Fed’s Powell opens door to potential rate cuts at Jackson Hole

Royal Caribbean Cruises Ltd (NYSE:RCL) reported strong second-quarter 2025 results with significant year-over-year improvements across key metrics, according to the company’s earnings presentation. Despite the positive performance and raised full-year guidance, the stock was trading down 5.54% in premarket at $332.50.

Quarterly Performance Highlights

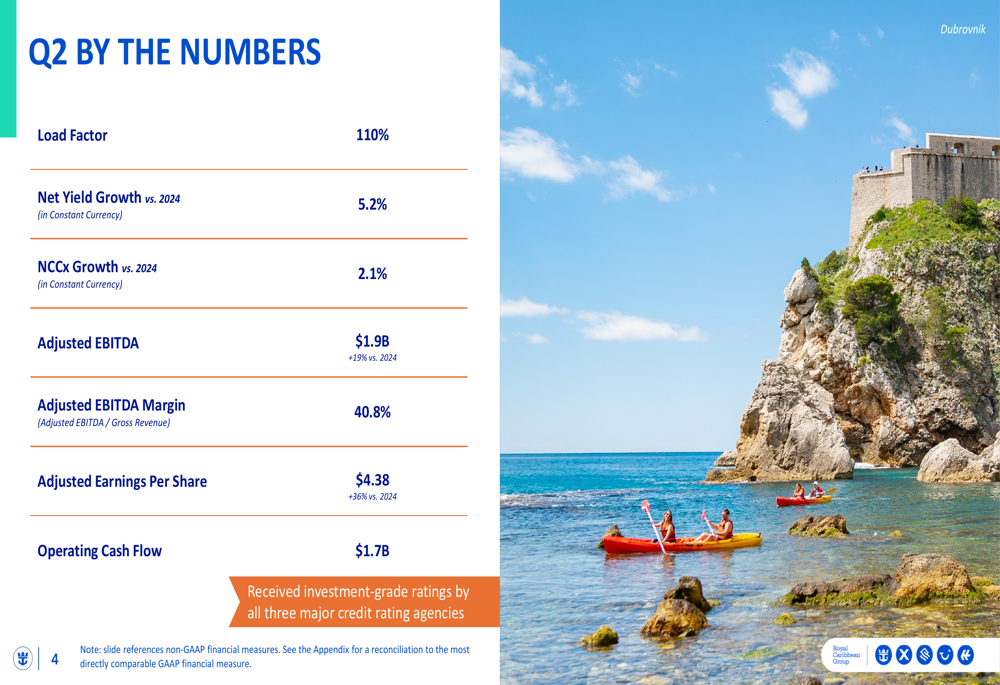

The cruise operator delivered impressive financial results for Q2 2025, achieving a 36% increase in adjusted earnings per share to $4.38 compared to the same period in 2024. The company reported a robust load factor of 110%, indicating ships operating above nominal capacity, while net yield grew 5.2% in constant currency.

Royal Caribbean’s adjusted EBITDA reached $1.9 billion, representing a 19% year-over-year increase, with an adjusted EBITDA margin of 40.8%. Operating cash flow remained strong at $1.7 billion for the quarter. The company also highlighted its achievement of investment-grade ratings from all three major credit rating agencies, reflecting its strengthened financial position.

As shown in the following comprehensive financial summary:

Forward Guidance

Royal Caribbean raised its full-year 2025 adjusted EPS guidance to $15.41-$15.55, up from its previous April guidance of $14.55-$15.55. The company attributed this increase to several factors, including Q2 business outperformance ($0.23), improved outlook for the remainder of the year ($0.20), and neutral impact from foreign exchange and fuel rates.

For the full year 2025, Royal Caribbean expects:

- Available Passenger Cruise Days (APCDs): 53.3 million

- Net Yield Growth: 3.5% to 4.0% (constant currency)

- Net Cruise Costs excluding Fuel (NCCx) Growth: Approximately 0.3%

- Fuel expenses: Approximately $1.143 billion

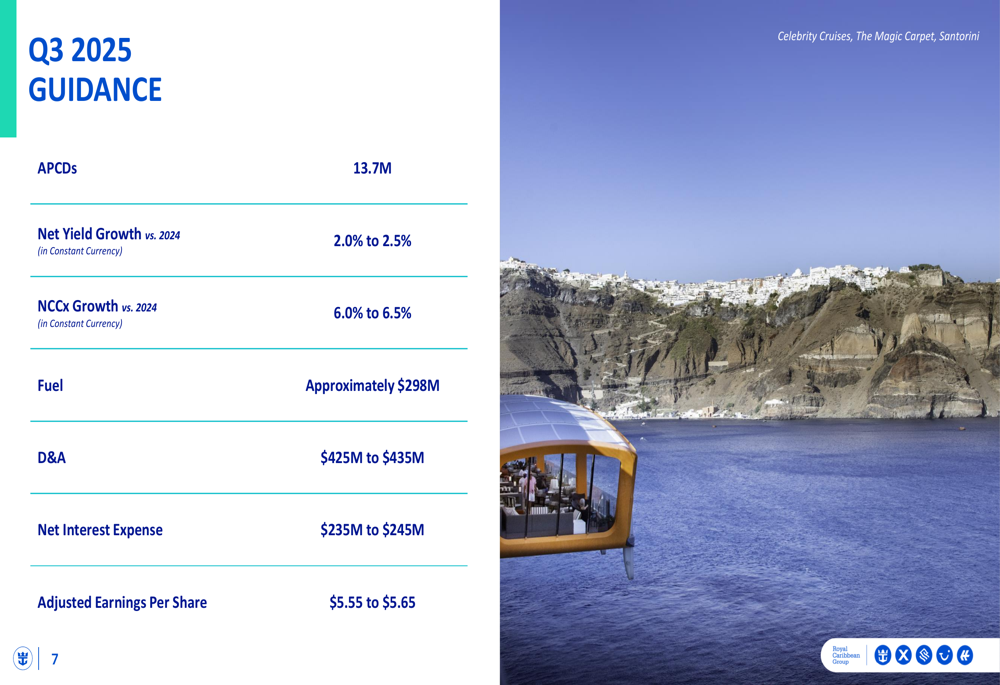

The detailed full-year guidance is presented here:

The company’s guidance revision breakdown shows the specific factors contributing to the improved outlook:

For the upcoming third quarter of 2025, Royal Caribbean projects:

- Available Passenger Cruise Days (APCDs): 13.7 million

- Net Yield Growth: 2.0% to 2.5% (constant currency)

- NCCx Growth: 6.0% to 6.5% (constant currency)

- Adjusted EPS: $5.55 to $5.65

Strategic Initiatives

Royal Caribbean unveiled its "Perfecta" program, a strategic initiative targeting 20% EPS CAGR and high teens Return on Invested Capital (ROIC) by 2027. The program focuses on delivering premium vacation experiences while maintaining solid investment-grade metrics.

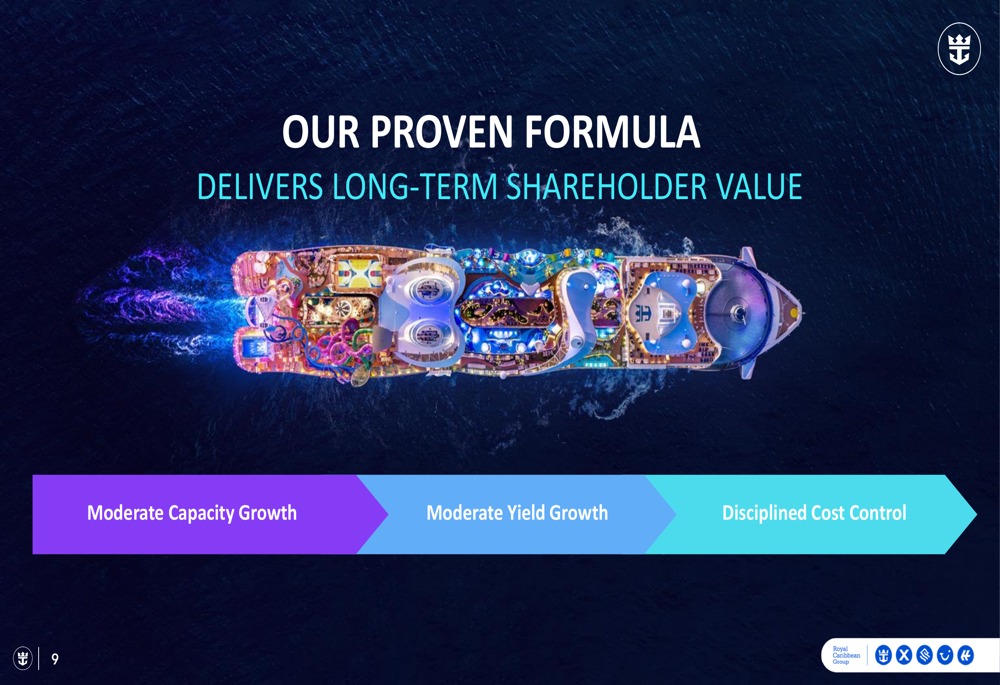

The company’s long-term value creation strategy centers on three key pillars: moderate capacity growth, moderate yield growth, and disciplined cost control. This balanced approach aims to drive sustainable profitability while managing expansion responsibly.

Royal Caribbean detailed an extensive pipeline of new ships scheduled to join its fleet through 2028, including Star of the Seas and Celebrity Xcel in 2025, followed by several additional vessels across its brands in subsequent years.

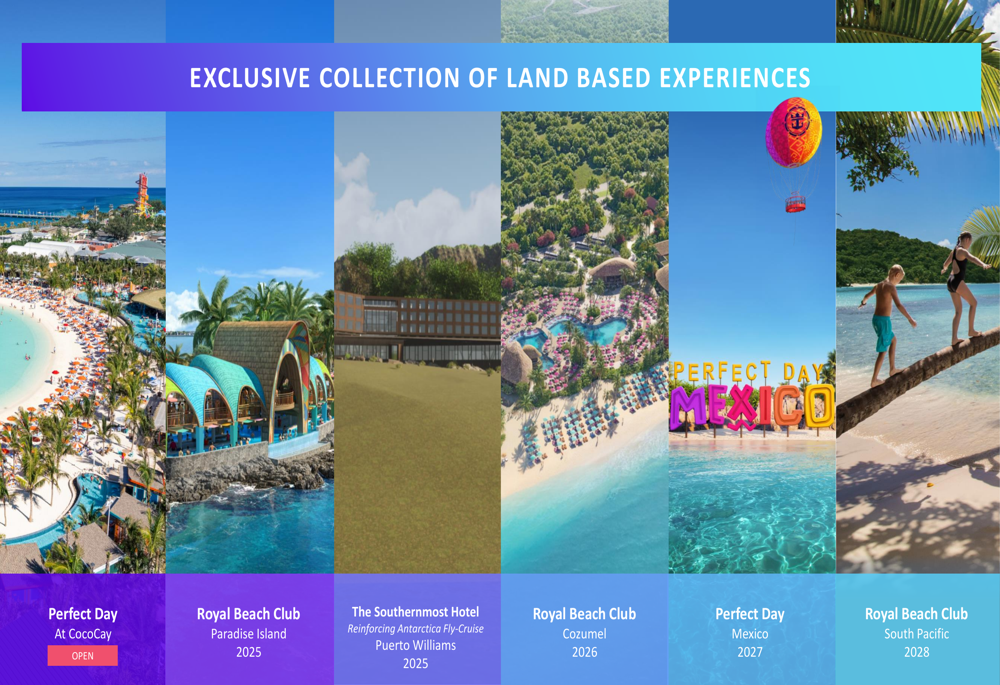

Complementing its cruise expansion, the company is developing an exclusive collection of land-based experiences, including the upcoming Royal Beach Club Paradise Island (2025), Royal Beach Club Cozumel (2026), Perfect Day Mexico (2027), and Royal Beach Club South Pacific (2028).

Market Reaction & Analysis

Despite the strong quarterly performance and raised guidance, Royal Caribbean’s stock was trading down 5.54% in premarket. This follows a similar pattern seen after Q1 2025 results, when the stock declined 2.16% despite exceeding EPS forecasts.

The market reaction may reflect concerns about the projected 6.0-6.5% increase in Net Cruise Costs excluding Fuel for Q3 2025, substantially higher than the full-year projection of approximately 0.3%. This cost acceleration could signal margin pressures in the coming quarters.

Additionally, while the company’s net yield growth remains positive at 2.0-2.5% for Q3 and 3.5-4.0% for the full year, these figures represent a deceleration from the 5.2% growth achieved in Q2. This moderation in yield growth, combined with higher costs, may be contributing to investor caution despite the overall strong performance.

Royal Caribbean’s stock has performed well over the past year, trading near its 52-week high of $355.91 prior to this earnings release, compared to a 52-week low of $130.08. The current pullback may also reflect profit-taking following this substantial appreciation, as investors reassess the company’s growth trajectory against its valuation.

While the company’s operational performance remains strong and its strategic initiatives promising, the market appears to be focusing on potential headwinds in the near term, particularly related to cost management and yield growth sustainability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.