ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Ryanair Holdings PLC (LON:RYA) released its H1 FY26 results on November 3, 2025, showcasing robust performance across key metrics. The Irish low-cost carrier’s stock rose 2.01% to close at $26.89 following the announcement, reflecting positive investor sentiment toward the company’s financial health and growth trajectory.

The airline continues to strengthen its position in the European aviation market, leveraging its cost advantage to drive profitability despite ongoing industry challenges including air traffic control disruptions and regional conflicts.

H1 FY26 Financial Performance

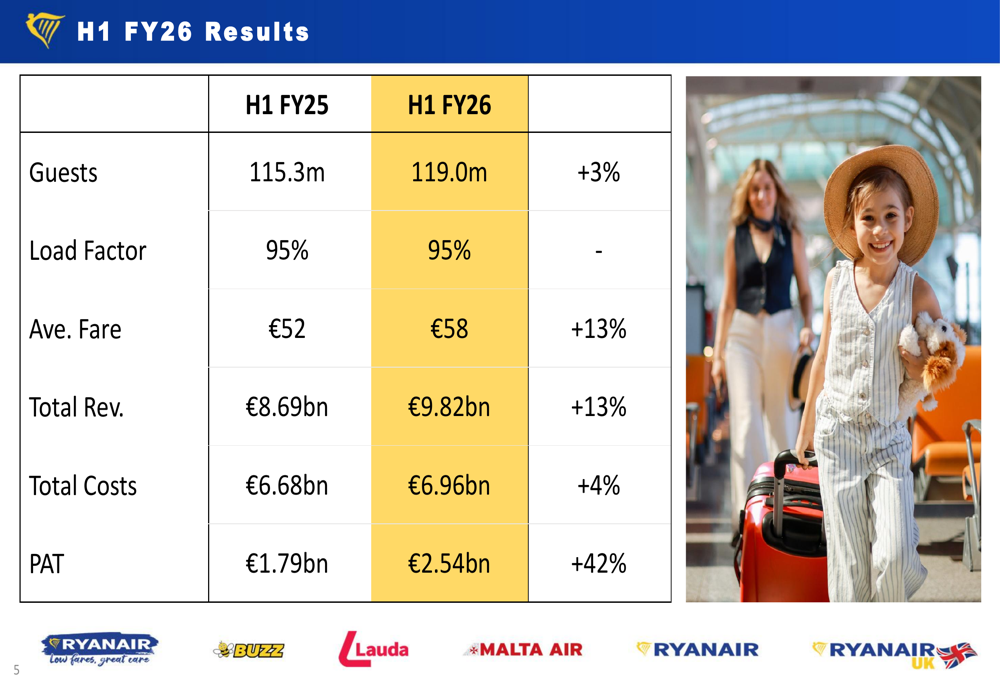

Ryanair reported exceptional financial results for the first half of fiscal year 2026, with profit after tax soaring 42% year-over-year to €2.54 billion. This performance was driven by a 13% increase in total revenue to €9.82 billion, supported by both traffic growth and higher average fares.

The airline carried 119 million passengers during the period, representing a 3% increase compared to H1 FY25, while maintaining a strong load factor of 95%. Average fares rose 13% to €58, contributing significantly to the revenue growth.

As shown in the following financial results summary:

Total costs increased by a modest 4% to €6.96 billion, significantly below the revenue growth rate, allowing for substantial margin expansion. This cost discipline remains a cornerstone of Ryanair’s business model and competitive advantage.

Fortress Balance Sheet

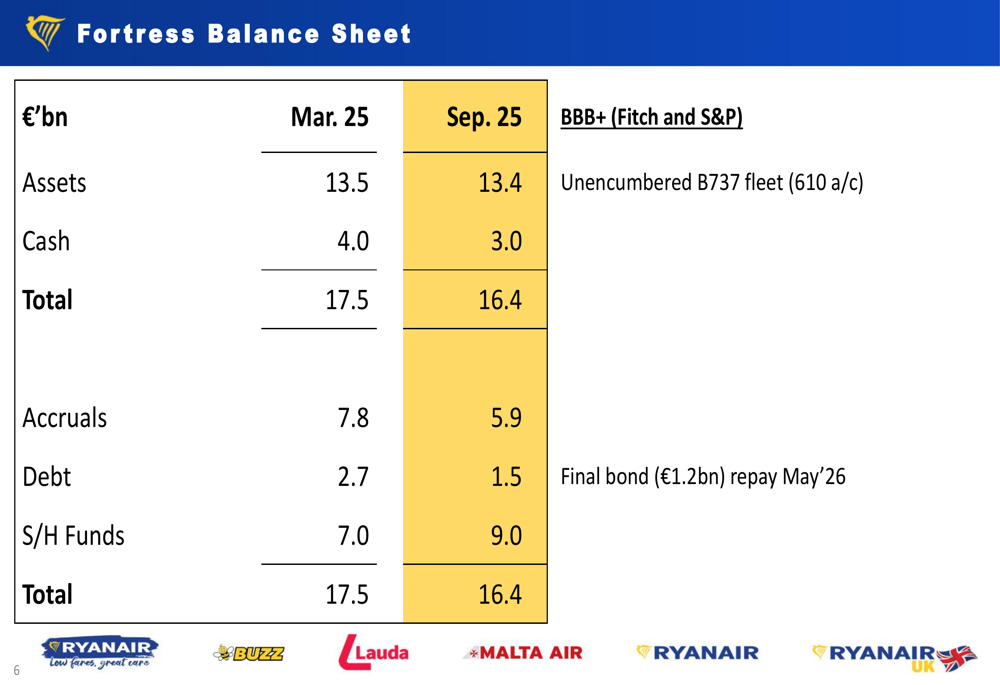

Ryanair’s financial position continues to strengthen, with shareholder funds increasing from €7.0 billion in March 2025 to €9.0 billion by September 2025. The company maintains a robust cash position of €3.0 billion, though this represents a planned reduction from €4.0 billion in March as the airline allocates capital to growth initiatives and shareholder returns.

The airline has significantly reduced its debt from €2.7 billion to €1.5 billion between March and September 2025, with only one remaining bond of €1.2 billion due in May 2026. Ryanair maintains investment-grade credit ratings (BBB+) from both Fitch and S&P, reflecting its financial stability.

The company’s balance sheet summary illustrates this strong financial foundation:

This financial strength provides Ryanair with strategic flexibility to navigate market uncertainties while continuing to invest in fleet expansion and return capital to shareholders through dividends and share buybacks.

Competitive Cost Advantage

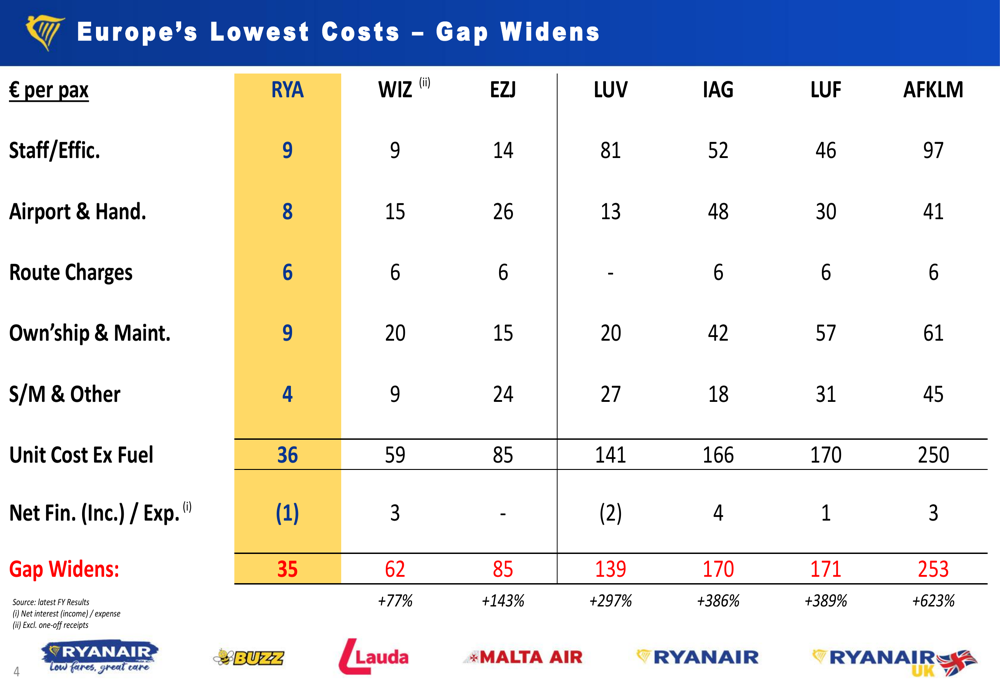

Central to Ryanair’s business model is its industry-leading cost structure. The airline maintains the lowest unit costs among European carriers, with a widening gap to competitors that reinforces its ability to offer lower fares while maintaining profitability.

The detailed cost comparison presented in the slides demonstrates Ryanair’s significant advantage:

With a unit cost excluding fuel of just €35 per passenger, Ryanair operates at a 77% cost advantage over its nearest competitor Wizz Air (€62) and a staggering 143% advantage over easyJet (€85). This gap extends to 623% when compared to Air France-KLM (€253).

This cost leadership enables Ryanair to profitably serve an extensive network spanning 95 bases and 224 airports across 36 countries, providing unmatched coverage in the European market.

Fleet Expansion and Growth Strategy

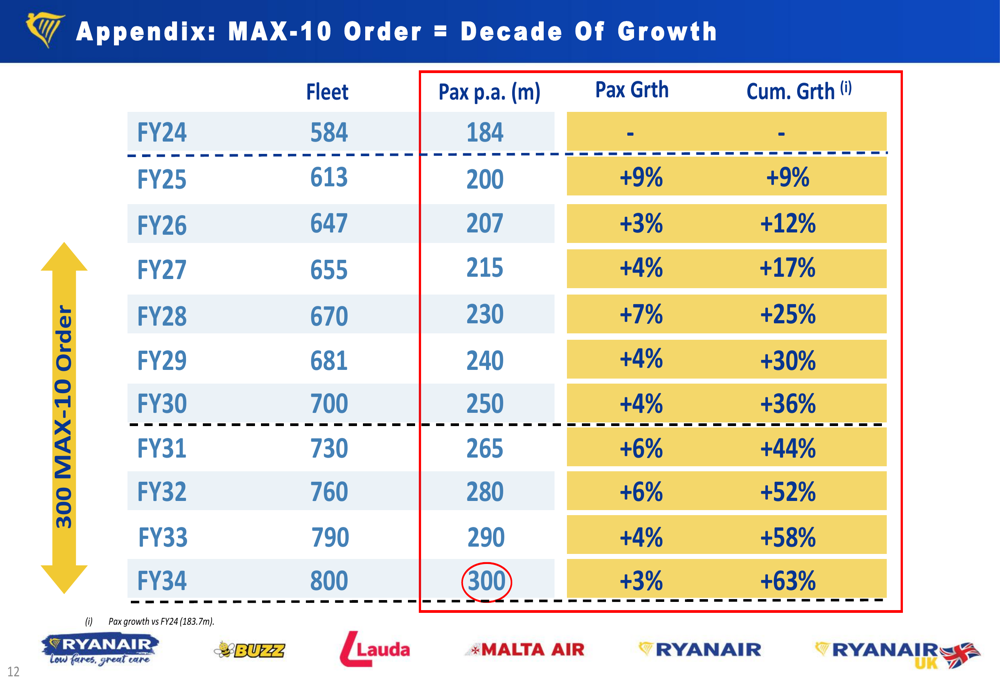

Ryanair has raised its full-year traffic target to 207 million passengers (previously 206 million), representing a 3% increase over FY25. The airline’s fleet currently stands at 640 aircraft, including 204 fuel-efficient "Gamechanger" models.

Looking ahead, Ryanair has placed a significant order for 300 Boeing MAX-10 aircraft, which will form the backbone of its growth strategy through 2034. These aircraft will deliver 20% more seats while reducing fuel consumption by 20% compared to current models, supporting both growth and environmental objectives.

The company’s long-term passenger forecast illustrates its ambitious growth trajectory:

This plan targets 300 million passengers annually by FY34, representing a 63% increase from FY24 levels. The growth will be supported by fleet expansion to 800 aircraft by FY34, with steady annual passenger increases averaging 5% per year.

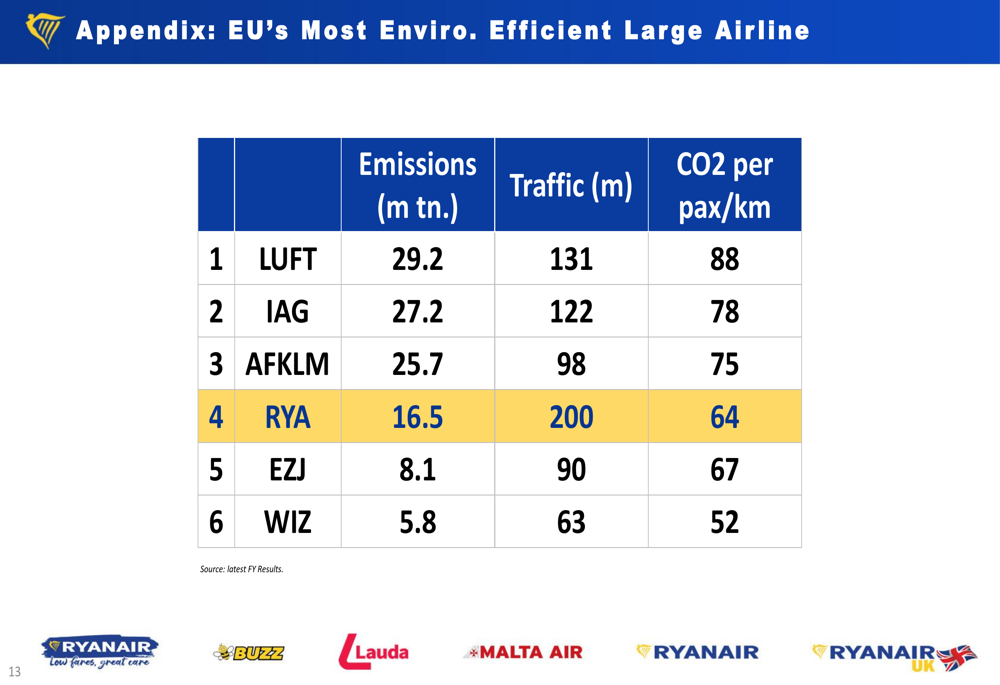

Environmental Positioning

Ryanair emphasizes its environmental efficiency in its presentation, claiming to be the most environmentally efficient large airline in Europe based on CO2 emissions per passenger kilometer.

The comparative data presented shows Ryanair’s environmental performance relative to competitors:

With CO2 emissions of 64 grams per passenger kilometer, Ryanair outperforms larger legacy carriers like Lufthansa (88), IAG (78), and Air France-KLM (75). Only Wizz Air shows better efficiency at 52 grams per passenger kilometer.

The airline’s environmental strategy is supported by its fleet modernization plan, with the future MAX-10 aircraft expected to further reduce emissions through improved fuel efficiency.

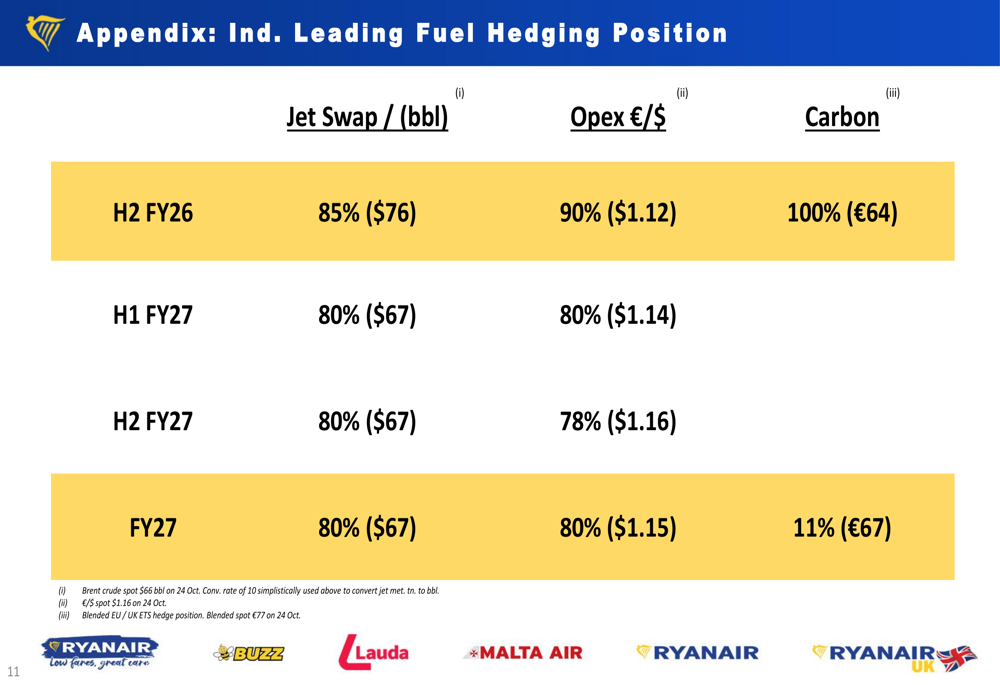

Fuel Hedging and Cost Management

Ryanair maintains an industry-leading fuel hedging position that provides significant cost visibility and protection against price volatility. The company has secured favorable rates for both jet fuel and currency exchange, positioning it well for future profitability.

The detailed hedging position illustrates this strategic approach:

With 85% of its H2 FY26 fuel requirements hedged at $76 per barrel and 80% of FY27 needs locked in at $67 per barrel, Ryanair has secured substantial savings compared to current market prices. Similarly, the company has hedged 80-90% of its dollar exposure for operational expenses at favorable rates.

Outlook and Forward Guidance

While Ryanair delivered strong H1 results, management expressed caution about the second half of the fiscal year, noting "tougher prior year comparisons" and "almost zero Q4 visibility" without the benefit of Easter falling in the period.

The company expects modest unit cost inflation for FY26, partially offset by fuel hedging benefits. Management indicated it’s "too early for FY26 PAT guidance" but expressed confidence in recovering all of the prior year’s 7% fare decline.

For FY27, Ryanair projects 4% traffic growth to 215 million passengers, supported by Boeing deliveries and favorable fuel hedging positions that lock in cost savings.

The airline’s long-term strategy remains focused on leveraging its cost advantage and fleet expansion to deliver sustainable growth, targeting 300 million passengers annually by FY34 while maintaining its position as Europe’s leading low-cost carrier.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.