Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

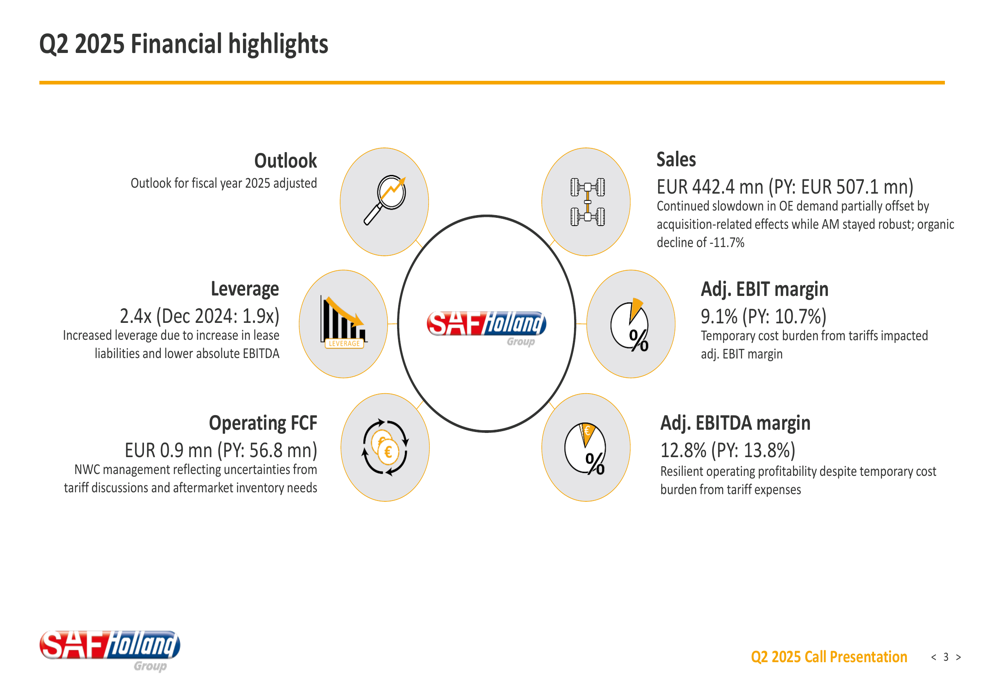

SAF-Holland SE (ETR:SFQ) presented its Q2 2025 financial results on August 7, 2025, revealing continued pressure on both revenue and profitability amid challenging market conditions and trade policy uncertainties. The commercial vehicle component supplier reported sales of €442.4 million, down from €507.1 million in the same period last year, representing an organic decline of 11.7%. The company’s stock closed at €15.66, showing a modest 0.26% increase on the day of the presentation.

The quarter was marked by subdued demand across commercial vehicle markets, particularly in North America where tariff-related uncertainties have dampened purchasing activity. Despite these headwinds, the company maintained relatively resilient profitability metrics, though at lower levels compared to the previous year.

Quarterly Performance Highlights

SAF-Holland’s Q2 2025 financial performance reflected the challenging market environment, with key metrics showing declines compared to the prior year period. The company’s adjusted EBIT margin contracted to 9.1% from 10.7% in Q2 2024, while the adjusted EBITDA margin fell to 12.8% from 13.8%.

As shown in the following financial highlights summary:

Operating free cash flow declined dramatically to €0.9 million compared to €56.8 million in the same quarter last year, primarily due to working capital management challenges related to tariff uncertainties and aftermarket inventory needs. The company’s leverage ratio increased to 2.4x from 1.9x at the end of December 2024, reflecting both increased lease liabilities and lower absolute EBITDA.

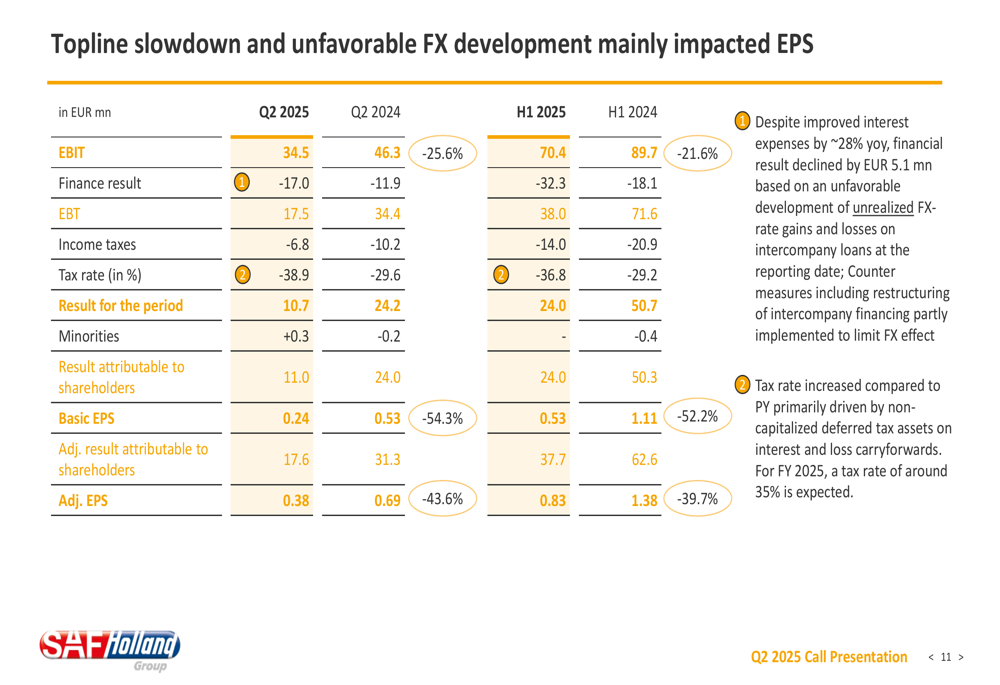

Basic earnings per share fell to €0.24 from €0.53 in Q2 2024, while adjusted EPS declined to €0.38 from €0.69. The financial result was negatively impacted by unfavorable development of unrealized foreign exchange rate effects, as illustrated in this detailed breakdown:

Regional Analysis

SAF-Holland’s performance varied significantly across its three main regions, with each facing distinct challenges and opportunities.

EMEA Region

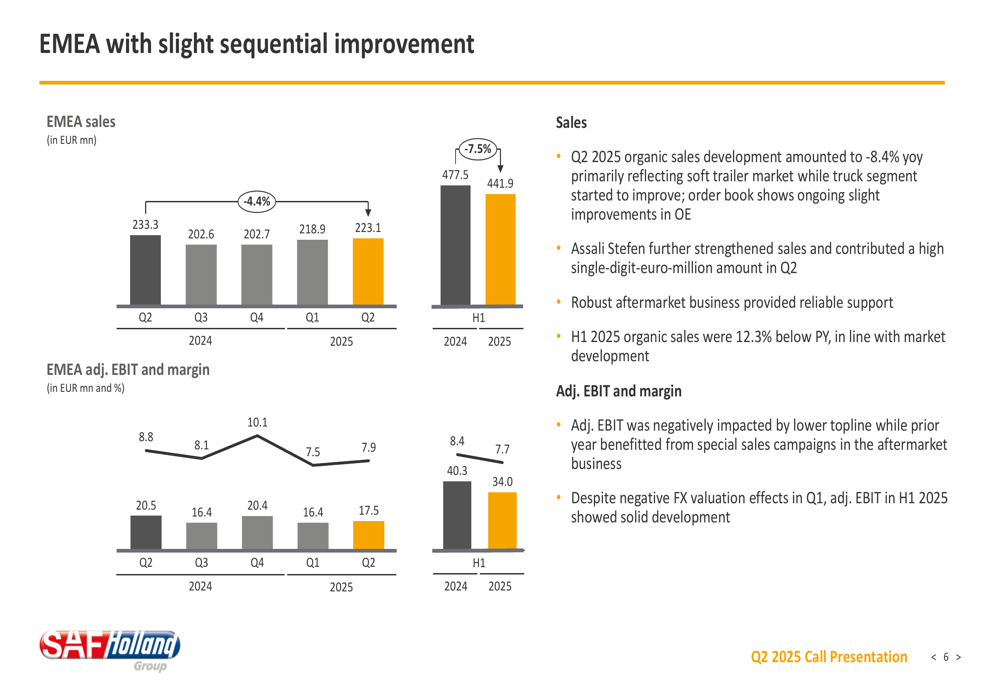

The EMEA region showed slight sequential improvement with sales of €223.1 million in Q2 2025, though still below the €233.3 million recorded in Q2 2024. The organic sales development was -8.4% year-over-year, primarily reflecting a soft trailer market, while the truck segment started to show improvement. The acquisition of Assali Stefen contributed positively to the region’s results.

Americas Region

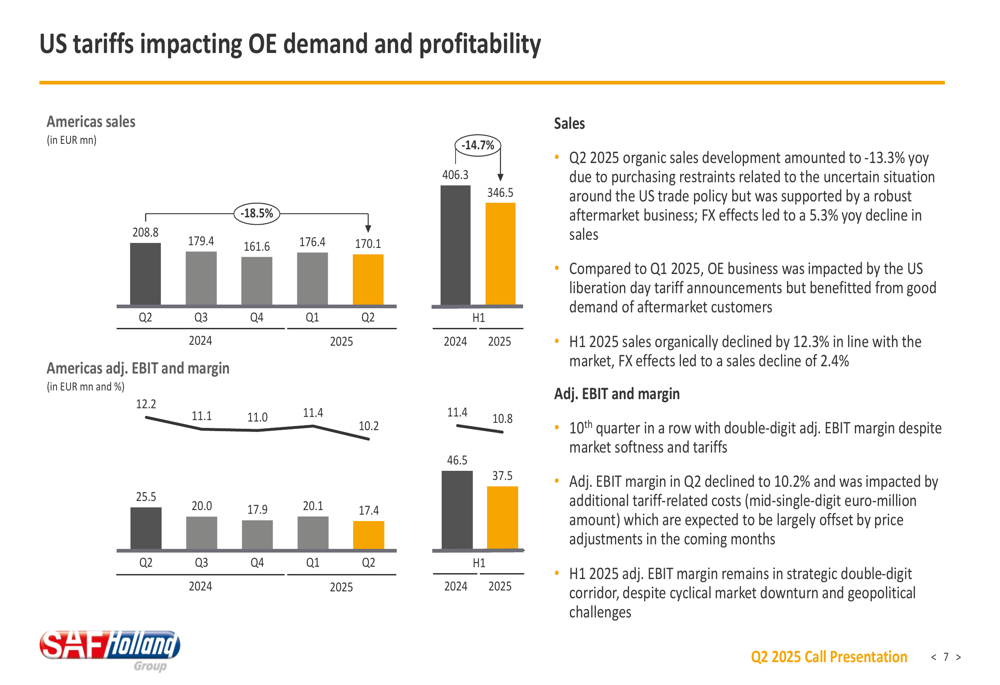

The Americas region was particularly impacted by US tariffs, with sales declining to €170.1 million from €208.8 million in Q2 2024. Organic sales development amounted to -13.3% year-over-year, largely due to purchasing restraints related to uncertainties surrounding US trade policy. These factors also pressured profitability in the region.

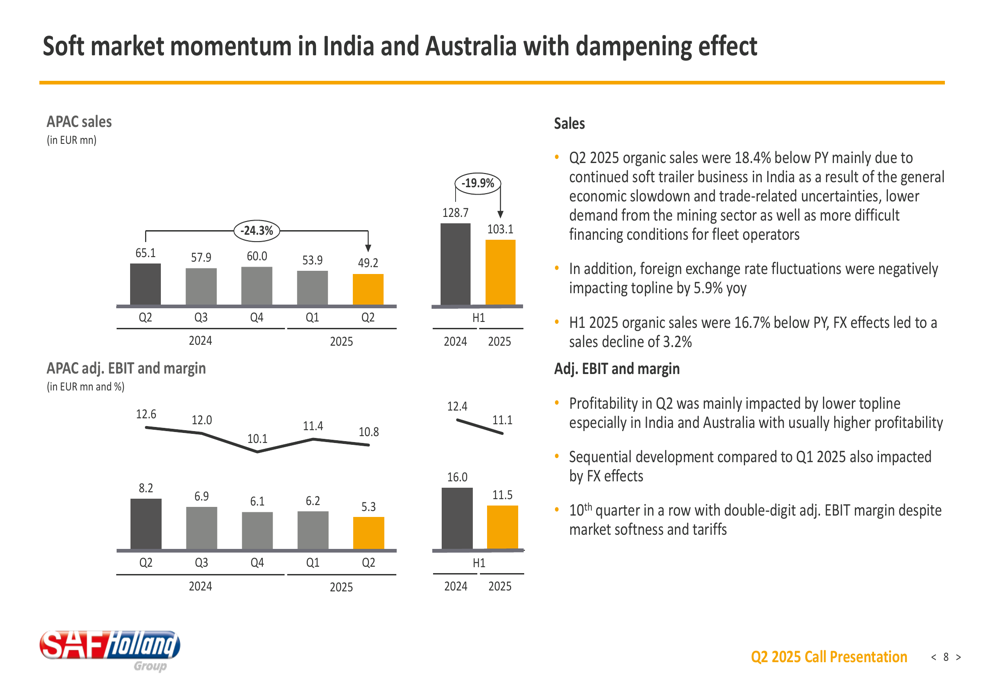

APAC Region

The APAC region faced the steepest decline, with sales falling to €49.2 million from €65.1 million in Q2 2024. Organic sales were 18.4% below the previous year, mainly due to continued soft trailer business in India and challenging market conditions in Australia.

The company’s sales mix by region and customer segment has shifted notably, with APAC increasing its share of total sales to 50.5% in Q2 2025 from 41.2% in Q2 2024, while EMEA’s share declined to 38.4% from 46.0%.

Tariff and Currency Impacts

A significant factor affecting SAF-Holland’s performance has been the impact of tariffs and currency effects. The company noted that tariff-related costs created a temporary burden on profitability, particularly in the Americas region.

Currency effects also played a major role in the company’s financial results. Despite improved interest expenses, the financial result declined based on unfavorable development of unrealized foreign exchange rate gains and losses. In response, SAF-Holland announced an adjustment to its dividend calculation method to account for these unrealized exchange rate changes.

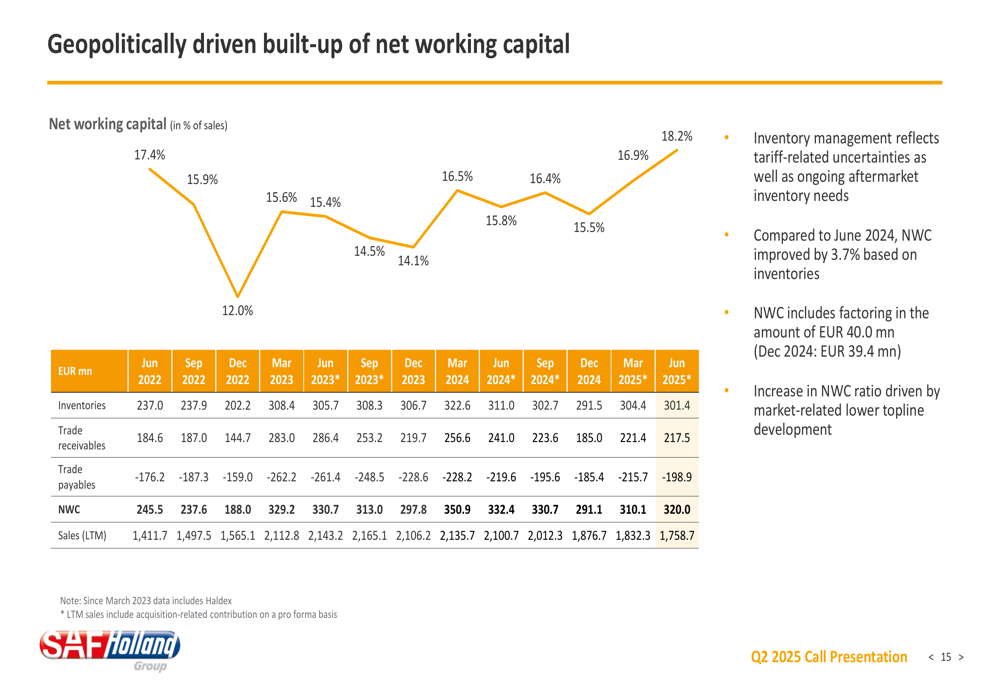

The company has also been managing its working capital carefully in response to geopolitical uncertainties, as illustrated in this analysis of net working capital development:

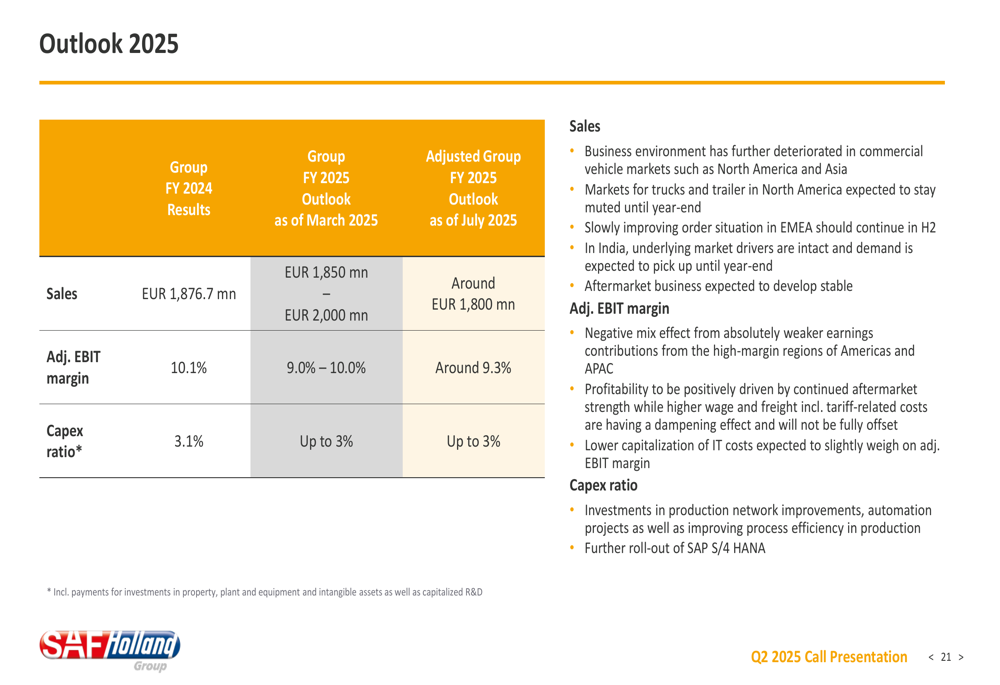

Outlook & Guidance

In light of the challenging business environment, SAF-Holland has adjusted its outlook for fiscal year 2025. The company now expects group sales between €1.85 billion and €2.0 billion, with an adjusted EBIT margin between 9-10%.

The revised outlook reflects further deterioration in commercial vehicle markets, particularly in North America and Asia, as shown in this market outlook summary:

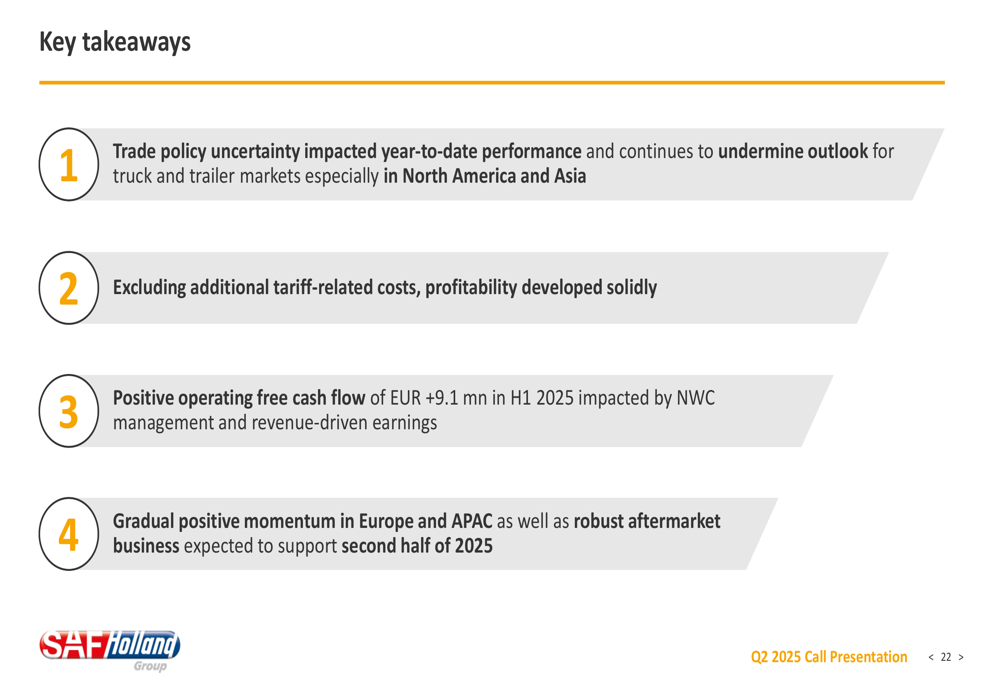

Despite these challenges, the company highlighted several positive developments, including gradual positive momentum in Europe and APAC, and a positive operating free cash flow of €9.1 million in the first half of 2025.

Strategic Initiatives

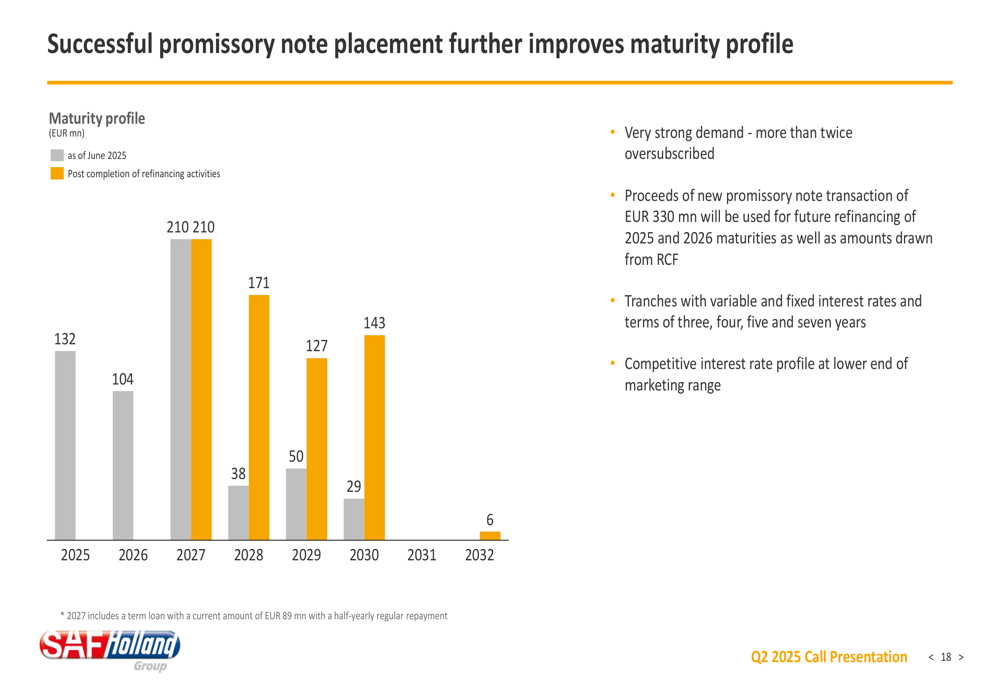

SAF-Holland has undertaken several strategic initiatives to strengthen its financial position amid market uncertainties. The company successfully placed a promissory note that improves its debt maturity profile, with strong demand resulting in the offering being more than twice oversubscribed.

The company also highlighted its focus on managing net working capital effectively, though this has been complicated by the need to maintain adequate inventory levels due to tariff-related uncertainties and aftermarket needs.

In its key takeaways, SAF-Holland emphasized that excluding additional tariff-related costs, its underlying profitability remained solid, and that it is seeing gradual positive momentum in Europe and APAC markets that could support improved performance in the coming quarters.

Looking ahead, SAF-Holland will need to navigate continued trade policy uncertainties while managing costs and working capital effectively to maintain profitability in a challenging market environment. The company’s ability to leverage its strong aftermarket business and regional diversification will be key factors in its performance for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.