Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Redwood Trust Inc . (NYSE:RWT) presented its second quarter 2025 results on July 30, revealing a strategic acceleration toward core business segments amid challenging GAAP financial performance. The company, which specializes in products underserved by government "Agency" home loan programs, is capitalizing on significant shifts in the banking sector as traditional lenders retreat from residential mortgage lending.

The presentation comes after Redwood’s stock closed at $6.07 on July 29, up 1% for the day, according to market data. With a 52-week range of $4.68 to $8.15, the company continues to navigate a complex mortgage financing environment while maintaining its dividend.

Executive Summary

Redwood reported a GAAP loss of $(0.76) per share for Q2 2025, representing a significant deterioration from the $0.14 EPS reported in Q1. However, the company highlighted its Non-GAAP Core Segments EAD (Economic Adjusted Distributable) earnings of $0.18 per share with a 14.5% ROE, suggesting stronger underlying performance in its strategic business units.

The quarter was marked by robust operational metrics, including the largest quarter of Sequoia lock volume since 2021 ($3.3 billion) and the highest CoreVest funded volume since 2022 ($509 million). The company maintained its quarterly dividend at $0.18 per share, representing a 12.2% indicative yield.

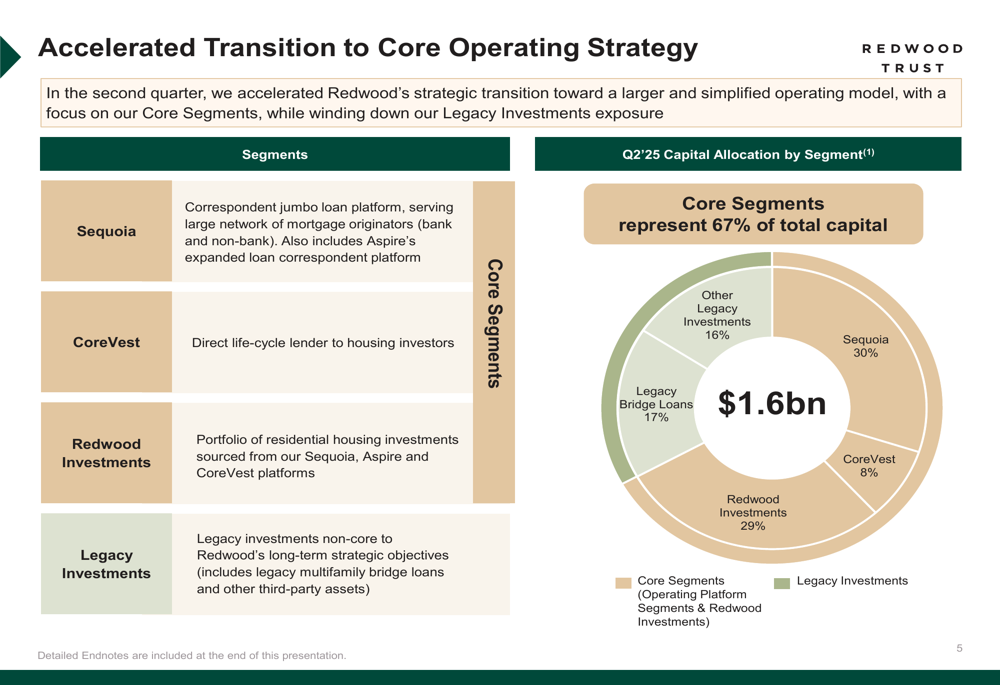

As shown in the following slide detailing Redwood’s strategic transition:

The company is accelerating its shift toward Core Segments (Sequoia, CoreVest, and Redwood Investments), which now represent 67% of its $1.6 billion total capital. This strategic pivot aims to simplify operations while winding down Legacy Investments exposure, which still accounts for 33% of capital allocation.

Quarterly Performance Highlights

Despite the negative GAAP results, Redwood’s mortgage banking platforms delivered strong returns exceeding 20% for the fourth consecutive quarter. The company distributed $3.5 billion of loans across its combined mortgage banking platforms in Q2, marking its most active quarter since 2021.

Book value per share stood at $7.49, with a total economic return of -8.6%. The company’s liquidity position improved from $260 million in Q1 to $302 million in Q2, though recourse debt increased from $2.9 billion to $3.3 billion.

The following slide summarizes the quarter’s key highlights and positioning:

Redwood’s loan distribution network continues to expand, with active relationships with over 210 jumbo loan sellers and approximately 40 non-QM loan sellers. The company reported a 65% quarter-over-quarter increase in Aspire loan sellers, demonstrating growing market penetration in the non-QM space.

Strategic Initiatives

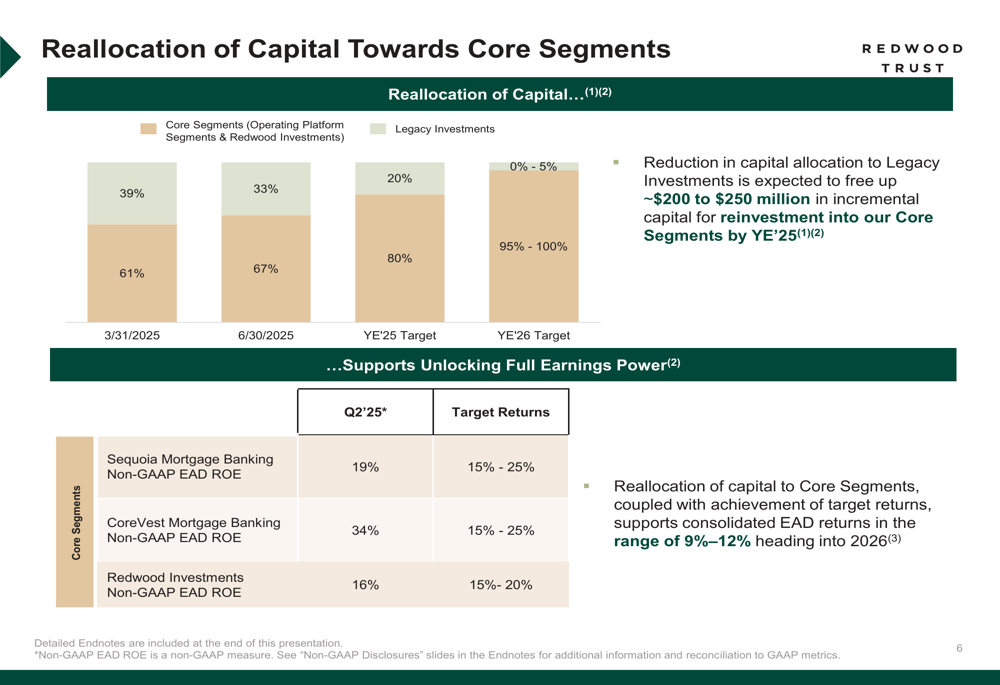

A central theme of Redwood’s presentation was its accelerated capital reallocation strategy, which aims to shift resources from Legacy Investments toward Core Segments. This transition is expected to free up approximately $200-250 million by year-end 2025.

The strategic shift is illustrated in the following chart:

The company targets reducing Legacy Investments from 33% of capital allocation currently to 0-5% by year-end 2026. Simultaneously, Redwood is targeting returns of 15-25% for its mortgage banking segments and 15-20% for Redwood Investments, with consolidated EAD returns of 9-12% heading into 2026.

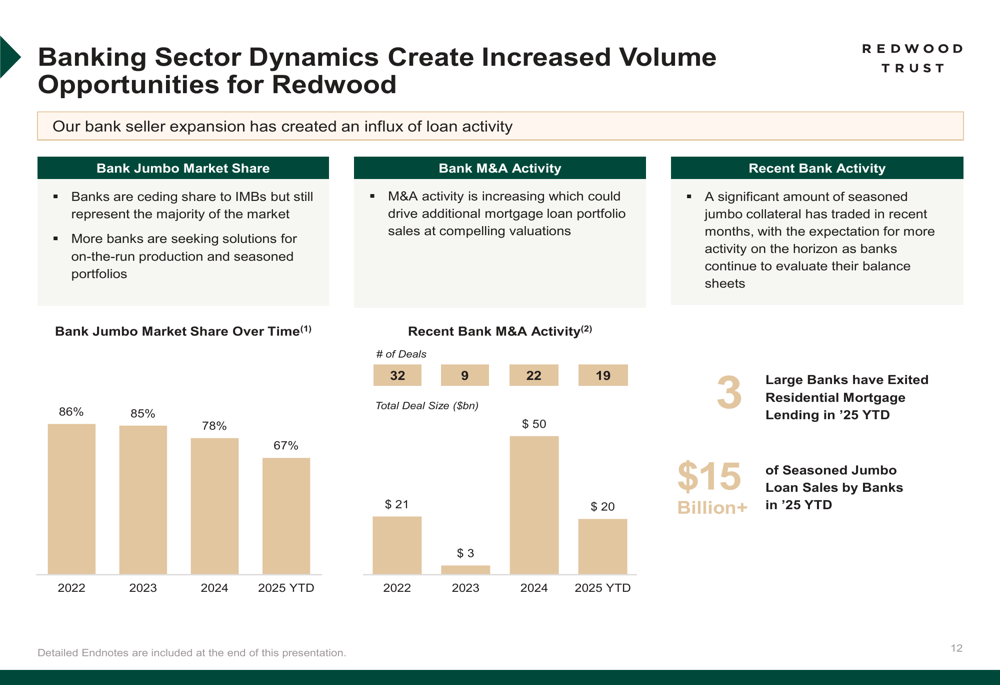

Redwood is positioning itself to capitalize on significant changes in the banking sector, where traditional lenders are retreating from residential mortgage lending. This market dynamic is creating increased volume opportunities for non-bank lenders like Redwood.

The following slide illustrates these banking sector dynamics:

Banks’ jumbo market share has declined from 86% in 2022 to 67% in 2025 YTD, creating opportunities for Redwood to expand its footprint. The company noted that over $15 billion of seasoned jumbo loans have been sold by banks in 2025 YTD, with more activity expected as banks continue to evaluate their balance sheets.

Segment Performance

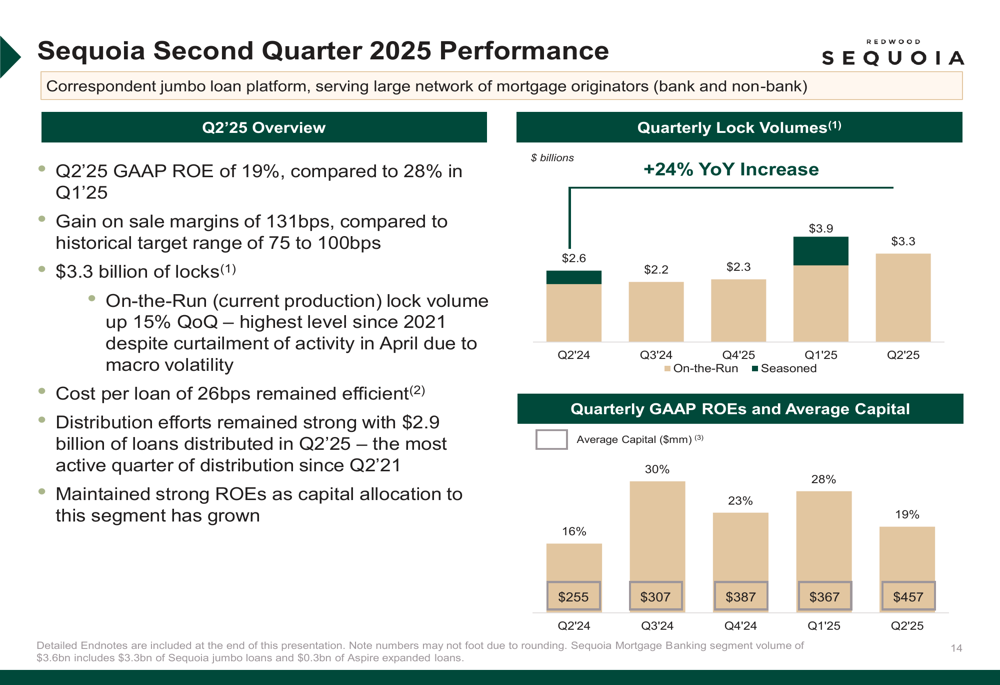

Redwood’s Sequoia segment, which focuses on jumbo mortgage lending, reported GAAP segment net income of $22.2 million with a 19% ROE in Q2. The segment achieved $3.6 billion of lock volume, representing a 30% year-over-year increase despite a 14% quarter-over-quarter decline.

The following slide details Sequoia’s quarterly performance:

CoreVest, which provides business purpose loans to housing investors, delivered GAAP segment net income of $6.1 million with a GAAP ROE of 27% and Non-GAAP EAD ROE of 34%. The segment funded $509 million of loans, up 6% quarter-over-quarter and 11% year-over-year.

Redwood Investments contributed GAAP segment net income of $11.9 million with a GAAP ROE of 11% and Non-GAAP EAD ROE of 16%. The segment deployed approximately $100 million of capital primarily into accretive retained operating investments.

The company’s Aspire platform, which focuses on non-QM lending, showed significant growth with $330 million of lock volume, representing a 197% quarter-over-quarter increase. Aspire’s loan seller network expanded to approximately 40 originators, up about 60% quarter-over-quarter.

Forward-Looking Statements

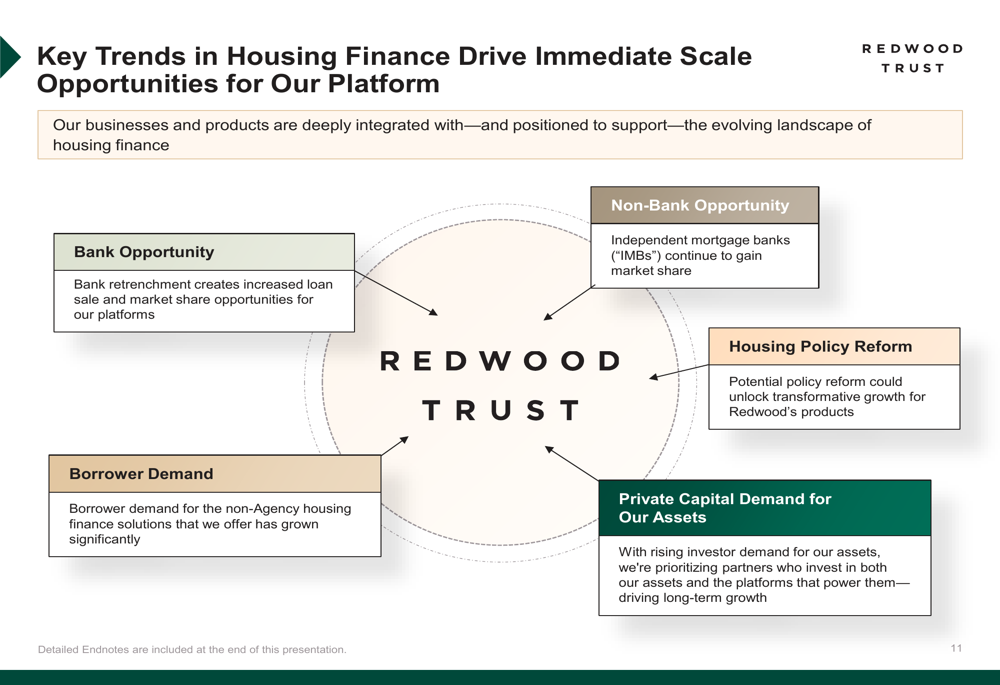

Looking ahead, Redwood identified several key trends driving growth opportunities for its platform:

The company expects to benefit from bank retrenchment, continued market share gains by independent mortgage banks, potential housing policy reform, growing borrower demand for non-Agency solutions, and increasing private capital demand for its assets.

For Q3 2025 quarter-to-date, Redwood reported locking/funding $1.6 billion of loans and distributing approximately $0.7 billion of loans across its operating platforms.

The company’s long-term strategy centers on establishing itself as the leading non-bank distributor of jumbo loans, leveraging its competitive advantages including faster turn times than peers and extensive securitization experience. Redwood highlighted its position as the #1 non-bank issuer of jumbo loan RMBS, with 144 RMBS securitizations and $70 billion of jumbo loan collateral securitized since inception.

As Redwood continues its strategic transition, investors will be watching closely to see if the company can translate its operational strengths into improved GAAP financial performance while maintaining its attractive dividend yield in a challenging mortgage market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.