Raymond James initiates QXO stock with Outperform rating on acquisition strategy

Introduction & Market Context

Science Applications International Corp (NYSE:SAIC) released its second-quarter fiscal year 2026 financial results on September 4, 2025, revealing a mixed performance that prompted a downward revision in revenue guidance while simultaneously raising earnings per share expectations. The government technology services provider’s stock dropped 3% in premarket trading to $110.69, reflecting investor concerns about the revenue outlook despite improved profitability metrics.

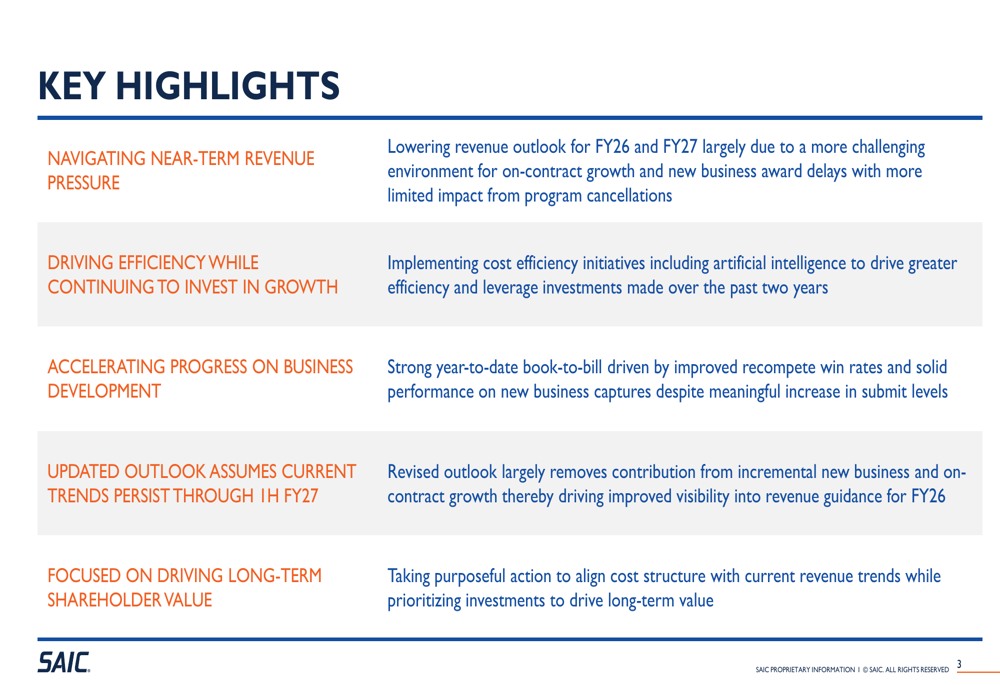

The company’s presentation highlighted ongoing challenges in the federal contracting environment, including program cancellations and award delays that are pressuring near-term revenue growth. However, SAIC emphasized its focus on operational efficiency and strategic cost management to maintain profitability despite these headwinds.

Quarterly Performance Highlights

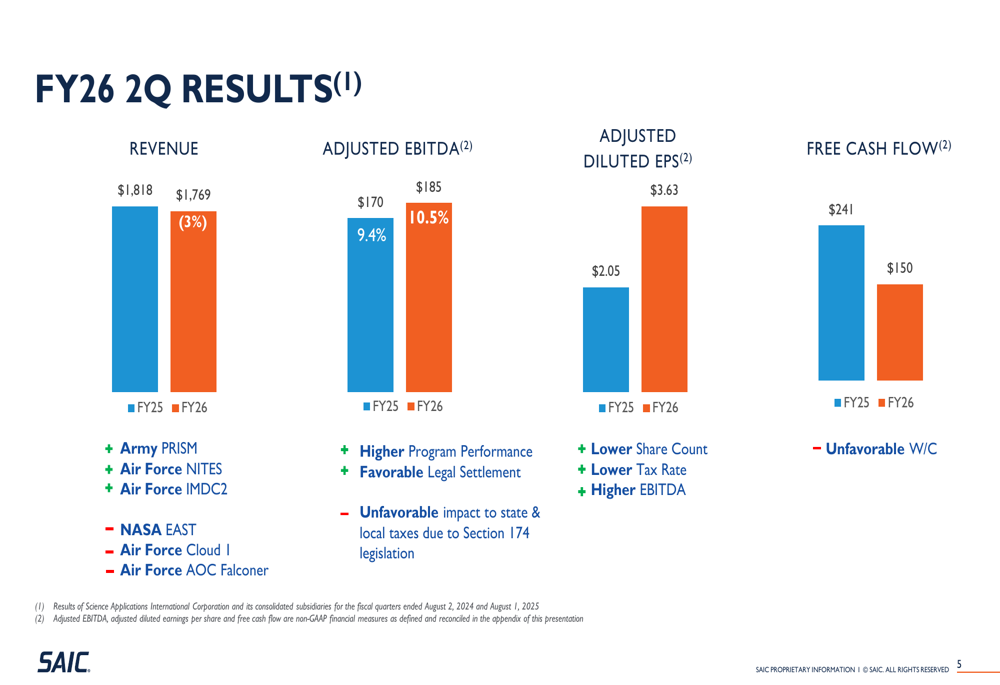

SAIC reported second-quarter revenue of $1,769 million, representing a 3% decrease compared to $1,818 million in the same period last year. Despite this revenue decline, the company achieved significant improvements in profitability metrics.

As shown in the following quarterly results summary:

Adjusted EBITDA increased to $185 million from $170 million in the prior year, with the margin expanding to 10.5% from 9.4%. This improvement reflects the company’s success in enhancing operational efficiency despite revenue challenges. Adjusted diluted earnings per share saw a substantial increase to $3.63 from $2.05 in the prior-year quarter, benefiting from higher EBITDA, a lower share count due to ongoing repurchases, and a favorable tax rate.

Free cash flow for the quarter was $150 million, down from $241 million in the same period last year, primarily due to unfavorable working capital movements. The company identified several positive and negative factors affecting quarterly performance, with programs like Army PRISM and Air Force NITES providing positive contributions, while NASA EAST and Air Force Cloud I represented headwinds.

Guidance Revision

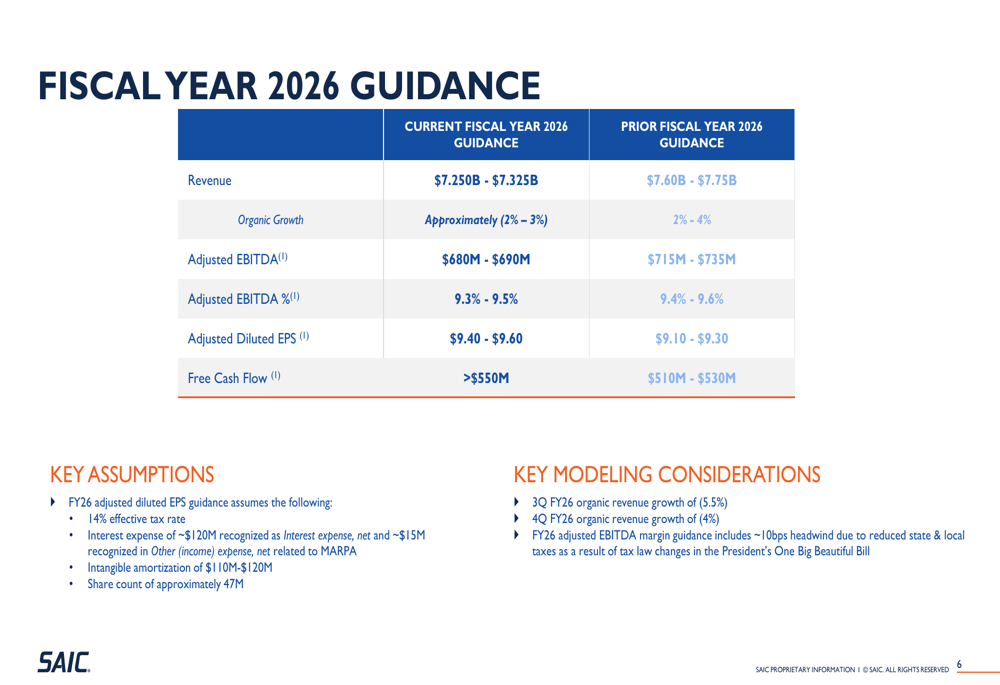

A central theme of SAIC’s presentation was the significant revision to its fiscal year 2026 guidance, with revenue expectations lowered but EPS and free cash flow projections increased.

The updated guidance comparison reveals substantial changes across key metrics:

SAIC lowered its revenue guidance for fiscal 2026 to $7.250-$7.325 billion from the previous range of $7.60-$7.75 billion. Organic growth expectations shifted dramatically from positive 2-4% to negative 2-3%, reflecting the challenging federal contracting environment. Despite the revenue reduction, the company raised its adjusted diluted EPS guidance to $9.40-$9.60 from $9.10-$9.30 and increased its free cash flow projection to over $550 million from the previous range of $510-$530 million.

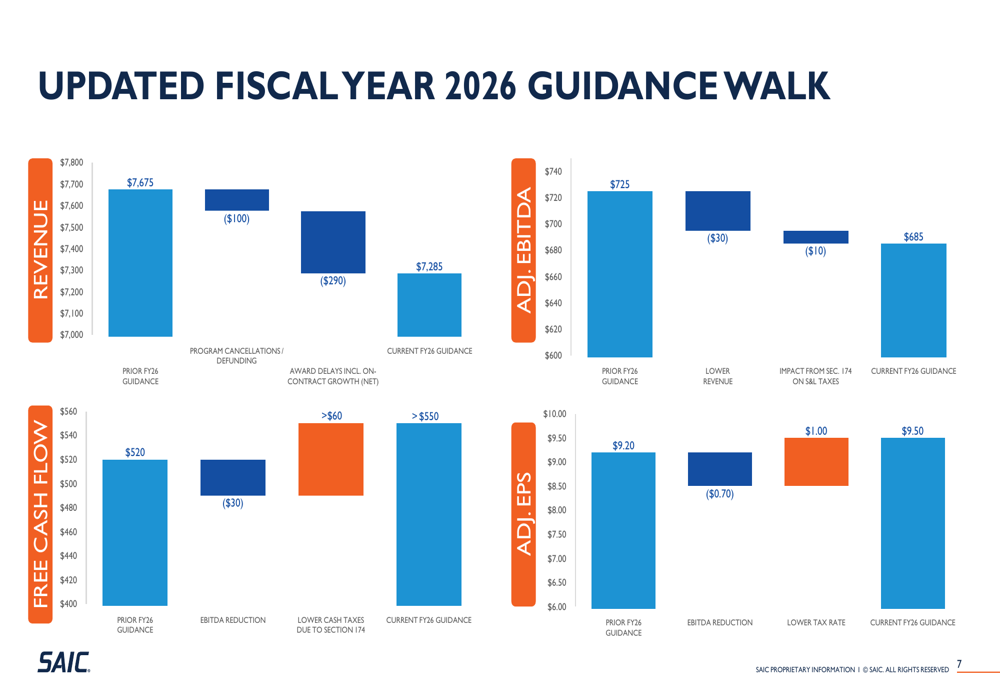

The company provided a detailed walkdown of the factors driving these guidance changes:

The presentation attributes approximately $100 million of the revenue reduction to program cancellations and defunding, with a much larger $290 million impact from award delays. These factors combined to reduce the revenue guidance by nearly $400 million. Despite this significant revenue headwind, the adjusted EPS guidance actually increased, benefiting from a lower tax rate that offset the negative impact of reduced EBITDA.

Business Development Progress

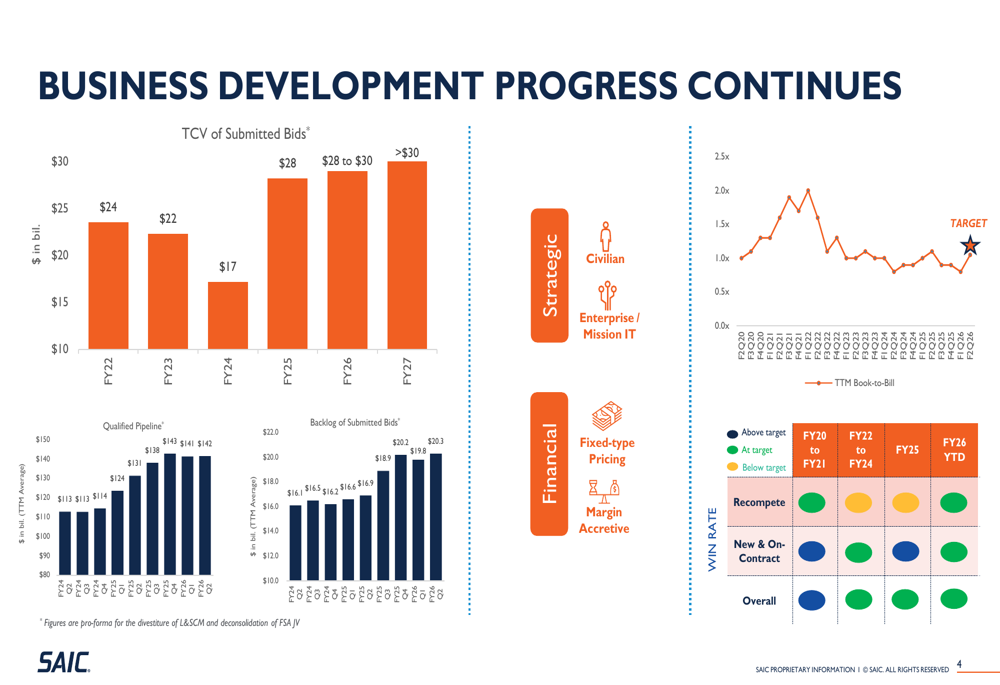

Despite the near-term revenue challenges, SAIC emphasized continued progress in business development activities, highlighting growth in both its qualified pipeline and backlog of submitted bids.

The company’s business development metrics show encouraging trends:

The qualified pipeline reached $22.0 billion in Q2 FY26, continuing a steady growth trend from $20.3 billion in Q1 FY26 and $18.9 billion in Q2 FY25. Similarly, the backlog of submitted bids increased to $150 billion, up from $143 billion in the previous quarter and $138 billion a year ago.

Win rates present a mixed picture, with recompete wins at target levels (yellow indicator) but new and on-contract business below target (red indicator). The time-to-market book-to-bill ratio remains above the 1x target, suggesting continued momentum in contract awards relative to revenue recognition.

Strategic Initiatives

SAIC outlined several strategic initiatives aimed at navigating the current challenging environment while positioning for long-term growth. The company is implementing cost efficiency measures, including leveraging artificial intelligence to drive greater operational efficiency while continuing to invest in growth opportunities.

The key strategic highlights emphasize this balanced approach:

The presentation acknowledges near-term revenue pressure but frames it primarily as a timing issue related to award delays rather than a fundamental deterioration in market opportunity. Management emphasized their focus on driving long-term shareholder value through purposeful action to align the cost structure with current revenue trends while prioritizing investments that support future growth.

Long-term Financial Outlook

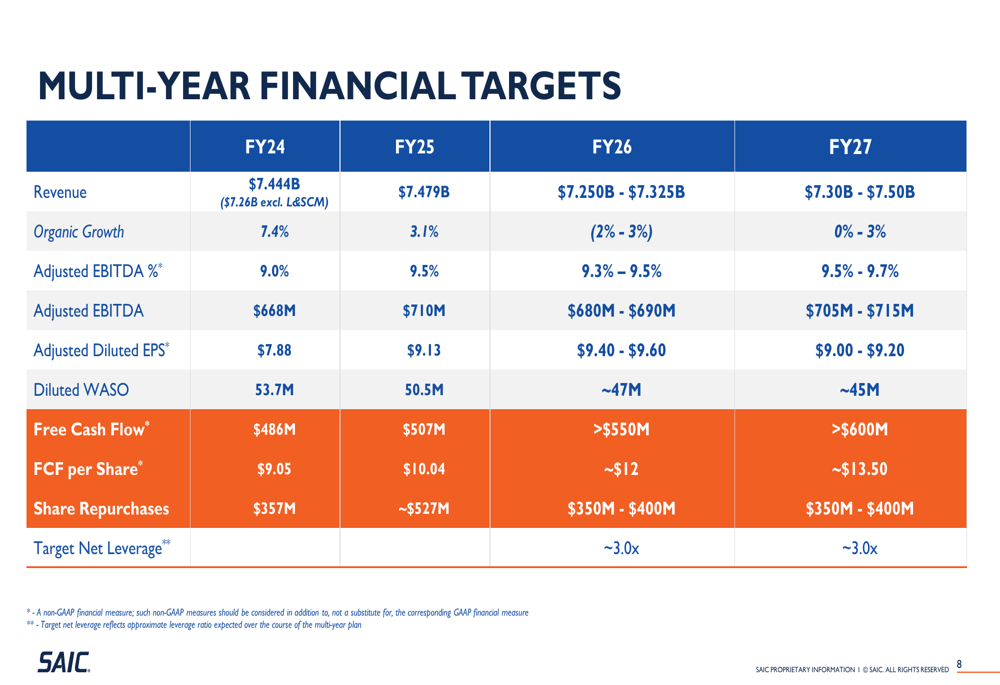

Looking beyond the current fiscal year, SAIC provided multi-year financial targets that suggest a return to growth in fiscal 2027 after the current year’s contraction.

The company’s multi-year financial projections show the following trajectory:

For fiscal 2027, SAIC projects revenue of $7.30-$7.50 billion, representing organic growth of 0-3% after the expected contraction in fiscal 2026. Adjusted EBITDA margin is forecast to improve to 9.5-9.7% from 9.3-9.5% in the current year. The company expects adjusted diluted EPS of $9.00-$9.20, slightly below the fiscal 2026 projection due to a higher tax rate assumption.

Free cash flow is projected to exceed $600 million in fiscal 2027, with free cash flow per share reaching approximately $13.50, benefiting from both improved operational performance and continued share repurchases. The company plans to maintain its share repurchase program at $350-400 million annually and targets a net leverage ratio of approximately 3.0x.

Historical Performance Context

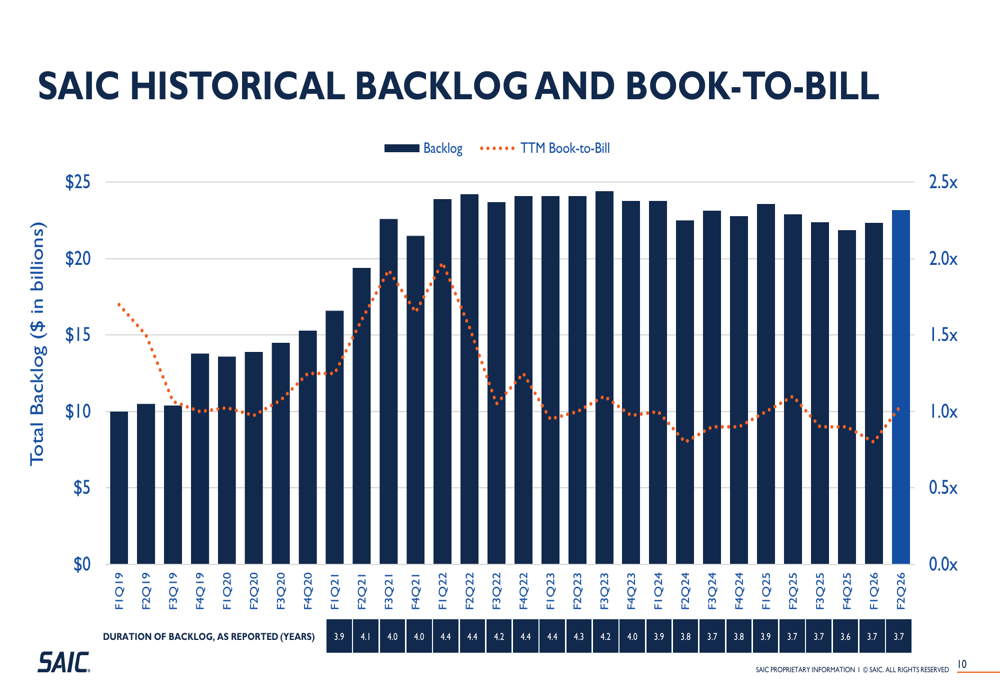

SAIC’s presentation included historical data on backlog and book-to-bill ratio, providing context for the company’s current performance relative to longer-term trends.

The historical backlog and book-to-bill chart shows consistent growth:

The company has maintained a book-to-bill ratio above 1.0x for most of the period shown, contributing to steady backlog growth. This historical perspective suggests that the current revenue challenges may be temporary, with the growing backlog potentially supporting a return to growth in future periods.

Conclusion

SAIC’s second-quarter fiscal 2026 results and updated guidance reflect a company navigating near-term revenue headwinds through operational efficiency and cost management. While the lowered revenue outlook prompted a negative market reaction, the improved profitability metrics and raised EPS guidance suggest management is effectively executing on factors within its control.

The company’s focus on business development appears to be yielding results in terms of pipeline and backlog growth, though challenges remain in winning new business. With a continued commitment to shareholder returns through substantial share repurchases and a strategy that balances cost efficiency with targeted investments, SAIC is positioning itself to weather the current challenging environment while maintaining its long-term growth trajectory.

Investors will likely focus on whether the company can execute on its efficiency initiatives while successfully converting its growing pipeline into revenue-generating contracts in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.