Gold prices slip as stronger dollar, Fed uncertainty weigh

Introduction & Market Context

Quorum Information Technologies Inc (TSXV:QIS) presented its Q2 2025 results on August 27, 2025, highlighting modest revenue growth alongside improved profitability metrics and significant debt reduction. The North American SaaS provider for automotive dealerships and OEMs continues to execute on its strategic focus of profitable growth and financial discipline.

Trading at $0.70 per share as of August 27, 2025, Quorum maintains a diluted market capitalization of $51.3 million and an enterprise value of $52.3 million. The company serves over 1,400 dealerships across North America, with a substantial 40% market penetration in Canada compared to just 0.6% in the United States, suggesting significant growth potential in the US market.

Quarterly Performance Highlights

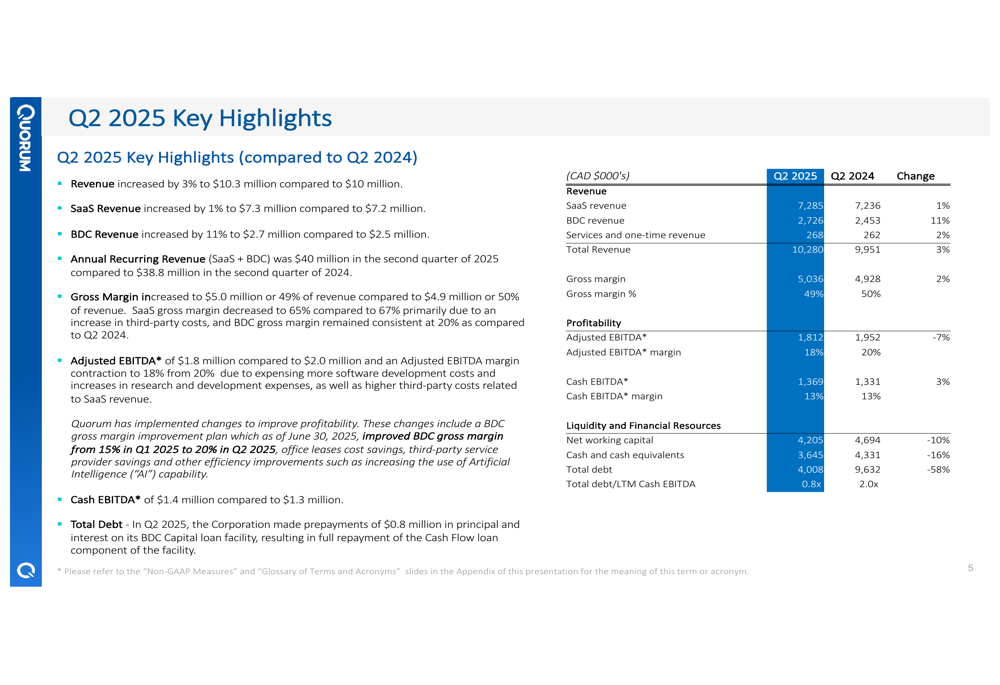

Quorum reported total revenue of $10.3 million for Q2 2025, representing a 3% increase compared to the same period last year. This modest growth shows a slight acceleration from the 1% revenue increase reported in Q1 2025.

The company’s revenue streams showed varied performance, with SaaS revenue growing by 1% to $7.3 million, while BDC (Business Development Centre) revenue demonstrated stronger growth of 11% to reach $2.7 million. Annual Recurring Revenue (ARR) reached $40 million, up from $38.8 million in the comparable period.

As shown in the following comprehensive financial comparison:

Profitability metrics showed notable improvement, with Adjusted EBITDA reaching $1.8 million (18% margin) and Cash EBITDA of $1.4 million (13% margin). The gross margin stood at 49%, a slight improvement from the 48% reported in Q1 2025. This improvement in profitability metrics suggests that the company’s cost management initiatives, including the previously announced $1.3 million in annual savings expected to be realized in Q3 2025, may be starting to yield results.

Debt Reduction Progress

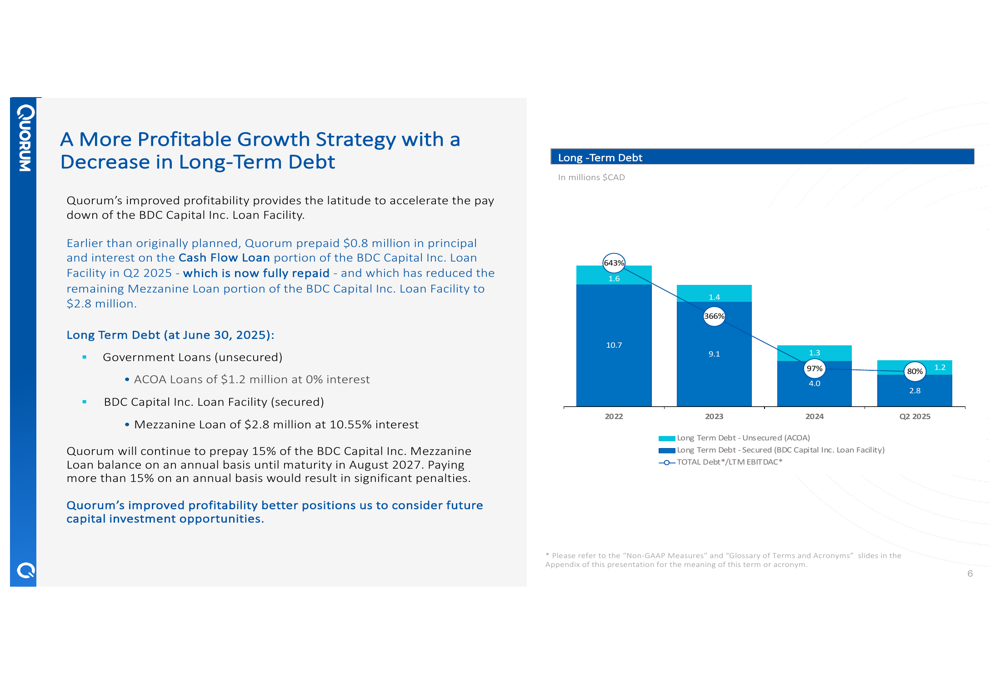

A central element of Quorum’s financial strategy has been its aggressive debt reduction plan, which continued to show significant progress in Q2 2025. The company prepaid $0.8 million during the quarter, fully repaying its Cash Flow Loan.

Total debt decreased substantially to $4.0 million from $9.6 million in the comparable period last year. The remaining debt consists of a $2.8 million Mezzanine Loan and $1.2 million in Government Loans. Quorum has committed to continuing prepayments of 15% of the Mezzanine Loan, with plans to fully repay its BDC Capital loan by the end of 2025.

The following chart illustrates Quorum’s debt reduction trajectory:

This significant debt reduction has improved the company’s financial flexibility, potentially enabling future strategic investments while reducing interest expenses.

Strategic Initiatives and Market Position

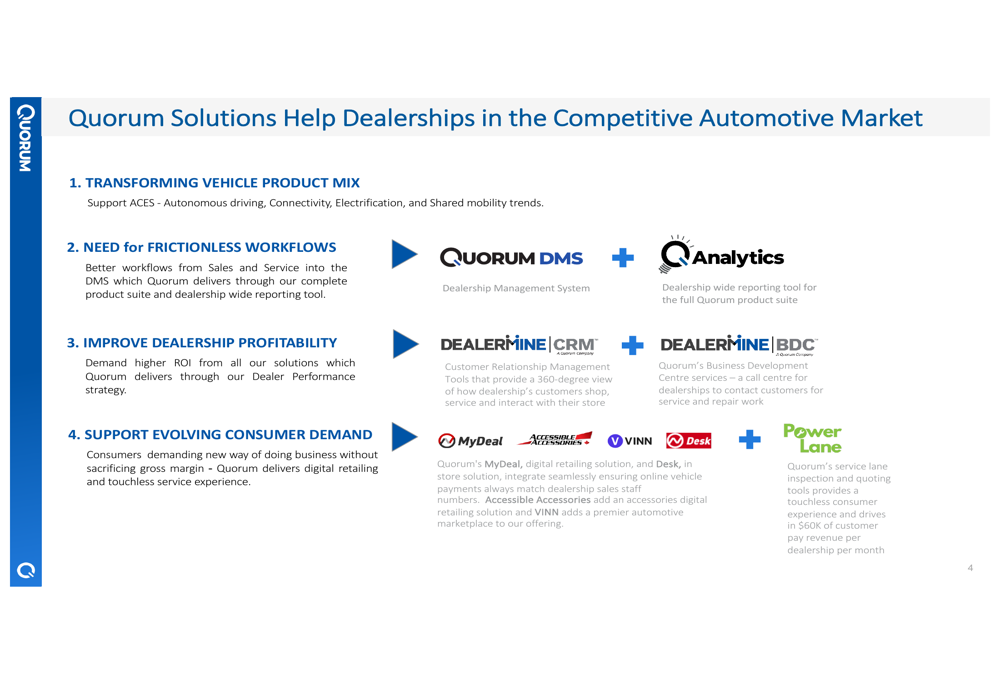

Quorum positions itself as a comprehensive solutions provider for automotive dealerships, offering a suite of products designed to address key industry challenges. The company’s solutions aim to transform vehicle product mix, create frictionless workflows, improve dealership profitability, and support evolving consumer demand.

The following slide illustrates Quorum’s product portfolio:

With its established market position in Canada and minimal penetration in the much larger US market, Quorum has identified cross-selling opportunities and US market expansion as key growth drivers. The company’s strategic focus centers on profitable growth, effective cost management, debt reduction, and targeted investments in future growth opportunities.

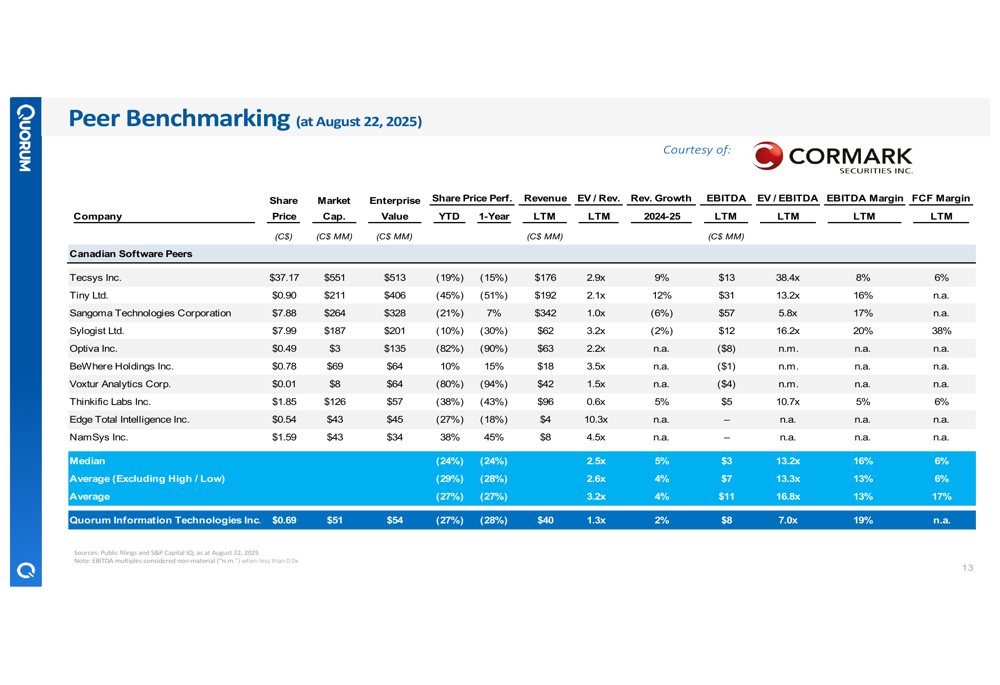

In the competitive landscape, Quorum benchmarks itself against other Canadian software peers:

Forward-Looking Statements

Looking ahead, Quorum’s management has outlined several strategic priorities. The company plans to continue its debt reduction strategy while exploring various capital allocation options, including organic sales growth initiatives, potential acquisitions, share repurchases, and dividend considerations.

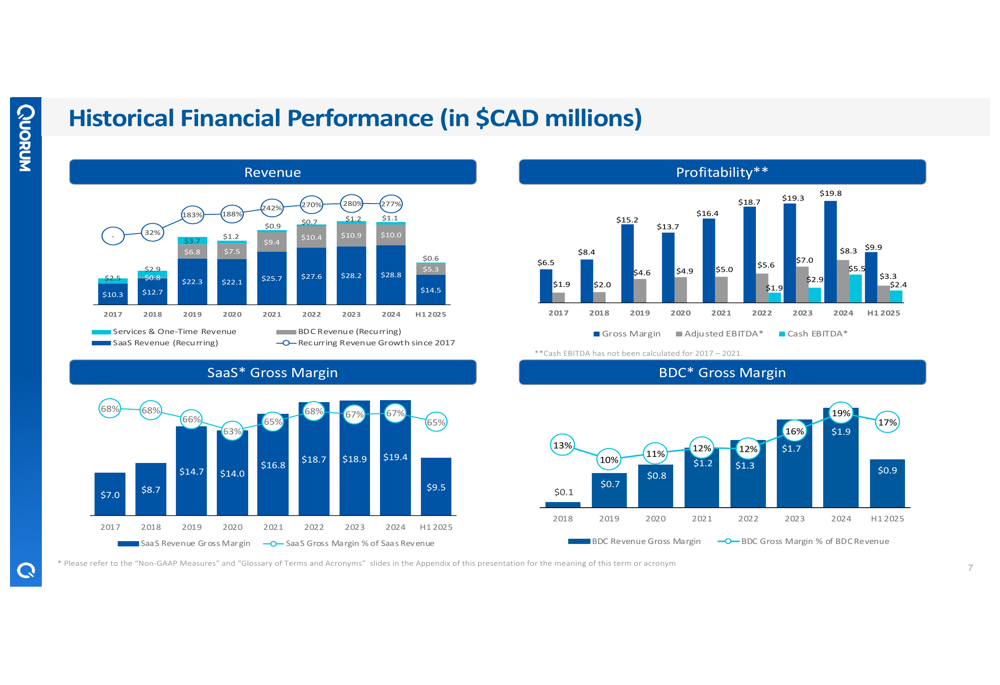

The company’s historical financial performance shows a pattern of steady growth with improving profitability metrics:

While Quorum faces potential challenges from economic headwinds and competitive pressures in the automotive software market, its improved financial position provides greater flexibility to navigate market uncertainties. The significant reduction in debt levels and focus on profitability enhancement position the company to potentially capitalize on growth opportunities, particularly in the underpenetrated US market.

CEO Maury Marks has previously emphasized the demand for Quorum’s service CRM and BDC services, noting that the company’s improved profitability and reduced debt provide latitude for strategic future capital allocation decisions. The Q2 2025 results appear to reinforce this strategic direction, with improved profitability metrics and continued progress on debt reduction.

As Quorum continues to execute its strategic plan, investors will likely focus on the company’s ability to accelerate revenue growth while maintaining the improved profitability demonstrated in Q2 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.