Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Revolve Group LLC (NYSE:RVLV) presented its second quarter 2025 financial results on August 5, showing continued momentum with 9% year-over-year revenue growth despite ongoing retail sector challenges. The fashion e-commerce company’s stock responded positively, gaining 2.5% in aftermarket trading to $20.92, following a 1.22% increase during regular trading hours.

The Q2 results demonstrate a significant improvement from the company’s first quarter performance, when Revolve’s stock dropped 12.62% despite beating earnings expectations. This quarter’s presentation highlighted strong operational execution and exceptional cash flow generation, which appears to have resonated with investors despite a notable decline in net income.

Quarterly Performance Highlights

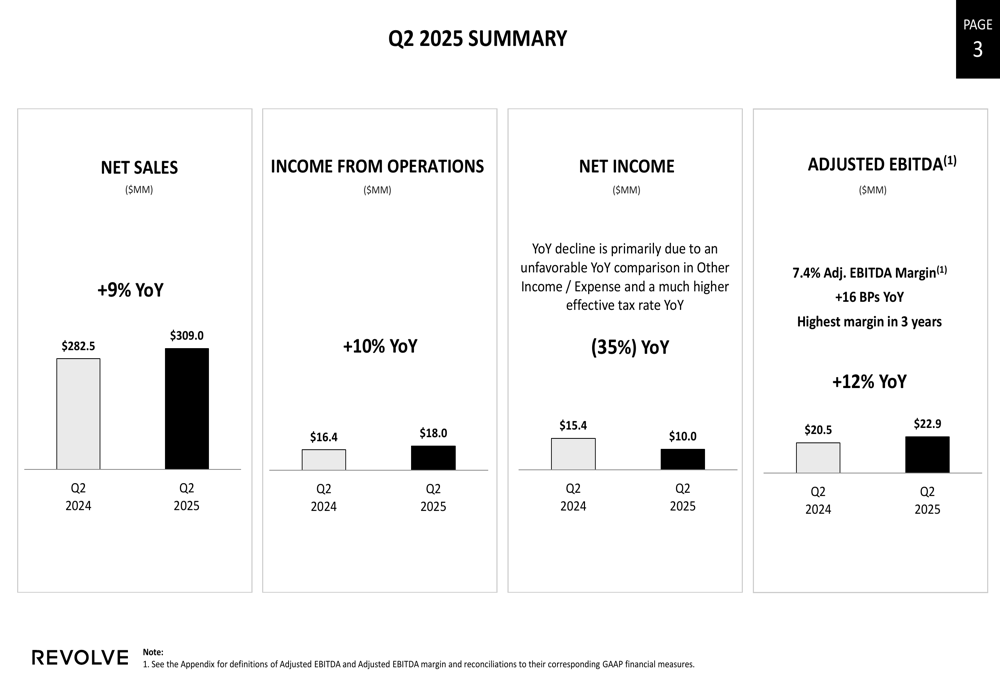

Revolve reported net sales of $309.0 million for Q2 2025, a 9% increase from $282.5 million in the same period last year. Income from operations grew 10% year-over-year to $18.0 million, while adjusted EBITDA increased 12% to $22.9 million, representing a margin of 7.4% – the highest in three years.

As shown in the following chart of quarterly financial performance:

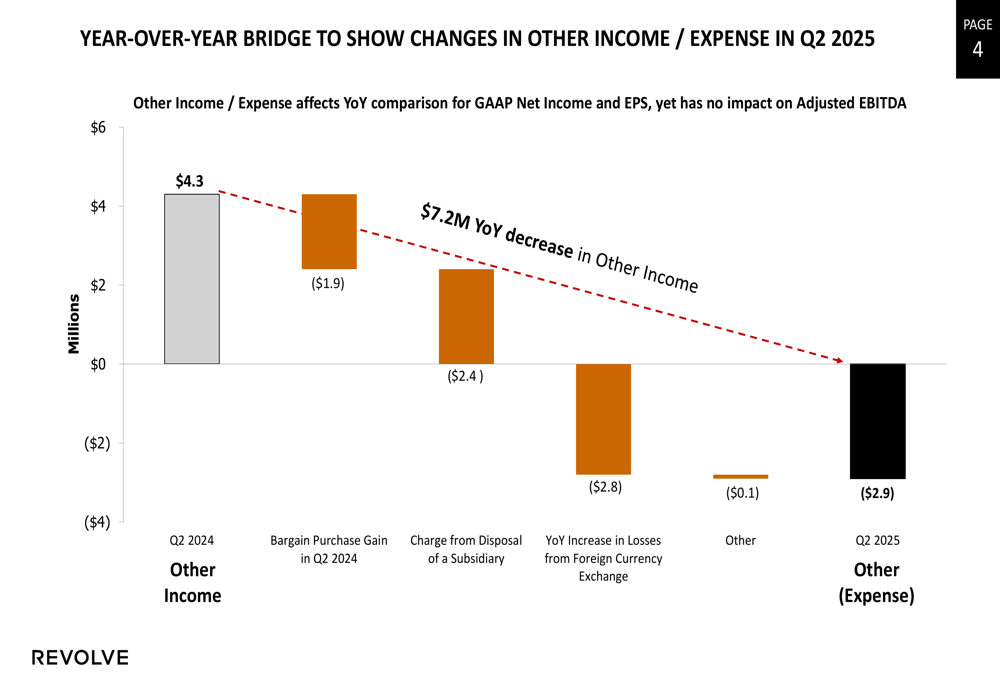

Despite operational improvements, net income declined 35% year-over-year to $10.0 million, resulting in diluted earnings per share of $0.14 compared to $0.21 in Q2 2024. This decline was primarily attributed to unfavorable comparisons in other income/expense items and a higher effective tax rate, rather than core business performance issues.

The company provided a detailed breakdown of the factors affecting the year-over-year comparison in other income/expense:

Detailed Financial Analysis

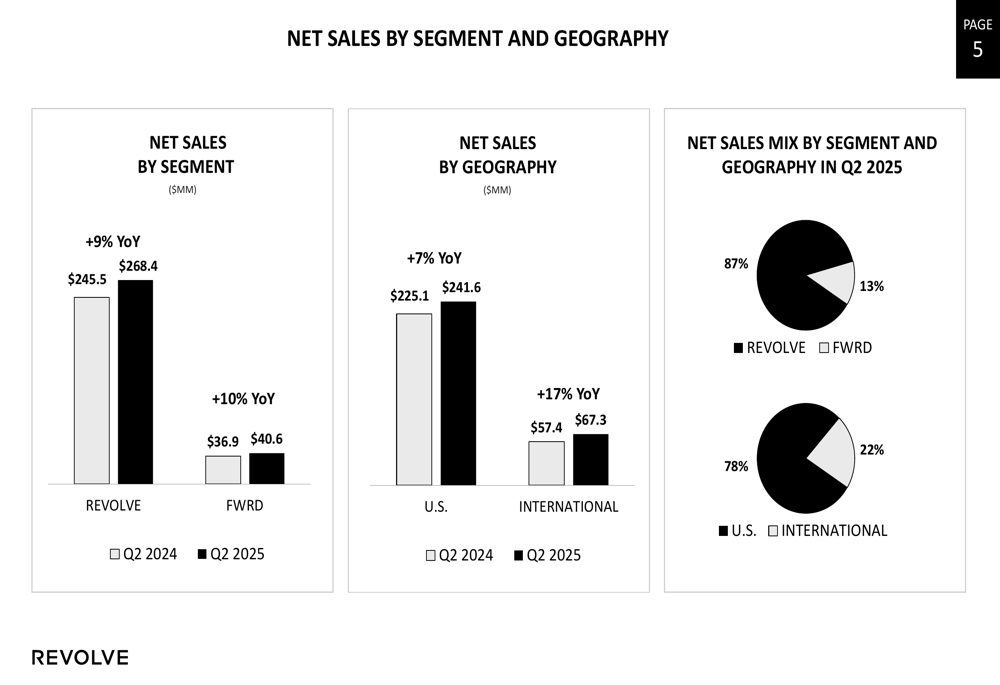

Both of Revolve’s business segments demonstrated strong growth, with the core REVOLVE segment increasing 9% year-over-year to $268.4 million and the luxury FWRD segment growing 10% to $40.6 million. Geographically, U.S. sales rose 7% to $241.6 million while international sales surged 17% to $67.3 million, highlighting the company’s successful global expansion.

The following chart illustrates the sales breakdown by segment and geography:

Revolve’s operating metrics showed healthy consumer engagement, with active customers increasing to 2.74 million and total orders placed reaching 2.42 million. Average order value grew to $300, reflecting the company’s ability to maintain premium positioning despite broader market pressures toward lower price points mentioned in previous earnings calls.

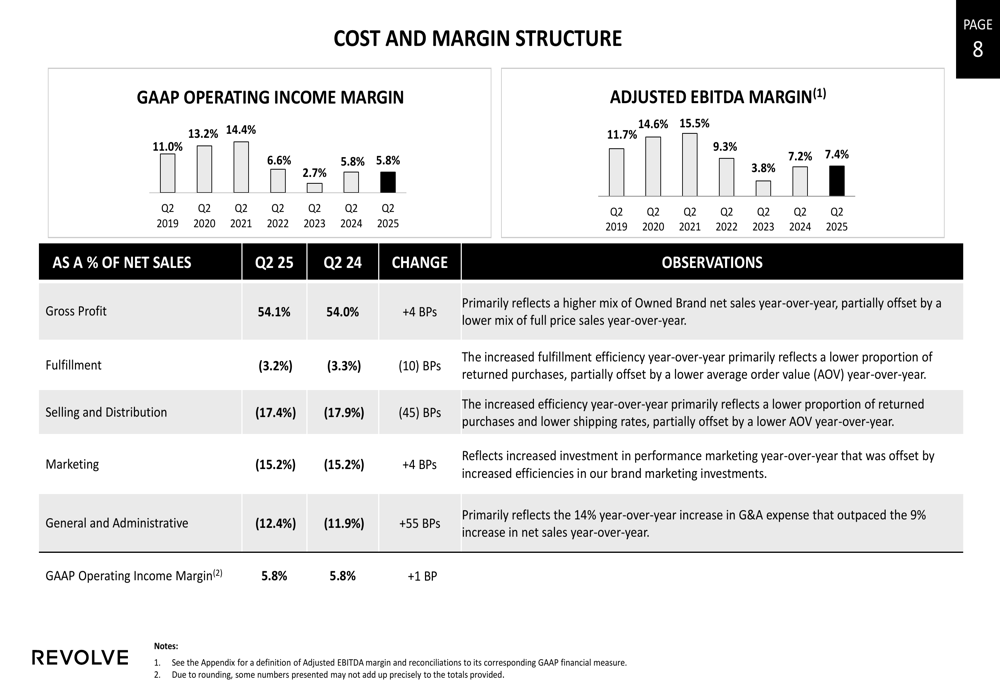

The company maintained stable margins, with GAAP operating income margin holding steady at 5.8% year-over-year, while adjusted EBITDA margin improved by 16 basis points to 7.4%. This performance is particularly noteworthy given the challenging retail environment and previous concerns about tariff impacts on gross margins.

The cost and margin structure breakdown reveals:

Cash Flow & Balance Sheet Strength

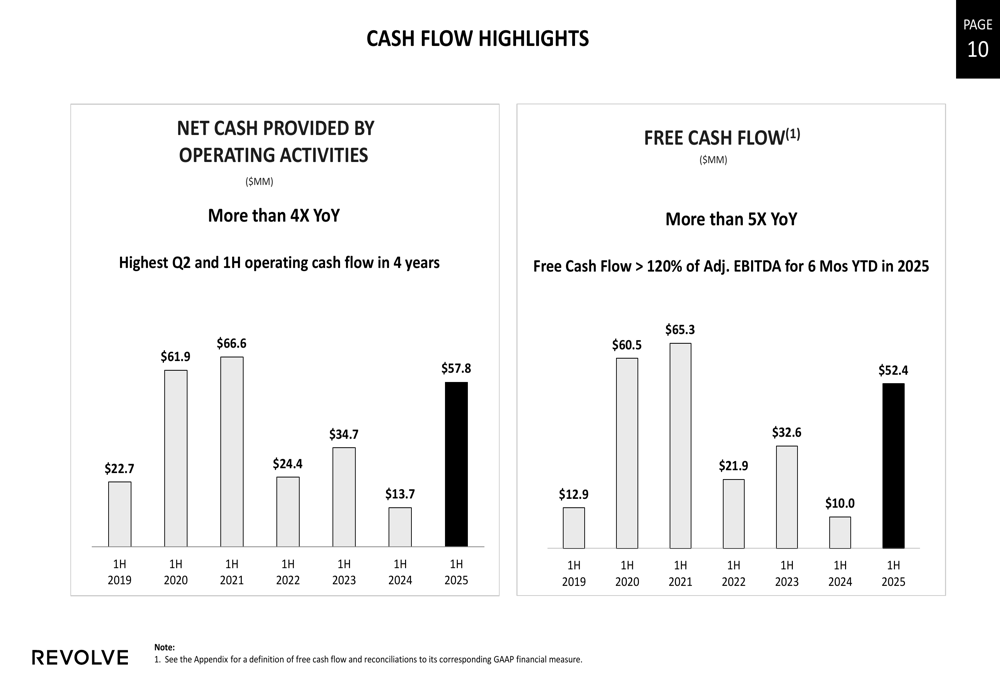

One of the most impressive aspects of Revolve’s Q2 performance was its exceptional cash flow generation. Operating cash flow increased more than four times year-over-year, reaching the highest Q2 and first-half levels in four years. Free cash flow grew more than five times compared to the prior year, exceeding 120% of adjusted EBITDA for the first six months of 2025.

The following chart highlights this dramatic improvement in cash flow:

The company’s balance sheet remains robust, with cash and cash equivalents reaching $310.7 million, up 27% year-over-year and 3% quarter-over-quarter. This strong cash position provides Revolve with significant flexibility for investments and shareholder returns.

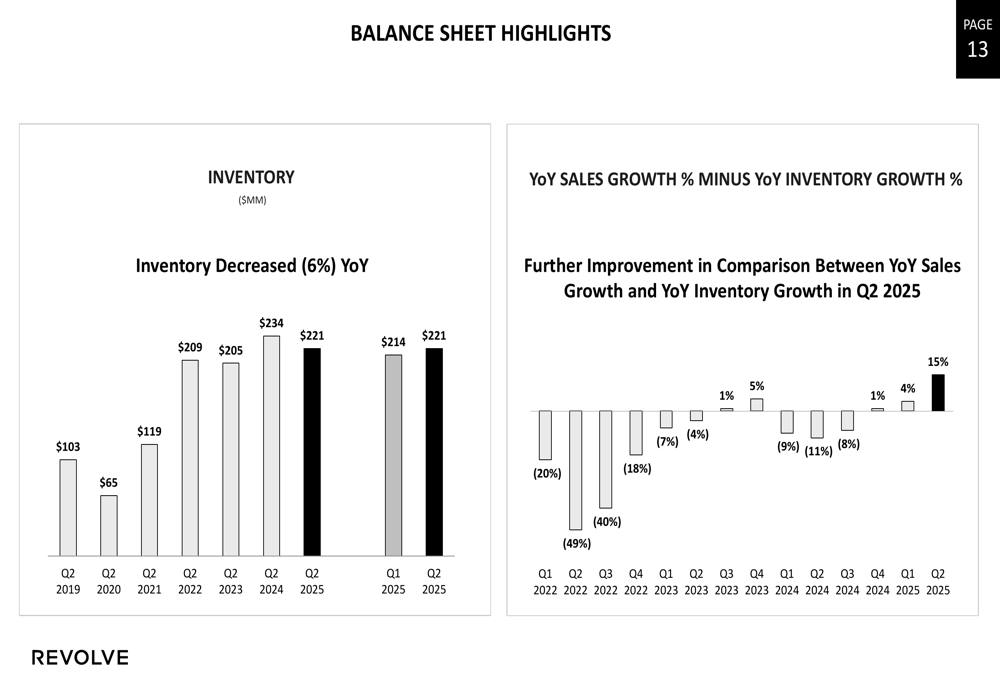

During Q2 2025, Revolve repurchased 92,583 shares of Class A common stock at an average cost of $18.78 per share, with $55.9 million remaining in its repurchase authorization. The company has also demonstrated improved inventory management, with inventory decreasing 6% year-over-year while sales grew 9%, creating a positive spread of 15 percentage points.

The inventory efficiency improvement is illustrated in this chart:

Strategic Initiatives & Forward Outlook

While the Q2 presentation didn’t explicitly update guidance, Revolve’s strategic focus appears to remain consistent with initiatives outlined in its Q1 earnings call, including continued investment in owned brands and AI technologies, with potential physical retail expansion including a new store at The Grove in Los Angeles.

The company’s strong cash position and improved operational efficiency suggest it is well-positioned to navigate ongoing macroeconomic uncertainties, including the tariff concerns that prompted a reduction in gross margin guidance to 50-52% during the previous quarter.

Revolve’s upcoming investor engagement includes participation in the Piper Sandler Growth Frontiers Conference scheduled for September 10, 2025, where management will likely provide additional insights into the company’s strategic direction and outlook.

The Q2 2025 results demonstrate Revolve’s resilience and operational execution despite challenging market conditions. While net income declined due to non-operational factors, the core business metrics—revenue growth, operational income improvement, customer acquisition, and cash flow generation—all point to underlying strength in the business model. The positive market reaction suggests investors are focusing on these fundamental performance indicators rather than the temporary impact on bottom-line results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.