Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Ryerson Holding Corp (NYSE:RYI) returned to profitability in the second quarter of 2025, according to its latest earnings presentation released on July 30, 2025. The metal service center operator posted a modest profit after reporting a loss in the previous quarter, though overall market conditions remain challenging.

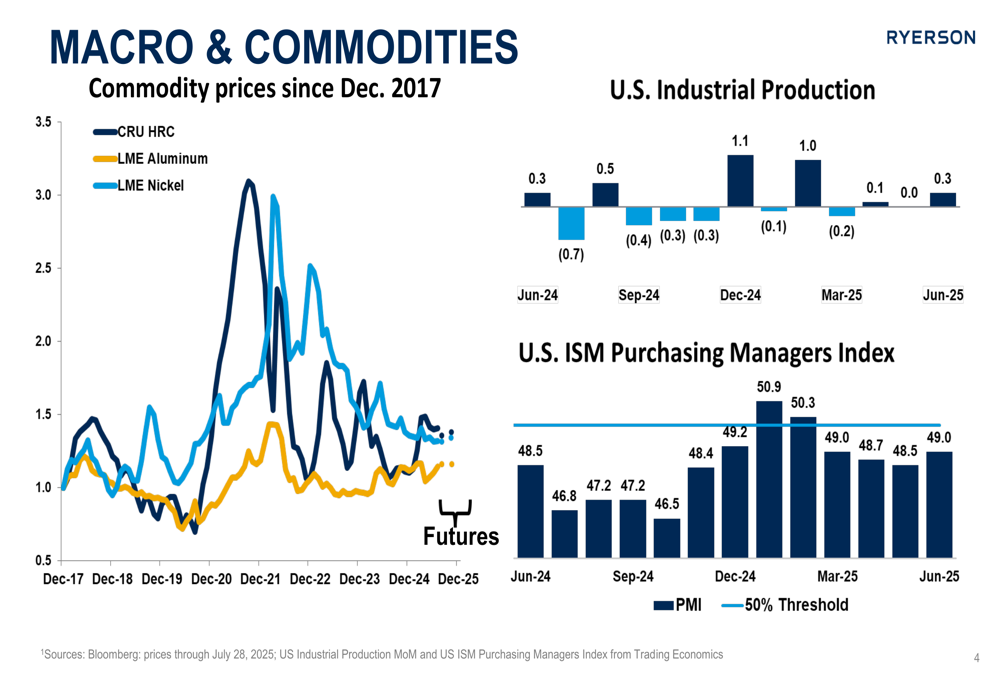

The company’s performance comes against a backdrop of tepid industrial activity, with the U.S. ISM Purchasing Managers Index remaining below the 50% expansion threshold at 48.5 in June 2025. U.S. Industrial Production showed modest month-over-month growth of 0.3% in June, down from stronger readings earlier in the year.

As shown in the following chart of macroeconomic indicators and commodity prices, the operating environment remains challenging:

Quarterly Performance Highlights

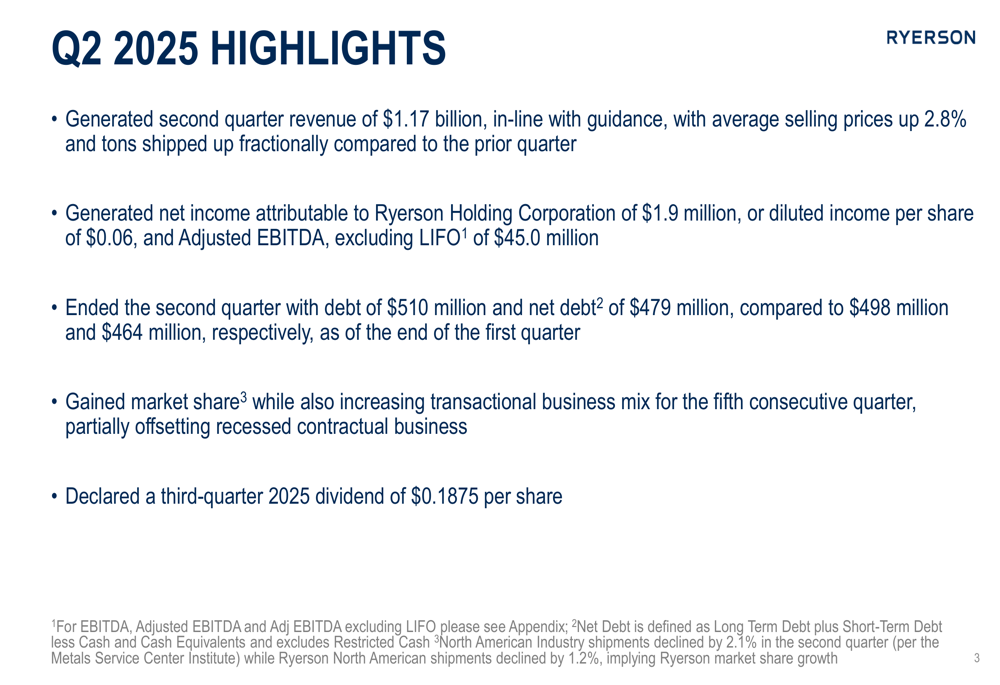

Ryerson reported Q2 2025 revenue of $1.17 billion, in line with guidance and representing a 3.0% increase from the previous quarter. The company returned to profitability with net income of $1.9 million, or $0.06 per diluted share, compared to a loss of $5.6 million, or -$0.18 per share in Q1 2025.

The following slide summarizes Ryerson’s key Q2 2025 highlights, including revenue performance and dividend declaration:

Adjusted EBITDA excluding LIFO reached $45.0 million, up $12.2 million quarter-over-quarter and at the high end of the company’s previous guidance range. This improvement came despite continued challenges in the stainless steel market that had impacted Q1 results.

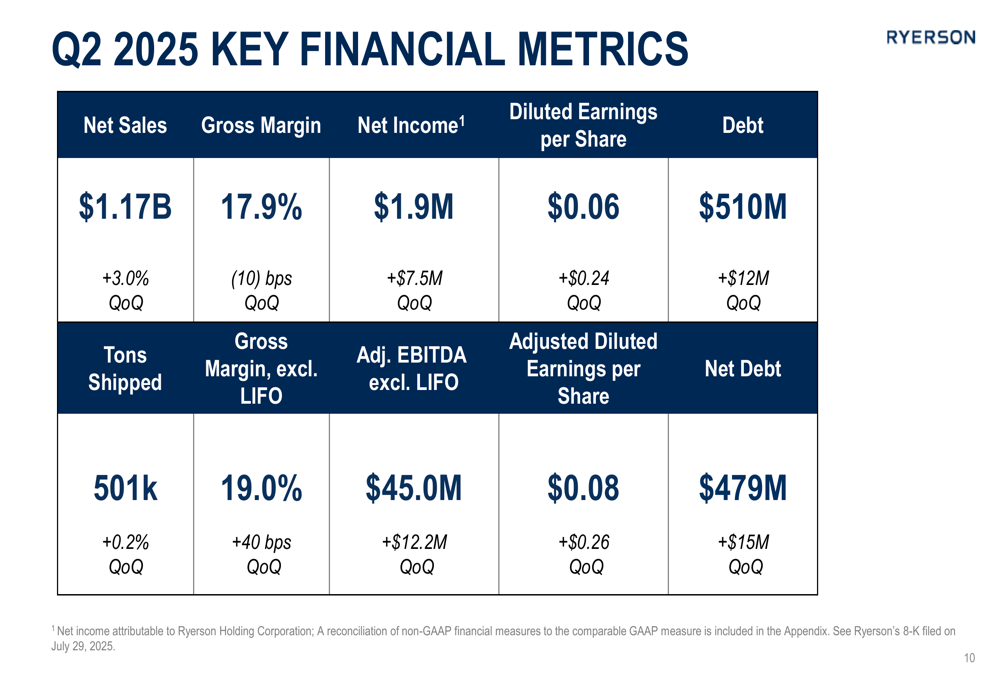

The comprehensive overview of key financial metrics shows the sequential improvement across multiple indicators:

Ryerson shipped 501,000 tons in Q2, representing a fractional increase of 0.2% compared to Q1. Average selling prices rose 2.8% to $2,334 per ton. Gross margin excluding LIFO improved to 19.0%, up 40 basis points from the previous quarter.

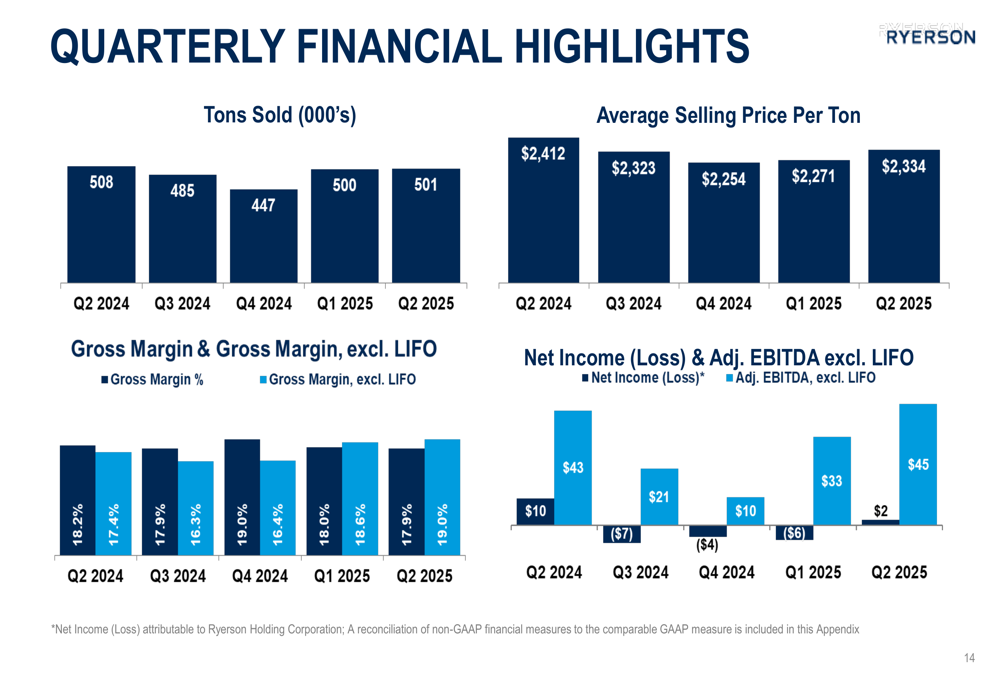

The following chart illustrates the quarterly progression of tons sold, average selling prices, and financial metrics:

Detailed Financial Analysis

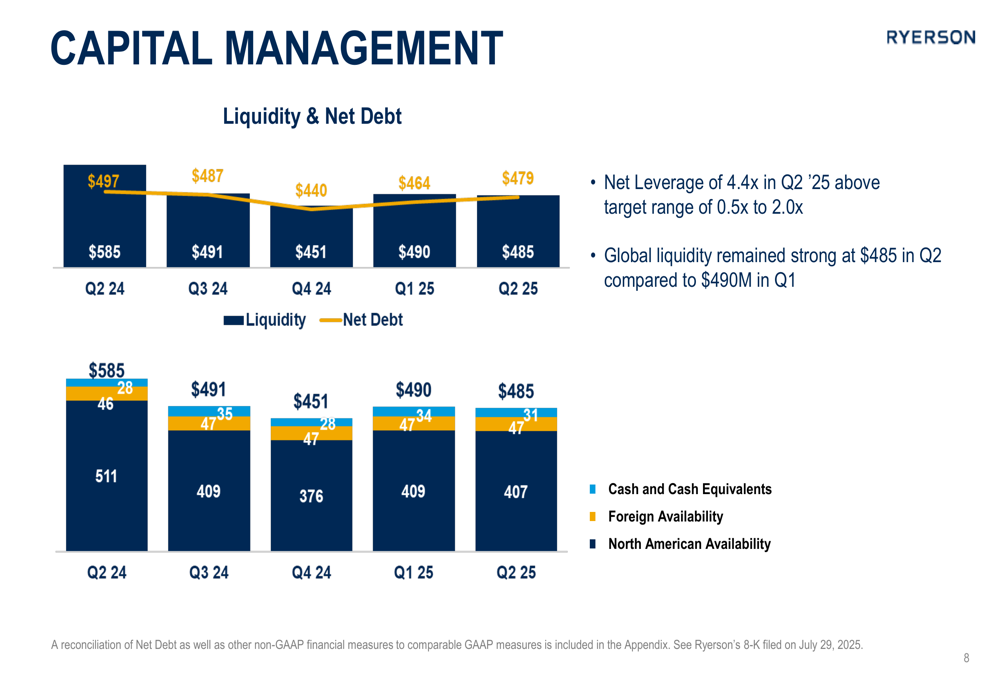

Ryerson’s capital management remains a focus area, with net debt increasing to $479 million from $464 million in Q1. The company’s net leverage ratio of 4.4x remains above its target range of 0.5x to 2.0x, though liquidity remains strong at $485 million.

The following chart illustrates Ryerson’s liquidity position and net debt trends:

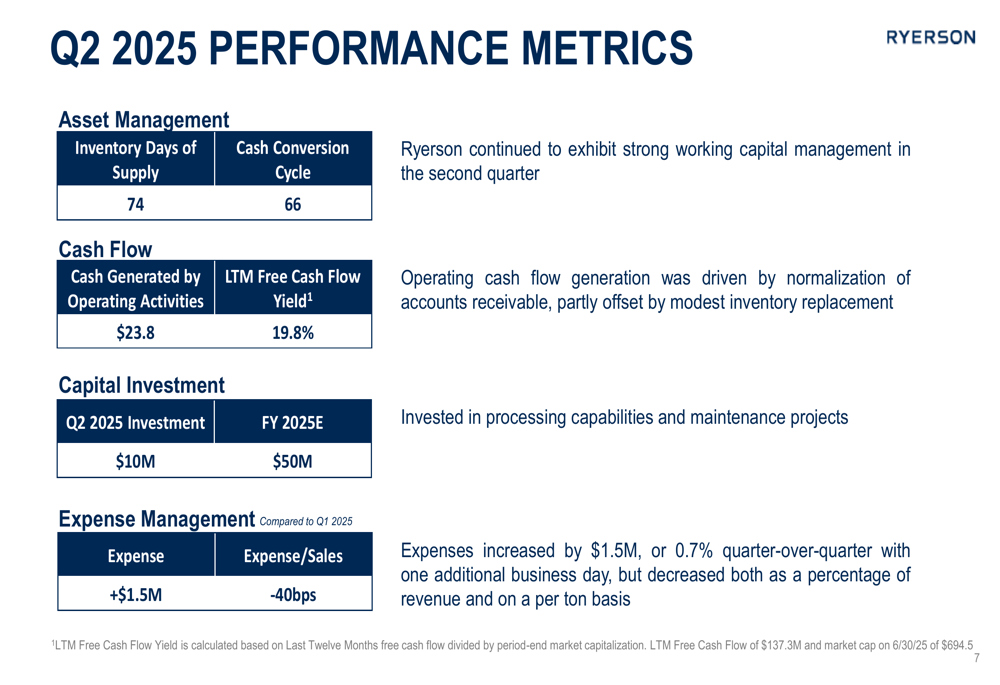

The company continues to demonstrate strong working capital management, with inventory days of supply at 74 and a cash conversion cycle of 66 days. Cash generated by operating activities reached $23.8 million, driven by normalization of accounts receivable, partially offset by modest inventory replacement.

Ryerson’s performance metrics across various operational categories show the company’s focus on efficiency:

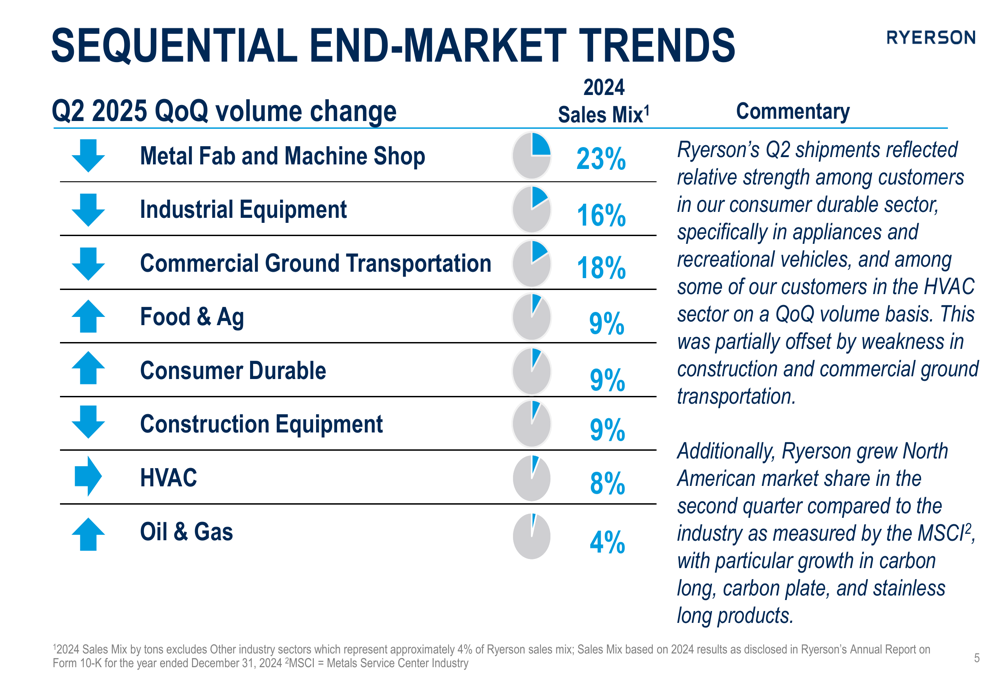

The company’s end-market performance varied by sector, with Ryerson gaining North American market share particularly in carbon long, carbon plate, and stainless long products. The sales mix remains diversified across multiple industries, with metal fabrication and machine shops (23%), commercial ground transportation (18%), and industrial equipment (16%) representing the largest segments.

The following slide details the sequential end-market trends and sales mix:

Strategic Initiatives

Ryerson continues to invest in modernizing its operations and enhancing its service capabilities. The company invested $10 million in capital projects during Q2 2025, with a full-year target of $50 million focused on processing capabilities and maintenance projects.

Key strategic investments include the Shelbyville expansion project, which features a state-of-the-art cut-to-length line and automated storage and retrieval system for sheet products. The company expects this $40 million investment to generate an internal rate of return of approximately 35%.

The following slide details Ryerson’s ongoing business investments:

Ryerson’s capital allocation strategy prioritizes operationalization of existing investments, with a quarterly dividend of $0.1875 per share declared for Q3 2025. The company is currently prioritizing deleveraging over share repurchases while maintaining a selective approach to M&A opportunities.

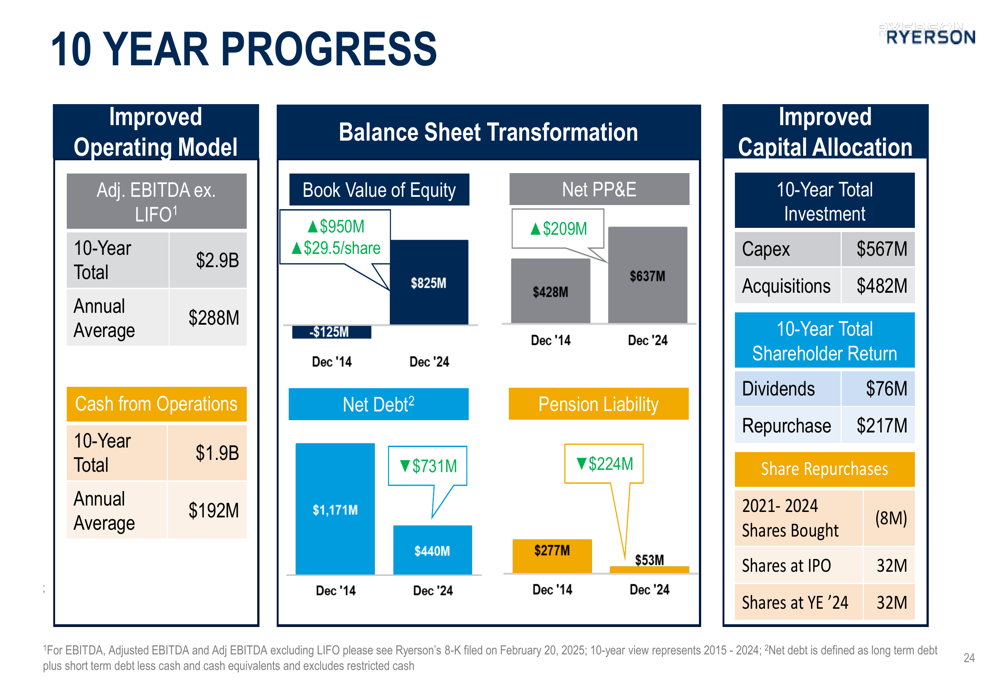

Looking at the company’s 10-year progress, Ryerson has generated $2.9 billion in adjusted EBITDA excluding LIFO over the past decade, while significantly improving its balance sheet. The book value of equity has increased by $950 million, while net debt has decreased by $731 million.

The following chart summarizes Ryerson’s 10-year progress:

Forward-Looking Statements

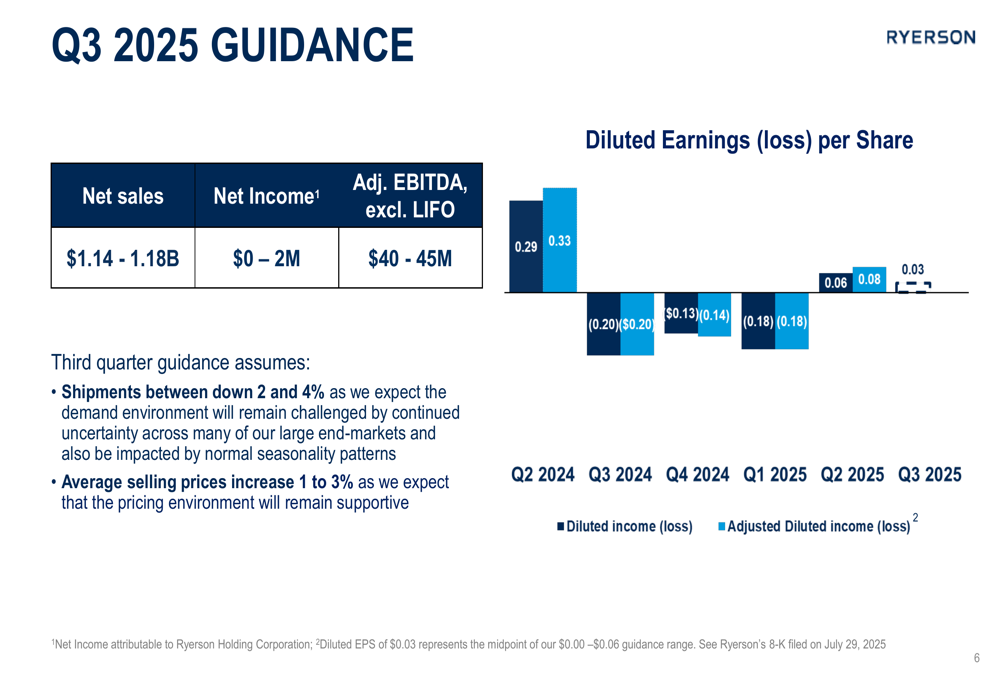

For Q3 2025, Ryerson provided guidance for net sales between $1.14 billion and $1.18 billion, with net income projected between $0 and $2 million. Adjusted EBITDA excluding LIFO is expected to be between $40 million and $45 million.

The company anticipates shipments to decline between 2% and 4% in Q3, while average selling prices are expected to increase between 1% and 3%. Diluted earnings per share are projected at approximately $0.03 for Q3 2025.

The following slide details Ryerson’s Q3 2025 guidance:

Ryerson’s longer-term strategy focuses on three phases: deleveraging and reorienting toward public shareholders; investing in modernization and automation while integrating its North American service center network; and gaining market share with margin accretion. The company has set a target of $350-400 million in through-the-cycle adjusted EBITDA.

Despite returning to profitability in Q2, Ryerson’s stock has faced pressure, with shares declining 3.63% to $22.62 in recent trading. The stock remains above its 52-week low of $17.18 but well below its 52-week high of $27.41, reflecting ongoing investor concerns about the challenging market environment and the company’s above-target leverage ratio.

As Ryerson continues to execute its strategic initiatives and navigate market headwinds, the company’s focus on operational efficiency, market share gains, and strategic investments positions it to capitalize on any improvement in industrial activity and metal demand in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.