Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Sandoz Group AG (SIX:SDZ) presented its first quarter 2025 sales update on April 30, revealing 3% net sales growth in constant currency terms, primarily driven by strong biosimilar performance. The company maintained its full-year guidance despite ongoing pricing pressures and confirmed tariffs in certain markets.

The Swiss generics and biosimilars manufacturer reported that its Q1 performance was "in line with expectations," according to CEO Richard Saynor, with volume growth offsetting anticipated price erosion in key markets.

Quarterly Performance Highlights

Sandoz reported net sales growth of 3% in constant currency and 5% in comparable terms for Q1 2025. The growth was primarily volume-driven, with a 6 percentage point positive impact from volume, offset by a 3 percentage point negative impact from pricing and a 3 percentage point headwind from foreign exchange.

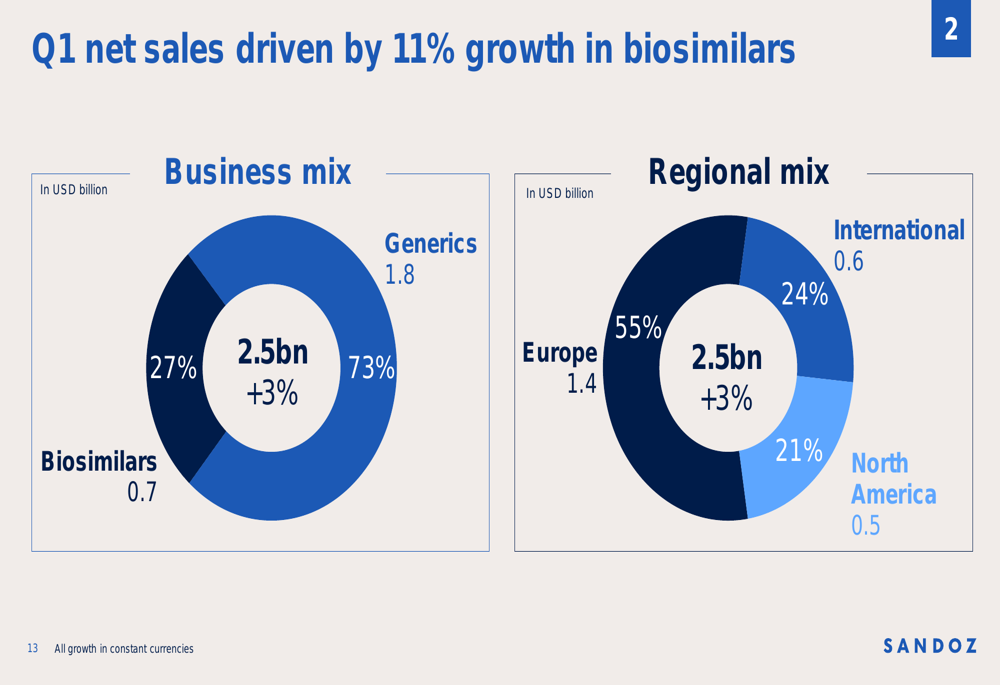

As shown in the following chart detailing the company’s sales breakdown:

Biosimilars now represent 27% of Sandoz’s total sales, while generics account for 73%. From a regional perspective, Europe remains the company’s largest market at 55% of total sales, followed by International markets (24%) and North America (21%).

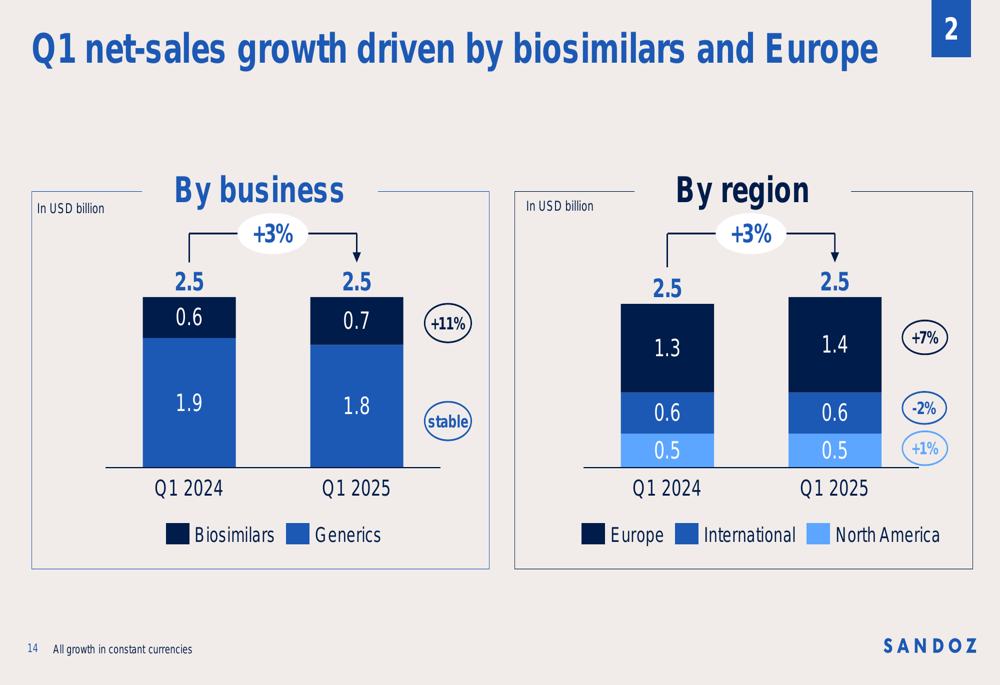

The quarterly performance comparison by business segment and region demonstrates the company’s growing reliance on biosimilars and European markets:

Biosimilars showed impressive growth of 11% year-over-year, increasing from 0.6 billion to 0.7 billion, while generics remained stable at 1.8 billion. Europe led regional performance with 7% growth, while North America showed modest 1% growth and International markets declined by 2%.

Biosimilar Portfolio Performance

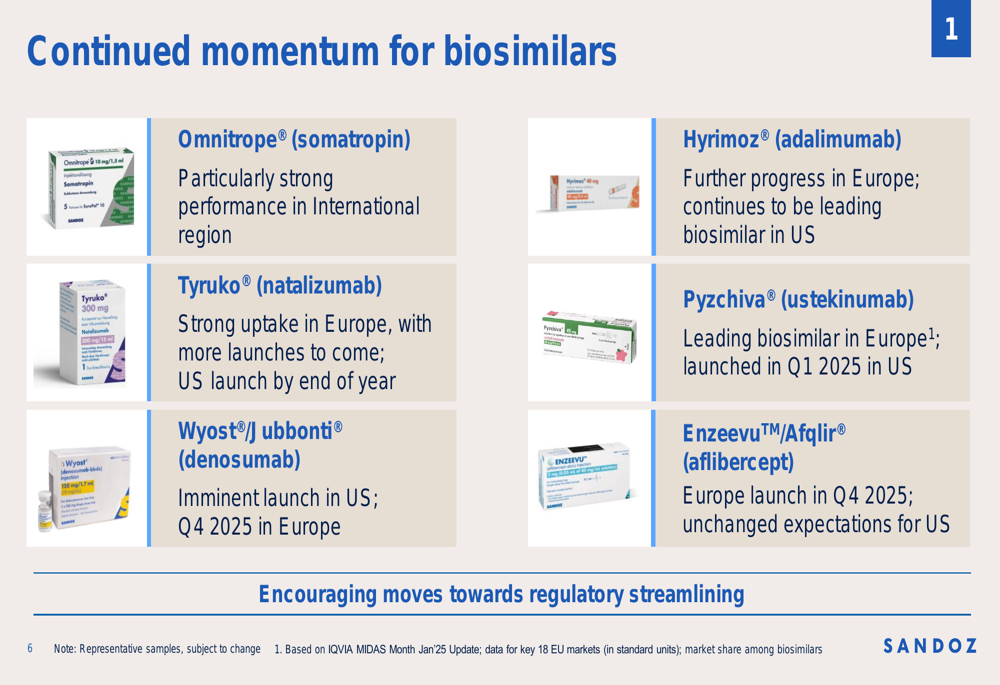

Sandoz highlighted several key biosimilar products driving its performance, with particularly strong results from established and newly launched products.

The company’s comprehensive biosimilar strategy is illustrated in this overview:

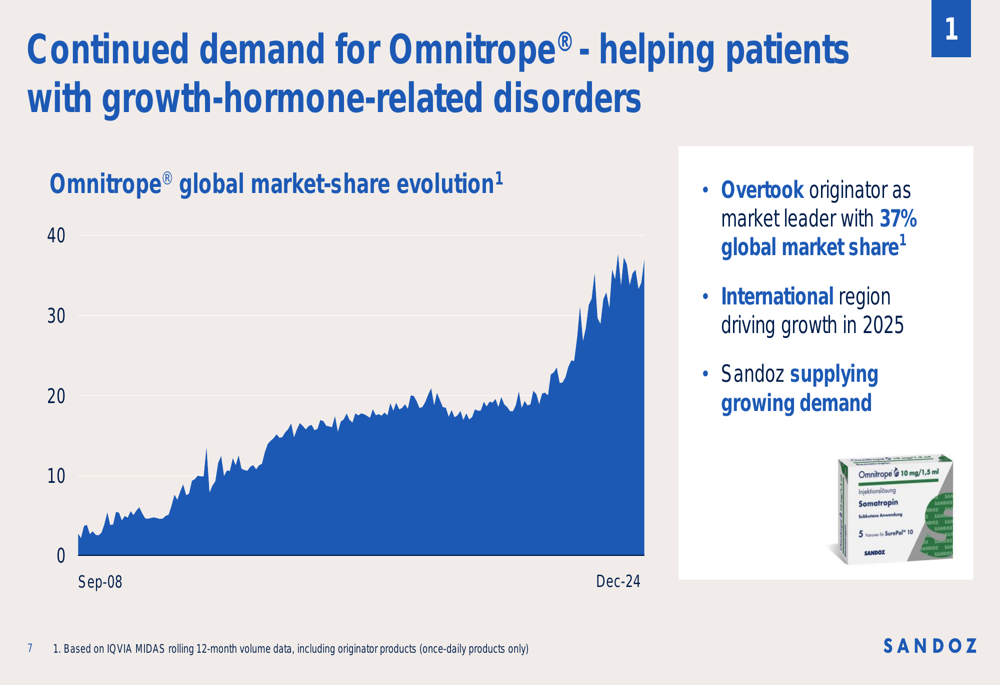

Omnitrope (somatropin) has achieved market leadership, overtaking the originator product with a 37% global market share. The growth hormone treatment has shown particularly strong performance in International markets, as demonstrated in the following market share evolution:

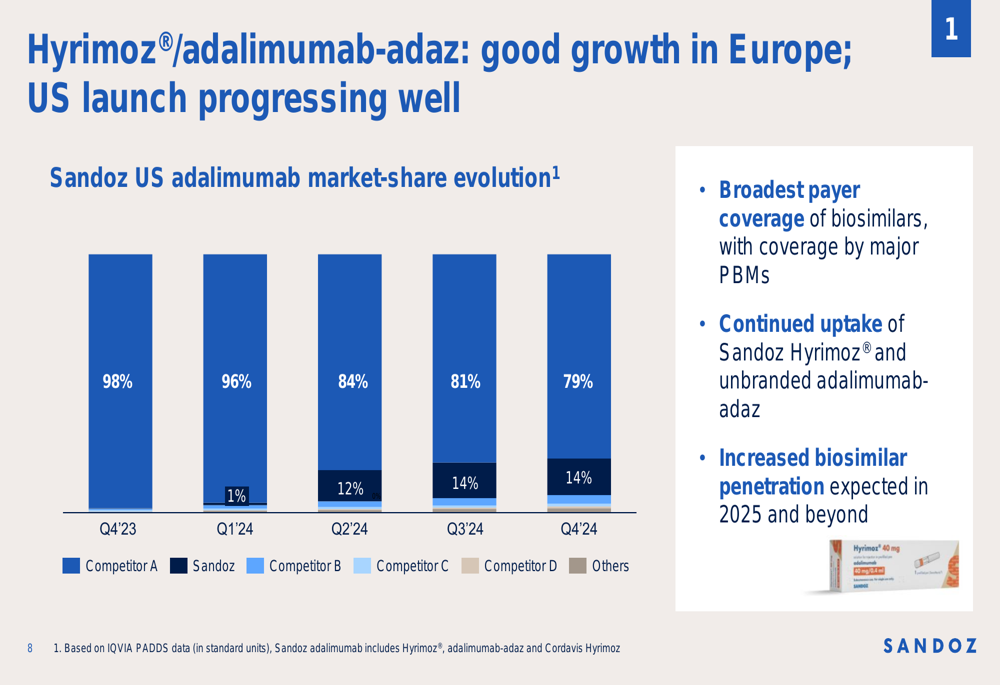

In the competitive U.S. adalimumab market, Sandoz’s Hyrimoz and unbranded adalimumab-adaz have gained significant traction, increasing from just 1% market share in Q4 2023 to 14% by Q4 2024. The company attributes this success to securing "the broadest payer coverage of biosimilars, with coverage by major PBMs."

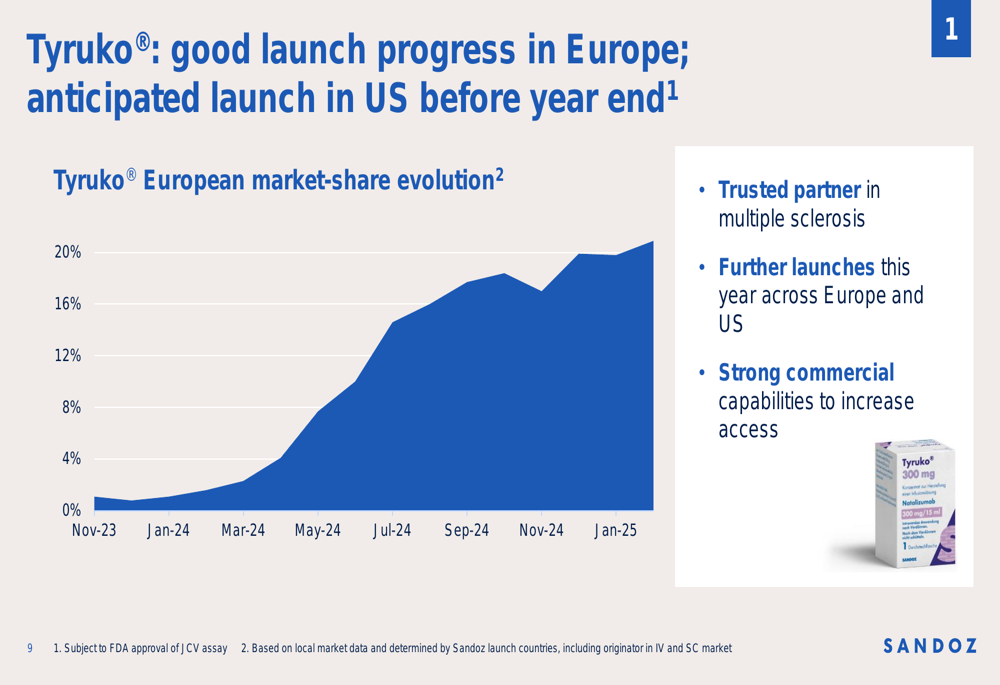

Tyruko (natalizumab) has shown strong uptake in Europe since its launch in late 2023, reaching 20% market share by January 2025. The company anticipates launching the multiple sclerosis treatment in the U.S. before year-end, pending FDA approval of a JCV assay.

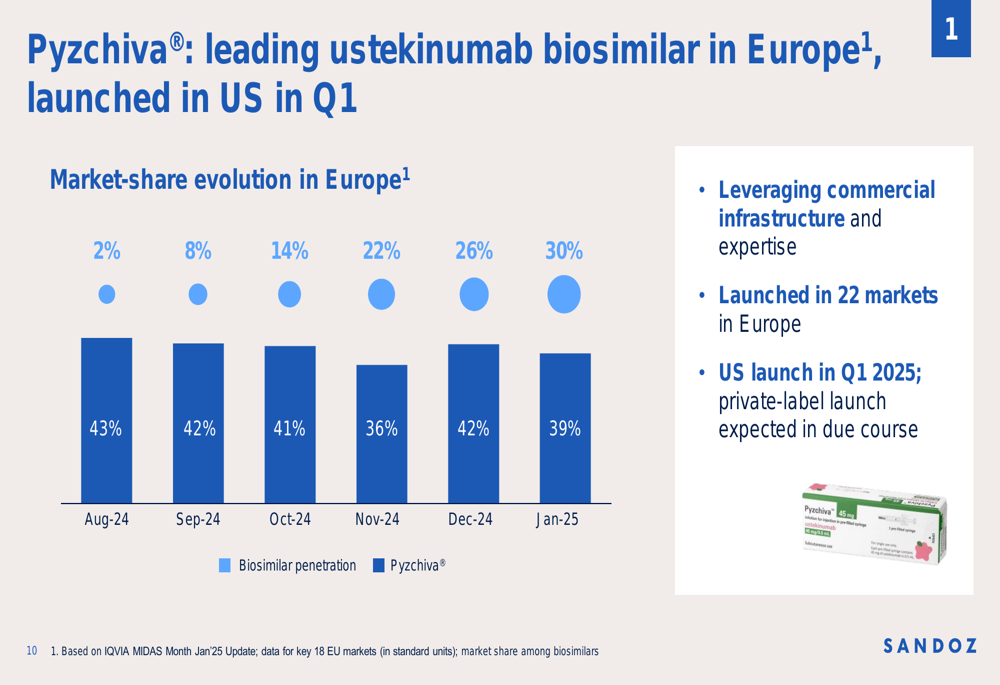

Pyzchiva (ustekinumab) has established itself as the leading ustekinumab biosimilar in Europe with 30% market share and was launched in the U.S. market during Q1 2025.

Financial Position & Balance Sheet

Sandoz reported significant steps to strengthen its balance sheet and improve liquidity during the quarter. The company secured a new USD 2.0 billion multi-currency revolving credit facility, replacing its initial USD 1.25 billion facility, and issued dual-tranche CHF 400 million and single-tranche EUR 500 million bonds.

The proceeds were used to repay term loans, extending debt maturities to 2035 and reducing overall interest expenses. The company maintains investment grade credit ratings of BBB from S&P and Baa2 from Moody’s, with a target leverage ratio (net debt to core EBITDA) below 2.0x in the mid-term.

Regarding U.S. tariffs, Sandoz indicated that the confirmed tariff impact is limited to China. With a manufacturing footprint of 15 sites, including 11 in Europe and one in the U.S., the company expects the full-year impact of confirmed tariffs to be absorbed within its existing guidance.

Forward-Looking Statements & Guidance

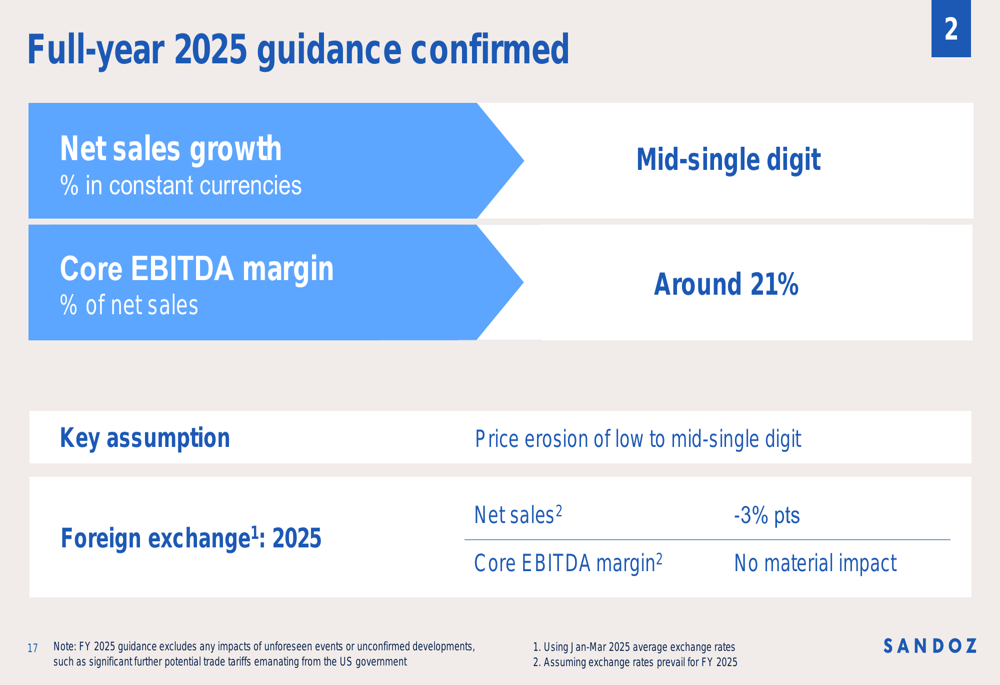

Sandoz confirmed its full-year 2025 guidance with the following key metrics:

The company expects mid-single digit net sales growth in constant currencies and a core EBITDA margin of around 21%. This guidance assumes price erosion in the low to mid-single digits and accounts for an anticipated 3 percentage point negative impact from foreign exchange on net sales.

Looking ahead, Sandoz highlighted several important upcoming milestones:

1. Imminent U.S. launch of Wyost/Jubbonti (denosumab) with European launch in Q4 2025

2. Enzeevu/Afqlir (aflibercept) launch in Europe in Q4 2025

3. Tyruko (natalizumab) launch in the U.S. by the end of the year, pending FDA approval of JCV assay

CEO Richard Saynor emphasized three key priorities for 2025: "Deliver for patients on launches and pipeline, maintain unrelenting focus on commercial execution, and drive further growth in sales, margin and free cash flow."

The company’s robust biosimilar pipeline includes multiple products targeting major biologics with combined originator sales of USD 54 billion, positioning Sandoz for continued growth in this high-value segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.