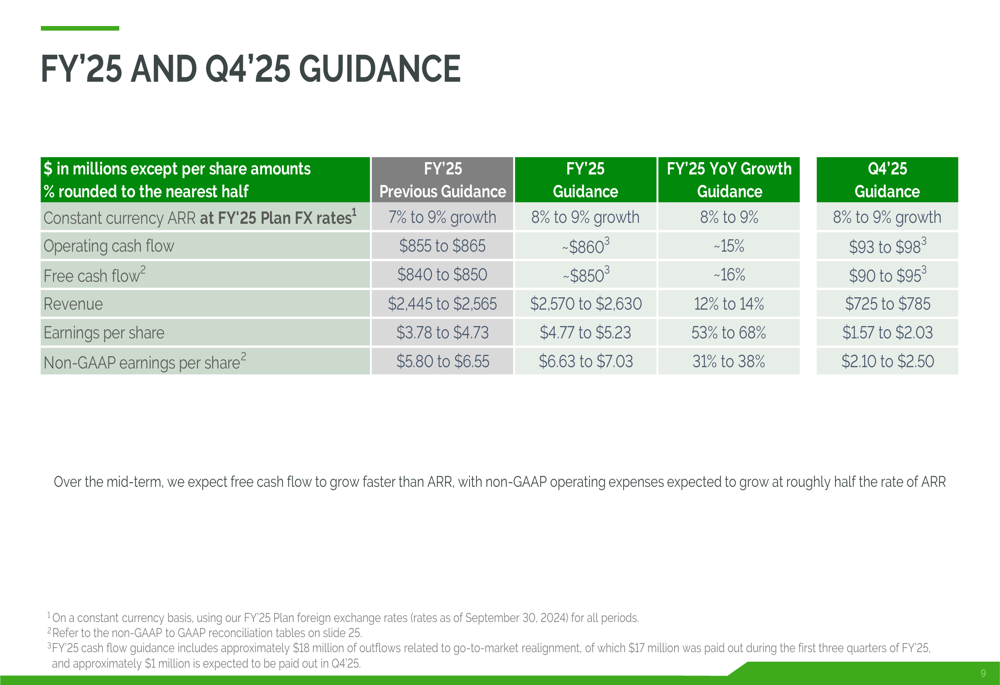

Looking ahead, PTC provided guidance for both Q4’25 and the full fiscal year. For FY’25, the company expects constant currency ARR growth of 8% to 9%, operating cash flow of approximately $860 million, and free cash flow of approximately $850 million. Revenue is projected to be between $2,570 million and $2,630 million, with non-GAAP earnings per share between $6.63 and $7.03.

The company’s detailed guidance is presented in the following slide:

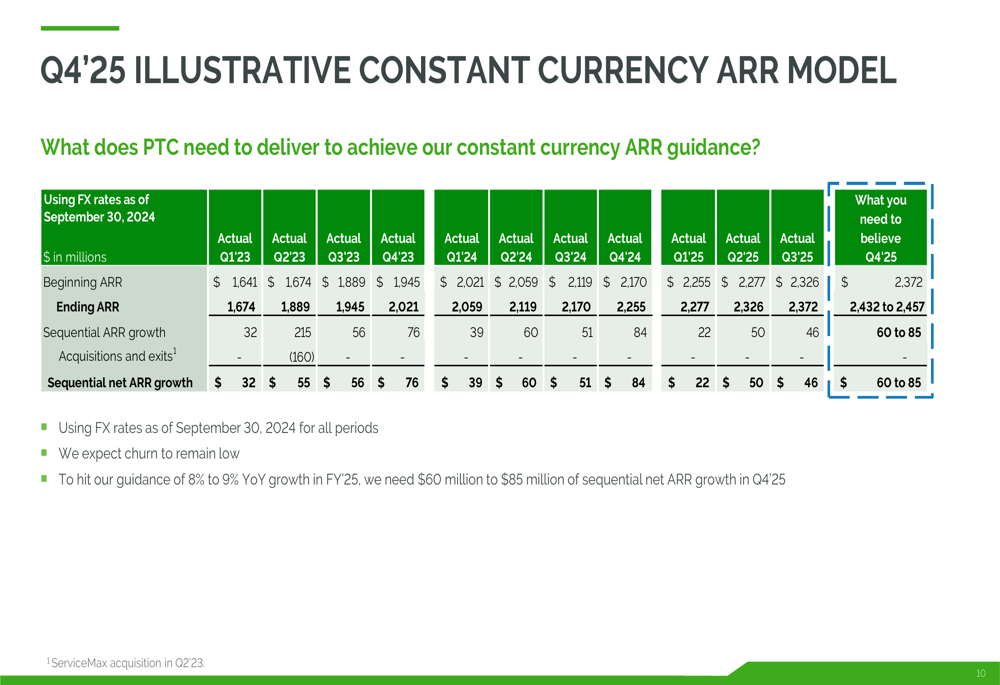

For Q4’25 specifically, PTC anticipates operating cash flow of $93 million to $98 million and free cash flow of $90 million to $95 million. To achieve its full-year ARR growth target of 8% to 9%, the company needs to generate sequential net ARR growth of $60 million to $85 million in Q4’25.

The company’s Q4’25 ARR growth model is illustrated here:

Over the mid-term, PTC expects free cash flow to grow faster than ARR, with non-GAAP operating expenses projected to grow at roughly half the rate of ARR. This disciplined approach to expense management, combined with the company’s ongoing transition to SaaS offerings and AI integration across its portfolio, positions PTC to continue delivering value to shareholders despite near-term macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.