TSX up after index logs fresh record high close

Introduction & Market Context

PYC Therapeutics (ASX:PYC) presented its Q2 2025 investor webinar on May 30, outlining progress across its genetic medicine pipeline while facing continued market skepticism. The company’s stock closed at $1.20 prior to the presentation, representing a significant 42% year-to-date decline despite recent fundraising success.

The presentation highlighted PYC’s focus on developing disease-modifying therapeutics for rare genetic disorders, emphasizing a differentiated approach that targets the root causes of diseases with high unmet needs. This strategy positions PYC in the specialized RNA therapeutics space, where it faces both significant opportunities and challenges in bringing novel treatments to market.

Pipeline Progress and Clinical Milestones

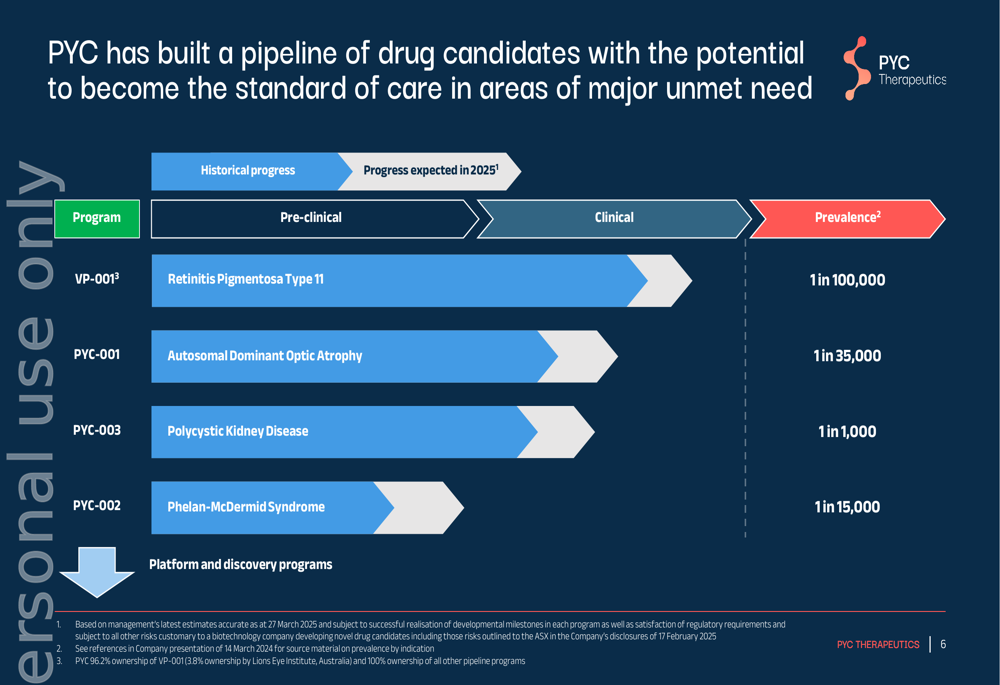

PYC’s presentation emphasized its pipeline of drug candidates targeting rare genetic disorders, with four main programs in various stages of development. The company’s approach focuses on monogenic disorders, which management believes offers a higher probability of clinical success.

As shown in the following comprehensive pipeline overview:

The company’s lead program, VP-001 for Retinitis Pigmentosa Type 11 (prevalence 1 in 100,000), is advancing toward later-stage clinical trials. Other key programs include PYC-001 for Autosomal Dominant Optic Atrophy (1 in 35,000), PYC-003 for Polycystic Kidney Disease (1 in 1,000), and PYC-002 for Phelan-McDermid Syndrome (1 in 15,000).

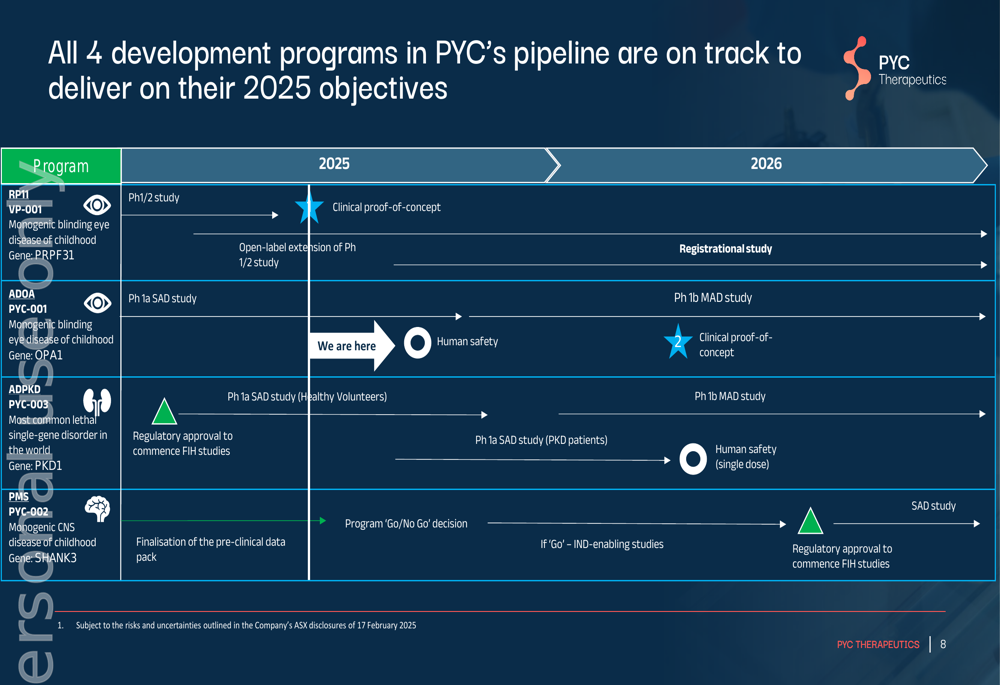

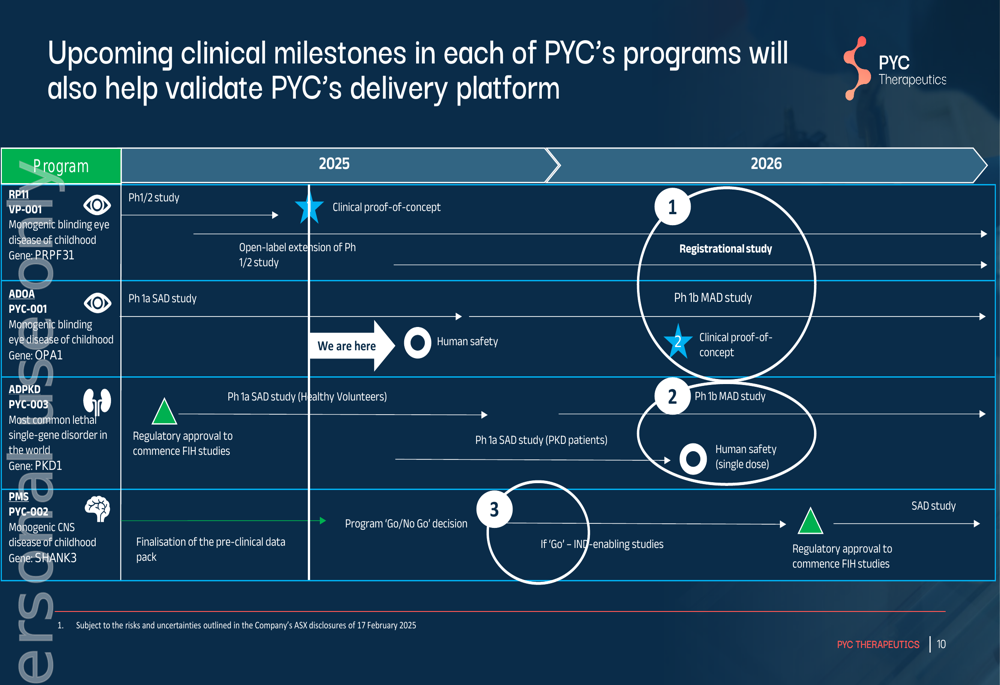

PYC presented a detailed timeline of expected clinical milestones through 2025-2026, highlighting several potential value-creating events:

Key upcoming milestones include the planned commencement of a registrational study for VP-001 in 2026, human safety data for PYC-001 in 2025, and regulatory approval to commence first-in-human studies for PYC-003 in 2025. For PYC-002, the company expects to make a "go/no-go" decision in 2025 based on pre-clinical data.

Strategic Approach to Partnerships and Value Creation

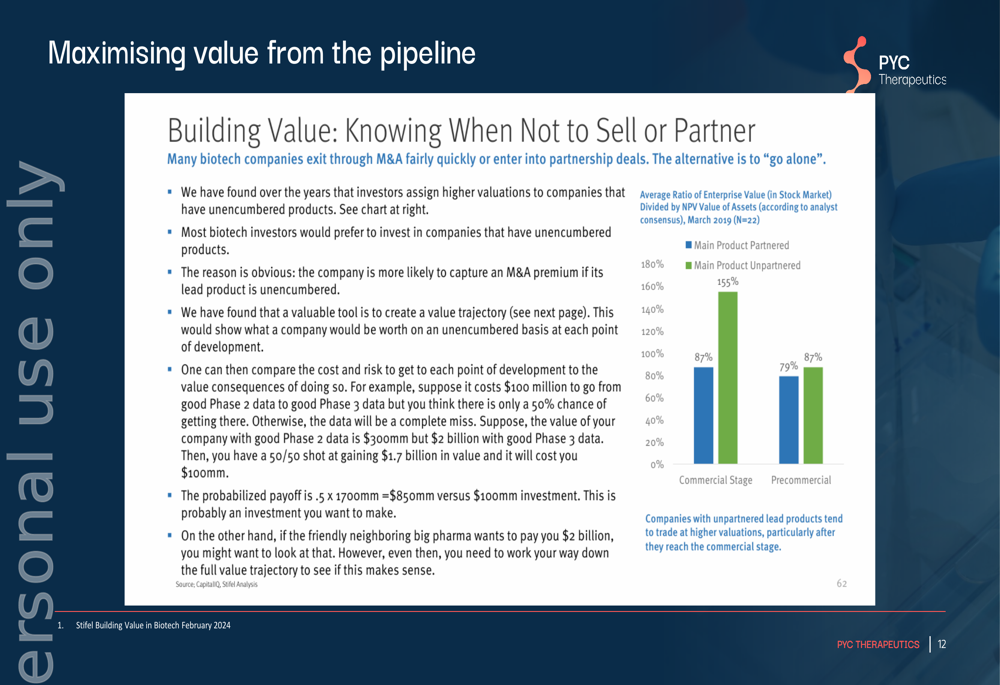

A notable aspect of PYC’s strategy is its approach to partnerships and potential commercialization. The company presented data suggesting that maintaining unencumbered products can maximize enterprise value, particularly at the commercial stage.

According to the company’s analysis, unpartnered products at the commercial stage command a significantly higher enterprise value (155% of NPV) compared to partnered products (87%). This data supports PYC’s strategy of maintaining full ownership of its assets to potentially capture higher M&A premiums in the future.

This approach aligns with management’s statements from the Q1 earnings call, where executives emphasized the company’s focus on monogenic disorders as a strategic differentiator. "We make drugs for patients who have mutations in a single gene or what we call monogenic disorders," a company executive noted during that call.

Financial Position and Market Performance

While the presentation focused primarily on clinical development and strategy, PYC’s financial position provides important context. According to the company’s Q1 2025 earnings report, PYC raised $145 million through a rights issue, establishing a cash runway estimated between $202-250 million. This funding is expected to support approximately 24 months of planned operations, covering the key milestones outlined in the presentation.

Despite this financial cushion, market sentiment remains cautious. PYC’s stock has declined 42% year-to-date, with a beta of 1.66 indicating higher volatility than the broader market. This disconnect between the company’s optimistic clinical outlook and market performance suggests investors may be taking a wait-and-see approach regarding the company’s ability to execute on its ambitious timeline.

Forward-Looking Statements

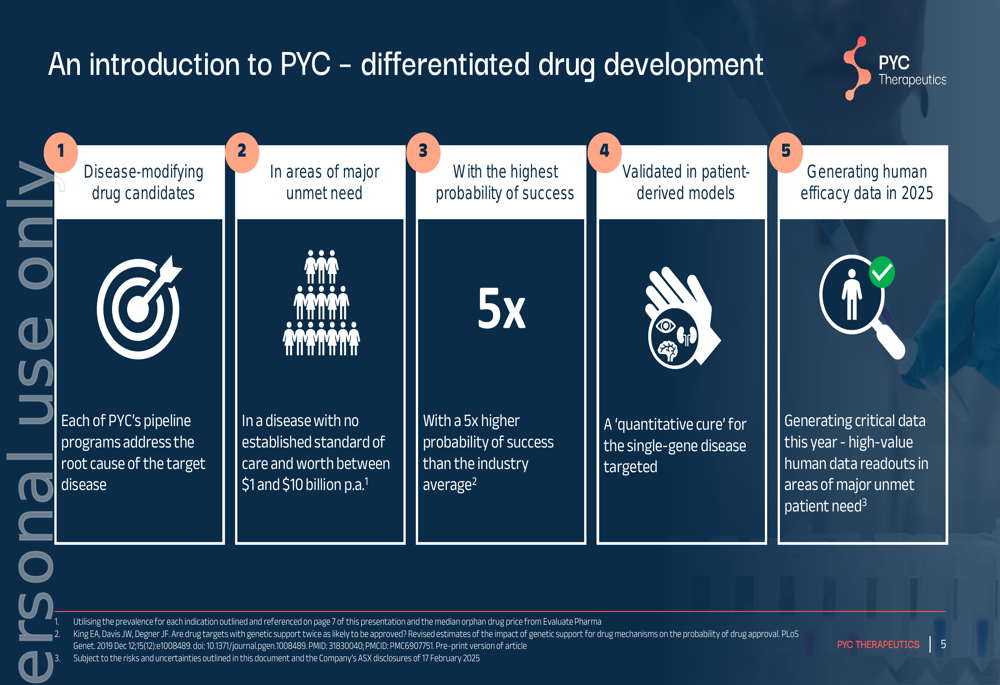

PYC’s presentation emphasized several differentiating factors that management believes will drive future success. The company highlighted that its drug candidates address root causes of diseases with major unmet needs, claiming a "5x higher probability of success than the industry average" based on their approach.

As illustrated in this slide detailing PYC’s differentiated drug development approach:

The company’s focus on generating "quantitative cures" for single-gene diseases and producing human efficacy data in 2025 represents ambitious goals that could significantly impact valuation if achieved. However, these forward-looking statements should be viewed in the context of the company’s current market performance and the inherent risks of drug development.

The clinical milestones outlined for 2025-2026 will be critical validation points for PYC’s platform technology:

Success across multiple programs would not only advance individual drug candidates but also validate PYC’s underlying delivery platform, potentially creating additional value beyond the current pipeline.

As PYC moves forward with its ambitious clinical development plans, investors will be closely watching for execution on these milestones, particularly the human safety data expected in 2025 and the potential commencement of a registrational study for VP-001 in 2026, which could represent significant inflection points for the company’s valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.