Gold prices rebound as risk-off mood grips markets; US payroll data awaited

Introduction & Market Context

RE/MAX Holdings, Inc. (NYSE:RMAX) presented its third quarter 2025 earnings results on October 31, revealing mixed performance with declining revenue despite achieving record total agent count. The real estate franchisor reported revenue of $73.3 million, down 6.7% year-over-year, while maintaining stable profitability with a slight improvement in adjusted EBITDA margin.

The company continues to navigate a challenging U.S. housing market characterized by affordability concerns and elevated mortgage rates, which industry forecasts suggest will remain around 6.4% through 2026. RE/MAX’s stock traded at $8.27 following the earnings release, near its 52-week low of $6.90, reflecting ongoing investor caution about the company’s domestic performance.

Quarterly Performance Highlights

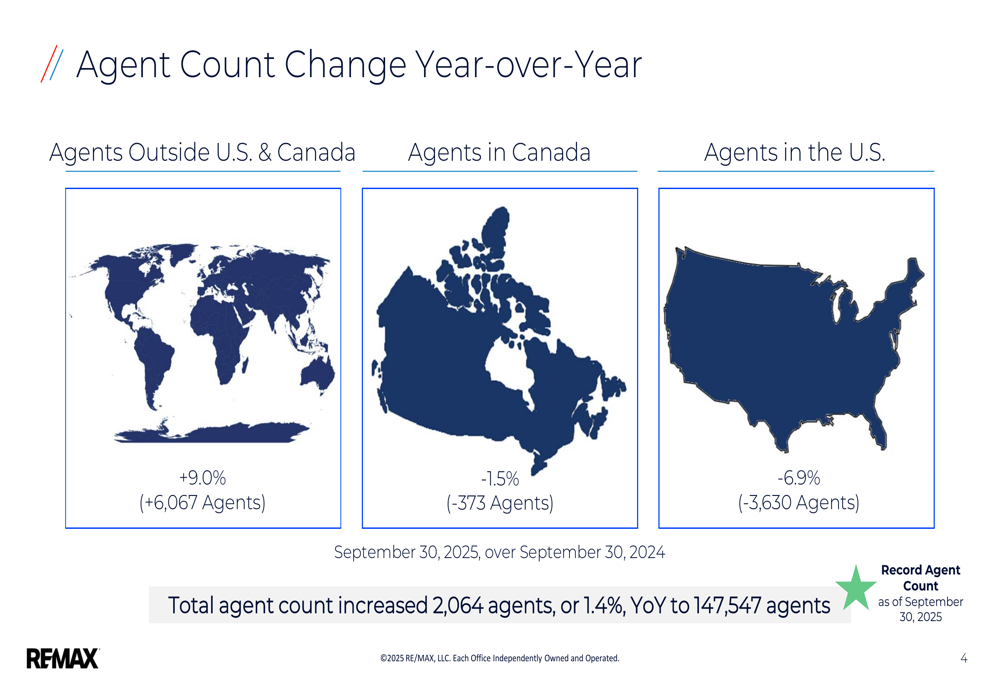

RE/MAX reported contrasting agent count trends across its markets. While total agent count reached a record 147,547 agents, representing a 1.4% year-over-year increase, this growth was entirely driven by international markets. Agent count outside the U.S. and Canada grew by 9.0% (+6,067 agents), while the combined U.S. and Canada agent count declined by 5.1% (-4,003 agents).

As shown in the following visualization of agent count changes:

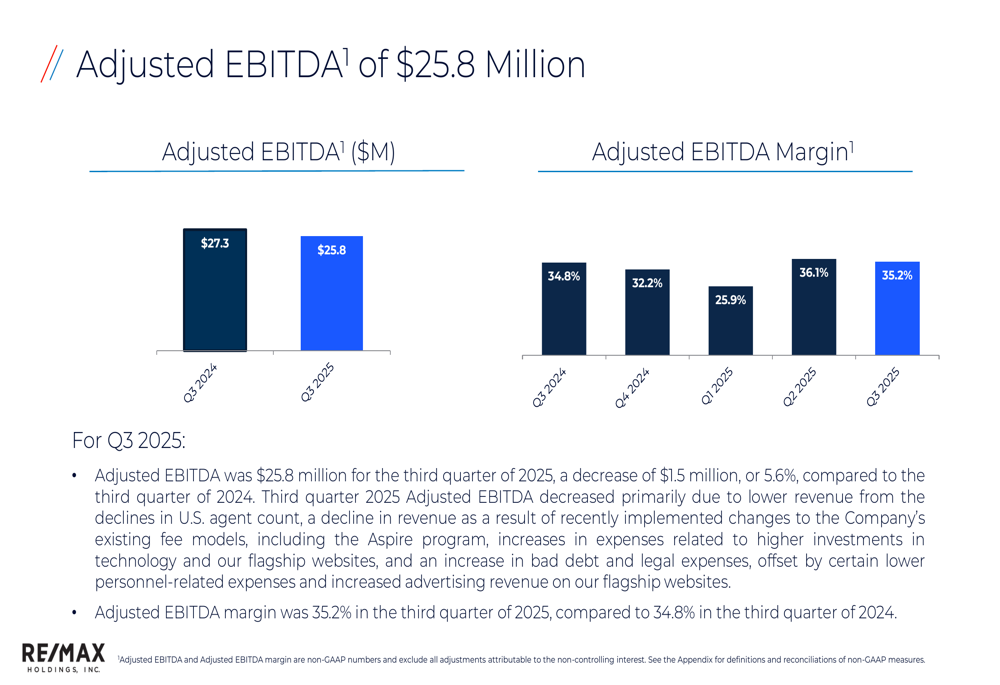

The company’s financial results reflected these operational challenges. RE/MAX reported adjusted diluted EPS of $0.37, slightly above analyst expectations of $0.36. Adjusted EBITDA was $25.8 million, down 5.6% year-over-year, though the adjusted EBITDA margin improved by 40 basis points to 35.2%.

The following chart illustrates the company’s adjusted EBITDA and margin trends:

Detailed Financial Analysis

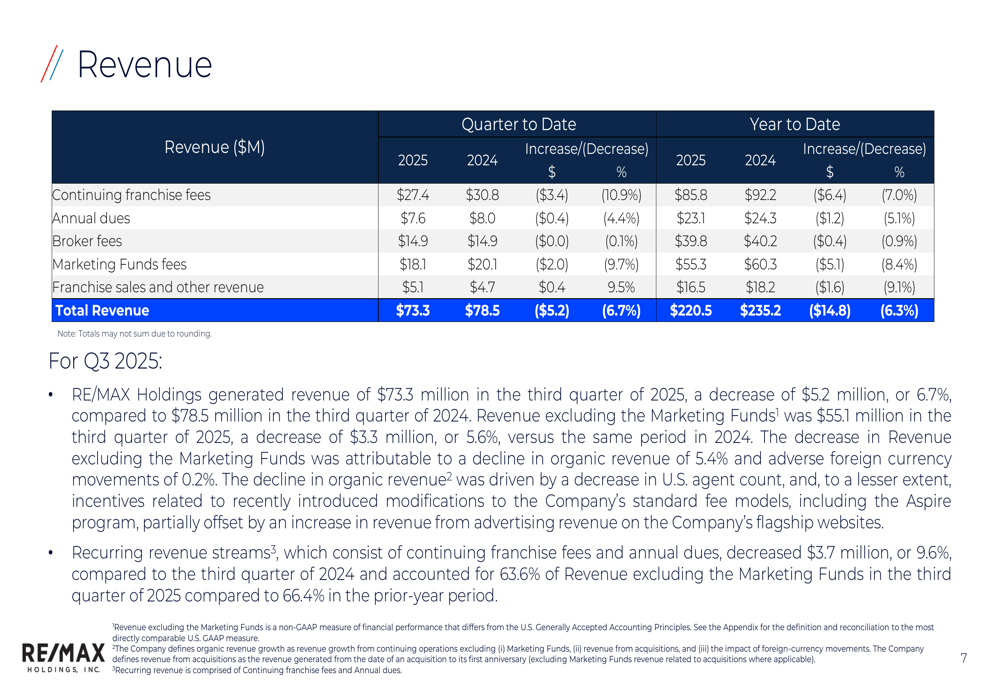

Revenue declined across most categories, with continuing franchise fees down 10.9% to $27.4 million and marketing funds fees down 9.7% to $18.1 million. The only revenue category showing growth was franchise sales and other revenue, which increased by 9.5% to $5.1 million.

The detailed revenue breakdown is presented in the following table:

Despite revenue challenges, RE/MAX managed to reduce its operating expenses by 9.7% year-over-year to $32.5 million. This reduction was primarily driven by a 21.0% decrease in personnel expenses, which fell to $18.5 million. However, professional fees increased significantly by 70.1% to $4.0 million.

The company maintained a strong balance sheet with a cash balance of $107.5 million as of September 30, 2025, up $10.9 million from December 31, 2024. RE/MAX reported $437.9 million in outstanding debt, with a total debt to trailing twelve-month adjusted EBITDA ratio of 4.6:1 and a net debt ratio of 3.5:1.

Strategic Initiatives

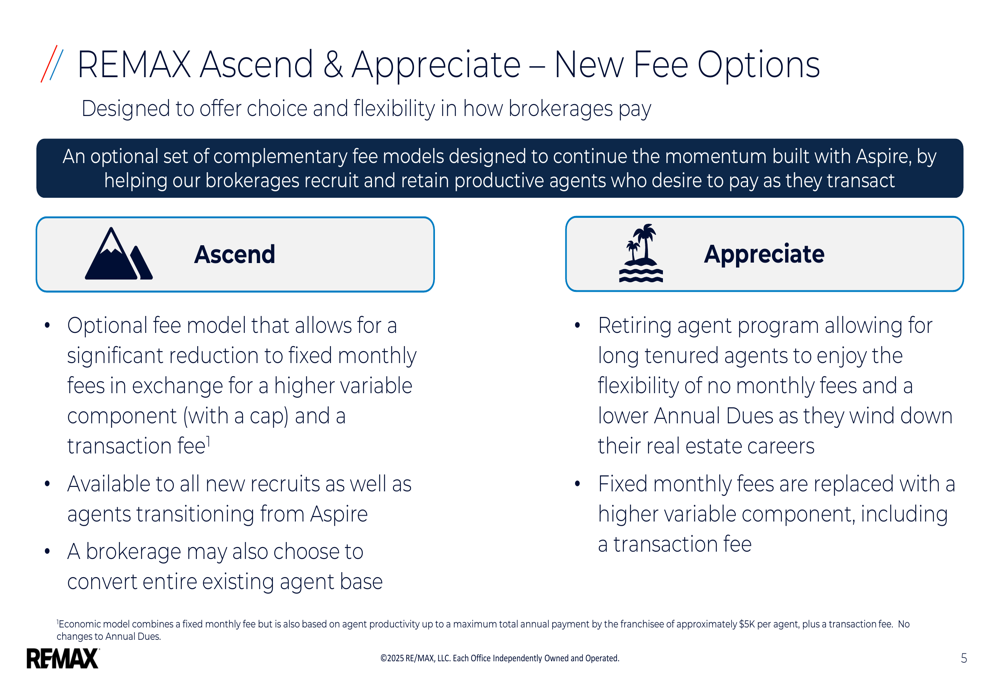

In response to the challenging domestic market, RE/MAX introduced two new fee options designed to provide flexibility for brokerages and agents. The "Ascend" model allows for reduced fixed monthly fees in exchange for higher variable components, while "Appreciate" targets retiring agents by eliminating monthly fees as they wind down their careers.

The company presented these new fee structures as follows:

Additionally, RE/MAX launched a new "Marketing as a Service" (MaaS) platform to enhance agent productivity and marketing capabilities. This digital platform provides agents with templates for creating various marketing materials, including social media posts, direct mail pieces, and other assets.

The MaaS platform interface is illustrated here:

CEO Erik Carlson emphasized the company’s strategic direction during the earnings call, stating, "We’re in a new era, one defined by clarity, purpose, and action." He noted positive early reception to the new marketing platform, reporting "a lot of inbound requests... which is very encouraging for our franchise sales and our network."

Forward-Looking Statements

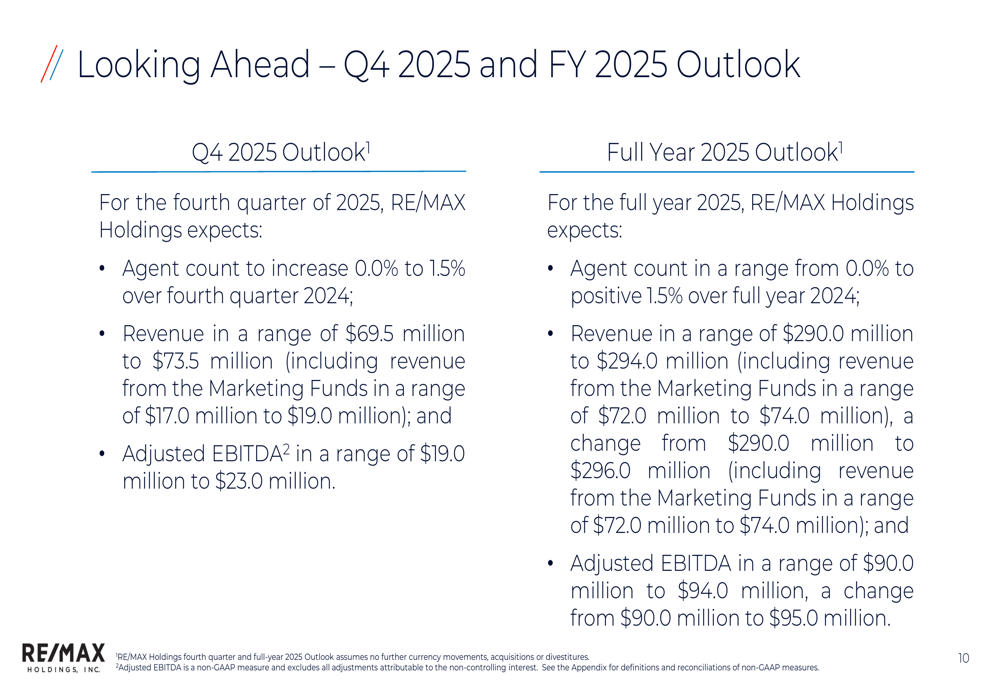

RE/MAX provided guidance for both Q4 2025 and the full year. For Q4, the company expects agent count to increase between 0.0% and 1.5% year-over-year, with revenue between $69.5 million and $73.5 million, and adjusted EBITDA between $19.0 million and $23.0 million.

For the full year 2025, RE/MAX projects:

- Agent count increase from 0.0% to positive 1.5% over full year 2024

- Revenue between $290.0 million and $294.0 million

- Adjusted EBITDA between $90.0 million and $94.0 million

The outlook is presented in detail here:

The company faces several challenges moving forward, including declining organic revenue, persistent housing market affordability issues, and industry consolidation pressures. However, management remains focused on enhancing its value proposition and diversifying revenue streams, with particular emphasis on growing its mortgage business through Motto Mortgage, which the company highlights as the "First-and-Only National Mortgage Brokerage Franchise in U.S."

RE/MAX continues to position itself as a leading dual-brand franchisor, emphasizing its global footprint and recurring revenue model with high margins and strong free cash flow generation. The effectiveness of its new fee models and marketing platform in reversing domestic agent decline will be crucial for the company’s performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.