US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

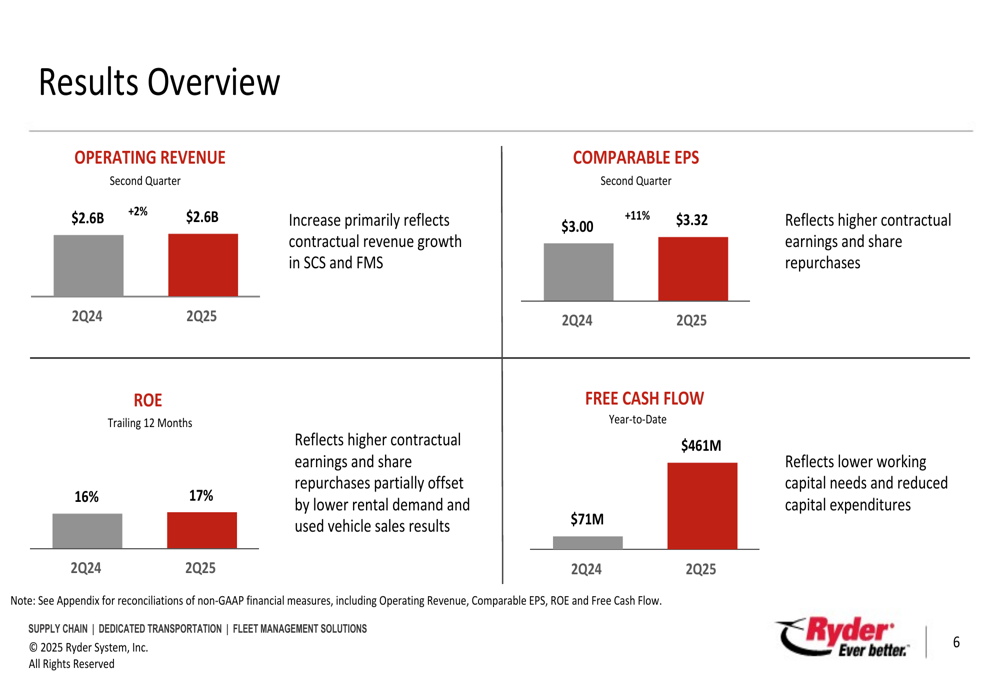

Ryder System Inc. (NYSE:R) presented its second quarter 2025 earnings on July 24, showcasing how its transformed business model is delivering stronger results despite ongoing challenges in the freight market. The company reported a 2% year-over-year increase in operating revenue to $2.6 billion and an 11% rise in comparable earnings per share to $3.32, demonstrating resilience in a difficult operating environment.

The logistics provider’s stock closed at $179.79 on the day of the presentation, up 0.83% for the session, though it showed a slight premarket decline of 0.65% the following day. According to available market data, Ryder shares have delivered approximately 29% returns over the past six months.

Quarterly Performance Highlights

Ryder’s second quarter results demonstrated the company’s ability to grow earnings despite market headwinds. Comparable EPS increased 11% year-over-year to $3.32, while return on equity improved to 17% from 16% in the same quarter last year. Free cash flow saw dramatic improvement, reaching $461 million year-to-date compared to just $71 million in the prior year period.

As shown in the following chart of key financial metrics for Q2 2025:

The company’s performance reflects higher contractual earnings and the impact of share repurchases, partially offset by lower rental demand and weaker used vehicle sales results. Management highlighted that the business transformation undertaken in recent years has structurally improved Ryder’s earnings and returns profile, making it more resilient during freight market downturns.

Segment Performance Analysis

Ryder’s performance varied across its three business segments, with Supply Chain Solutions (SCS) showing the strongest results.

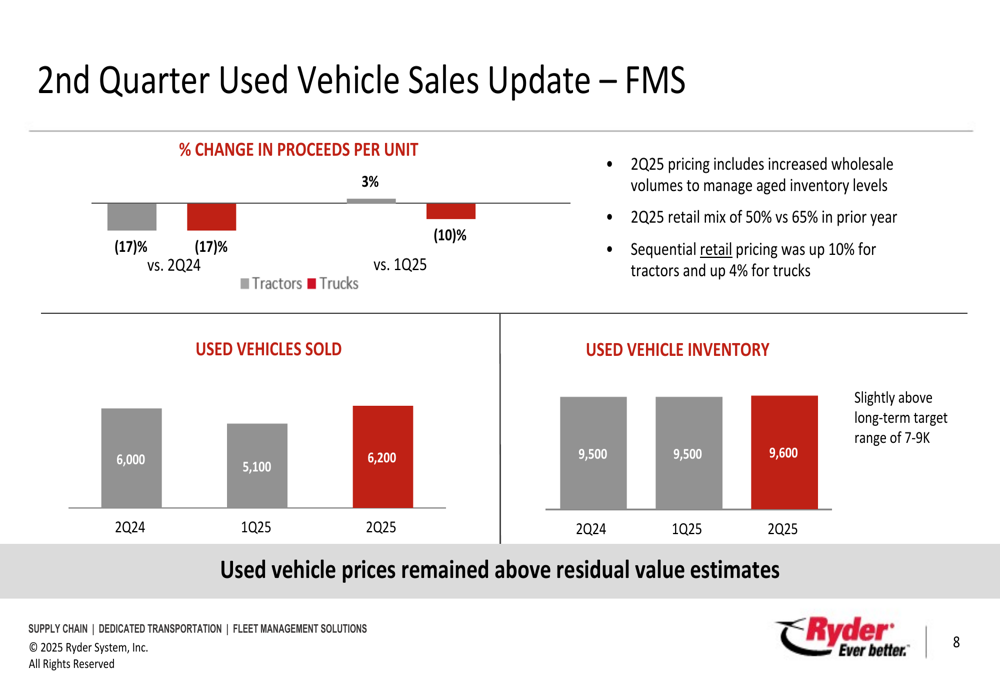

The Fleet Management Solutions (FMS) segment saw a modest 1% increase in operating revenue to $1.3 billion, but earnings before tax decreased 6% to $126 million. This decline was attributed to weaker used vehicle sales, which faced challenging market conditions and required higher wholesale volumes to manage aged inventory.

As shown in the following used vehicle sales update:

Used vehicle pricing declined 17% year-over-year for both tractors and trucks, with retail pricing showing some sequential improvement. The retail mix decreased to 50% compared to 65% in the prior year as the company worked to manage inventory levels, which remained slightly above the long-term target range of 7,000-9,000 units.

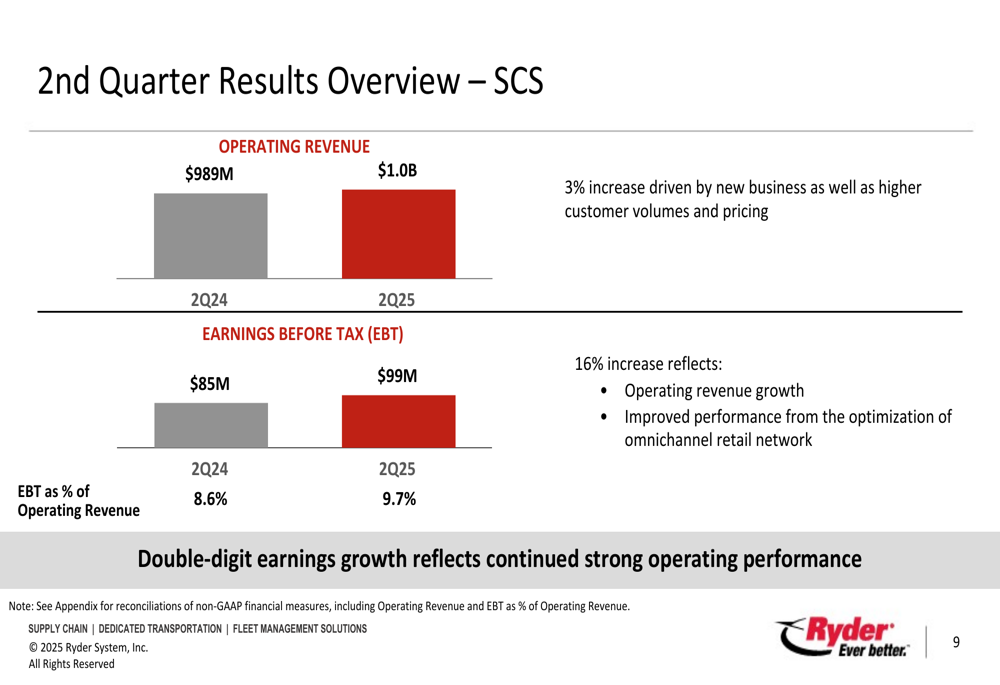

In contrast, the Supply Chain Solutions segment delivered strong results with a 3% increase in operating revenue to $1.0 billion and a substantial 16% increase in earnings before tax to $99 million. This performance was driven by new business, higher customer volumes, improved pricing, and better performance from the optimization of Ryder’s omnichannel retail network.

As illustrated in the SCS results:

The Dedicated Transportation Solutions (DTS) segment faced challenges with a 3% decrease in operating revenue to $470 million, reflecting lower fleet count due to the prolonged freight market downturn. Despite this, earnings before tax increased slightly by 1% to $37 million, supported by acquisition synergies and the absence of prior year integration costs.

Capital Allocation & Cash Flow

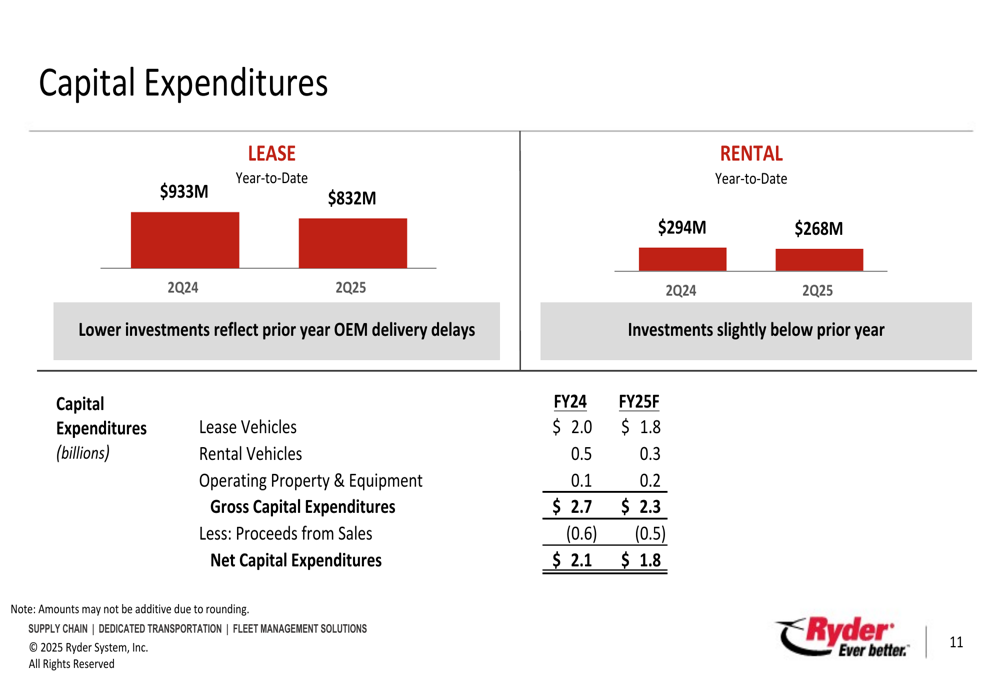

A significant highlight of Ryder’s presentation was the substantial improvement in cash flow and capital deployment capacity. The company increased its 2025 free cash flow forecast to $900 million - $1 billion, up $500 million from previous guidance, driven by reduced capital spending and the permanent reinstatement of tax bonus depreciation.

The capital expenditure breakdown shows a more disciplined approach to investments:

Year-to-date lease expenditures decreased from $933 million in Q2 2024 to $832 million in Q2 2025, while rental expenditures decreased slightly from $294 million to $268 million. For the full year 2025, Ryder forecasts gross capital expenditures of $2.3 billion, down from $2.7 billion in 2024.

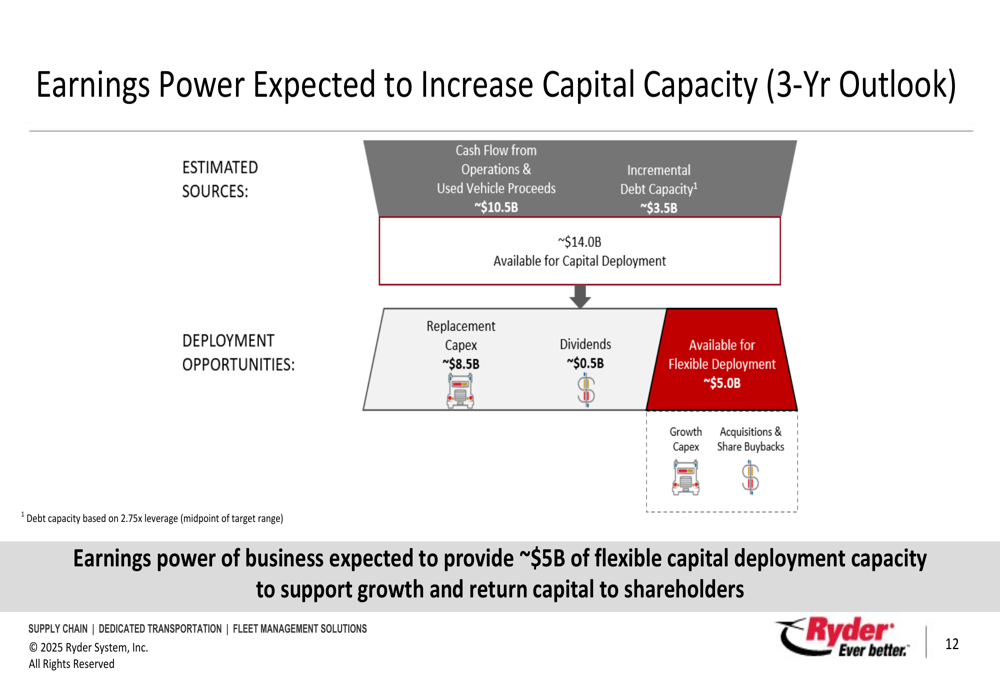

Looking ahead, Ryder expects significant capital deployment capacity over the next three years:

The company anticipates approximately $14 billion available for capital deployment, with about $5 billion available for flexible deployment after accounting for replacement capital expenditures and dividends. This flexibility positions Ryder to pursue growth opportunities and return capital to shareholders.

Strategic Initiatives & Outlook

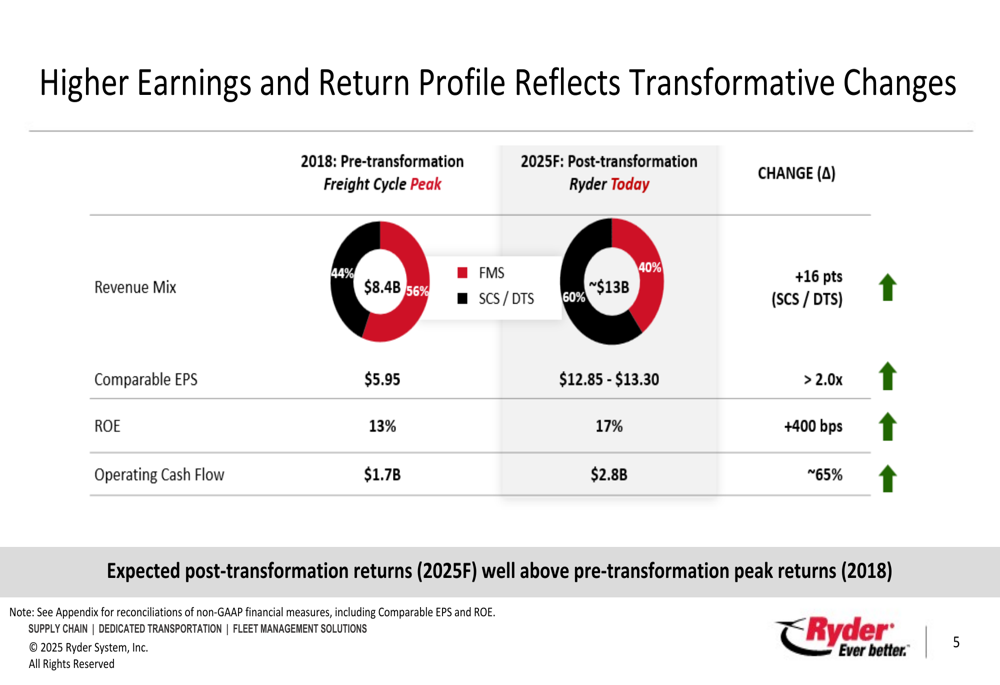

Ryder’s transformation has fundamentally changed its earnings and return profile compared to previous cycles. The company provided a compelling comparison of its financial performance between the pre-transformation peak in 2018 and its forecast for 2025:

This comparison shows that comparable EPS has more than doubled from $5.95 in 2018 to a projected $12.85-$13.30 in 2025, while ROE has improved by 400 basis points to 17%. Operating cash flow has increased by approximately 65% to $2.8 billion. Additionally, the revenue mix has shifted toward higher-margin Supply Chain and Dedicated Transportation services, which now represent 60% of revenue compared to 56% in 2018.

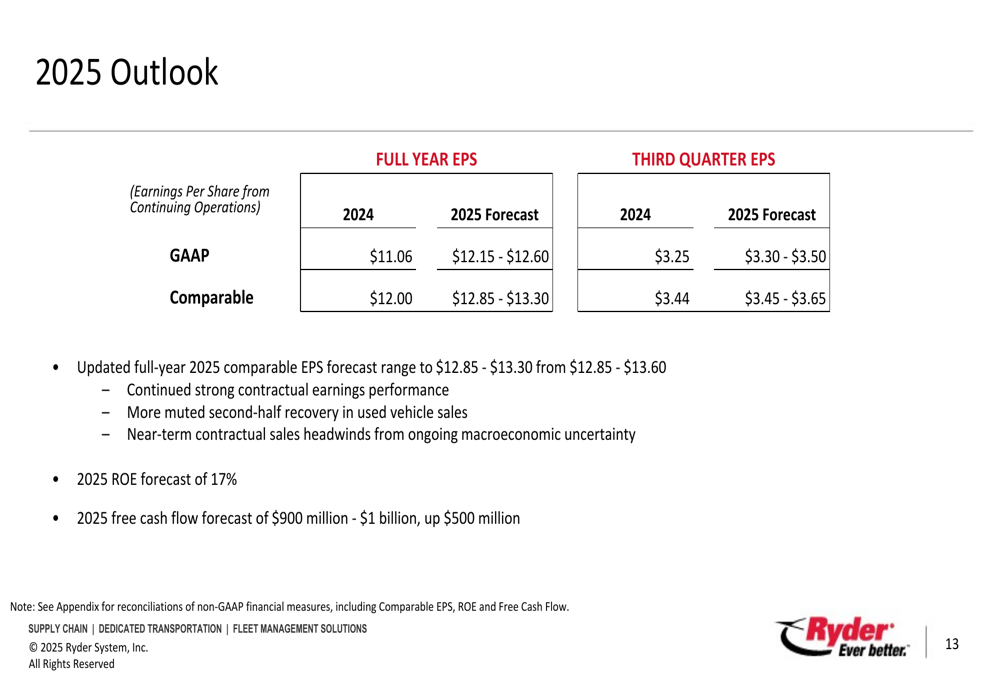

For the remainder of 2025, Ryder provided the following outlook:

The company updated its full-year 2025 comparable EPS forecast range to $12.85-$13.30, with third-quarter comparable EPS projected at $3.45-$3.65. This guidance reflects continued strong contractual earnings performance, though tempered by a more muted second-half recovery in used vehicle sales and near-term contractual sales headwinds from ongoing macroeconomic uncertainty.

Ryder identified several strategic initiatives expected to drive earnings growth, including profitable contractual growth across all segments, ChoiceLease pricing and maintenance cost savings, acquisition synergies, and optimization of its omnichannel retail network. These initiatives are expected to deliver more than $150 million in pre-tax earnings benefits, with an additional $200+ million potential benefit when market conditions improve.

During the earnings call, CEO Robert Sanchez emphasized the company’s strategic focus, stating, "We are expecting long-term secular trends that favor transportation and logistics outsourcing remain strong." He also highlighted Ryder’s financial flexibility, noting, "We feel really good about the dry powder. We’ve got repurchase programs in place already."

While Ryder faces challenges from the prolonged freight market downturn and uncertainty in contractual sales, its transformed business model appears well-positioned to continue delivering improved returns and shareholder value through the current market cycle and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.