Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Roper Technologies Inc (NYSE:NASDAQ:ROP) presented its Q1 2025 financial results on April 28, 2025, highlighting strong performance across its business segments and announcing a significant acquisition. The diversified technology company, which focuses on software and technology-enabled products, reported solid growth metrics despite facing a slight decline in premarket trading, with shares down 0.48% to $555.00 before the presentation.

The company’s Q1 results build upon its strong performance in Q4 2024, when it exceeded analyst expectations with revenue of $1.88 billion and earnings per share of $4.81. The latest quarterly presentation reveals continued momentum in Roper’s business model, which emphasizes market-leading positions in defensible niches, a decentralized operating environment, and process-driven capital deployment.

Quarterly Performance Highlights

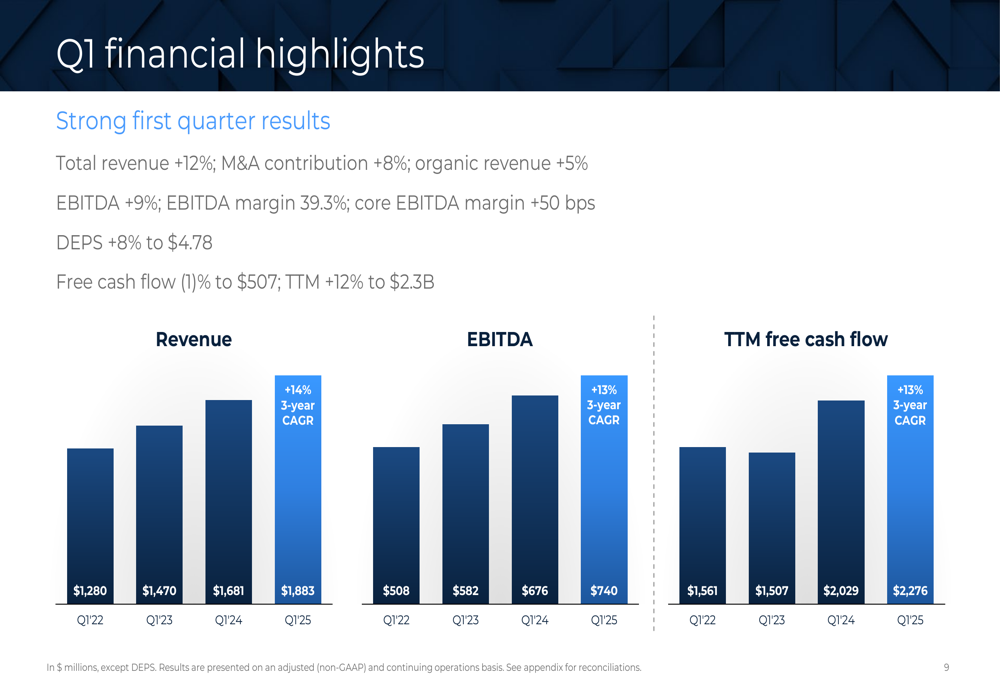

Roper reported impressive financial results for Q1 2025, with total revenue increasing 12% compared to the same period last year. This growth included an 8% contribution from mergers and acquisitions and 5% organic growth, demonstrating both successful integration of acquired businesses and internal expansion.

As shown in the following financial highlights chart, the company achieved significant improvements across key metrics:

Diluted earnings per share (DEPS) grew 8% to $4.78, while EBITDA increased 9% with a margin of 39.3%. The company’s free cash flow, a critical metric for Roper’s acquisition-focused strategy, grew 12% to $507 million for the quarter. On a trailing twelve-month basis, free cash flow reached $2.3 billion with a robust 31% margin.

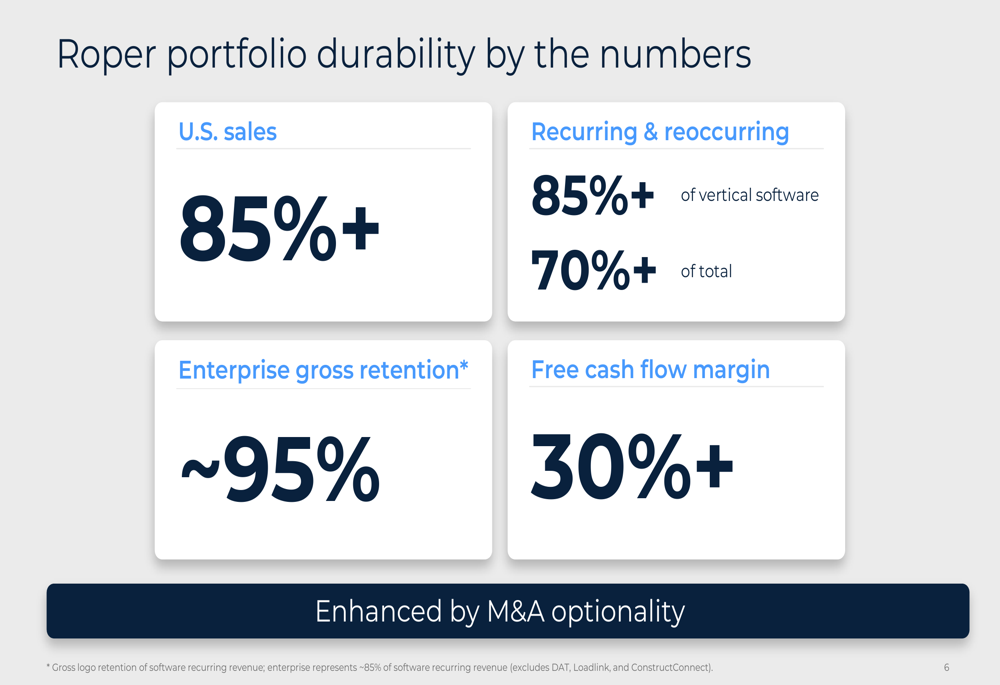

The company’s portfolio continues to demonstrate strong durability, supported by several key characteristics:

With over 85% of sales coming from the U.S. market, approximately 95% enterprise gross retention, and more than 85% recurring and reoccurring revenue in its vertical software businesses, Roper has built a stable foundation for consistent performance. This high level of recurring revenue provides visibility into future results and reduces vulnerability to economic fluctuations.

CentralReach Acquisition Analysis

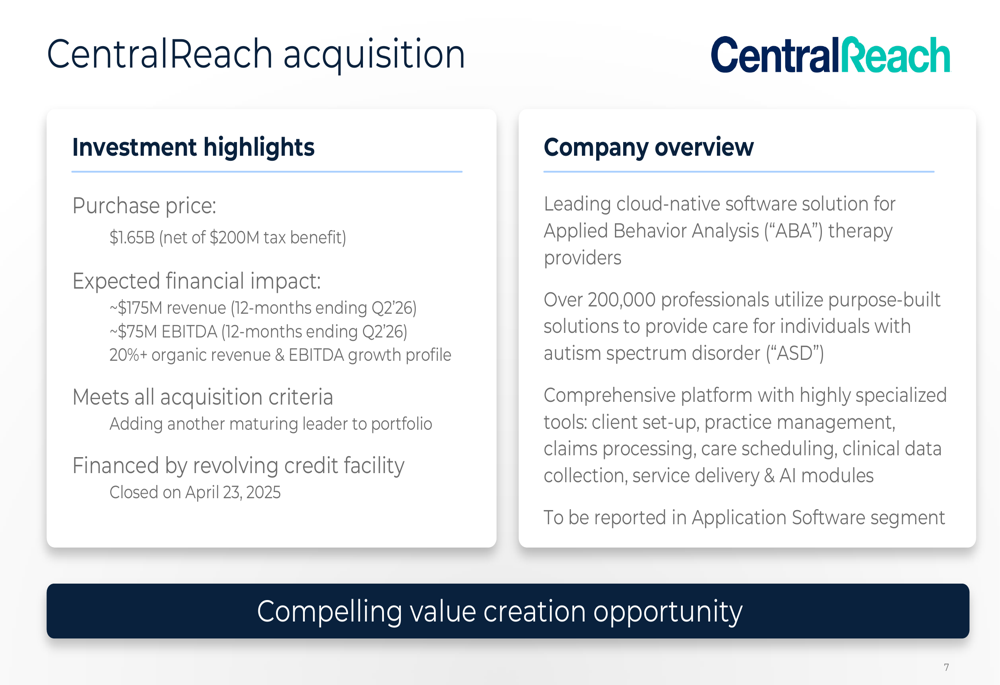

A major highlight of the presentation was Roper’s announcement of its acquisition of CentralReach for $1.65 billion (net of a $200 million tax benefit). The transaction, which closed on April 23, 2025, adds a leading cloud-native software solution for Applied Behavior Analysis (ABA) therapy providers to Roper’s portfolio.

The strategic rationale and financial details of the acquisition are outlined below:

CentralReach is expected to contribute approximately $175 million in revenue and $75 million in EBITDA in the 12 months ending Q2 2026. The business has an impressive growth profile, with both revenue and EBITDA projected to increase by more than 20% organically. The acquisition was financed through Roper’s revolving credit facility and will be reported in the company’s Application Software (ETR:SOWGn) segment.

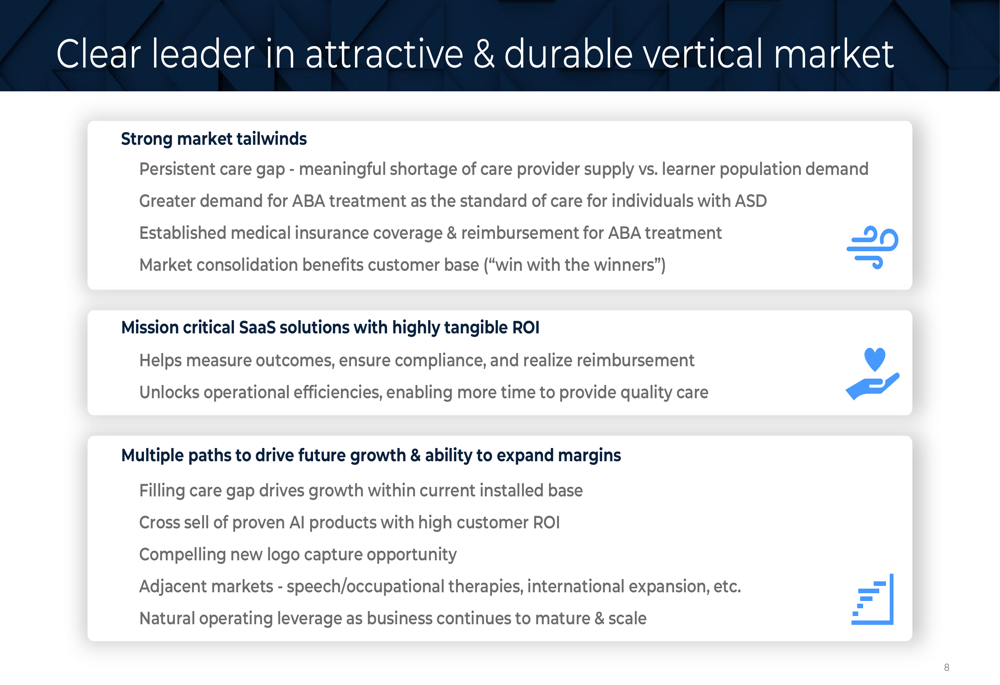

The acquisition aligns with Roper’s strategy of targeting market leaders in attractive vertical markets:

CentralReach benefits from strong market tailwinds, including persistent care gaps, increasing demand for ABA treatment, established medical insurance coverage, and market consolidation. Its mission-critical SaaS solutions help providers measure outcomes, ensure compliance, and improve operational efficiency. Multiple growth paths exist, including filling care gaps, cross-selling AI products, new customer acquisition, expansion into adjacent markets, and natural operating leverage.

Segment Performance

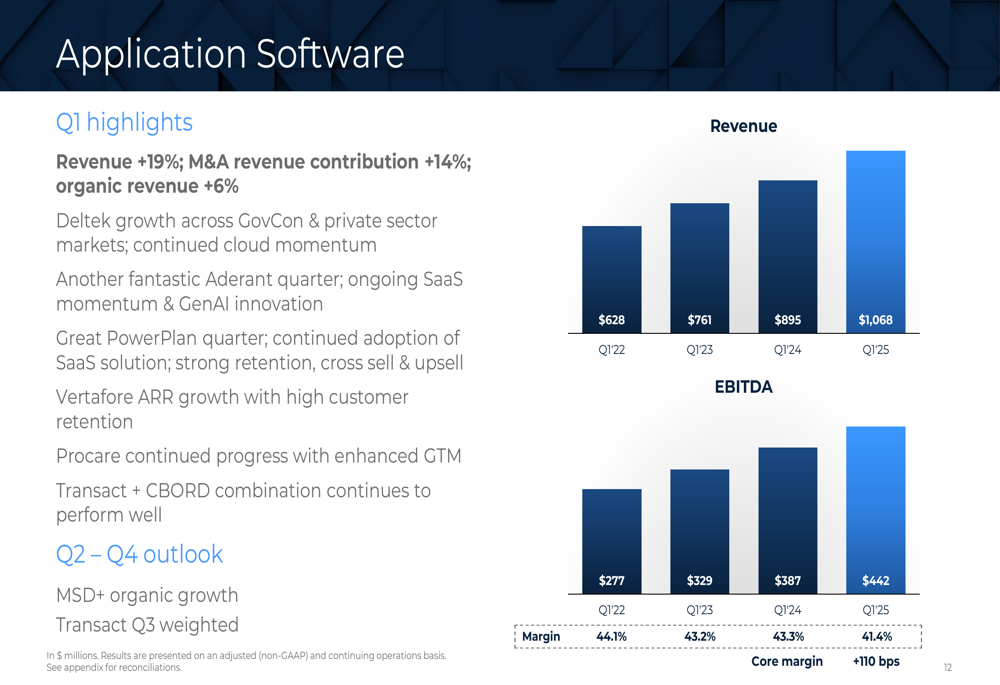

Roper’s three business segments showed varying performance in Q1 2025, with Application Software leading the growth:

The Application Software segment, which will now include CentralReach, delivered exceptional results with 19% revenue growth, including 14% from M&A and 6% organic growth:

Key drivers included Deltek’s growth across all market verticals, Aderant’s strong performance in large law firms, PowerPlan’s increased adoption, and Vertafore’s ARR growth. The segment achieved an EBITDA margin of 41.4%, with core margin expanding 110 basis points.

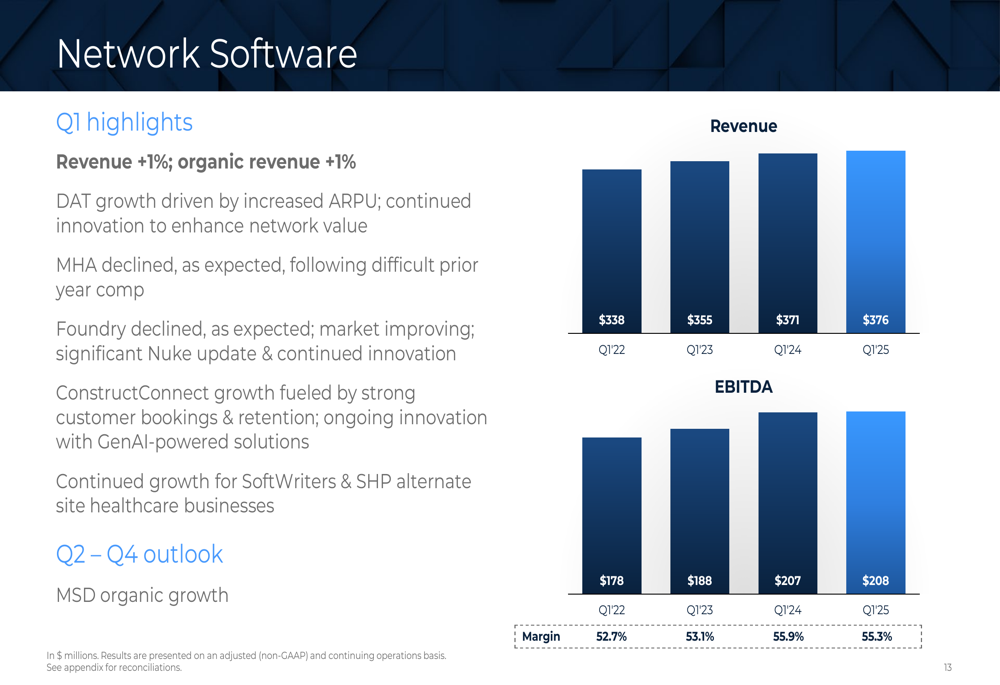

The Network Software segment showed more modest growth:

Revenue increased 1% organically, with DAT’s growth driven by increased average revenue per user (ARPU) and continued innovation. MHA experienced an expected decline following a difficult prior year comparison, while Foundry saw market improvement. The segment maintained a strong EBITDA margin of 55.3%.

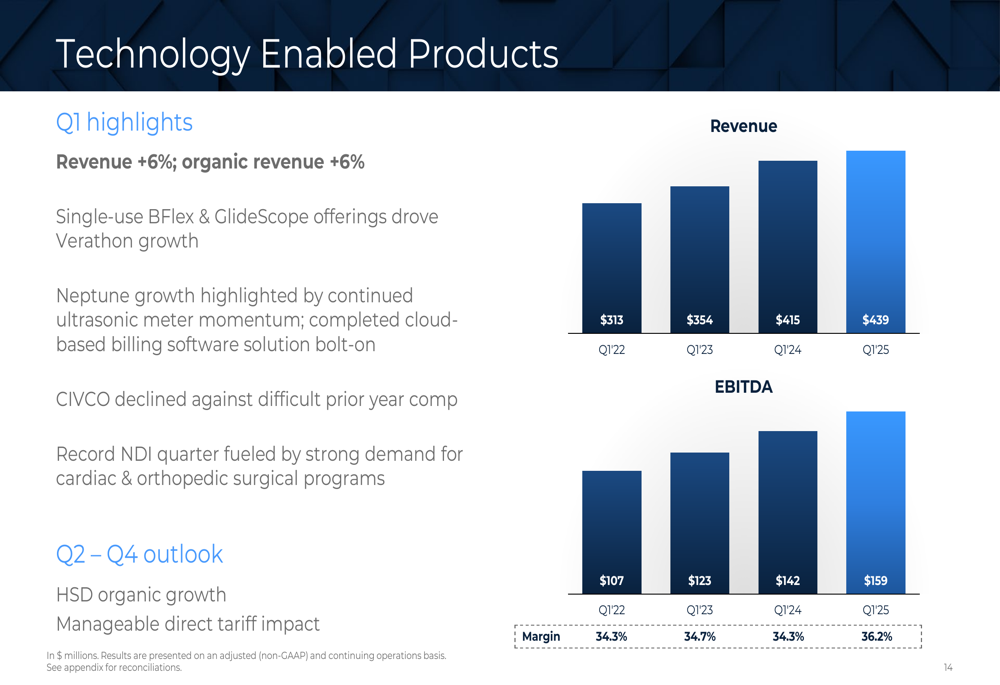

The Technology Enabled Products segment delivered solid performance:

Revenue grew 6% organically, driven by Verathon’s single-use BFlex and GlideScope offerings, Neptune’s ultrasonic meter momentum, and NDI’s record quarter in cardiac and orthopedic surgical programs. The segment achieved an EBITDA margin of 36.2%.

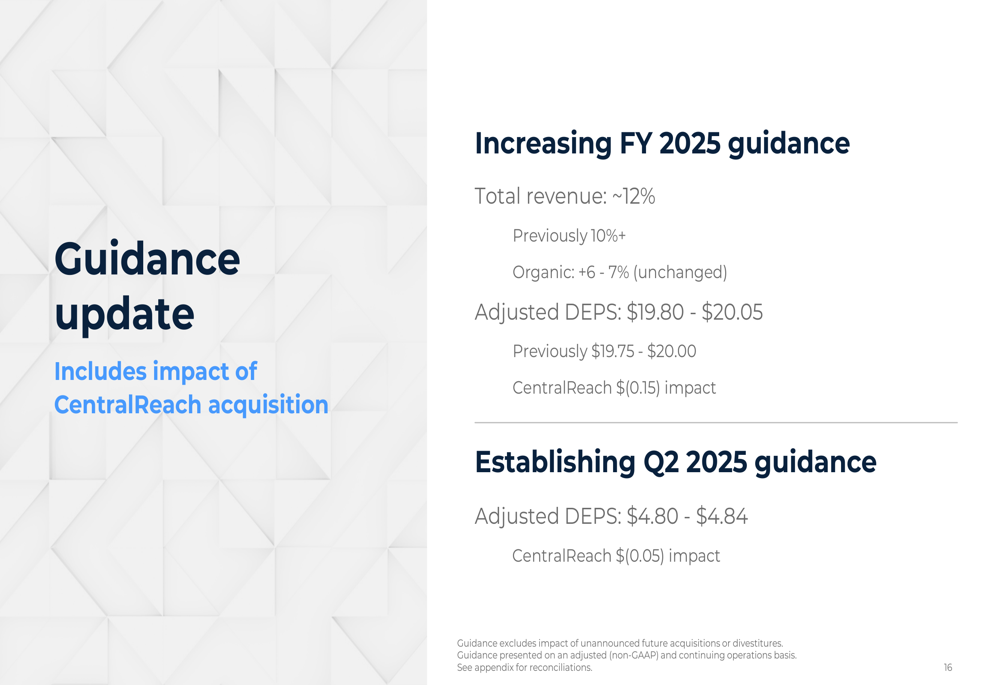

Updated Guidance & Outlook

Based on strong Q1 performance and the CentralReach acquisition, Roper has increased its full-year 2025 guidance:

Total (EPA:TTEF) revenue is now expected to grow approximately 12%, up from the previous guidance of 10%+, while organic growth projection remains at 6-7%. Adjusted diluted earnings per share (DEPS) guidance has been raised to $19.80-$20.05, compared to the previous range of $19.75-$20.00, despite a $0.15 negative impact from the CentralReach acquisition.

For Q2 2025, Roper expects adjusted DEPS of $4.80-$4.84, which includes a $0.05 negative impact from CentralReach. The guidance excludes any unannounced future acquisitions or divestitures.

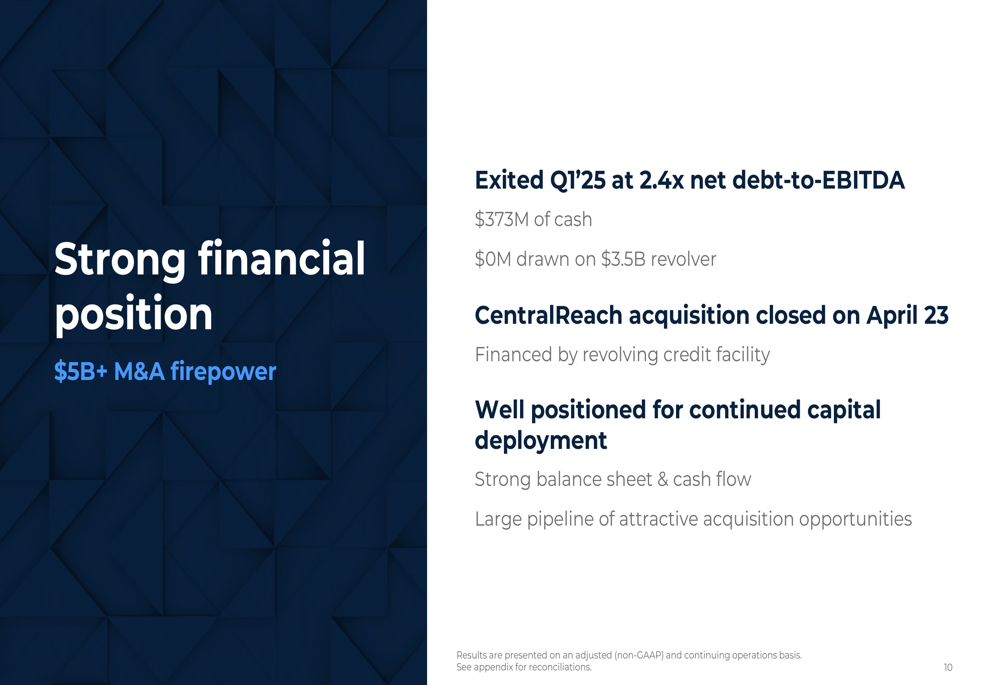

Financial Position & Capital Deployment Strategy

Roper maintains a strong financial position, positioning it well for continued capital deployment:

The company exited Q1 2025 with a net debt-to-EBITDA ratio of 2.4x, $373 million in cash, and no draws on its $3.5 billion revolving credit facility. Even after financing the CentralReach acquisition through its revolving facility, Roper remains well-positioned for additional acquisitions.

Management emphasized that the company has a strong balance sheet and cash flow generation capability, along with a large pipeline of attractive acquisition opportunities. This financial flexibility supports Roper’s long-term strategy of compounding cash flow through strategic acquisitions of high-quality, asset-light businesses with strong recurring revenue streams.

Summary

Roper Technologies’ Q1 2025 presentation demonstrates the company’s continued execution of its growth strategy, combining organic expansion with strategic acquisitions. The strong performance across segments, highlighted by the Application Software business, and the strategic acquisition of CentralReach have enabled management to raise full-year guidance despite some near-term earnings dilution from the acquisition.

With its durable portfolio of high-retention, recurring revenue businesses and strong financial position, Roper appears well-positioned to continue its track record of compounding cash flow and creating shareholder value through both organic growth and strategic capital deployment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.