Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

Rapid7 Inc (NASDAQ:RPD), a cybersecurity analytics and automation provider, released its Q1 2025 company overview presentation on May 12, 2025, highlighting its strategic shift from aggressive growth to improved profitability in an expanding security operations market.

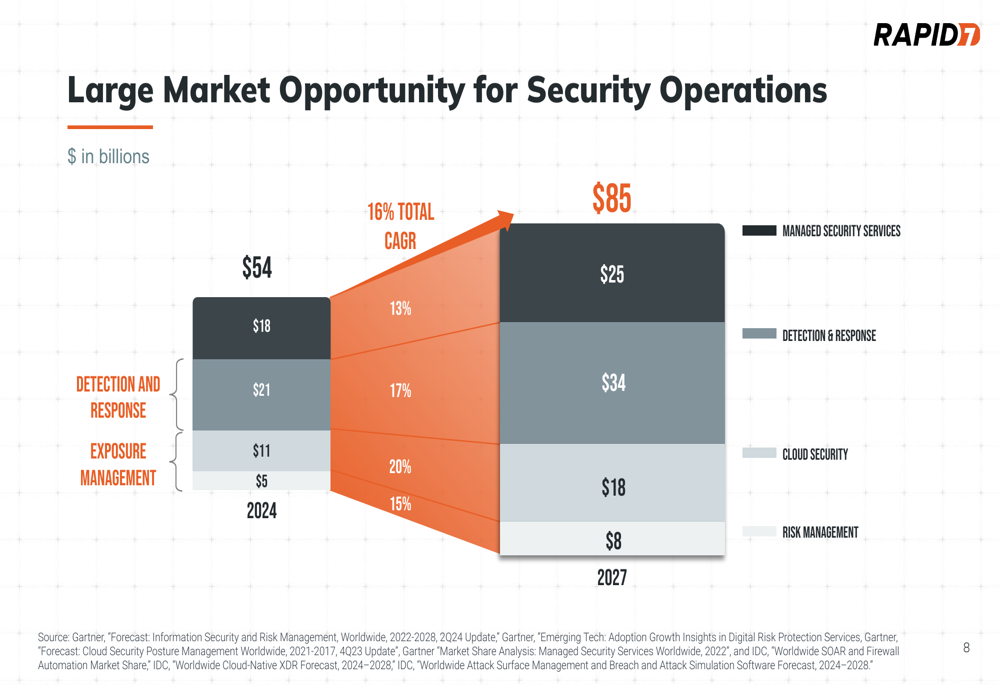

The presentation positions Rapid7 as a consolidator in the fragmented security operations landscape, which the company estimates represents a $54 billion market opportunity in 2024, expected to grow to $85 billion by 2027 at a 16% CAGR.

As shown in the following market opportunity chart, Rapid7 sees significant growth across all security operation categories, with Detection & Response representing the largest segment:

Despite recent market challenges mentioned in the company’s Q3 2024 earnings call, including elongated deal cycles particularly affecting larger North American contracts, Rapid7 continues to emphasize its comprehensive security platform approach as a competitive advantage.

Executive Summary

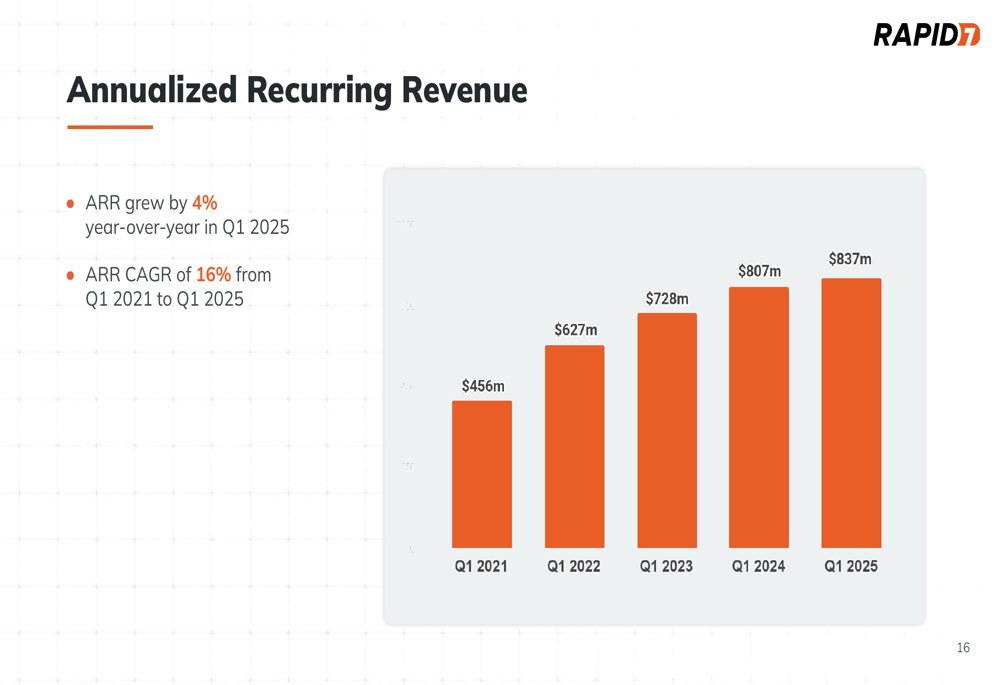

Rapid7 reported $837 million in Annualized Recurring Revenue (ARR) for Q1 2025, representing 4% year-over-year growth, a notable deceleration from previous years. However, the company has significantly improved profitability, with non-GAAP operating margins expanding to over 19% in 2024, up from just 0.5% in 2020.

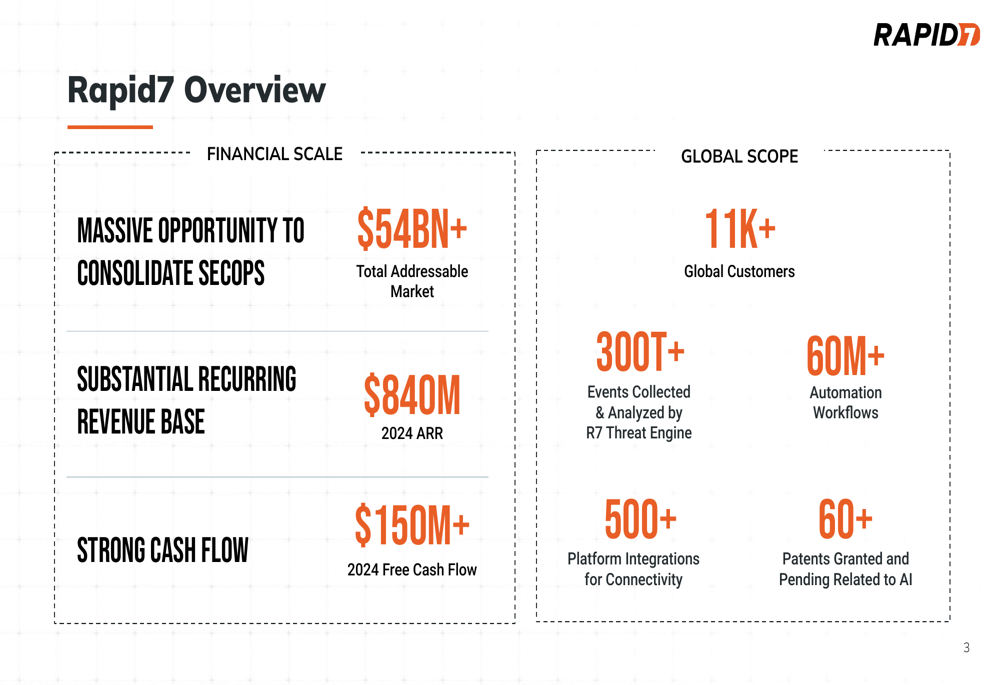

The company overview highlights Rapid7’s scale with over 11,000 global customers, $840 million in 2024 ARR, and more than $150 million in 2024 free cash flow. The presentation emphasizes the company’s AI capabilities, global threat intelligence, and extensive integration ecosystem with over 500 platform connections.

As illustrated in this company overview slide, Rapid7 positions itself as having substantial scale and global reach:

The company’s Q1 2025 guidance projects ARR of $850-880 million (1-5% growth) for the full year, with Q2 2025 revenue expected between $211-213 million and full-year revenue between $853-863 million.

Detailed Financial Analysis

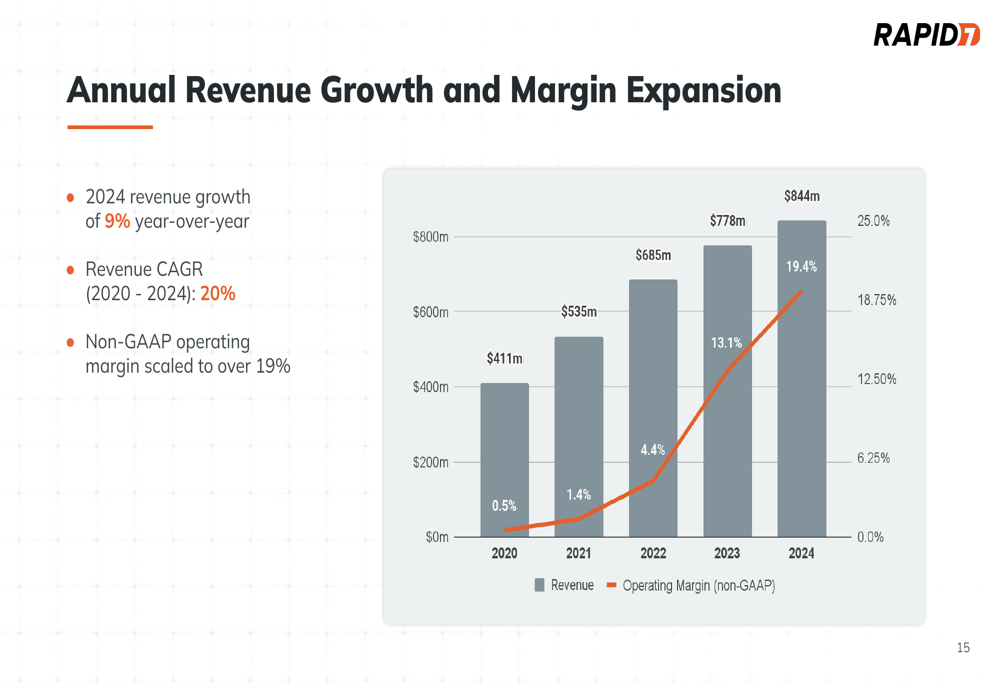

Rapid7’s financial trajectory shows a clear pivot from high growth to profitability focus. Annual revenue increased from $411 million in 2020 to $844 million in 2024, representing a 20% CAGR, though year-over-year growth slowed to 9% in 2024. Simultaneously, non-GAAP operating margins expanded dramatically from 0.5% to 19.4% over the same period.

The following chart illustrates this transition from growth to profitability:

ARR growth has moderated in recent quarters, with Q1 2025 showing 4% year-over-year growth to $837 million, compared to the 16% CAGR achieved from Q1 2021 to Q1 2025:

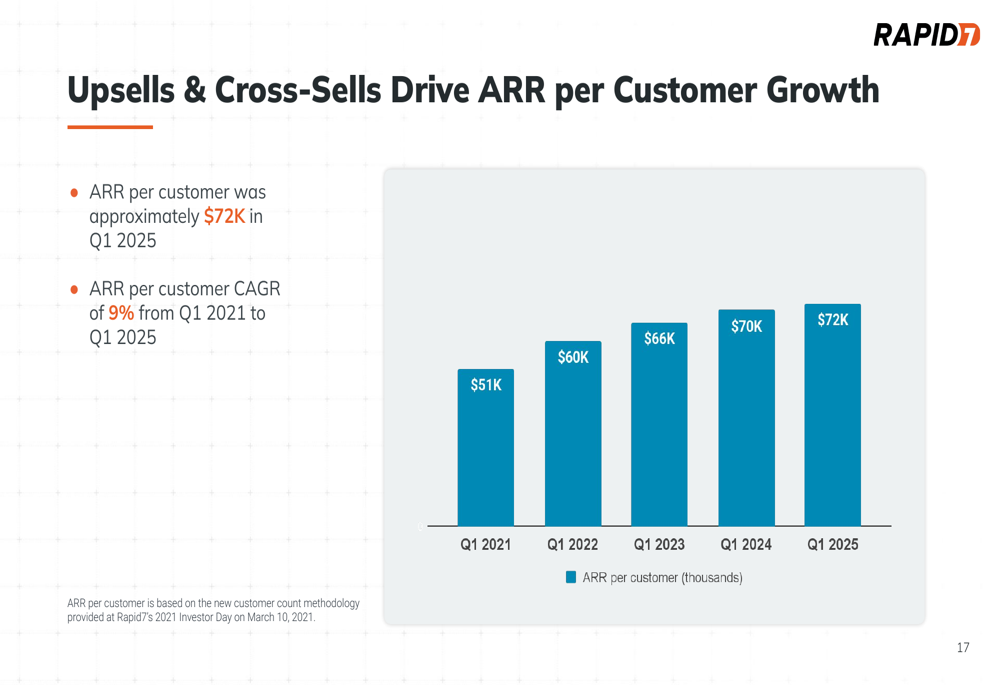

The company has successfully increased ARR per customer to approximately $72,000 in Q1 2025, up from $51,000 in Q1 2021, representing a 9% CAGR. This growth in customer value reflects Rapid7’s effective cross-selling and upselling strategy:

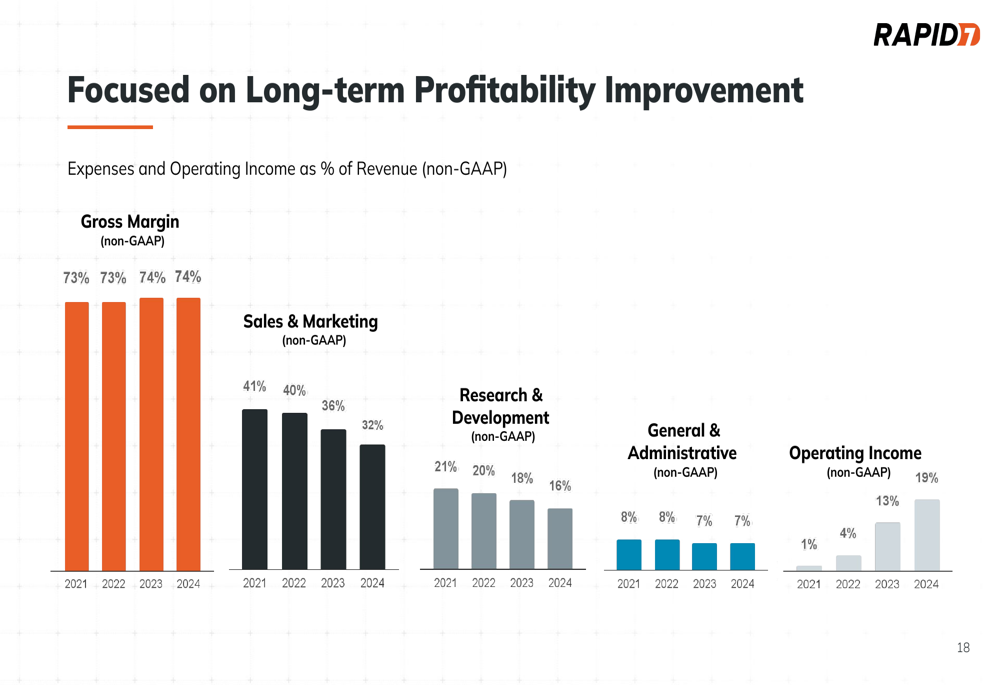

Rapid7’s profitability improvements stem from disciplined expense management. As a percentage of revenue, sales and marketing expenses decreased from 41% in 2021 to 32% in 2024, while research and development costs fell from 21% to 16% during the same period. These efficiency gains have directly contributed to the operating margin expansion:

Strategic Initiatives

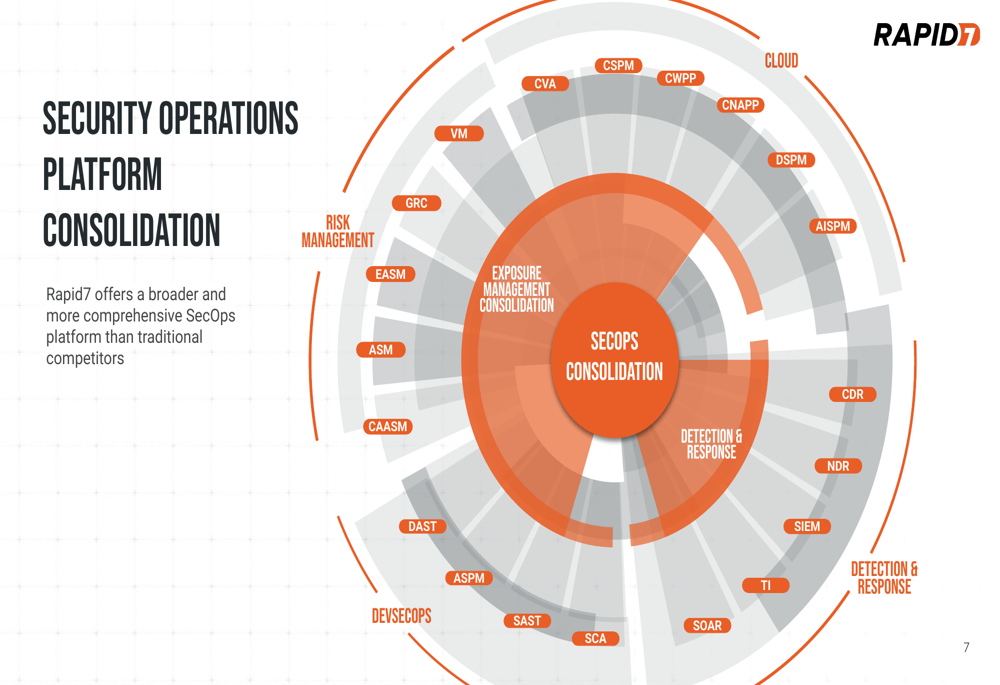

Rapid7’s presentation emphasizes its comprehensive security operations platform as a key differentiator. The company positions itself as offering broader capabilities than traditional competitors, spanning cloud security, risk management, detection and response, and development security operations.

The following diagram illustrates Rapid7’s security operations consolidation strategy:

The company identifies several market challenges driving its strategy, including the difficulty organizations face in securing fragmented attack surfaces, with more than 80% of organizations unable to see the majority of their attack surface according to Gartner (NYSE:IT) research cited in the presentation.

Rapid7’s value proposition centers on helping customers "anticipate, pinpoint, and act with confidence" through threat-aware risk context, actionable insights across diverse data sets, and expert-guided threat detection and response.

The company’s threat intelligence capabilities, branded as Rapid7 Labs, incorporate proprietary research, commercial threat feeds, and open-source communities to enhance product offerings. Additionally, Rapid7 has built a robust partner ecosystem including resellers, distributors, MSSPs, system integrators, and technology alliances.

Forward-Looking Statements

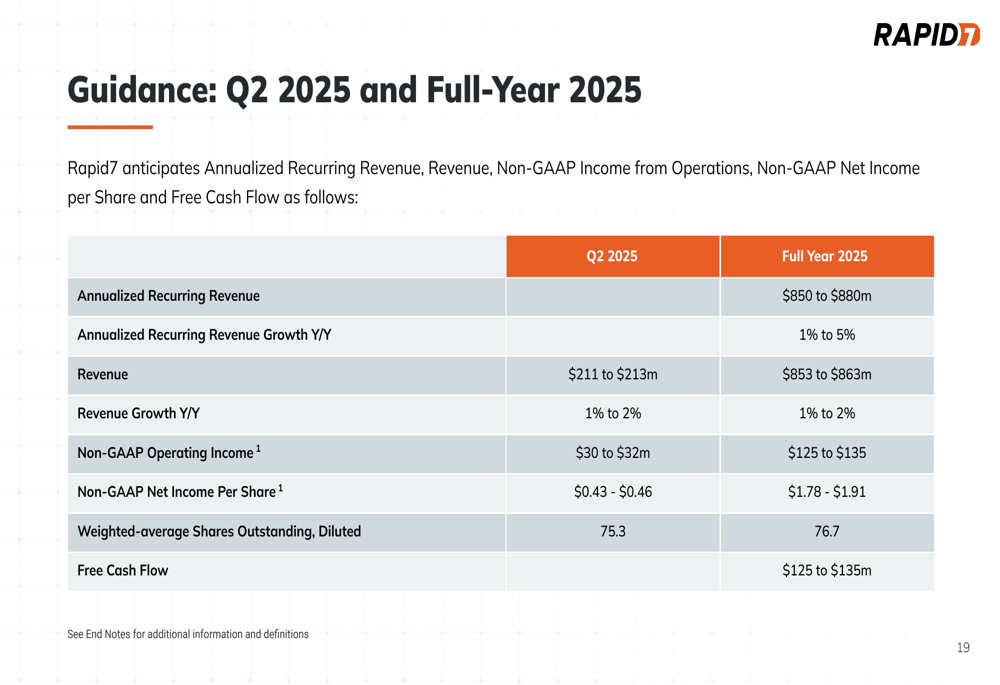

Rapid7’s guidance for Q2 and full-year 2025 suggests continued focus on profitability with modest growth expectations. For Q2 2025, the company projects revenue of $211-213 million with non-GAAP operating income of $30-32 million. Full-year 2025 guidance includes:

- ARR: $850-880 million (1-5% growth)

- Revenue: $853-863 million (1-2% growth)

- Non-GAAP Operating Income: $125-135 million

- Free Cash Flow: $125-135 million

The complete guidance is detailed in the following slide:

This outlook appears slightly more optimistic than the adjusted ARR guidance of $835-845 million mentioned in the company’s Q3 2024 earnings call, potentially indicating some improvement in business conditions.

However, the modest growth projections align with management’s previous comments about elongated deal cycles affecting larger contracts, particularly in North America. The company’s strategic shift toward partner-based initiatives, with 90% of new ARR bookings attributed to partnerships as mentioned in the Q3 2024 call, appears to be a response to these market challenges.

While Rapid7 faces growth headwinds in the near term, its improved profitability profile and focus on free cash flow generation provide financial stability as the company navigates the evolving cybersecurity landscape. The company’s positioning as a platform consolidator in the fragmented security operations market represents a long-term strategic bet on the industry’s direction, though execution will be critical in a competitive environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.