Trump says Nvidia not allowed to sell advanced AI chips to China- 60 Minutes

Introduction & Market Context

Rambus Inc. (NASDAQ:RMBS) released its third-quarter 2025 financial results on October 27, showcasing record product revenue and strong cash generation despite missing earnings expectations. The semiconductor company, which specializes in high-performance memory subsystems and interfaces, continues to benefit from growing demand in data center and AI markets.

The company’s shares rose 7.95% in aftermarket trading to $108.96, reflecting investor confidence in Rambus’s revenue growth trajectory and strategic positioning.

Quarterly Performance Highlights

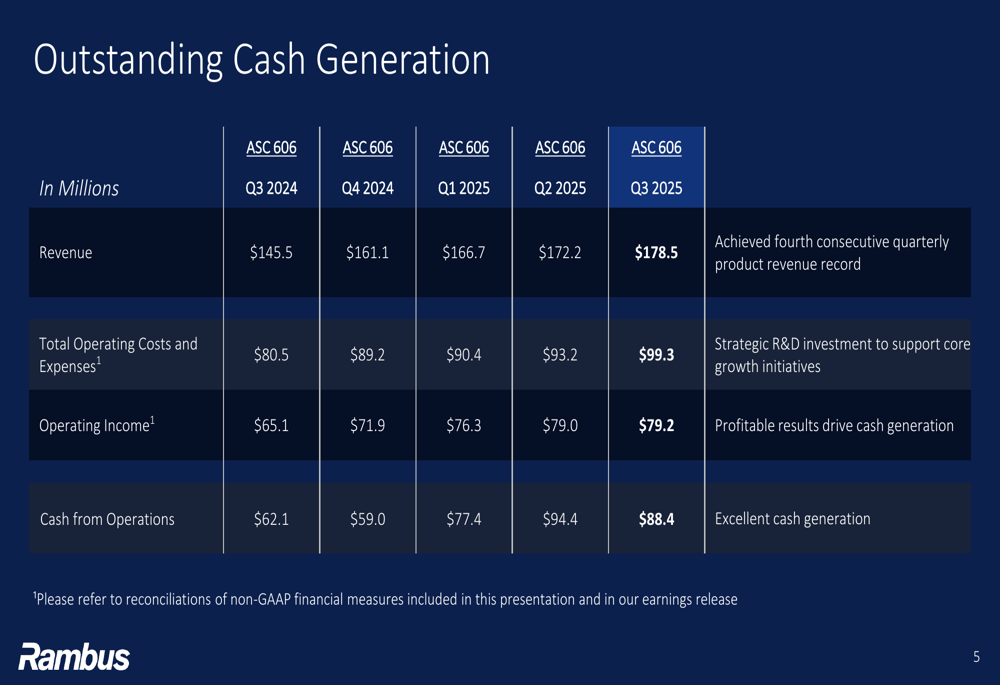

Rambus reported total revenue of $178.5 million for Q3 2025, representing a significant increase from $145.5 million in the same period last year. The company achieved its fourth consecutive quarterly product revenue record at $93 million, primarily driven by its Memory Interface Chips business.

As shown in the following highlights from the company’s presentation:

Cash from operations reached $88.4 million, marking an excellent quarterly result and demonstrating the company’s ability to convert growth into cash flow. This represents a substantial increase from $62.1 million in Q3 2024.

The detailed financial performance over the past five quarters shows consistent growth across key metrics:

Rambus reported earnings per share of $0.63, in line with the forecasted $0.63.

Detailed Financial Analysis

Rambus’s balance sheet continues to strengthen, with total cash and marketable securities increasing to $673.3 million in Q3 2025 from $432.7 million in Q3 2024, representing a 55.6% year-over-year increase. The company remains debt-free, providing significant financial flexibility to pursue strategic initiatives.

The following slide illustrates the company’s strong financial position:

Operating income increased to $79.2 million in Q3 2025 from $65.1 million in the same quarter last year, despite higher operating costs and expenses ($99.3 million vs. $80.5 million year-over-year). The company attributed the increased expenses to strategic R&D investments supporting core growth initiatives.

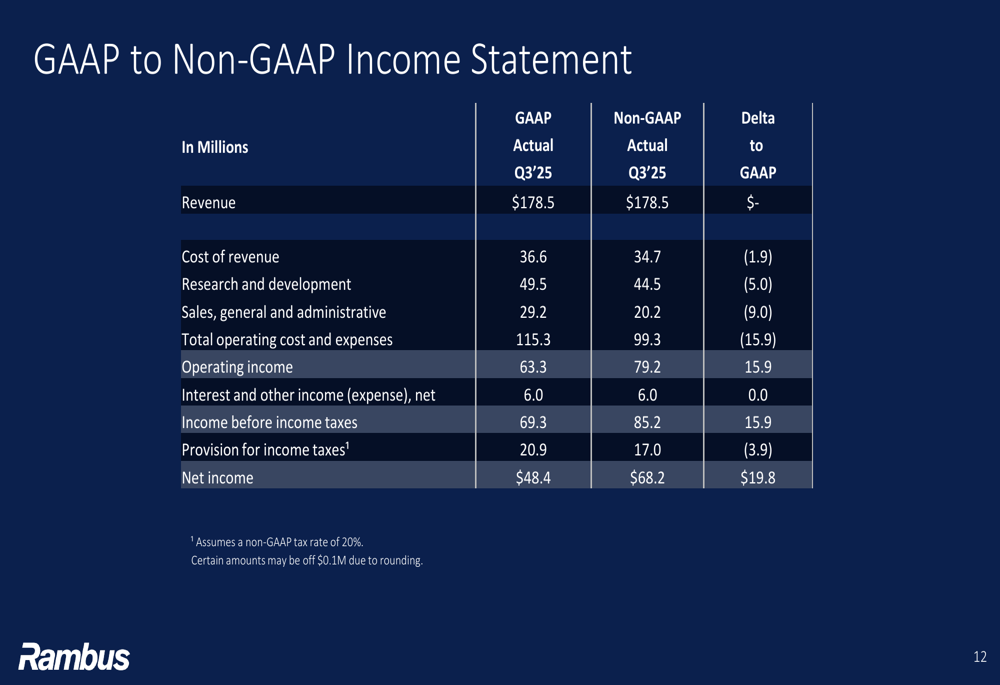

For investors seeking to reconcile GAAP and non-GAAP figures, the company provided detailed breakdowns of its financial metrics:

Strategic Initiatives & Market Positioning

Rambus continues to focus on expanding its leadership in the data center and AI markets, with particular emphasis on DDR5 RCD (Registering Clock Driver) technology. The company’s presentation highlighted its alignment with positive trends in these sectors, positioning it for long-term growth.

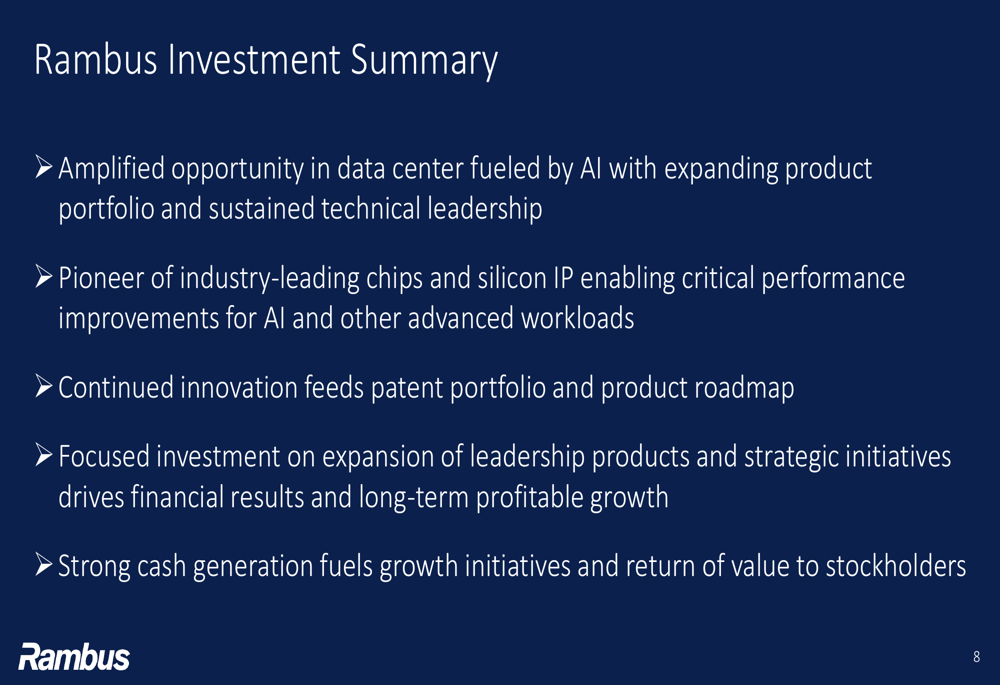

The investment summary slide outlines Rambus’s strategic focus and value proposition:

The company emphasized its role as a pioneer of industry-leading chips and silicon IP that enable critical performance improvements for AI and other advanced workloads. Continued innovation feeds both its patent portfolio and product roadmap, supporting sustainable growth.

CEO Luc Seraphin expressed optimism about the company’s future during the earnings call, stating, "We do see all the favorable tailwinds for our business going into 2026." He highlighted Rambus’s role in AI advancements, noting that their "groundbreaking memory connectivity and power management solutions are foundational to enabling the next generation of AI and HPC platforms."

Forward Guidance

Looking ahead to Q4 2025, Rambus provided the following non-GAAP outlook:

The company expects product revenue between $94-100 million for Q4 2025, continuing its growth trajectory. Licensing billings are projected at $60-66 million, with contract and other revenue between $25-31 million.

Management indicated that the company is on track to outpace the market with annual product revenue growth, driven by DDR5 RCD leadership and ramping contributions from new products. Additionally, Rambus anticipates its MRDIMM solutions to gain momentum by late 2026/2027.

While the company maintains a positive outlook, potential challenges include supply chain disruptions, market saturation in certain segments, macroeconomic pressures such as inflation, DRAM pricing fluctuations, and competition from other high-performance memory providers.

With its strong cash position, debt-free balance sheet, and strategic focus on high-growth markets, Rambus appears well-positioned to navigate these challenges while capitalizing on the expanding opportunities in AI and data center infrastructure.

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.