Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

Riley Exploration Permian Inc (NYSE AMERICAN:REPX) presented its Q1 2025 investor update, highlighting the company’s strategic shift toward a more diversified energy business model while maintaining strong cash flow generation. Despite a recent pullback in share price to $24.88 (down 1.85% as of May 7), the company continues to emphasize its competitive position in the Permian Basin and expansion into midstream and power generation projects.

The oil-focused producer, which recently missed Q4 2024 earnings expectations with EPS of $0.96 versus the forecasted $1.60, is now positioning itself as a growth-oriented energy company with activities spanning upstream, midstream, and power sectors in Texas and New Mexico.

Q1 2025 Performance Highlights

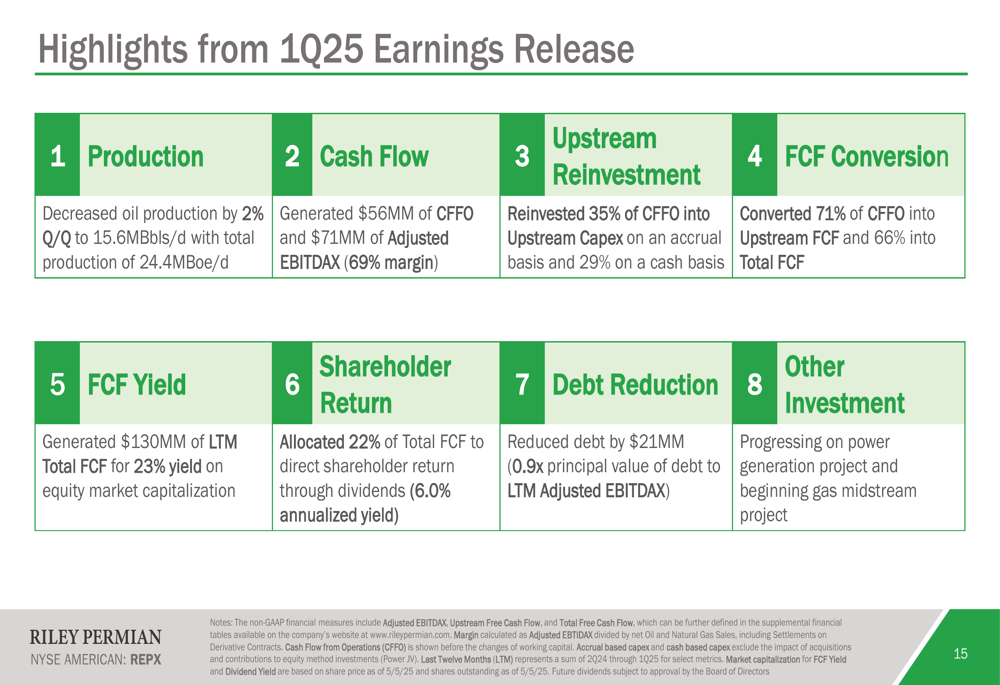

Riley Permian reported total production of 24.4 Mboe/d for Q1 2025, with oil production slightly decreasing by 2% quarter-over-quarter to 15.6 MBbls/d. Despite this modest decline in oil output, the company generated robust financial results with $56 million in cash flow from operations (CFFO) and $71 million in Adjusted EBITDAX, representing a 69% margin.

As shown in the following summary of quarterly performance metrics:

The company converted 71% of its CFFO into upstream free cash flow and 66% into total free cash flow. On a last-twelve-months basis, Riley generated $130 million in total free cash flow, representing a 23% yield on its equity market capitalization. This strong cash generation allowed the company to reduce debt by $21 million, bringing its leverage ratio to 0.9x.

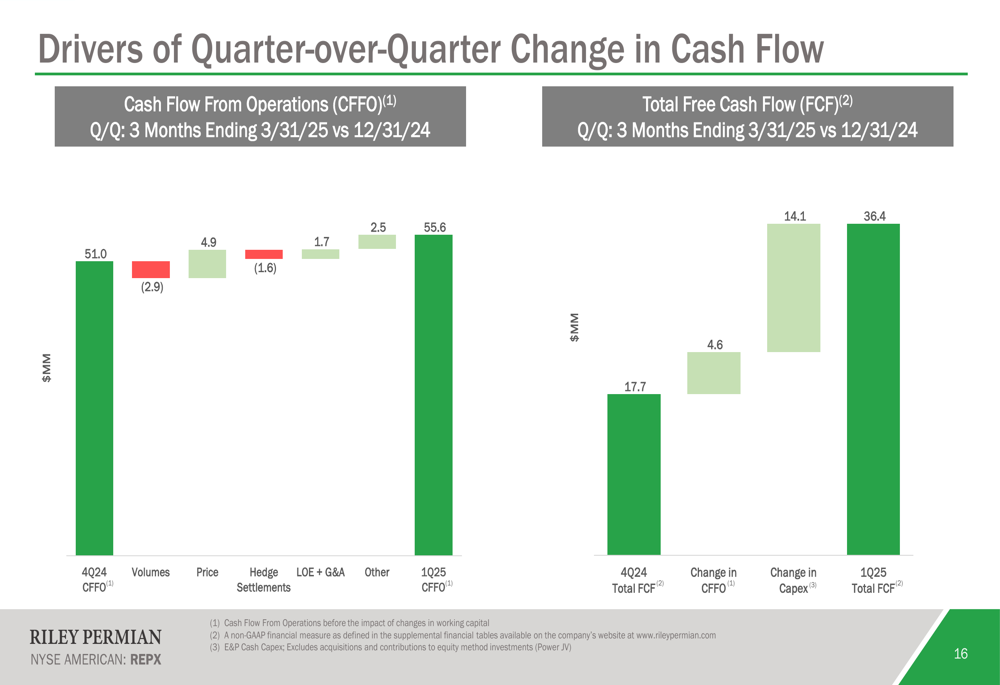

The drivers of Riley’s quarter-over-quarter cash flow changes reveal how price improvements offset volume declines:

Strategic Diversification Initiatives

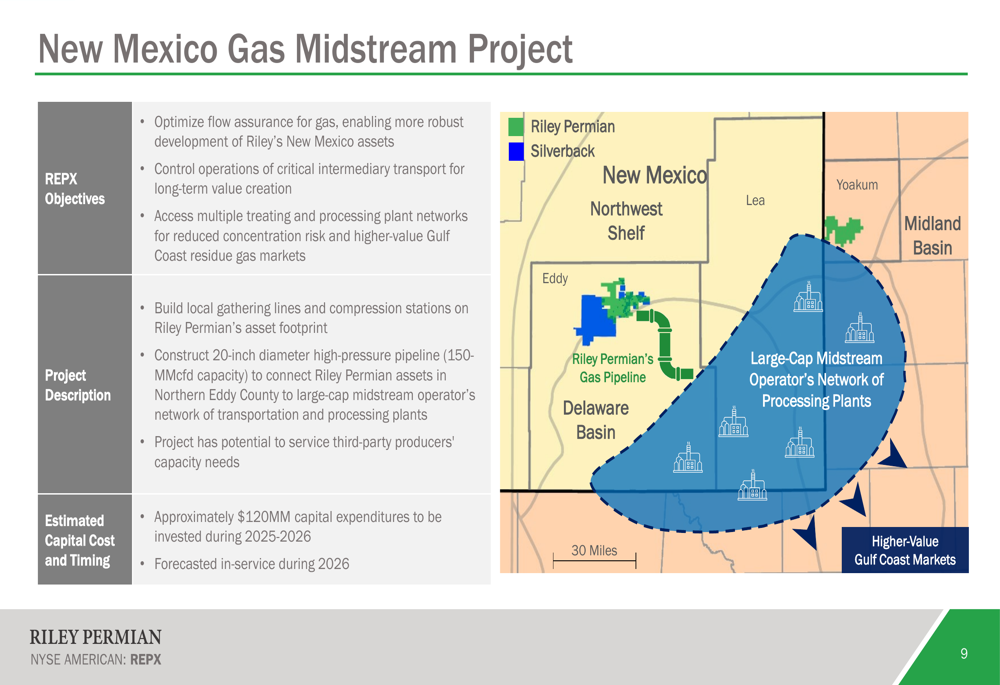

A key focus of Riley’s presentation was its diversification beyond traditional upstream operations. The company is developing a significant gas midstream project in New Mexico, which aims to optimize flow assurance and access multiple processing networks. This project involves building local gathering lines and a 20-inch high-pressure pipeline with 150 MMcfd capacity, requiring approximately $120 million in capital expenditures during 2025-2026.

The following map illustrates the scope and strategic positioning of this midstream initiative:

Additionally, Riley has formed a power joint venture (RPC (NYSE:RES) Power LLC) with Conduit Power LLC. The first project, focused on self-consumption with 20MW thermal nameplate capacity, is already operational. A second project aimed at selling power to the grid with 50MW thermal capacity has secured sites and completed permits.

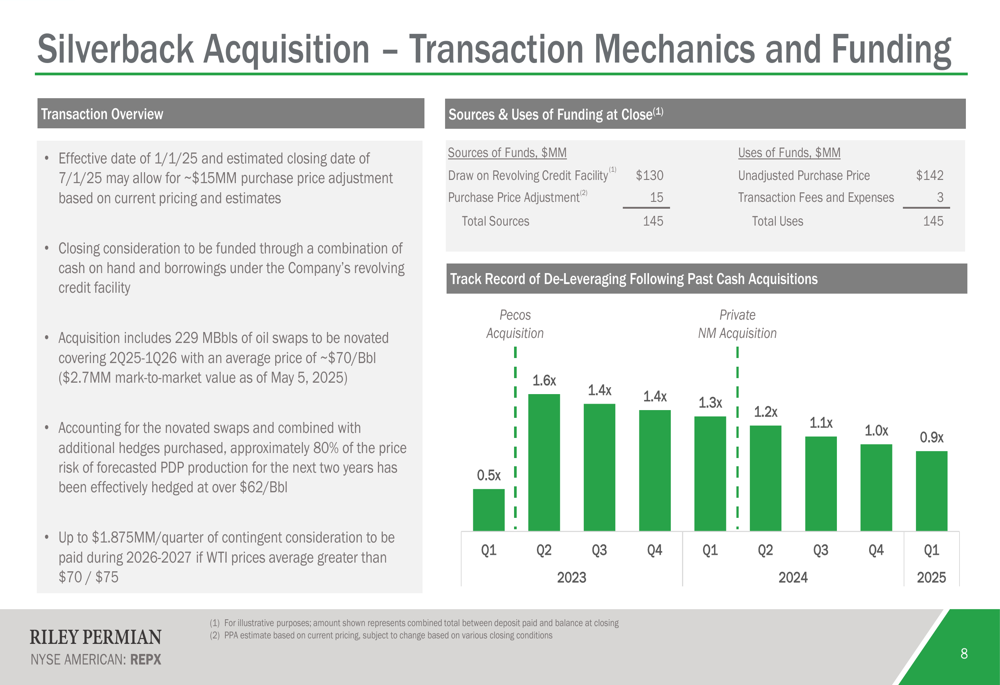

Silverback Acquisition Details

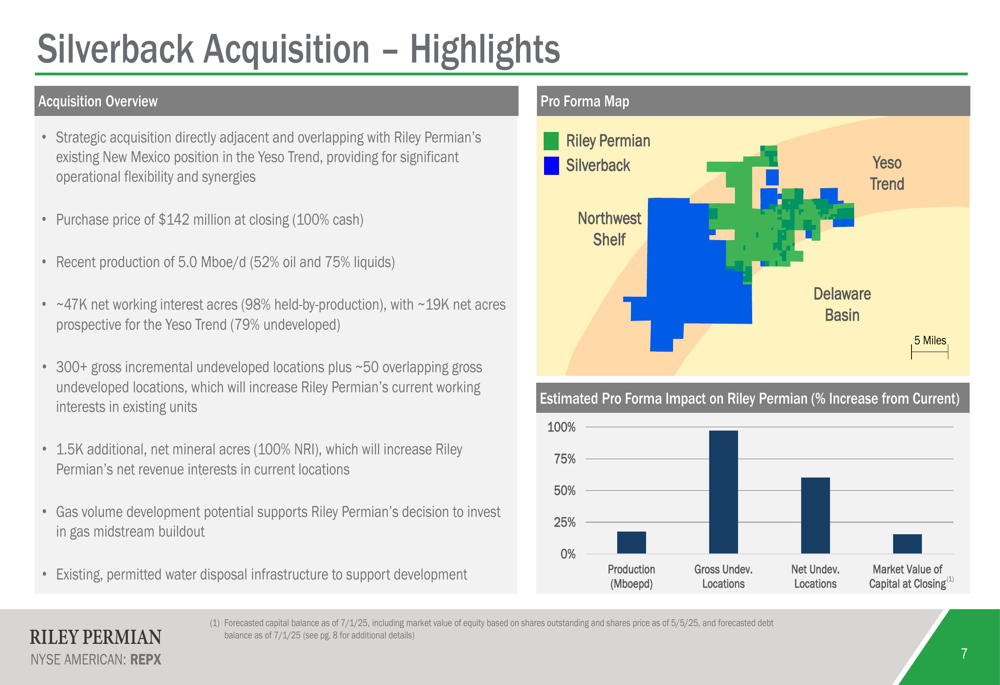

Riley Permian’s most significant growth initiative is its pending acquisition of Silverback, announced with a $142 million purchase price at closing. The acquisition, expected to close on July 1, 2025, will add approximately 5.0 Mboe/d of production (52% oil, 75% liquids) and includes approximately 47,000 net working interest acres, with 19,000 net acres prospective for the Yeso Trend.

The strategic rationale and impact of this acquisition are illustrated in the following slide:

The transaction will significantly expand Riley’s inventory, increasing gross undeveloped locations by approximately 75% and net undeveloped locations by 60%. The company plans to fund the acquisition through cash on hand and revolver borrowings, with a track record of quickly de-leveraging following past acquisitions.

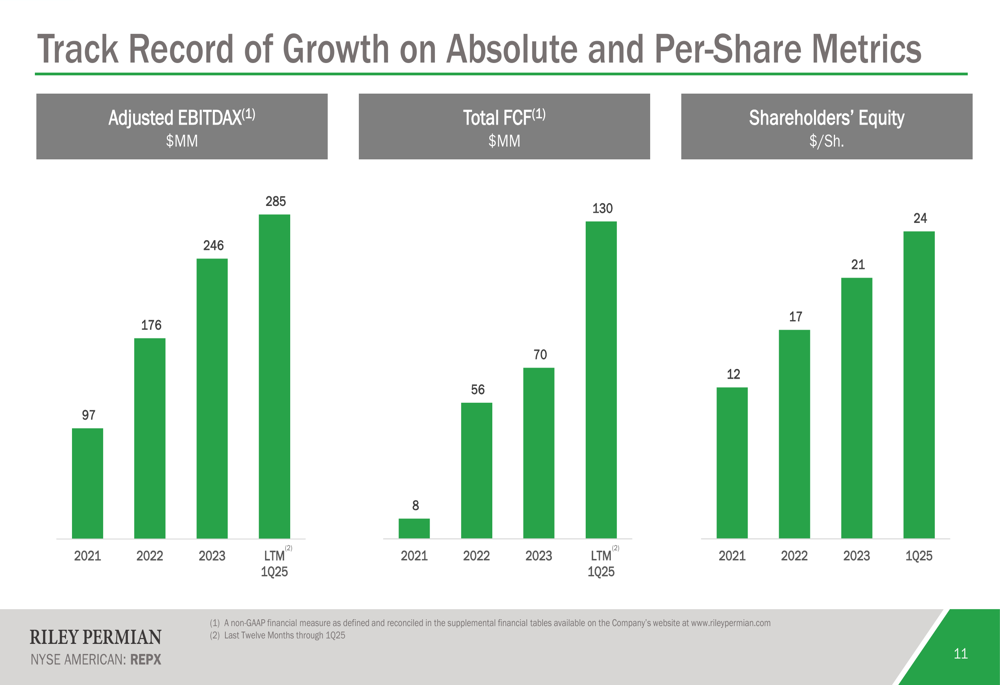

Financial Growth & Capital Allocation

Riley Permian has demonstrated consistent growth in key financial metrics over recent years. Adjusted EBITDAX increased from $97 million in 2021 to $285 million for the last twelve months ending Q1 2025. Total (EPA:TTEF) free cash flow saw even more dramatic growth, rising from $8 million in 2021 to $130 million in the same period. Shareholders’ equity per share doubled from $12 in 2021 to $24 in Q1 2025.

This growth trajectory is illustrated in the following chart:

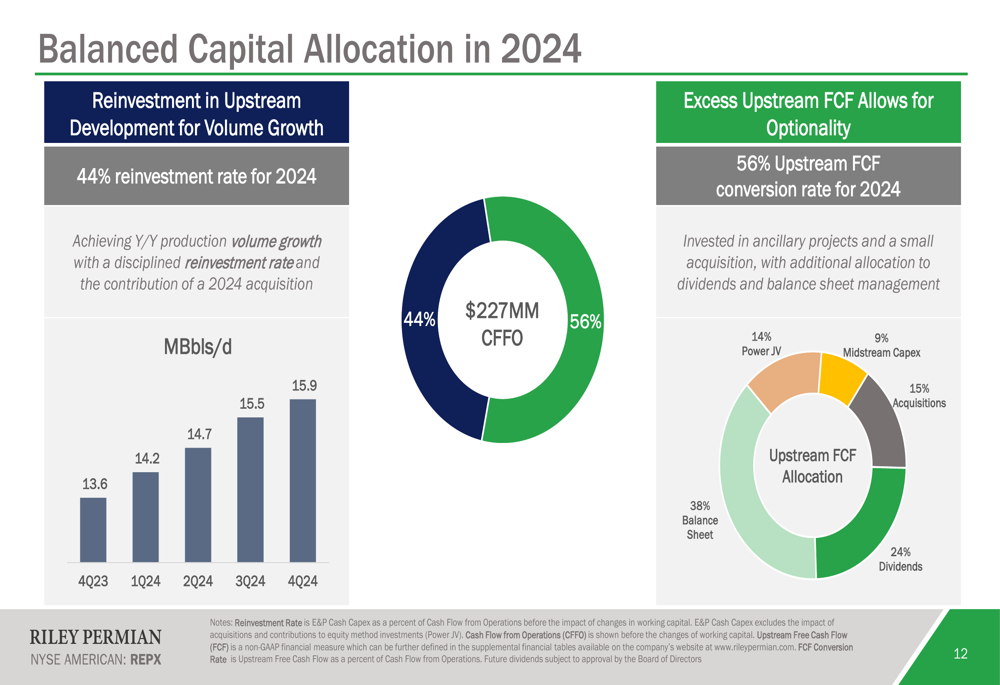

The company has maintained a balanced approach to capital allocation. In 2024, Riley reinvested 44% of its cash flow into upstream development while allocating the remainder to its balance sheet (38%), power joint venture (14%), midstream capex (9%), acquisitions (15%), and dividends (24%).

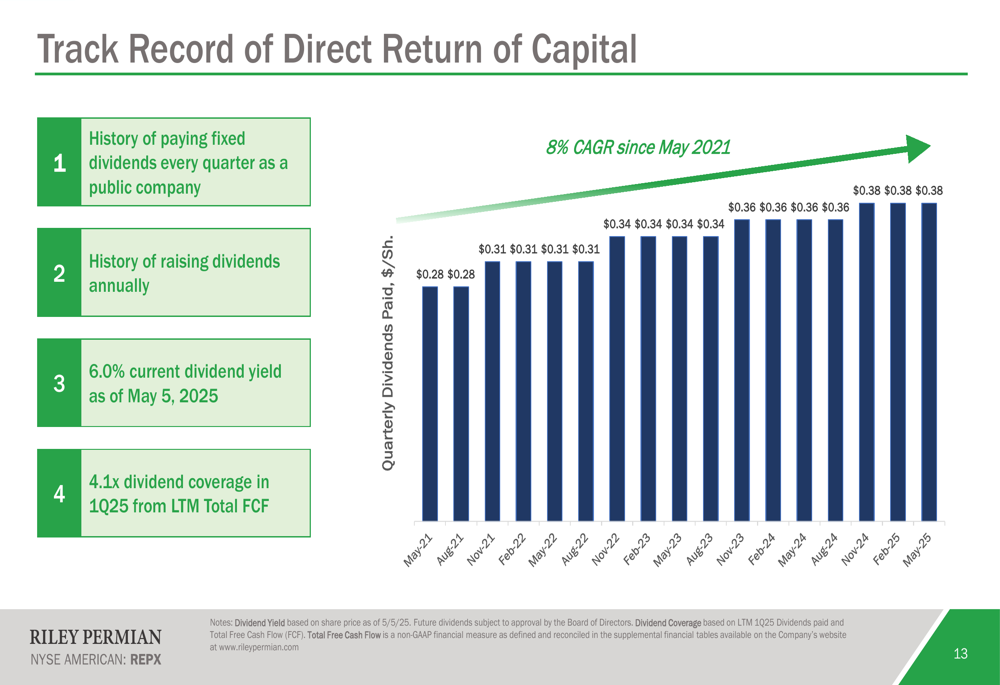

Shareholders have benefited from Riley’s strong cash flow through consistent dividend growth. The company has increased its dividend at an 8% CAGR since May 2021, from $0.28 per share to the current $0.38 per share, representing a 6.0% yield as of May 5, 2025.

Competitive Positioning & Asset Quality

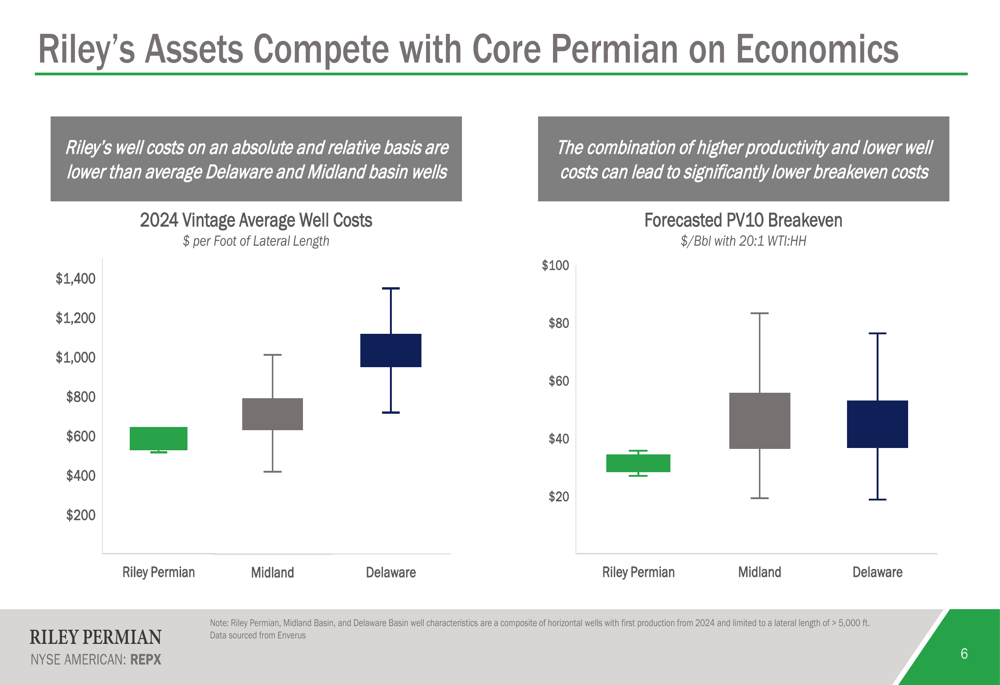

Riley Permian emphasized the quality of its assets compared to those in the core Permian Basin. According to the company’s analysis, its wells demonstrate lower relative declines and higher production than Delaware and Midland Basin wells based on 2019-2024 well characteristics.

The economic advantages are equally compelling, with Riley’s 2024 vintage average well costs lower than those in the Midland and Delaware basins. More importantly, the forecasted PV10 breakeven price for Riley’s wells is under $40 per barrel, compared to over $50 per barrel in the Midland Basin and closer to $60 per barrel in the Delaware Basin.

Forward Guidance & Outlook

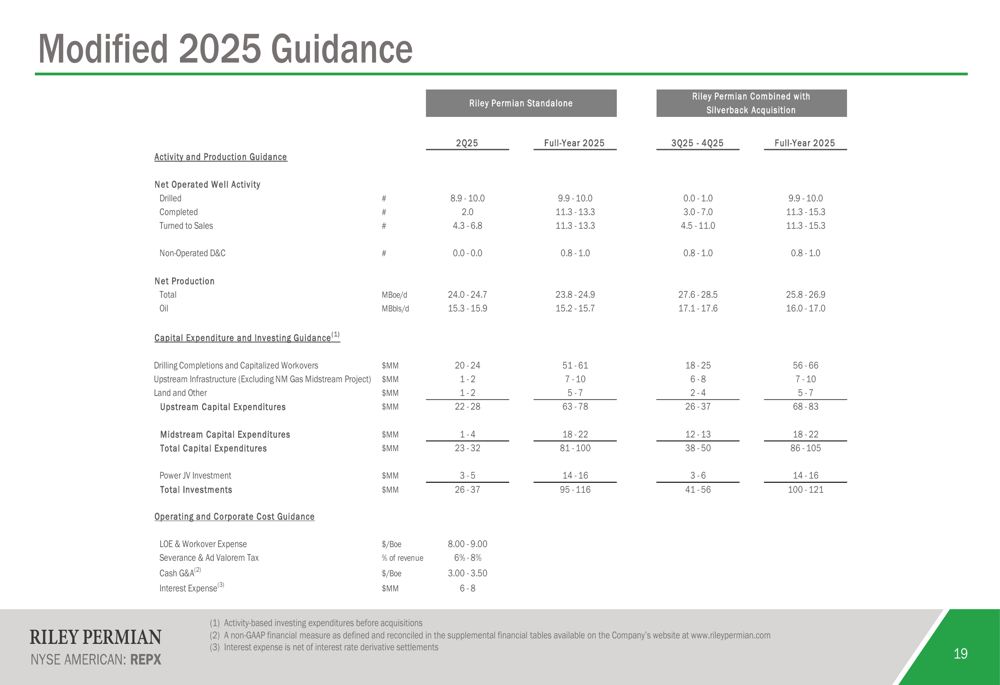

Looking ahead, Riley Permian has modified its 2025 guidance to account for the Silverback acquisition. The combined entity is expected to achieve higher production levels and increased capital expenditures, as detailed in the following guidance table:

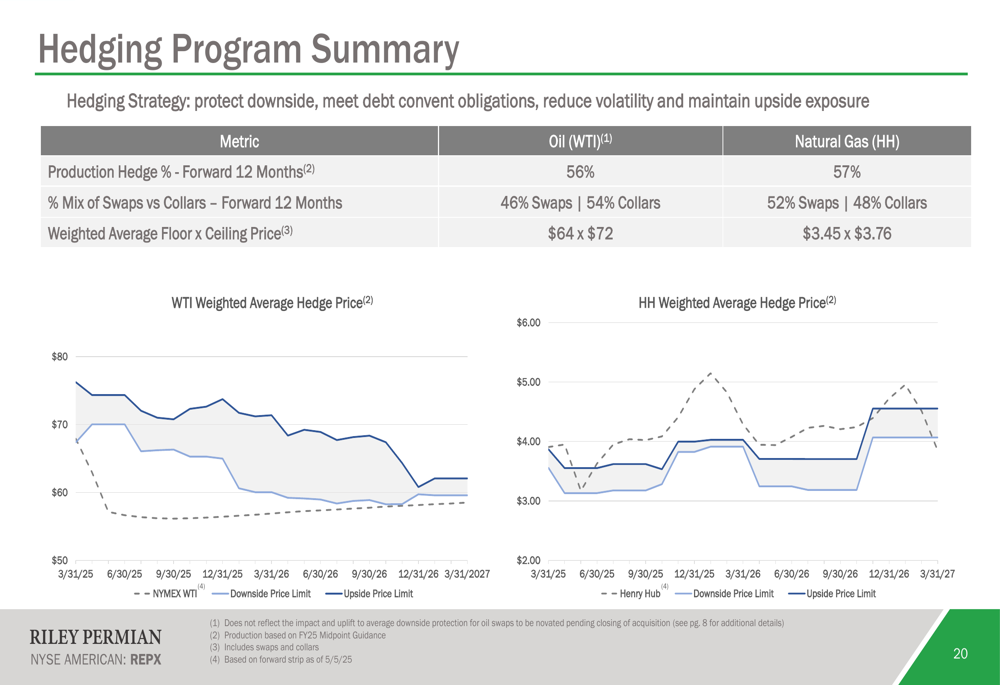

The company has also implemented a robust hedging program to protect against downside price risk while maintaining upside exposure. Currently, 56% of oil production and 57% of natural gas production are hedged for the forward 12 months, with a weighted average floor price of $64 for oil and $3.45 for natural gas.

Conclusion

Riley Permian’s Q1 2025 presentation portrays a company in transition, evolving from a pure-play upstream operator to a more diversified energy business. With strong free cash flow generation, a disciplined capital allocation strategy, and the transformative Silverback acquisition on the horizon, the company appears positioned for continued growth despite recent earnings disappointments.

The stock’s current trading level, which has pulled back from the post-Q4 earnings price of $29.30 to $24.88, may reflect investor caution following the earnings miss. However, the company’s 6% dividend yield, low leverage ratio, and strategic diversification initiatives could provide support for the shares as these growth projects materialize in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.