Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

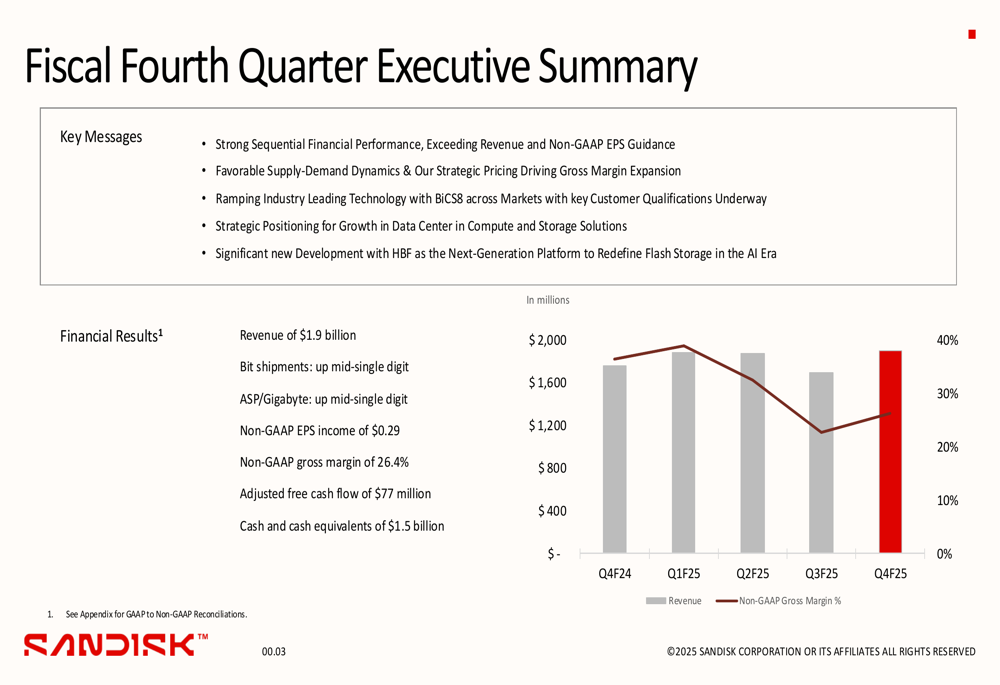

SanDisk Corporation (NASDAQ:SNDK) released its fiscal fourth quarter 2025 financial results on August 14, 2025, showcasing a significant sequential improvement across key metrics. The company reported revenue of $1.9 billion for the quarter ended June 27, 2025, exceeding its previous guidance and marking a recovery from challenges faced earlier in the fiscal year.

The results come amid favorable supply-demand dynamics in the memory market and growing demand for storage solutions in AI-driven workloads. SanDisk highlighted that hyperscaler capital expenditure grew 47% year-over-year to $368 billion, creating substantial opportunities for its flash memory products.

Quarterly Performance Highlights

SanDisk reported Q4 2025 revenue of $1.9 billion, representing a 12% sequential increase and an 8% year-over-year improvement. The company’s non-GAAP earnings per share reached $0.29, a dramatic 197% increase from the previous quarter when the company posted a loss of $0.30 per share. However, EPS remained 77% lower compared to the same quarter last year.

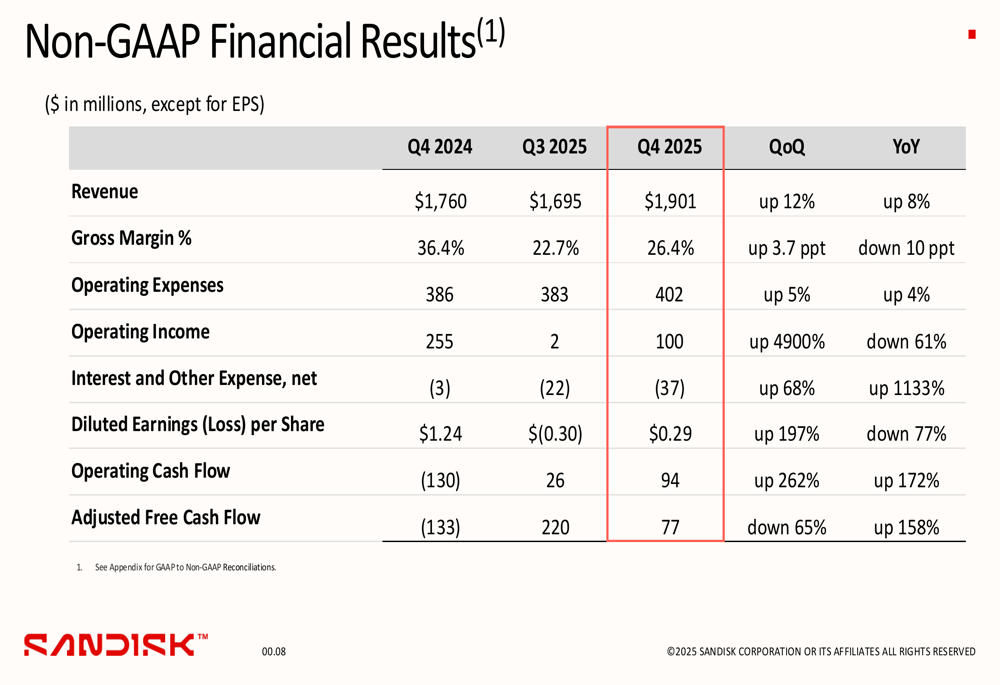

As shown in the following financial summary:

Non-GAAP gross margin improved to 26.4%, up 3.7 percentage points sequentially but down 10 percentage points year-over-year. The company generated adjusted free cash flow of $77 million and maintained a strong balance sheet with $1.5 billion in cash and cash equivalents.

The comprehensive financial results table provides additional context for SanDisk’s performance:

SanDisk’s bit shipments increased by mid-single digits during the quarter, while average selling price per gigabyte also rose by mid-single digits, indicating improving market conditions compared to previous quarters.

Segment Analysis

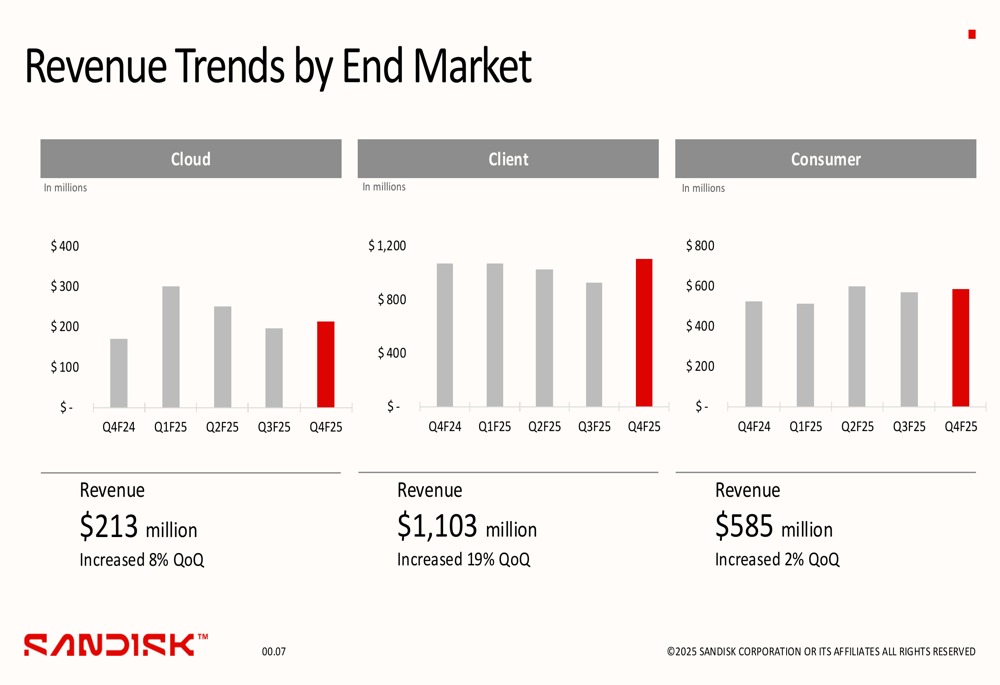

SanDisk’s business spans three key end markets: Cloud, Client, and Consumer. The Client segment was the standout performer in Q4, with revenue of $1.1 billion representing a 19% sequential increase. The Cloud segment grew 8% quarter-over-quarter to $213 million, while the Consumer segment increased 2% to $585 million.

The following chart illustrates revenue trends across all three segments:

In the Cloud segment, SanDisk noted that datacenter represented over 12% of total bits shipped, with clear momentum in AI-driven workloads and hyperscale demand. The company announced a 256 TB NVMe enterprise SSD with UltraQLC platform and is advancing customer qualifications for compute and storage eSSDs.

The Client segment benefited from ongoing uplift from AI-enabled PC demand and smartphone refresh cycles. SanDisk’s BiCS8-based SSDs are now qualified across all major PC OEMs, with additional qualifications underway. The company also expects tailwinds from Windows 10 end of life and post-pandemic refresh cycles in the second half of calendar year 2025.

In the Consumer segment, SanDisk continued to expand its product portfolio with next-generation portable SSDs and high-performance USB drives targeting creators and gamers. The company also highlighted co-branded expansions in gaming with Nintendo microSD Express and Xbox C50 Expansion Card.

Strategic Initiatives

SanDisk’s presentation emphasized its strategic positioning for growth in data centers and AI applications. The company is ramping up industry-leading technology and highlighted a significant new development with HBF (High Bandwidth Flash).

The company’s capital expenditure strategy focuses primarily on supporting BiCS8 technology investments. As illustrated in the presentation, SanDisk’s joint venture with Kioxia continues to be a critical component of its manufacturing strategy, with the partnership covering co-development of process technology and memory design.

SanDisk’s CMOS Bonded Array (CBA) architecture is driving performance and cost advantages in QLC-based SSDs, particularly important for competitive positioning in the client market. The company is also expanding its portfolio into high-performance use cases including automotive-grade storage.

Forward-Looking Statements

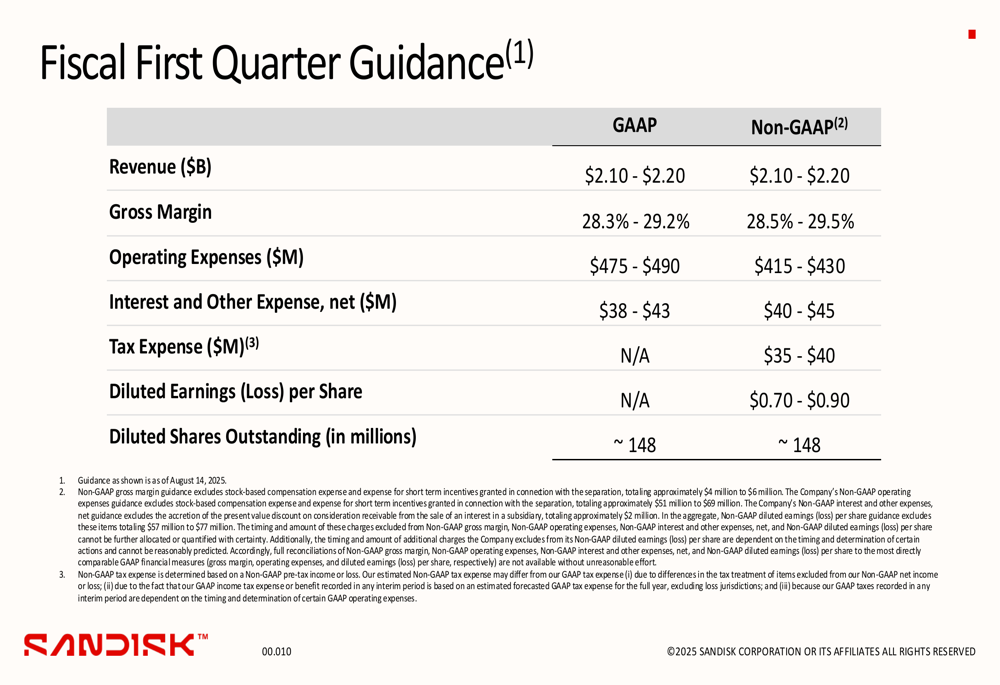

SanDisk provided an optimistic outlook for the first quarter of fiscal 2026, projecting revenue between $2.10 billion and $2.20 billion, which would represent a sequential increase of approximately 10-16%. The company expects non-GAAP gross margin to improve to 28.5-29.5% and forecasts non-GAAP earnings per share between $0.70 and $0.90.

The following guidance table details SanDisk’s expectations for Q1 2026:

This guidance suggests continued improvement in SanDisk’s financial performance, building on the recovery seen in Q4 2025. The company appears well-positioned to benefit from favorable industry dynamics, including strong global cloud infrastructure investment and increasing storage demands driven by AI applications.

SanDisk’s Q4 results and Q1 guidance represent a significant turnaround from the challenges faced in Q3 2025, when the company reported a revenue decline and a non-GAAP loss per share. The sequential improvement across all key metrics suggests that SanDisk’s strategic initiatives and favorable market conditions are beginning to yield positive results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.