Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Sabra Health Care REIT (NYSE:WELL) Inc (NASDAQ:SBRA) released its latest investor presentation on May 5, 2025, highlighting the company’s strategic positioning in the healthcare real estate sector. The presentation, themed "Strategic, Disciplined, Opportunistic," outlines Sabra’s portfolio composition, financial strength, and growth initiatives amid favorable demographic trends in the healthcare industry.

With a stock price of $17.28 as of May 5, 2025, Sabra trades at a discount to many of its peers while maintaining a robust dividend yield of 6.8%. The company’s presentation comes after a strong Q3 2024 performance that saw year-over-year revenue growth of 7.6% and a cash NOI increase of 17.8%.

Portfolio Composition and Strategy

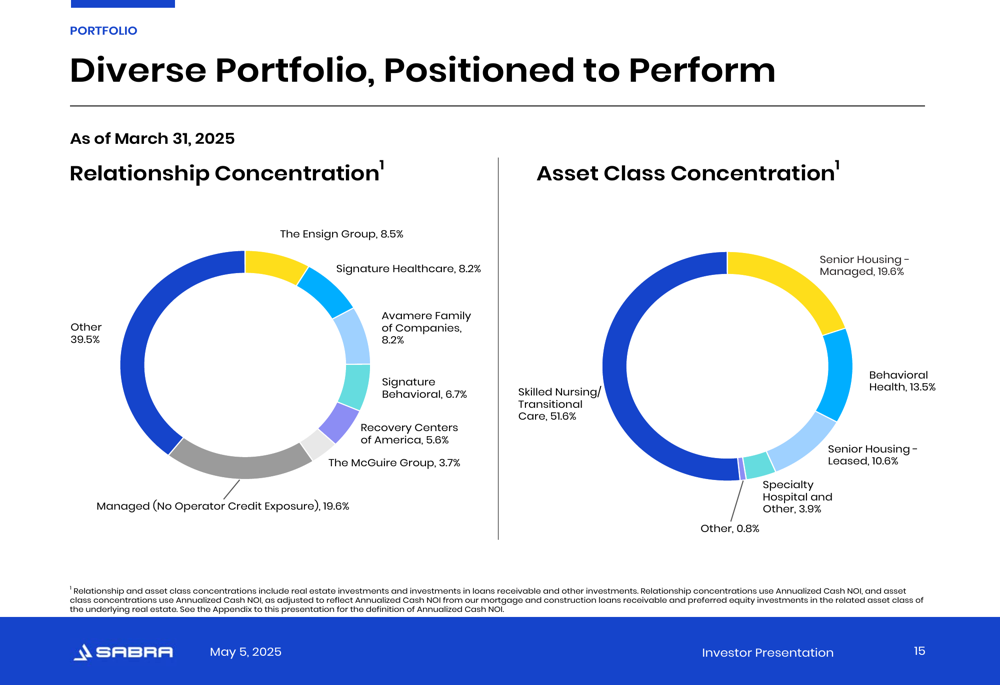

As of March 31, 2025, Sabra’s portfolio consists of 399 investments across 59 relationships with a weighted average remaining lease term of 7 years. The company maintains a diversified portfolio with a strategic focus on needs-based healthcare facilities.

The portfolio’s asset class concentration reveals a significant focus on skilled nursing facilities, which aligns with the company’s strategy to capitalize on favorable demographic trends.

As shown in the following chart of Sabra’s portfolio composition:

Skilled nursing and transitional care facilities represent the largest portion of Sabra’s portfolio at 51.6%, followed by senior housing-managed properties at 19.6%, behavioral health facilities at 13.5%, and senior housing-leased properties at 10.6%. This diversification strategy helps mitigate risk while maintaining exposure to high-demand healthcare segments.

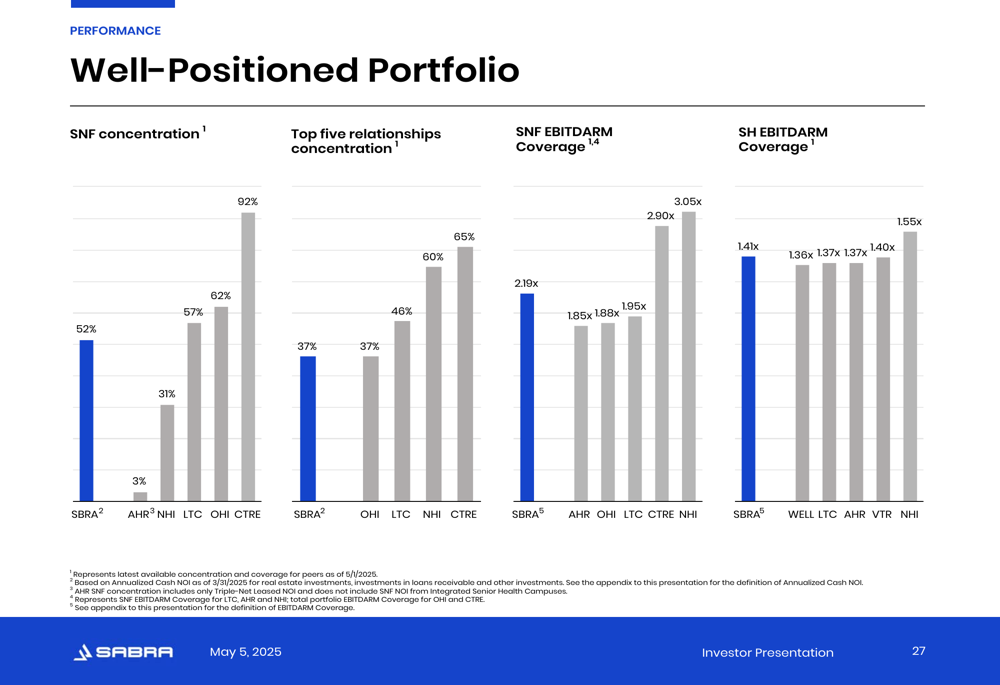

Occupancy rates across the portfolio stand at 82% for skilled nursing/transitional care, 90% for senior housing-leased, and 78% for behavioral health/hospitals/other facilities. The company’s EBITDARM coverage ratios demonstrate the financial health of its tenants, with 2.19x for skilled nursing/transitional care, 1.41x for senior housing-leased, and 3.77x for behavioral health/hospitals/other.

Market Dynamics and Growth Drivers

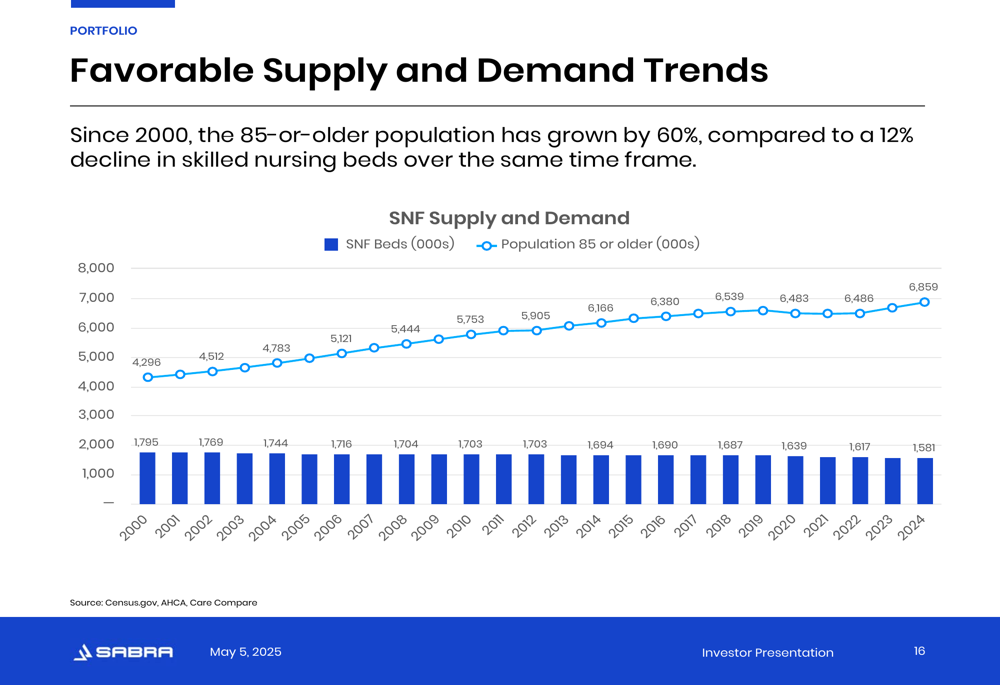

Sabra’s presentation highlights compelling demographic trends supporting long-term demand for healthcare facilities. The company notes that the population aged 85 or older is expected to grow 4% annually through 2040, creating sustained demand for senior care services.

The following graph illustrates the diverging trends between the growing elderly population and declining supply of skilled nursing beds:

Since 2000, the 85+ population has grown by 60%, while the supply of skilled nursing beds has declined by 12%. This supply-demand imbalance creates favorable conditions for existing skilled nursing facility operators and their REIT partners.

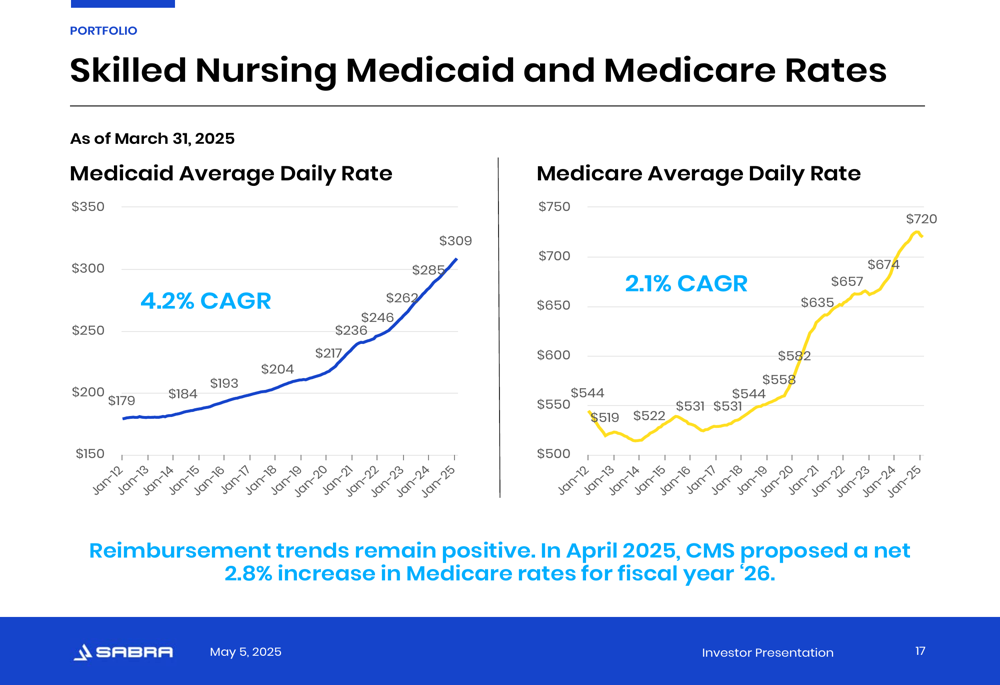

Additionally, reimbursement rates continue to show positive trends, providing revenue stability for operators:

Medicaid rates have increased from $179 in January 2012 to $309 in January 2025, representing a 4.2% CAGR. Medicare rates have grown from $519 to $720 over the same period, a 2.1% CAGR. The presentation also notes that in April 2025, CMS proposed a net 2.8% increase in Medicare rates for fiscal year 2026, further supporting operator financial stability.

Financial Position and Valuation

Sabra maintains a strong balance sheet with approximately $1 billion in liquidity and 98% of its borrowings being unsecured. The company’s term loans are hedged at a fixed rate of 4.1% through early 2028, providing interest rate stability.

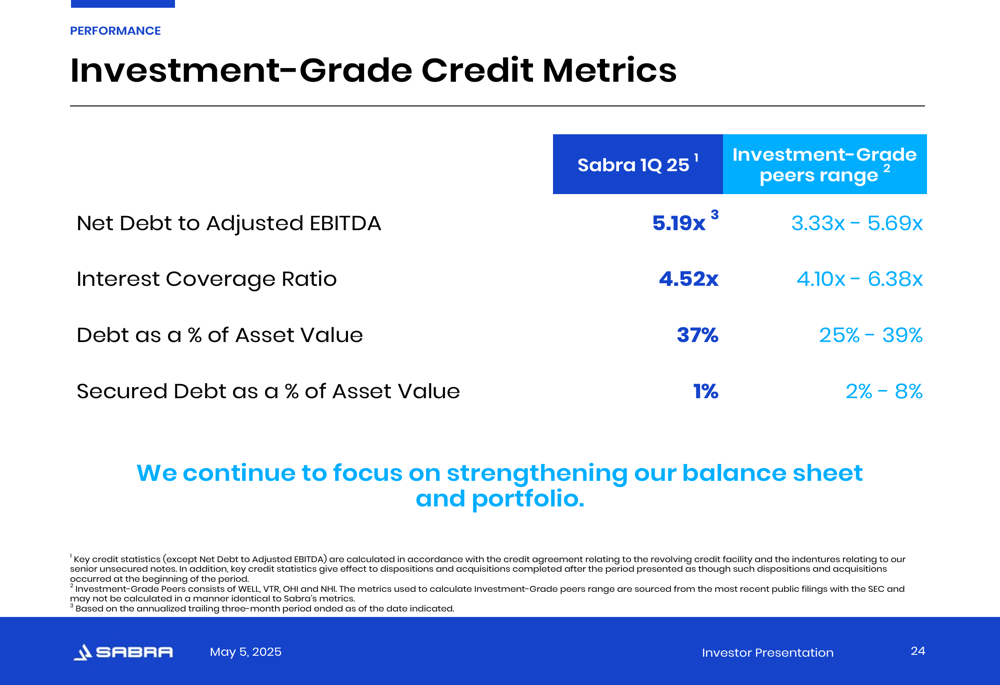

The company’s investment-grade credit metrics compare favorably to peers:

With a net debt to adjusted EBITDA ratio of 5.19x, Sabra falls within the range of investment-grade peers (3.33x-5.69x). The company’s interest coverage ratio stands at 4.52x, while debt as a percentage of asset value is 37%. These metrics demonstrate Sabra’s financial discipline and balance sheet strength.

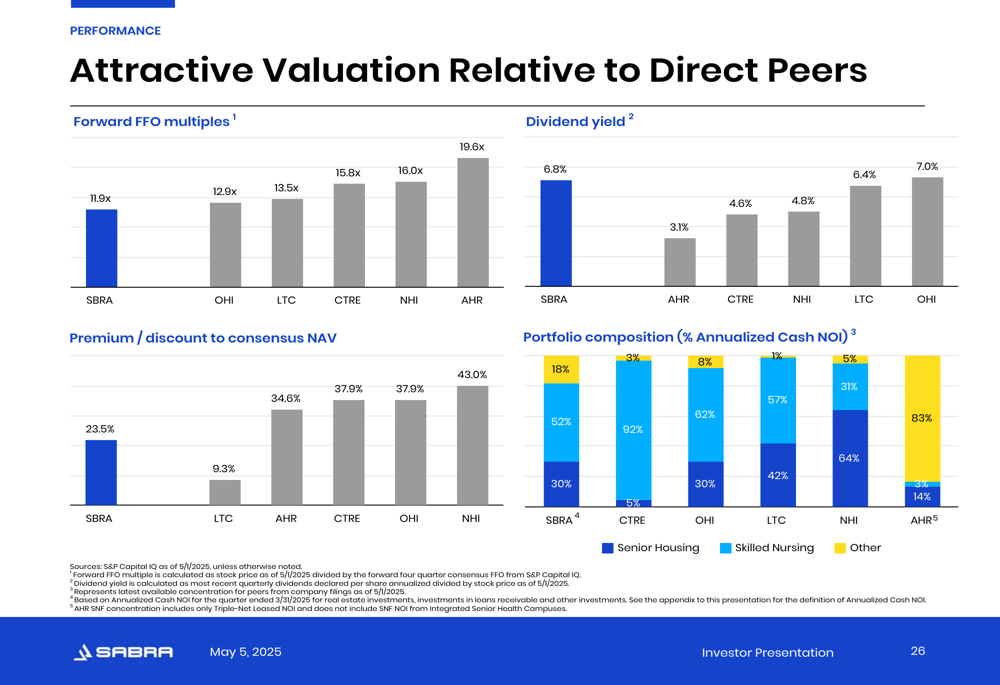

The presentation also highlights Sabra’s attractive valuation relative to peers:

Sabra trades at a forward FFO multiple of 11.9x, below the range of direct peers (12.9x-19.6x), suggesting potential upside opportunity. The company’s dividend yield of 6.8% is among the highest in its peer group, offering an attractive income component for investors.

ESG Initiatives

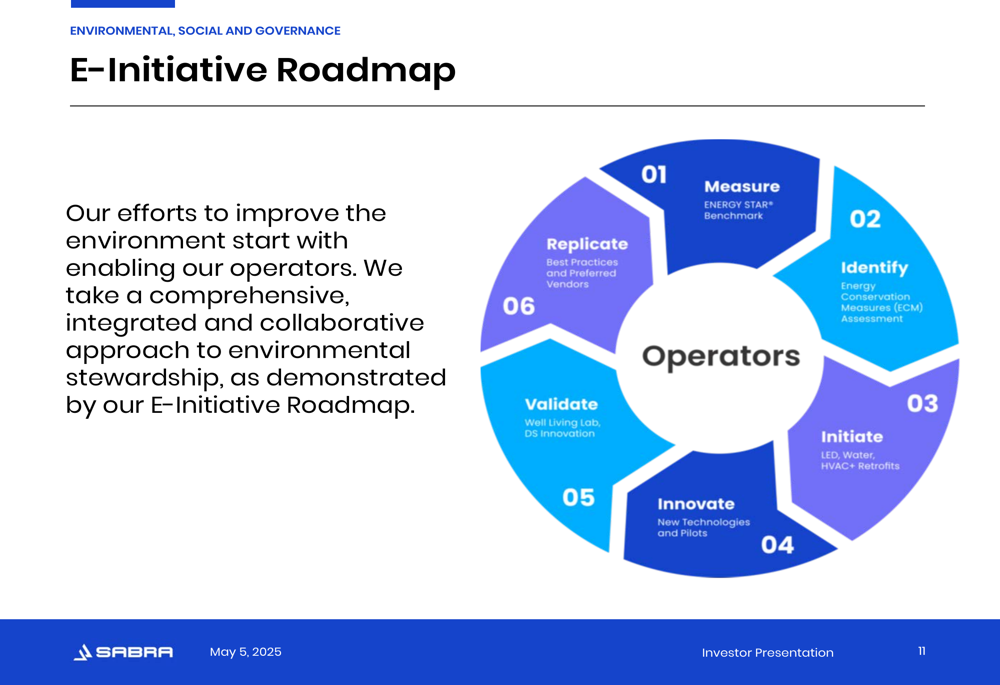

Sabra emphasizes its commitment to environmental, social, and governance initiatives. The company has implemented a comprehensive environmental roadmap focused on energy efficiency and sustainability:

The E-Initiative Roadmap outlines a six-step process for environmental improvements, starting with measurement and benchmarking, followed by identifying energy conservation measures, implementing retrofits, innovating with new technologies, validating results, and replicating successful practices across the portfolio.

The company also highlights its commitment to diversity, equity, and inclusion:

As of March 31, 2025, women comprise 57% of Sabra’s workforce and 61% of management/leadership positions. Additionally, 33% of team members self-identify as members of one or more ethnic minorities, with actual diversity potentially higher as 14% chose not to self-identify.

Strategic Initiatives and Forward Outlook

Sabra’s presentation outlines its execution strategy, focusing on unique, accretive investments, supporting operator expansion, creatively financed development, portfolio optimization, and prudent financing. The company positions itself as a capital partner of choice for operators committed to delivering quality care.

CEO Rick Matros emphasizes the importance of what happens inside Sabra’s buildings, highlighting the company’s alignment with operators who provide compassionate care. Chief Investment Officer Talya Nevo-Hacohen reinforces the commitment to delivering long-term value through consistent strategy execution and providing capital to tenants.

The company’s recent performance supports this strategic direction, with the Q3 2024 earnings report showing sequential improvement in skilled nursing facility occupancy by 130 basis points and triple-net senior housing occupancy stabilizing around 90%.

Competitive Industry Position

Sabra’s presentation positions the company favorably against its REIT peers:

The company’s portfolio demonstrates competitive EBITDARM coverage ratios and a balanced approach to property type concentration. This positioning, combined with the company’s focus on relationships with regional operators in markets with favorable demographics, supports Sabra’s competitive advantage in the healthcare REIT sector.

Looking ahead, Sabra appears well-positioned to capitalize on demographic tailwinds and reimbursement rate increases while maintaining financial discipline and supporting its operator partners. The company’s strategy of selective acquisitions in senior housing and skilled nursing, as mentioned in the Q3 2024 earnings call, aligns with its presentation messaging of being "strategic, disciplined, and opportunistic" in its approach to growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.