Fed’s Powell opens door to potential rate cuts at Jackson Hole

Pest control leader maintains growth momentum across all service lines while investing for future expansion

Introduction & Market Context

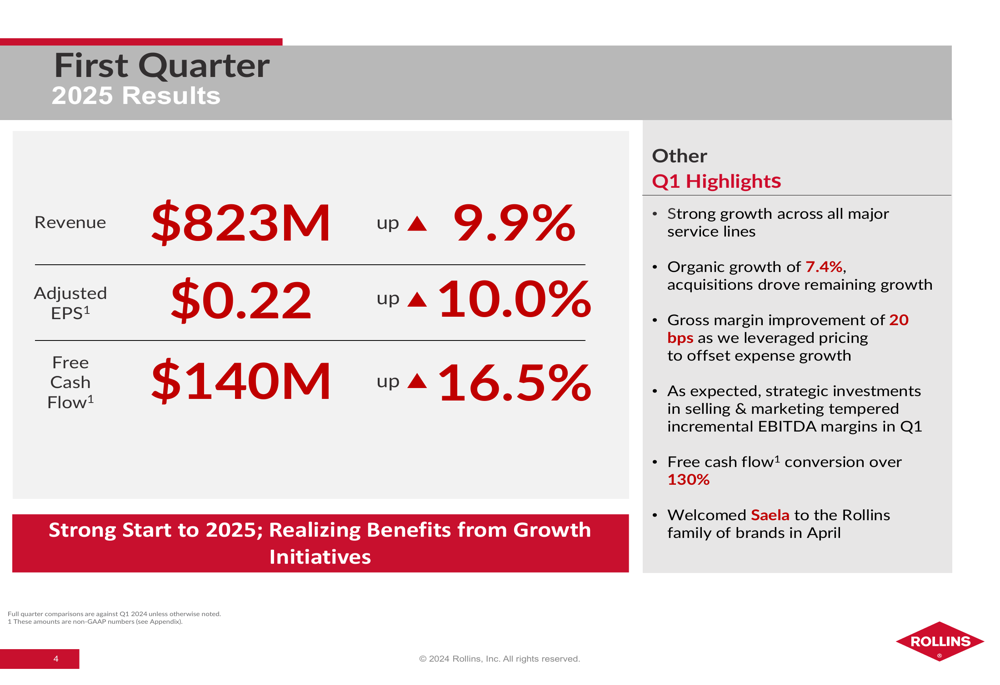

Rollins Inc . (NYSE:ROL) presented its first quarter 2025 earnings results on April 24, 2025, showcasing continued growth across all major service lines despite a challenging economic environment. The pest control giant reported revenue of $823 million, representing a 9.9% increase compared to the same period last year, while adjusted earnings per share rose 10% to $0.22.

The company’s stock closed at $54.93 on April 23, down 1.31% ahead of the earnings presentation, but still trading near its 52-week high of $56.26, reflecting investor confidence in the company’s recession-resilient business model and consistent performance.

Quarterly Performance Highlights

Rollins delivered strong results across key financial metrics in the first quarter of 2025, demonstrating the company’s ability to drive both organic growth and strategic acquisitions.

"We achieved strong growth across all major service lines, with organic growth of 7.4% complemented by acquisition-driven expansion," the company highlighted in its presentation. Free cash flow reached $140 million, a 16.5% increase compared to Q1 2024, with free cash flow conversion exceeding 130%.

As shown in the following summary of first quarter results:

The company’s performance builds on momentum from the previous quarter, where Rollins reported a 10.4% year-over-year revenue increase for Q4 2024. The consistent growth trajectory underscores the company’s strong positioning in the pest control market and its ability to execute on strategic initiatives.

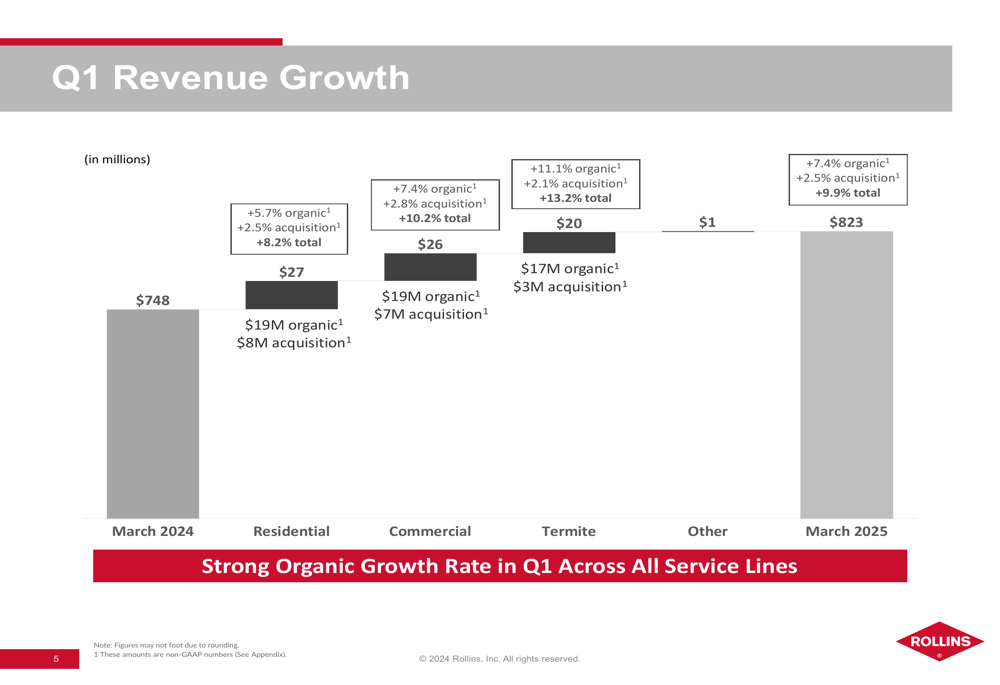

Revenue Growth by Service Line

Rollins’ revenue growth was broad-based across all major service lines, with particularly strong performance in the termite segment. The company’s diversified service portfolio continues to provide multiple growth avenues while reducing reliance on any single market segment.

The following chart breaks down revenue growth by service line, highlighting both organic and acquisition-driven components:

Residential services, which represent a significant portion of Rollins’ business, grew by 8.2%, with 5.7% coming from organic growth and 2.5% from acquisitions. Commercial services showed even stronger performance with 10.2% total growth (7.4% organic, 2.8% acquisition). The termite segment demonstrated the highest growth rate at 13.2%, with an impressive 11.1% organic growth component.

This balanced growth across service lines indicates healthy demand in both consumer and business markets, reinforcing the company’s recession-resistant business model that features over 75% recurring revenue.

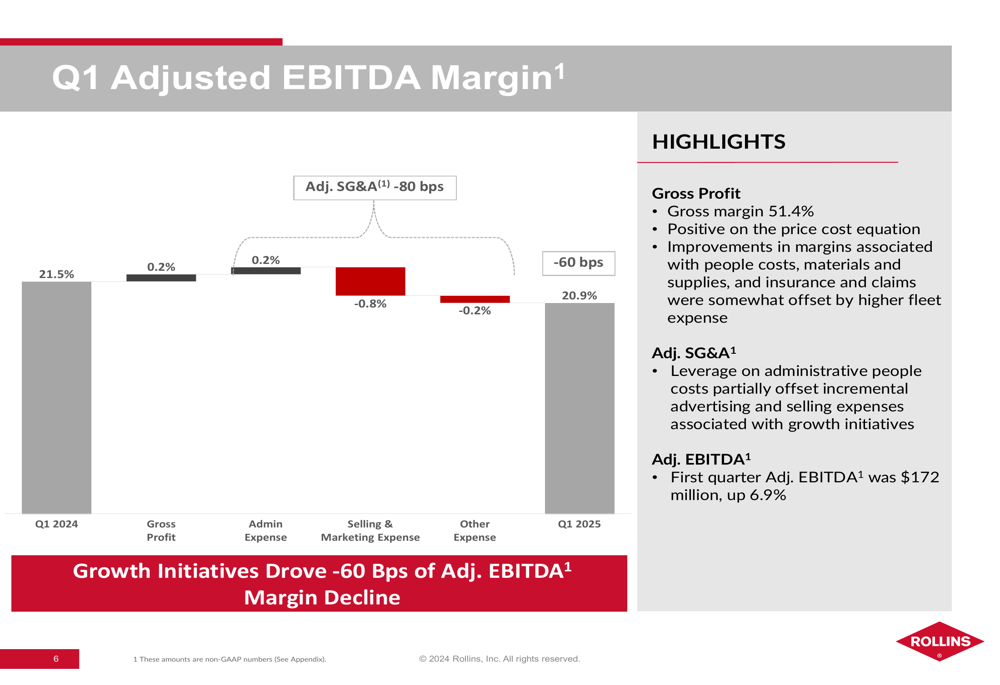

Margin Analysis and Strategic Investments

While Rollins delivered strong top-line growth, the company’s adjusted EBITDA margin decreased slightly from 21.5% in Q1 2024 to 20.9% in Q1 2025. This 60 basis point decline was attributed to strategic investments in selling and marketing initiatives designed to drive future growth.

The following chart illustrates the key factors affecting EBITDA margin performance:

Despite the slight margin compression, Rollins’ first quarter adjusted EBITDA reached $172 million, representing a 6.9% increase year-over-year. The company maintained a healthy gross profit margin of 51.4%, showing a 20 basis point improvement compared to the same period last year.

This strategic approach aligns with management’s comments from the Q4 2024 earnings call, where CEO Jerry Galoff expressed satisfaction with the company’s positioning and future prospects. The temporary margin impact reflects Rollins’ focus on long-term sustainable growth rather than short-term margin optimization.

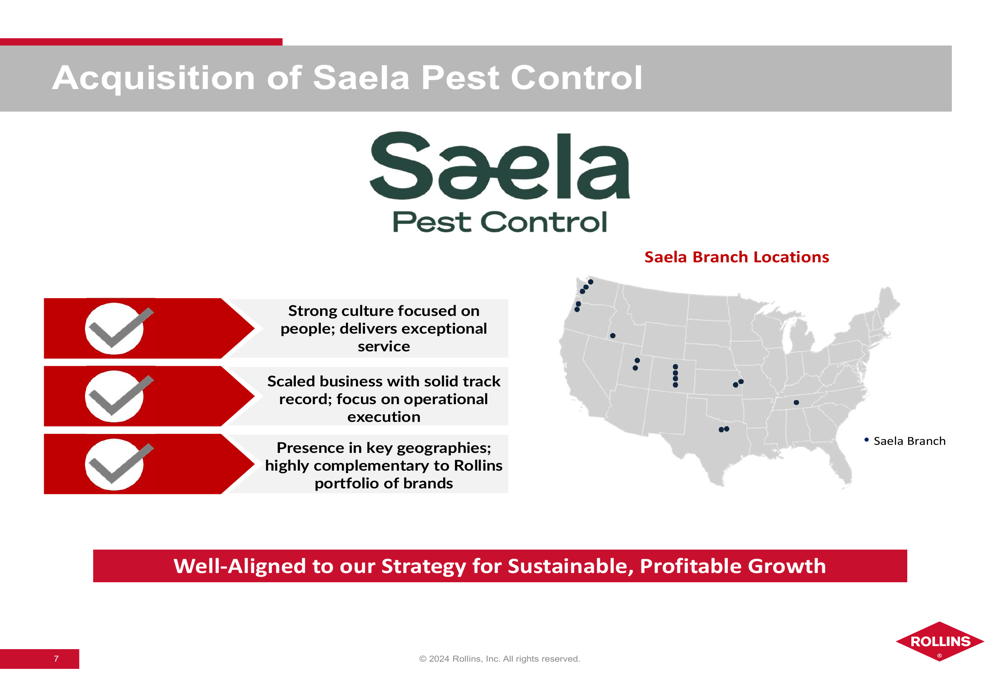

Acquisition Strategy and Capital Allocation

Rollins continues to execute its dual-growth strategy combining organic expansion with strategic acquisitions. In April 2025, the company welcomed Saela Pest Control to its family of brands, highlighting the acquisition’s strong cultural alignment and presence in key geographic markets.

The following slide details the strategic rationale behind the Saela acquisition:

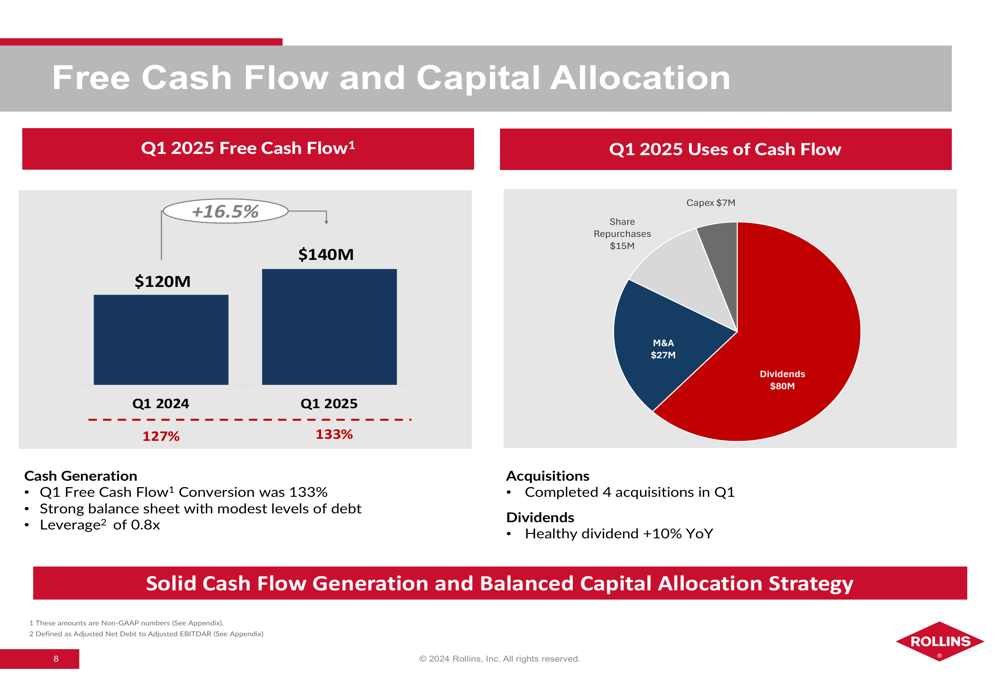

During the first quarter, Rollins completed four acquisitions, demonstrating the company’s active M&A pipeline. The company’s strong cash flow generation provides flexibility to pursue acquisition opportunities while maintaining a balanced capital allocation approach.

The following chart illustrates how Rollins deployed its cash flow during Q1 2025:

Of the $140 million in free cash flow generated during the quarter, Rollins allocated $80 million to dividends, $27 million to M&A activities, $15 million to share repurchases, and $7 million to capital expenditures. This balanced approach reflects management’s commitment to shareholder returns while investing in future growth.

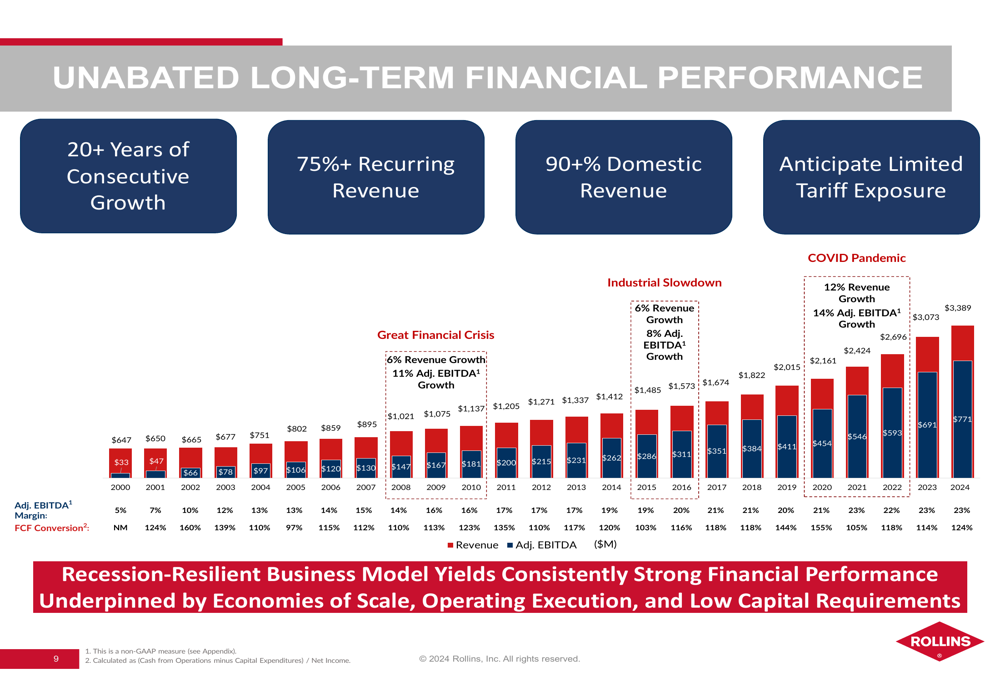

The company’s long-term financial performance demonstrates the effectiveness of this strategy, with over two decades of consecutive growth:

Forward-Looking Guidance

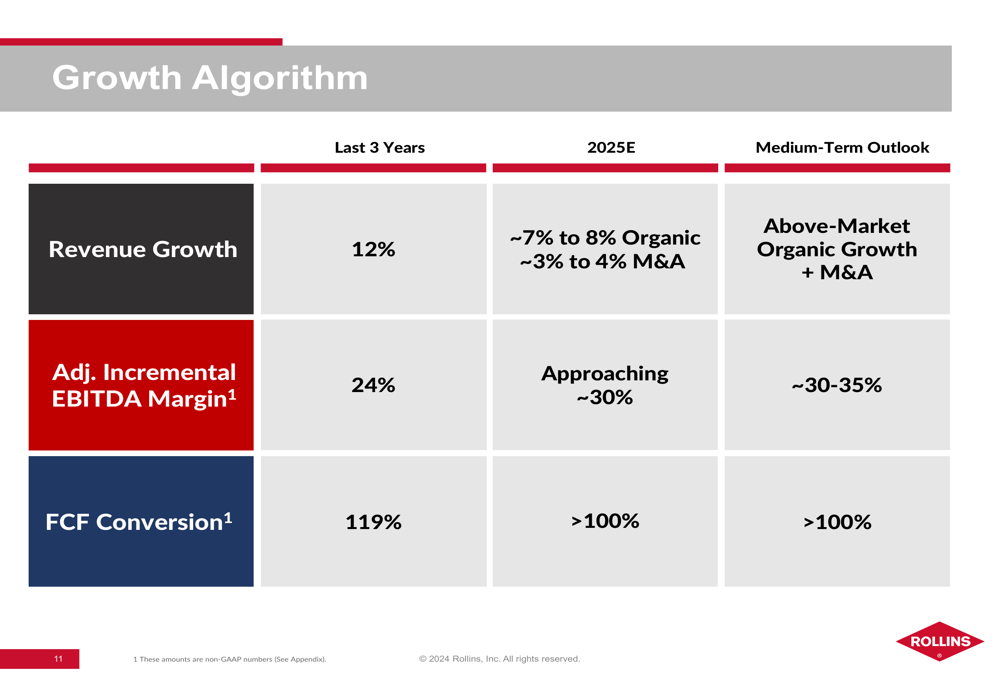

Looking ahead, Rollins provided a detailed growth algorithm for 2025 and beyond, maintaining its previous guidance of 7-8% organic growth supplemented by 3-4% growth from M&A activities. The company expects adjusted incremental EBITDA margins to approach 30% in 2025, with medium-term targets of 30-35%.

The following slide outlines the company’s growth expectations:

Rollins anticipates free cash flow conversion to remain above 100%, providing continued flexibility for strategic investments and shareholder returns. The company’s medium-term outlook projects above-market organic growth complemented by M&A activity, suggesting confidence in its ability to maintain momentum despite potential macroeconomic challenges.

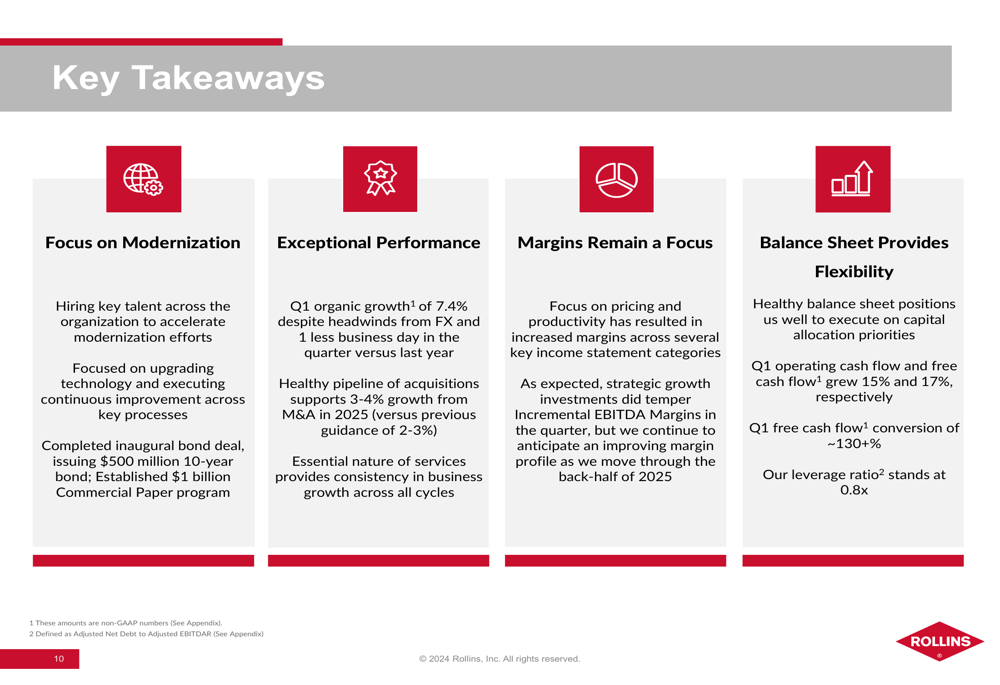

Key Takeaways

Rollins’ Q1 2025 presentation emphasized four strategic priorities that will guide the company’s future direction:

The company’s focus on modernization, exceptional performance, margin improvement, and balance sheet flexibility positions it well for continued success in the pest control industry. With a recession-resilient business model, strong recurring revenue base, and proven ability to execute both organic and acquisition-driven growth strategies, Rollins appears well-positioned to deliver on its medium-term financial targets.

As the company continues to integrate recent acquisitions and invest in growth initiatives, investors will be watching closely to see if these strategic investments translate into accelerated growth and margin expansion in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.