HK-listed gold stocks jump as US economic fears boost bullion prices

Introduction & Market Context

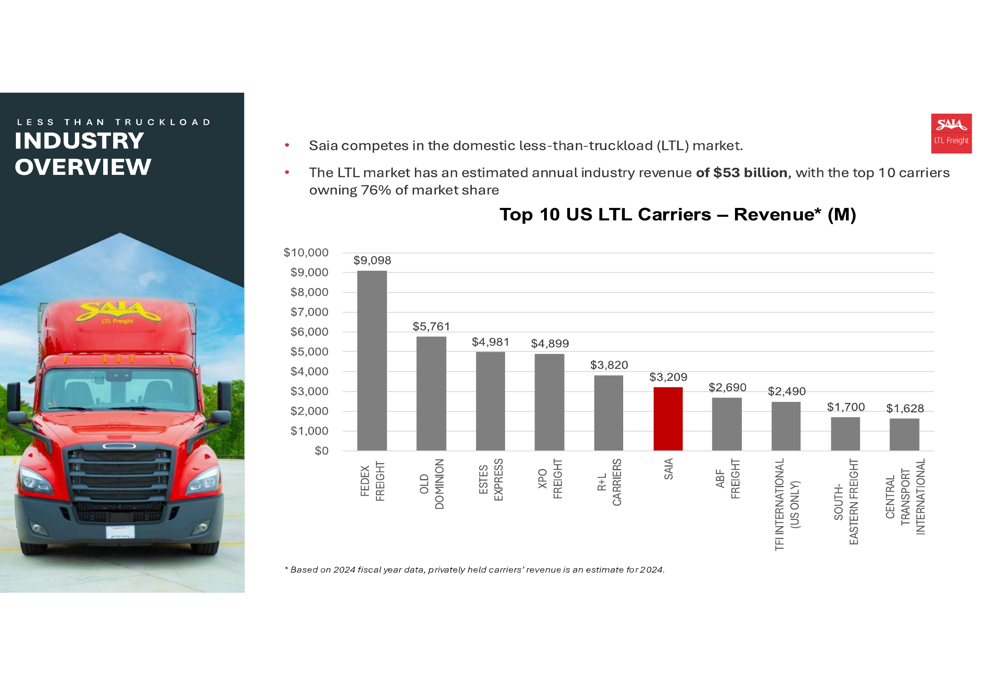

Saia Inc. (NASDAQ:SAIA) recently shared its Q2 2025 investor presentation, revealing a company balancing short-term performance pressures against an ambitious long-term growth strategy. The less-than-truckload (LTL) carrier operates in a $53 billion domestic market where the top 10 carriers control 76% of revenue, with Saia ranking as the sixth-largest player with annual revenue of $3.2 billion.

Despite challenging year-over-year comparisons, Saia’s Q2 results exceeded analyst expectations with earnings per share of $2.67 versus the forecasted $2.41, though this still represented a 30.3% decline from the same period last year. The company’s stock responded positively to the earnings beat, rising 7% in regular trading and an additional 13.26% in aftermarket trading.

As shown in the following competitive landscape chart, Saia continues to strengthen its position among the industry leaders:

Quarterly Performance Highlights

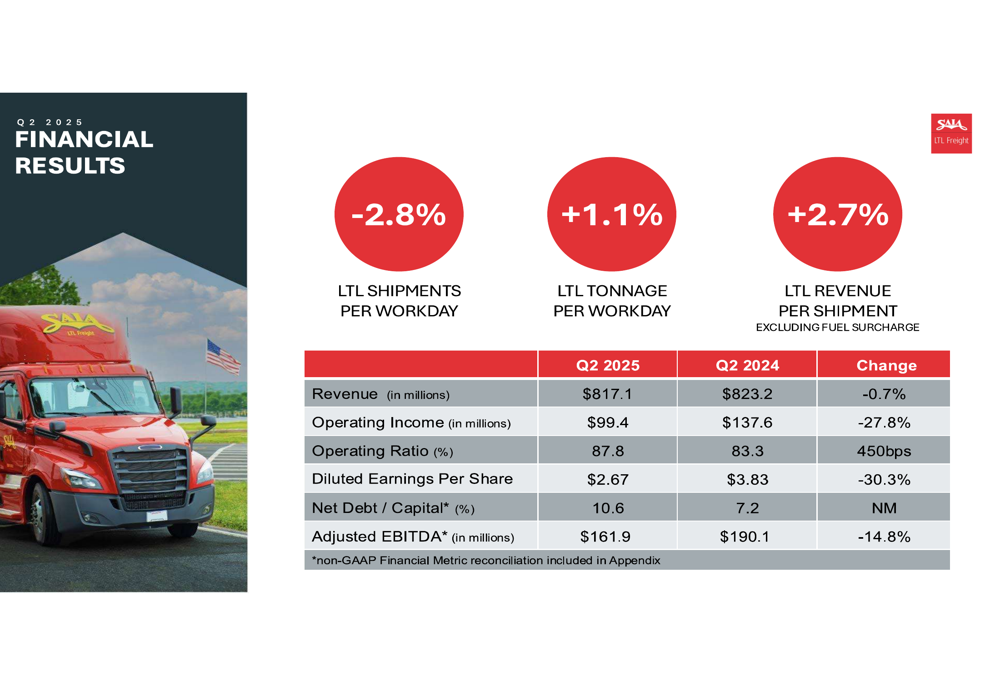

Saia’s Q2 2025 financial results revealed mixed performance metrics. Revenue declined slightly to $817.1 million, down 0.7% from $823.2 million in Q2 2024. More significantly, operating income fell 27.8% to $99.4 million, with the operating ratio deteriorating by 450 basis points to 87.8%. Earnings per share dropped 30.3% year-over-year from $3.83 to $2.67.

Despite these declines, CEO Fritz Hulscrief emphasized during the earnings call that the company remains "steadfast in our approach to providing industry-leading service levels while managing controllable costs and productivity."

The comprehensive financial results comparison is illustrated below:

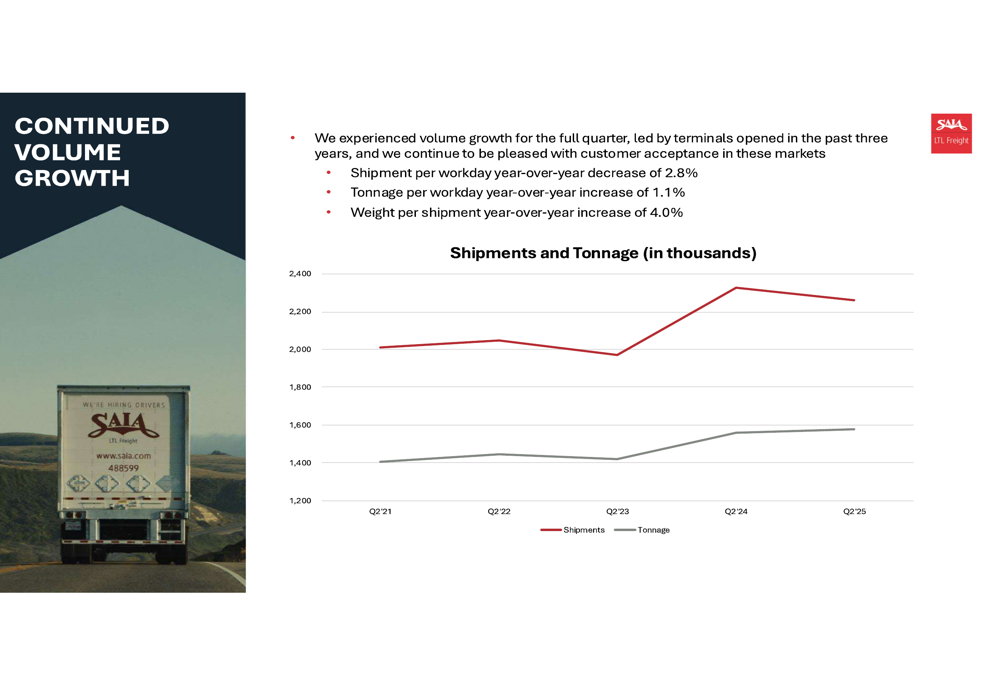

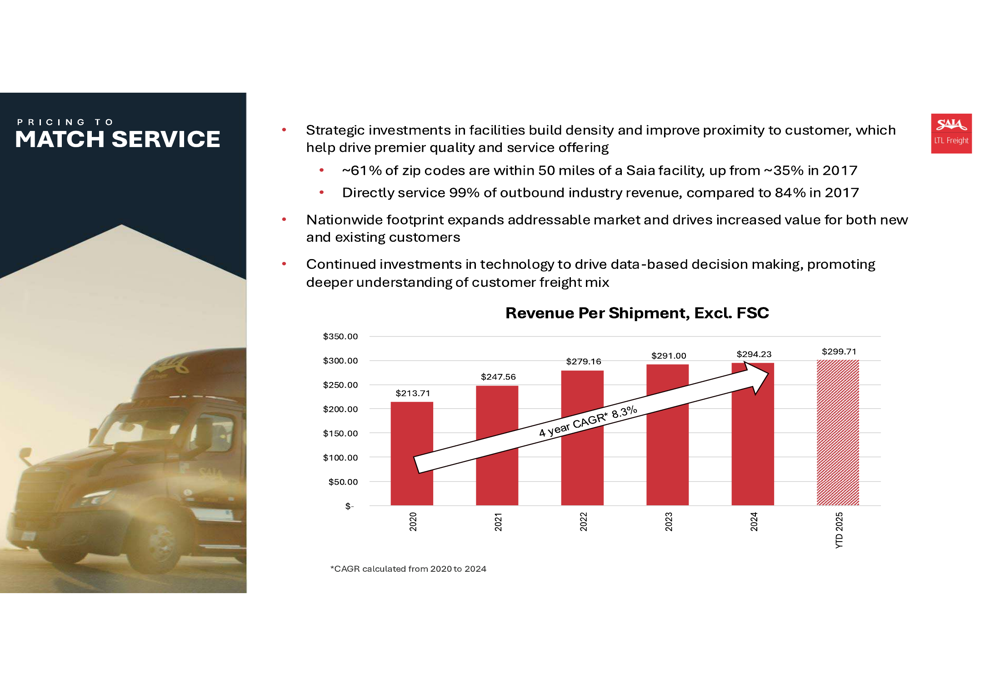

Operational metrics showed mixed trends as well. Shipments per workday decreased by 2.8% year-over-year, while tonnage per workday increased by 1.1%, indicating a shift toward heavier shipments. This was confirmed by the 4.0% increase in weight per shipment. Revenue per shipment, excluding fuel surcharge, grew by 2.7%, demonstrating the company’s continued pricing discipline.

The following chart illustrates the recent volume trends:

Strategic Growth Initiatives

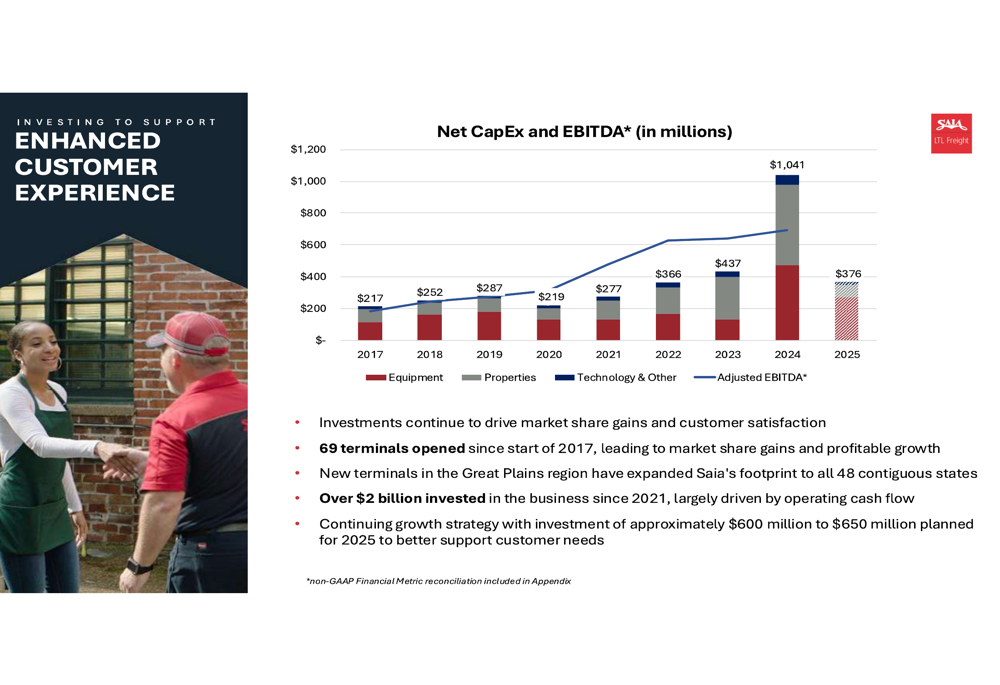

A central theme of Saia’s presentation was its continued investment in network expansion. The company has opened 69 terminals since the start of 2017, expanding its footprint to all 48 contiguous states. This expansion has significantly improved customer proximity, with approximately 61% of zip codes now within 50 miles of a Saia facility, up from 35% in 2017.

Saia has invested over $2 billion in the business since 2021 and plans to invest an additional $600-650 million in 2025. These investments are primarily focused on enhancing terminal capacity, upgrading equipment, and improving technology infrastructure.

The company’s capital expenditure and EBITDA trends are shown in the following chart:

This expansion strategy has yielded tangible service improvements. Approximately 60% of shipments are delivered within 48 hours, with an average length of haul of 893 miles. The Q2 2025 cargo claims ratio stood at 0.51%, reflecting the company’s commitment to service quality.

Saia’s pricing strategy aligns with its service quality improvements, as demonstrated by the consistent growth in revenue per shipment:

Competitive Industry Position

Saia serves a diverse customer base with no single customer representing more than 5% of sales. Its client roster includes major corporations such as Walmart (NYSE:WMT), Home Depot (NYSE:HD), Dell (NYSE:DELL), Starbucks (NASDAQ:SBUX), and Sherwin-Williams (NYSE:SHW), providing stability and growth opportunities across various sectors.

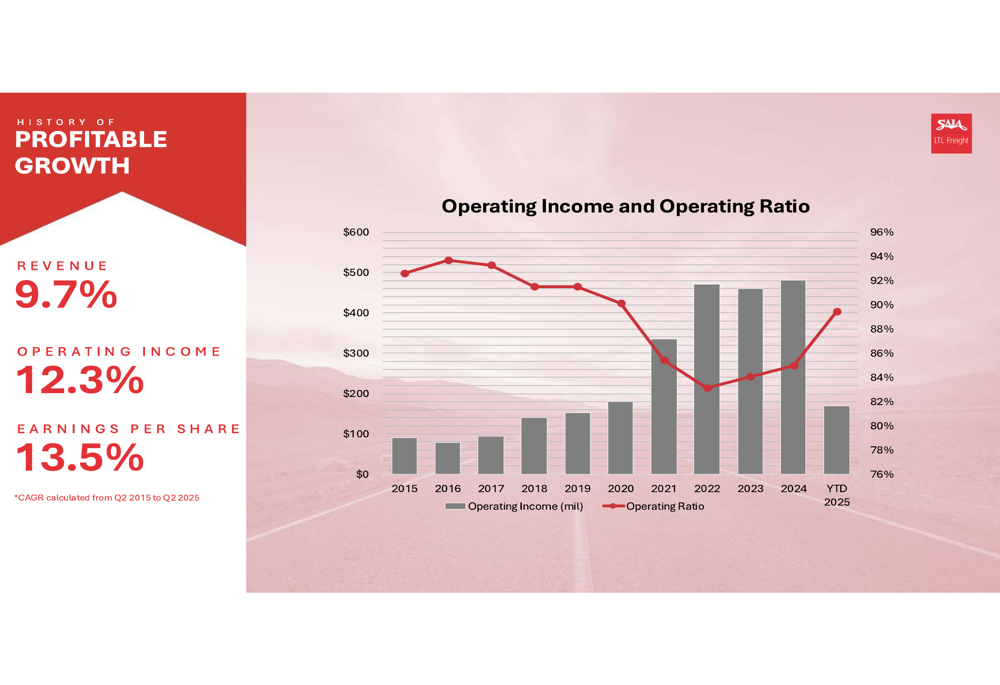

The company positions itself as offering premium service at competitive prices, targeting the "superior offering" quadrant in its customer satisfaction framework. This strategy has enabled Saia to achieve a 10-year revenue CAGR of 9.7% and an EPS CAGR of 13.5% from Q2 2015 to Q2 2025.

The long-term growth trajectory is illustrated in the following chart:

Financial Position and Outlook

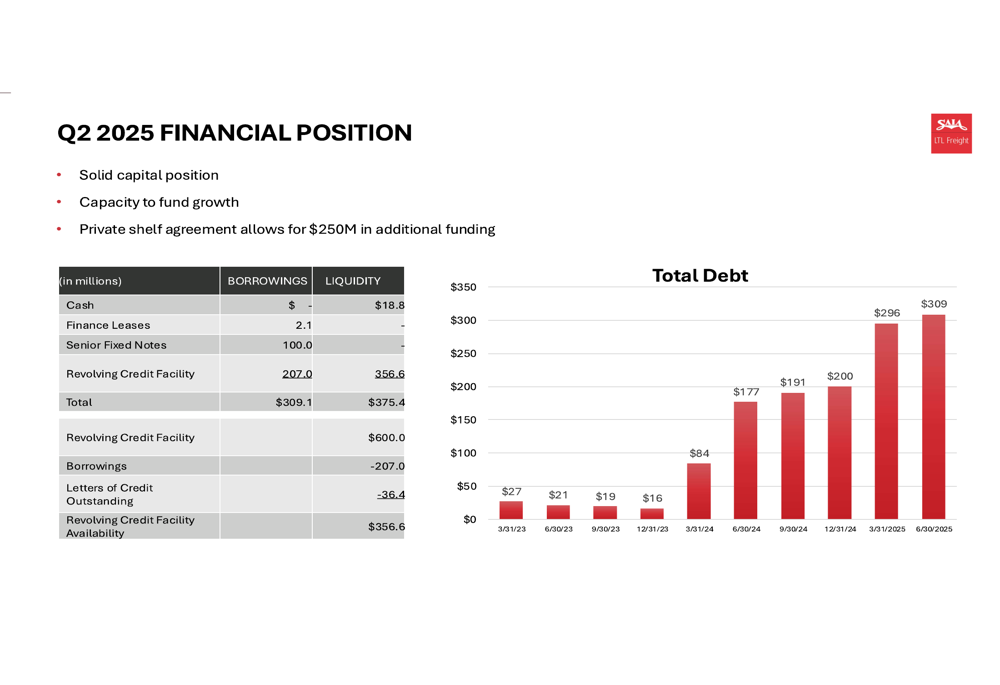

Saia’s financial position has evolved significantly as it funds its growth initiatives. Total (EPA:TTEF) debt has increased from $21 million in Q2 2023 to $309 million in Q2 2025, while the net debt to capital ratio rose to 10.6% from 7.2% a year ago. Despite this increase, the company maintains substantial liquidity with $375.4 million available.

The debt progression is shown in the following chart:

Looking forward, Saia anticipates a slight degradation in its operating ratio by approximately 100 basis points in Q3 2025. Management noted during the earnings call that July volumes were flat and that Q3 comparisons would be challenging due to recent terminal openings.

Despite these near-term challenges, management remains optimistic about long-term prospects. As CEO Hulscrief stated during the earnings call, "We’re in the early innings of tapping the potential of this business."

Saia’s investment thesis centers on its unique position as a century-old company with above-market growth potential, ongoing pricing improvement opportunities, and significant operating leverage. The company estimates that each 100 basis point improvement in operating margin would result in $0.91 of additional earnings per share.

As Saia continues to navigate a challenging freight environment, investors will be watching closely to see if the company’s substantial investments translate into improved financial performance in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.