Commerce launches BigCommerce Payments powered by PayPal for 2026

Introduction & Market Context

Safehold Inc (NYSE:SAFE), a leading ground lease-focused real estate investment trust, released its second quarter 2025 earnings presentation on August 5, 2025, showing modest revenue growth amid a challenging real estate environment. The company reported a 4% year-over-year increase in revenue while resuming portfolio expansion after a period of market volatility.

Following the announcement, Safehold’s stock closed at $14.15, up 0.67% for the day. The stock has been trading in a 52-week range of $13.68 to $28.80, indicating continued market uncertainty about the company’s growth trajectory despite its stable business model.

Quarterly Performance Highlights

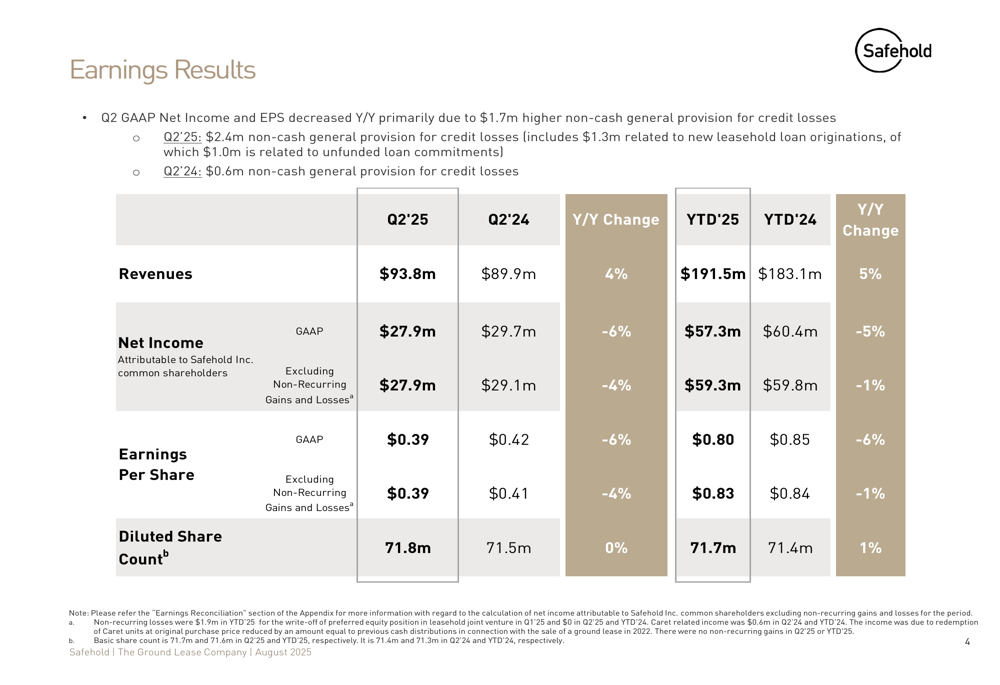

Safehold reported Q2 2025 revenues of $93.8 million, a 4% increase compared to $89.9 million in Q2 2024. However, GAAP net income decreased 6% year-over-year to $27.9 million, primarily due to a $1.7 million higher non-cash general provision for credit losses. Earnings per share followed a similar pattern, declining 6% to $0.39 from $0.42 in the same period last year.

As shown in the following earnings results table:

The company’s year-to-date performance showed similar trends, with revenues up 5% to $191.5 million, while net income decreased 5% to $57.3 million. When excluding non-recurring gains and losses, the decline in net income was less pronounced at 4% for the quarter and 1% for the year-to-date period, suggesting relatively stable core operations.

Portfolio Growth and Diversification

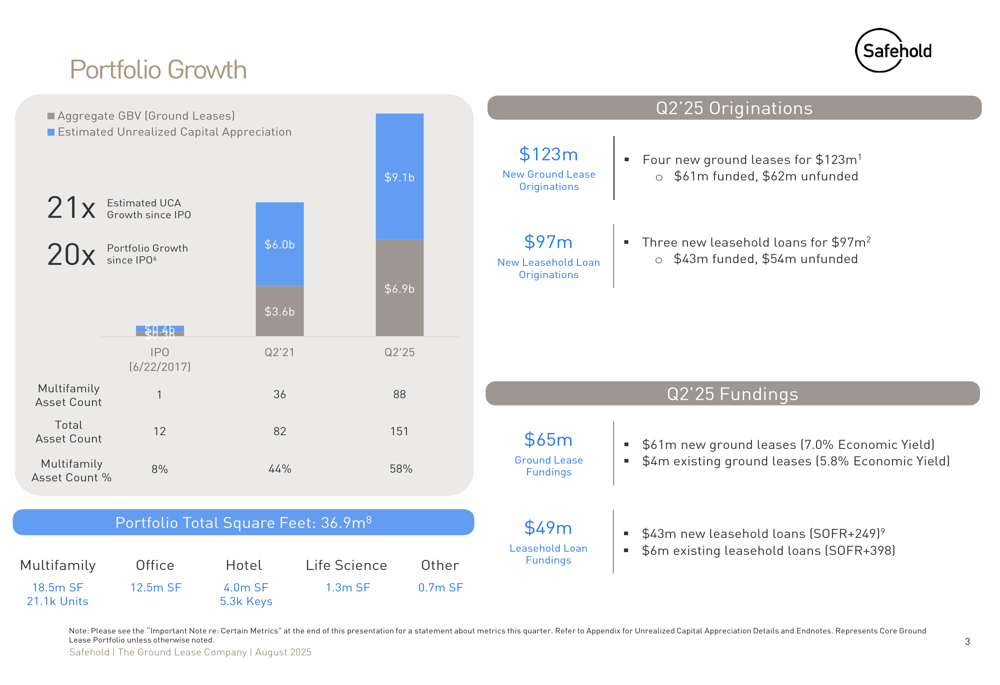

After reporting no new originations in Q1 2025 due to market volatility, Safehold resumed its portfolio expansion in Q2 with four new ground leases valued at $123 million and three new leasehold loans worth $97 million. This activity reflects improved market conditions and the company’s ability to identify attractive investment opportunities.

The following chart illustrates Safehold’s impressive portfolio growth since its IPO:

Since its IPO in June 2017, Safehold has achieved remarkable growth, expanding its portfolio 20x and its estimated unrealized capital appreciation (UCA) 21x. The company’s strategic focus on multifamily assets has resulted in this property type growing from just 8% of the portfolio at IPO to 58% currently, with 88 multifamily assets in the portfolio.

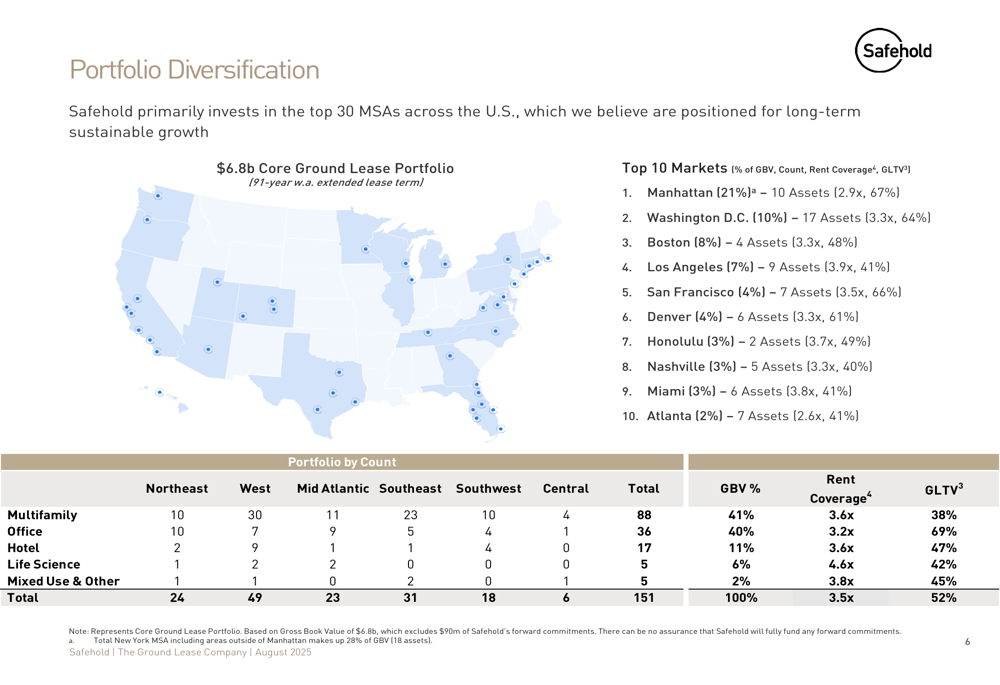

Safehold’s portfolio remains well-diversified across property types and geography, with a strong presence in major metropolitan areas. Manhattan represents the largest market concentration at 21% of the portfolio, followed by Washington D.C. (10%) and Boston (8%).

The company’s geographic and property type diversification is illustrated in the following breakdown:

The portfolio maintains healthy metrics with a ground lease-to-value (GLTV) ratio of 52% and rent coverage of 3.5x, indicating strong underlying asset quality and tenant financial health. Multifamily assets, which comprise 41% of the gross book value, show particularly strong metrics with 3.6x rent coverage and a conservative 38% GLTV.

Capital Structure and Financial Position

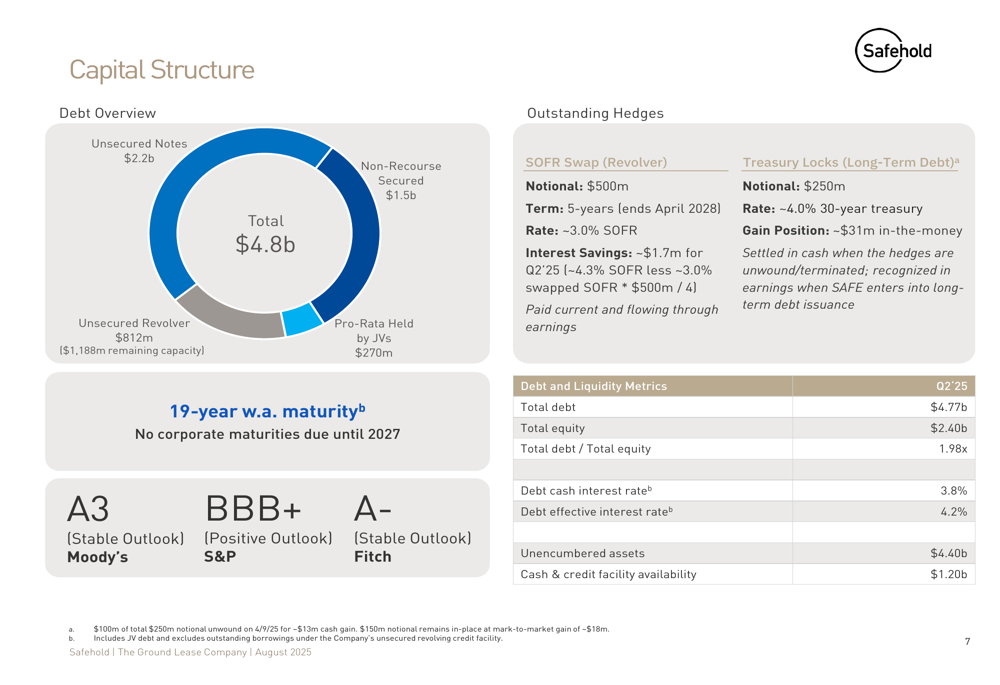

Safehold maintains a solid capital structure with $4.77 billion in total debt and $2.40 billion in total equity, resulting in a debt-to-equity ratio of 1.98x. The company’s debt carries an effective interest rate of 4.2%, with a weighted average maturity of 19 years and no corporate maturities due until 2027.

The following chart details Safehold’s capital structure:

The company maintains strong liquidity with $1.2 billion in cash and credit facility availability. Additionally, Safehold has $400 million in remaining capital for its joint venture with a leading sovereign wealth fund, providing ample resources for future growth opportunities.

Safehold’s financial strength is further validated by its investment-grade credit ratings: A3 (Stable Outlook) from Moody’s, BBB+ (Positive Outlook) from S&P, and A- (Stable Outlook) from Fitch. The positive outlook from S&P suggests potential for a rating upgrade, which could further reduce the company’s cost of capital.

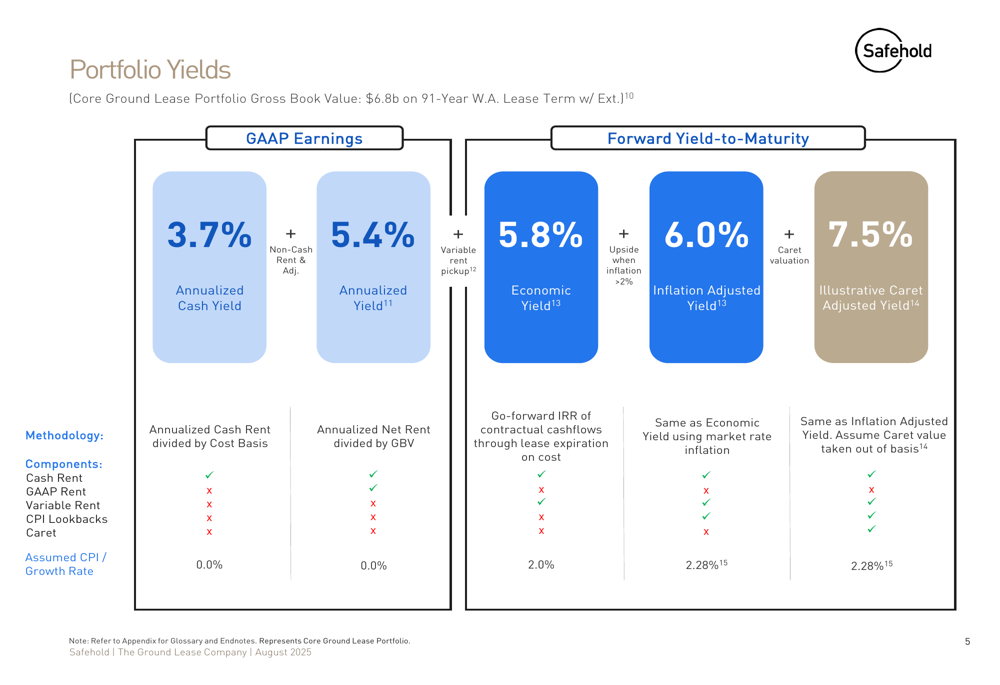

Yield Structure and Investment Returns

Safehold’s core ground lease portfolio, valued at $6.8 billion with a weighted average lease term of 91 years including extensions, generates multiple layers of returns for investors. The company’s yield structure is designed to provide both current income and long-term appreciation.

The following chart breaks down Safehold’s portfolio yields:

The portfolio generates an annualized cash yield of 3.7%, which increases to 5.4% on a GAAP basis. When considering forward yield-to-maturity metrics, the economic yield rises to 5.8%, with inflation adjustments pushing it to 6.0%. Including the potential value of Caret (Safehold’s structure for capturing ground lease appreciation), the illustrative yield reaches 7.5%.

Forward-Looking Statements

Looking ahead, Safehold appears well-positioned to continue its portfolio expansion with substantial liquidity and a diversified investment approach. The company’s strategic focus on multifamily assets provides stability, while its growing presence in life science properties (6% of GBV) offers exposure to a high-growth sector.

The resumption of origination activity in Q2 2025 suggests improving market conditions after a challenging first quarter. With $1.2 billion in available capital and strong credit ratings, Safehold has the financial flexibility to capitalize on attractive ground lease opportunities as they arise.

However, investors should note the continued pressure on earnings due to higher credit loss provisions and the potential impact of interest rate volatility on the company’s cost of capital. While Safehold’s long-term business model remains sound, near-term financial performance may continue to face headwinds as the real estate market adjusts to changing economic conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.