Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

Quest Diagnostics Incorporated (NYSE:DGX) released its first quarter 2025 financial results on April 22, showing strong revenue growth driven by acquisitions and advanced diagnostics. The company’s stock rose 1.94% in premarket trading to $165.00, reflecting positive investor sentiment following the earnings announcement.

The diagnostic testing leader reported total revenue of $2.65 billion, up 12.1% year-over-year, while adjusted diluted earnings per share reached $2.21, an 18.3% increase from the same period last year. These results continue the momentum seen in Q4 2024, when the company reported 14.5% revenue growth.

Quarterly Performance Highlights

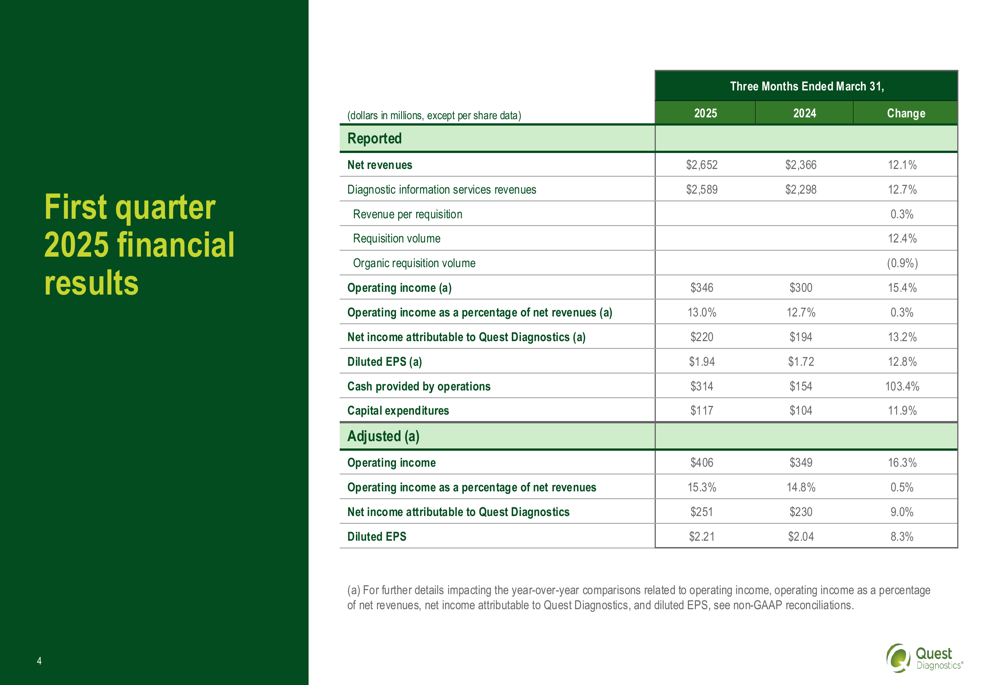

Quest Diagnostics delivered impressive financial results for the first quarter of 2025, with significant year-over-year improvements across key metrics. Total (EPA:TTEF) revenue grew 12.1% to $2.65 billion, while diagnostic information services revenues increased 12.7% to $2.59 billion compared to Q1 2024.

As shown in the following detailed financial comparison, the company achieved substantial growth in operating income and earnings per share:

Particularly noteworthy was the 103.4% increase in cash provided by operations, which reached $314 million compared to $154 million in Q1 2024. This dramatic improvement in cash flow demonstrates the company’s enhanced operational efficiency and successful integration of recent acquisitions.

The quarter also featured several strategic business developments, including:

- Being named the first independent national lab provider in the Optum Health Preferred Lab Network

- Forming an agreement with Fresenius Medical (TASE:BLWV) Care (NYSE:FMS) to provide lab testing for patients requiring kidney dialysis

- Announcing a collaboration with Google (NASDAQ:GOOGL) Cloud to streamline data management

- Beginning to receive commercial orders for Haystack MRD™ testing for cancer recurrence monitoring

Detailed Financial Analysis

While total requisition volume increased by 12.4% year-over-year, organic requisition volume (excluding acquisitions) decreased by 0.9%, indicating that growth was primarily driven by acquisitions rather than organic expansion. Revenue per requisition showed a modest increase of 0.3%.

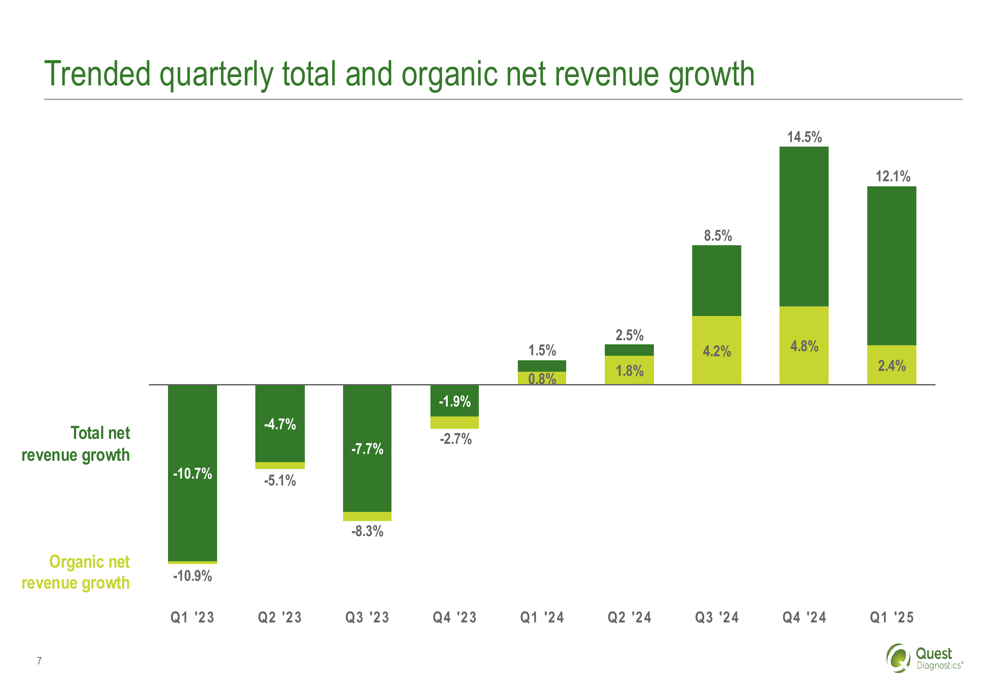

The following chart illustrates the company’s quarterly revenue growth trends, showing the transition from negative to positive territory over the past two years:

This trend analysis reveals that while total net revenue growth has been strong in recent quarters, organic net revenue growth has been more modest, reaching 2.4% in Q1 2025. This represents a deceleration from the 4.8% organic growth achieved in Q4 2024.

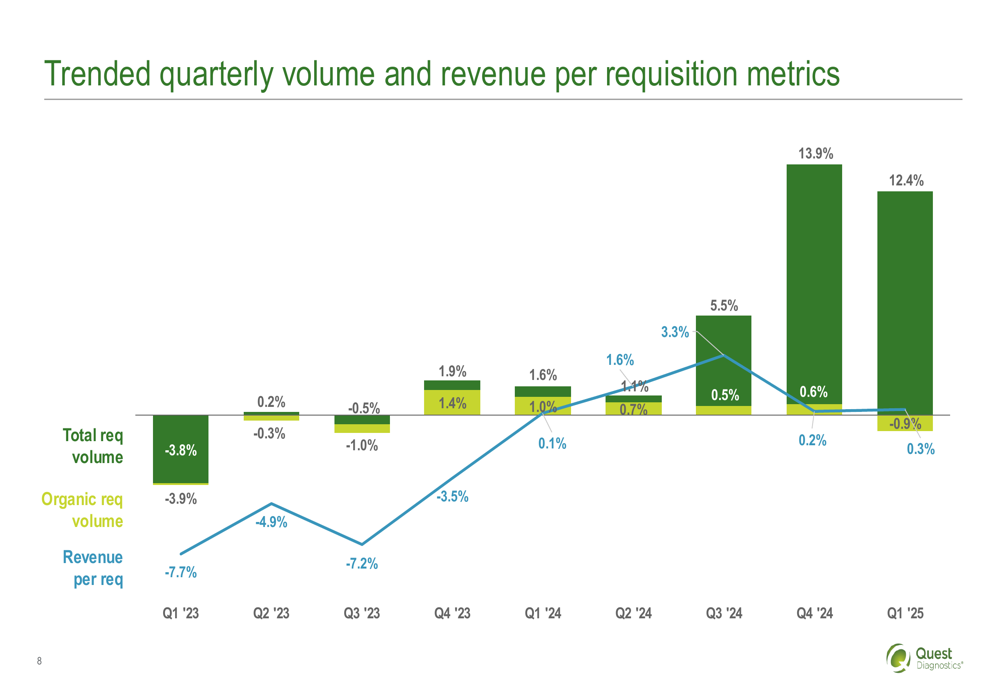

The volume and revenue per requisition metrics provide additional context for understanding the company’s performance dynamics:

The chart shows that total requisition volume growth has been robust, particularly in the last three quarters, while organic requisition volume has fluctuated and turned slightly negative in Q1 2025. Revenue per requisition has stabilized after earlier fluctuations.

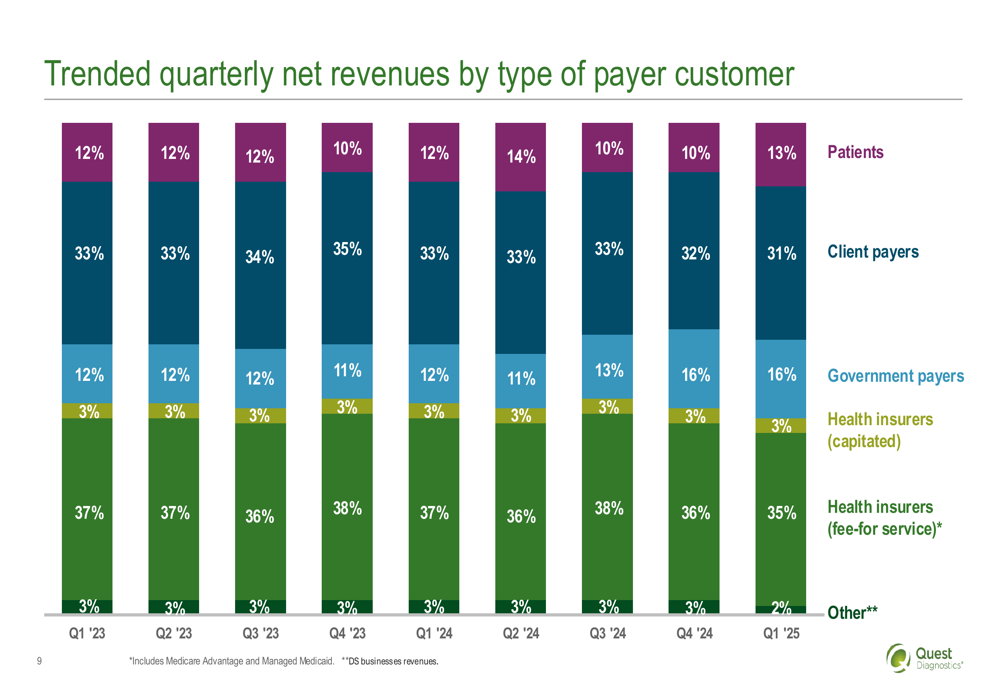

Quest Diagnostics’ revenue mix by payer type has remained relatively stable, as illustrated in the following chart:

Strategic Initiatives

Quest Diagnostics is investing in several strategic initiatives to drive future growth. The company is modernizing its IT infrastructure to improve operational efficiency and enhance the customer experience. These investments include migrating current systems to cloud-based platforms, which is expected to reduce complexity and lower IT costs over time.

Additionally, the company is preparing for upcoming FDA regulations on laboratory-developed tests, with initial requirements taking effect on May 6, 2025. This preparation includes establishing a complaint handling unit and enabling medical device reporting to the FDA.

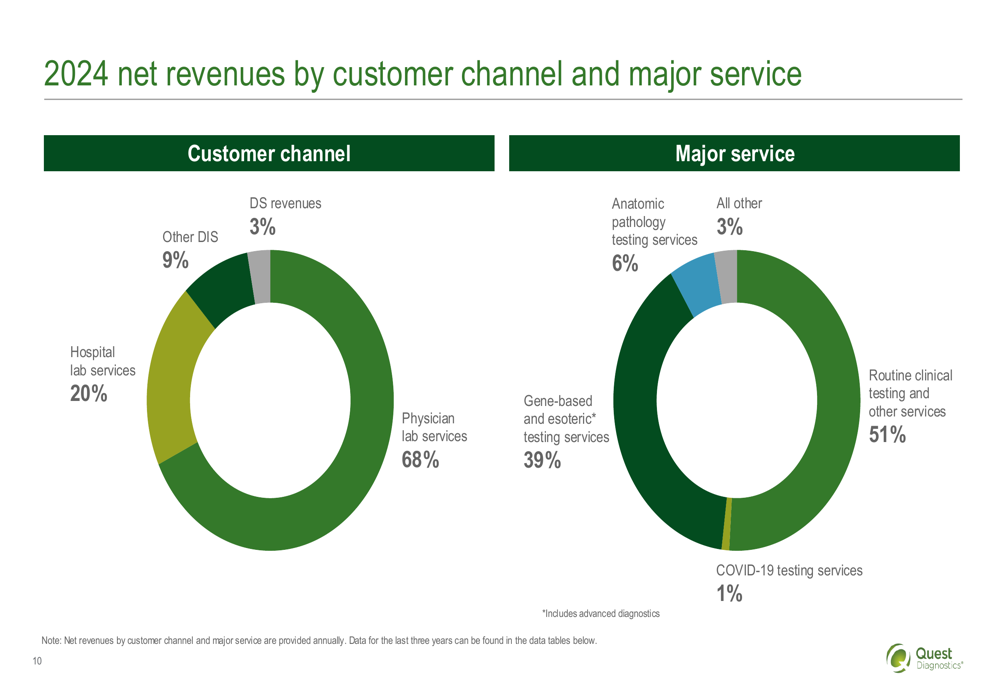

The company’s 2024 revenue breakdown by customer channel and major service provides insight into its diversified business model:

Physician lab services represent the largest portion of the company’s business at 68% of revenues, while gene-based and esoteric testing services account for 39% of revenues by service type. The latter category includes advanced diagnostics, which has been a key growth driver for the company.

Forward-Looking Statements

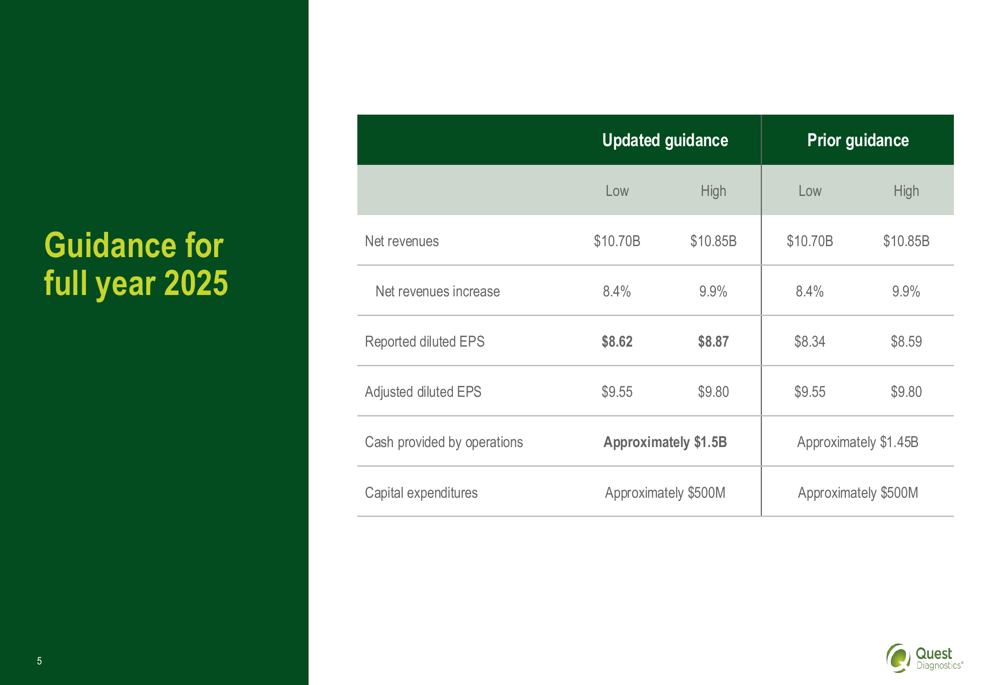

Quest Diagnostics reaffirmed its full-year 2025 guidance, projecting net revenues between $10.70 billion and $10.85 billion, representing an 8.4% to 9.9% increase over 2024. The company also maintained its adjusted diluted EPS guidance of $9.55 to $9.80, while slightly increasing its cash provided by operations forecast to approximately $1.5 billion.

The following table details the company’s updated guidance compared to prior projections:

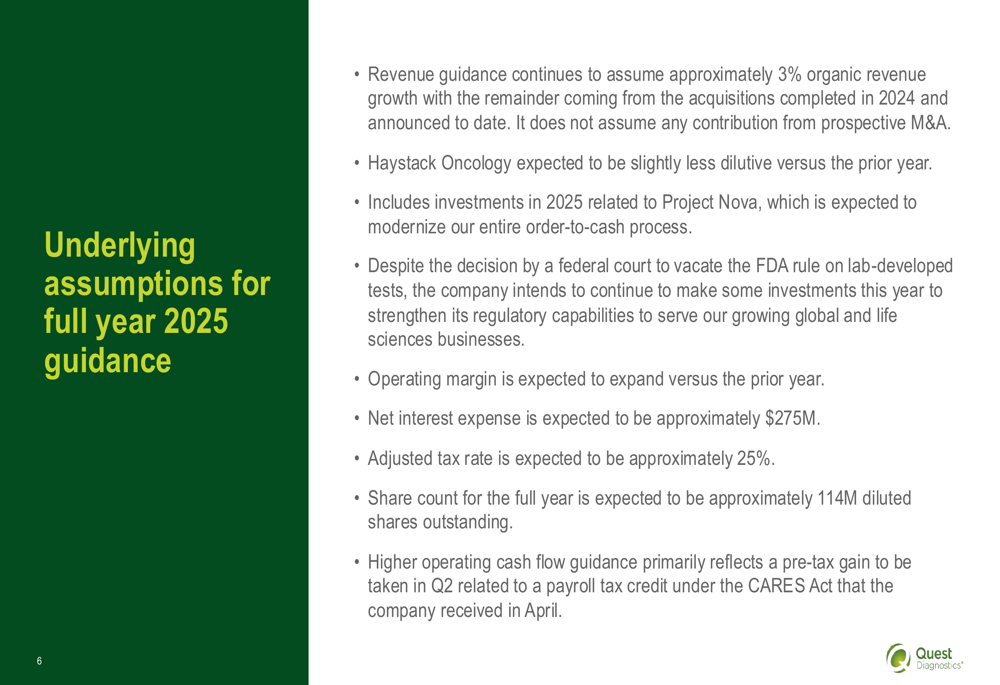

The guidance is based on several key assumptions, including approximately 3% organic revenue growth and continued investments in Project Nova to modernize the order-to-cash process. The company also expects Haystack Oncology to be slightly less dilutive compared to the prior year and anticipates operating margin expansion in 2025.

These underlying assumptions are outlined in detail below:

The higher operating cash flow guidance primarily reflects a pre-tax gain expected in Q2 related to a payroll tax credit under the CARES Act, demonstrating the company’s ability to capitalize on available financial opportunities while focusing on core business growth.

In summary, Quest Diagnostics’ Q1 2025 results show continued momentum in revenue and earnings growth, driven primarily by acquisitions and advanced diagnostics. While organic volume showed a slight decline, the company’s reaffirmed guidance suggests confidence in its ability to maintain growth throughout 2025 as it continues to invest in strategic initiatives and operational improvements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.