Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

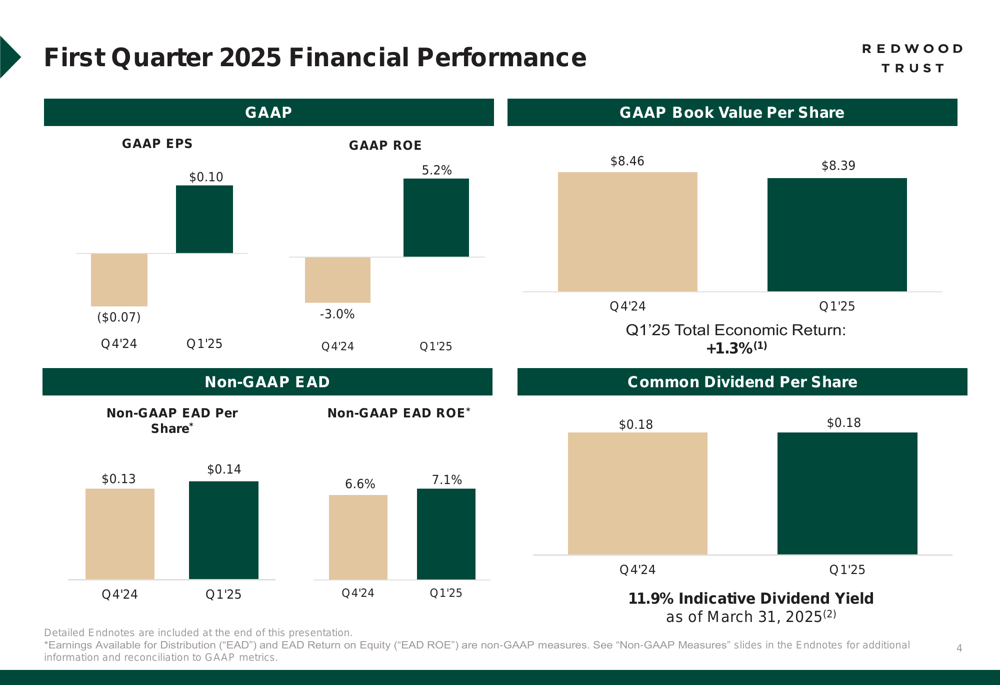

Redwood Trust, Inc. (NYSE:RWT) presented its first quarter 2025 financial results on April 30, showing a return to profitability after a challenging fourth quarter. The specialty mortgage real estate investment trust reported GAAP earnings per share of $0.10, compared to a loss of $0.07 in the previous quarter, while maintaining its $0.18 quarterly dividend.

Quarterly Performance Highlights

Redwood Trust reported a significant turnaround in profitability for Q1 2025, with GAAP return on equity reaching 5.2%, compared to -3.0% in Q4 2024. The company’s non-GAAP Earnings Available for Distribution (EAD) per share increased to $0.14 from $0.13 in the previous quarter, resulting in an EAD ROE of 7.1%.

"Our first quarter results demonstrate meaningful progress toward our strategic objectives, with improved performance across most business segments," said the company in its presentation materials.

As shown in the following chart of quarterly financial performance, Redwood Trust saw improvements in most key metrics compared to the previous quarter:

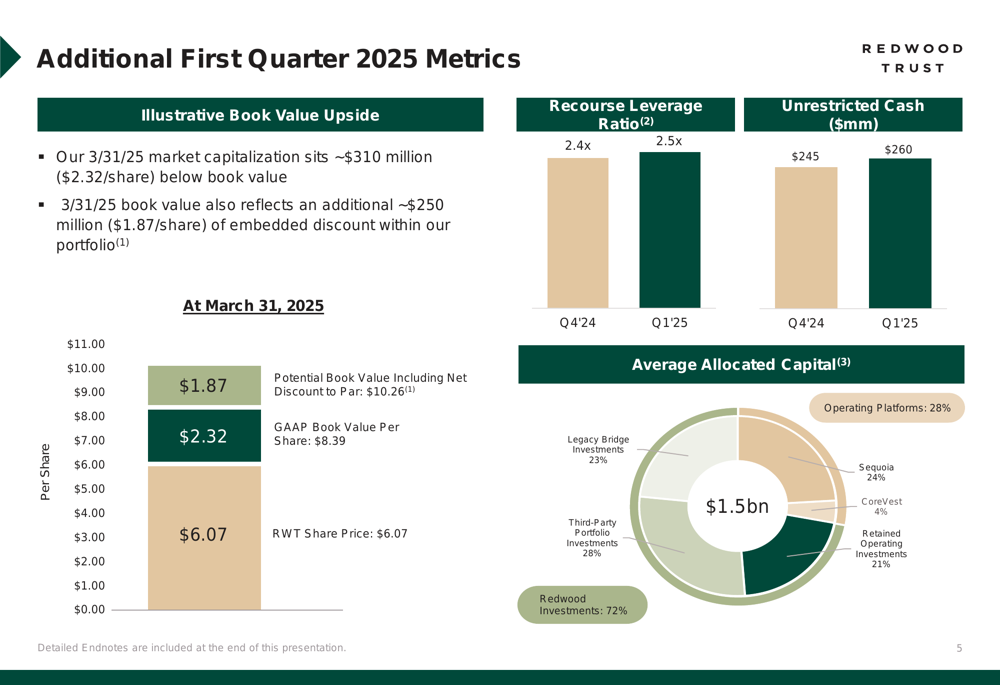

Despite the improved profitability, the company’s GAAP book value per share declined slightly to $8.39 from $8.46 at the end of 2024. However, Redwood highlighted that its market capitalization remains approximately $310 million ($2.32 per share) below book value, with an additional $250 million ($1.87 per share) of embedded discount within the portfolio.

The company’s total economic return for the quarter was 1.3%, while its dividend yield stood at an attractive 11.9% as of March 31, 2025, based on the current $0.18 quarterly dividend.

Segment Performance Analysis

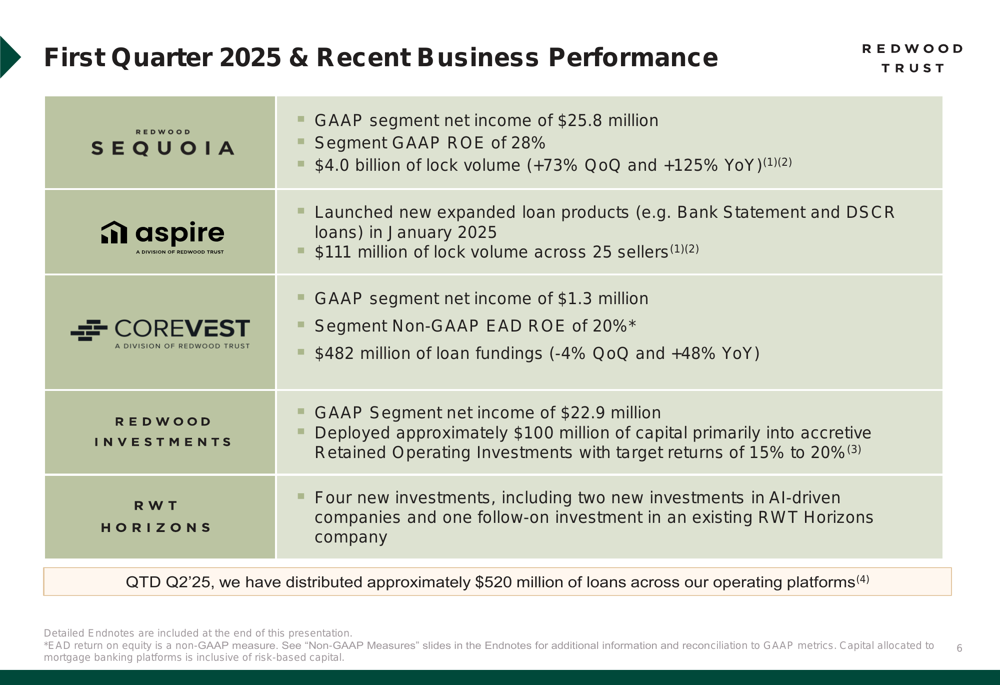

Redwood Trust operates through several business segments, with Sequoia (consumer home loan products) and CoreVest (business purpose loans) being the primary mortgage banking operations, complemented by Redwood Investments (portfolio management) and newer initiatives like Aspire and RWT Horizons.

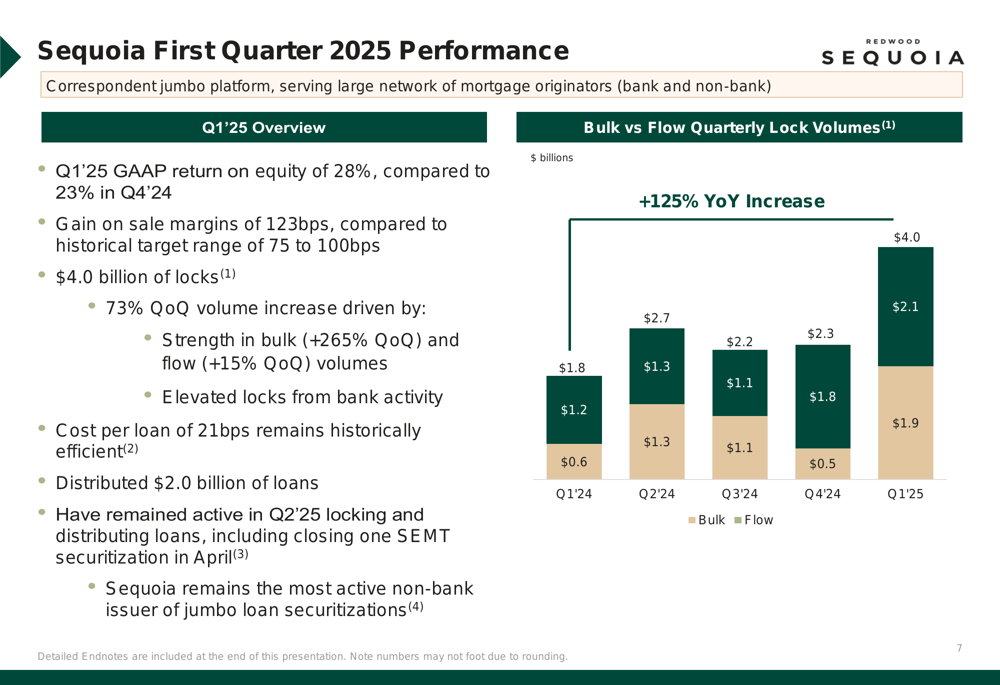

The Sequoia segment was the standout performer in Q1 2025, reporting GAAP segment net income of $25.8 million and a segment GAAP ROE of 28%. Lock volume reached $4.0 billion, representing a 73% increase quarter-over-quarter and a remarkable 125% year-over-year growth.

As illustrated in the following segment performance summary, each business unit contributed positively to the quarter’s results:

Sequoia’s performance was particularly impressive against industry benchmarks. While the broader mortgage industry saw a 22% decline in volumes from Q4 2024 to Q1 2025, Sequoia achieved 73% growth during the same period. The company attributed this outperformance to ongoing bank balance sheet management, including bulk transfers of seasoned loans, and growth in industry adjustable-rate mortgage production.

The following chart shows Sequoia’s quarterly lock volumes, with a significant increase in Q1 2025:

CoreVest, which focuses on loans to housing investors, reported GAAP segment net income of $1.3 million and a non-GAAP EAD ROE of 20%. The segment funded $482 million of loans, representing a 4% decrease quarter-over-quarter but a 48% increase year-over-year. Single-family bridge loans accounted for 59% of Q1 fundings, followed by term loans at 34%.

Redwood Investments, the company’s portfolio management segment, reported GAAP net income of $22.9 million. During the quarter, the segment deployed approximately $100 million of capital primarily into "accretive Retained Operating Investments" with target returns of 15% to 20%.

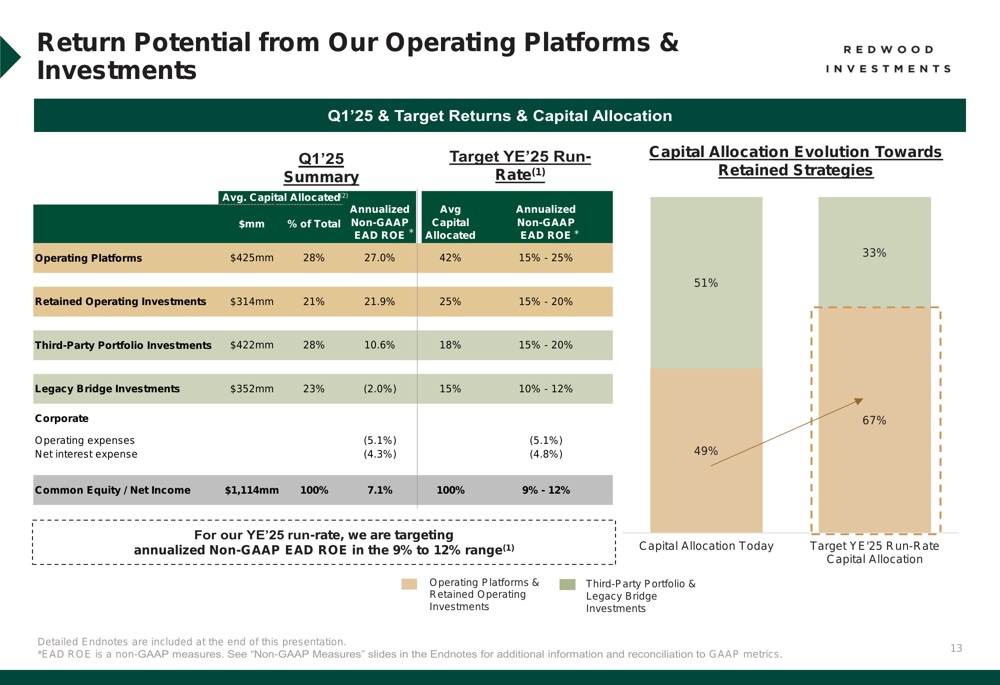

Strategic Initiatives and Capital Allocation

Redwood Trust outlined its strategy to improve returns through a shift in capital allocation. The company is targeting an increase in capital allocated to Retained Operating Investments from 21% in Q1 2025 to 67% in the future, while maintaining its Operating Platforms allocation at around 30%.

This strategic reallocation is expected to drive annualized non-GAAP EAD ROE to the 9% to 12% range by year-end 2025, up from the current 7.1%.

The company also highlighted progress with its newer Aspire segment, which launched expanded loan products in January 2025. Aspire locked $111 million of loans during the quarter across 25 sellers, with 72% in expanded loans and 28% in debt service coverage ratio (DSCR) loans.

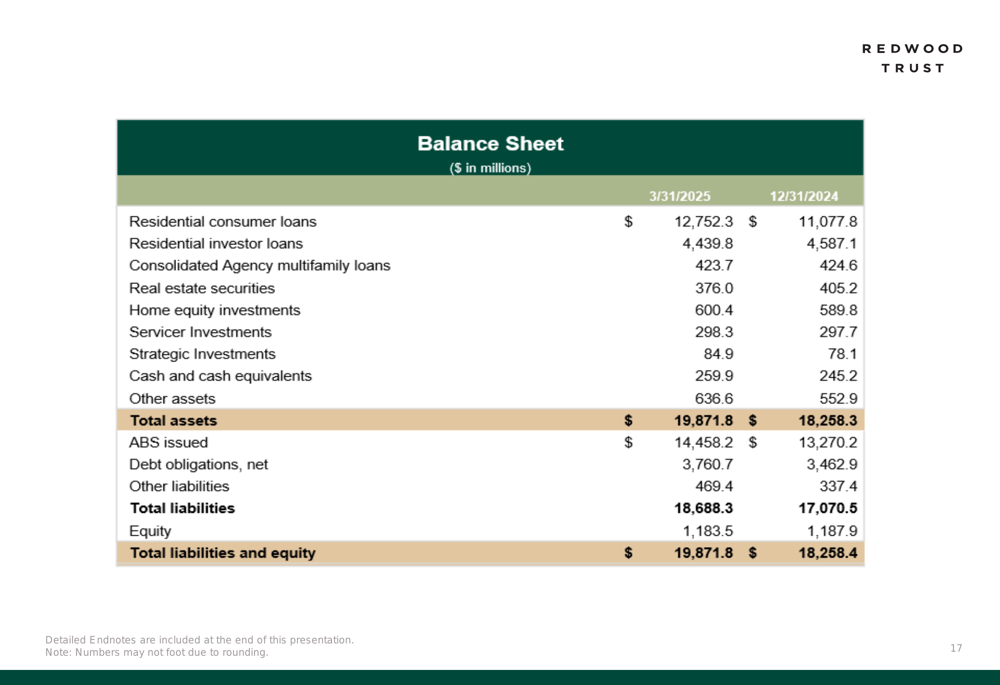

Financial Position and Outlook

Redwood Trust’s total assets increased to $19.87 billion as of March 31, 2025, compared to $18.26 billion at the end of 2024. Total (EPA:TTEF) equity stood at $1.18 billion, slightly down from $1.19 billion in the previous quarter.

The company maintained a recourse leverage ratio of 2.5x and reported unrestricted cash of $260 million. Total recourse debt increased slightly to $2.90 billion from $2.80 billion at year-end 2024.

Looking ahead, Redwood Trust appears positioned to benefit from its diversified business model and strategic focus on non-agency mortgage products. The company’s outperformance in loan volumes relative to industry trends suggests it may continue to gain market share, particularly in the jumbo loan segment where banks hold over $1 trillion of legacy collateral.

With its current trading price of $6.07 (as of March 31, 2025) significantly below book value, and a dividend yield near 12%, Redwood Trust offers an interesting value proposition for investors seeking exposure to the mortgage finance sector, provided the company can continue its trajectory of improving returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.