Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

SBA Communications (NASDAQ:SBAC), a leading tower infrastructure company with a market capitalization of $24.13 billion, recently presented its first quarter 2025 financial results. The company maintained stable performance with modest organic growth despite facing challenges in its international operations, including strategic exits from the Philippines and Colombia markets. While the company reported revenue slightly above expectations at $664.25 million (versus forecasted $661.68 million), its EPS of $1.77 fell short of the anticipated $2.11.

The company’s stock has shown resilience, trading at $232.79 as of July 10, 2025, within its 52-week range of $192.55 to $252.64. The modest aftermarket price increase following the earnings announcement suggests investors may be focusing on the company’s revenue performance and improved full-year outlook rather than the EPS miss.

Quarterly Performance Highlights

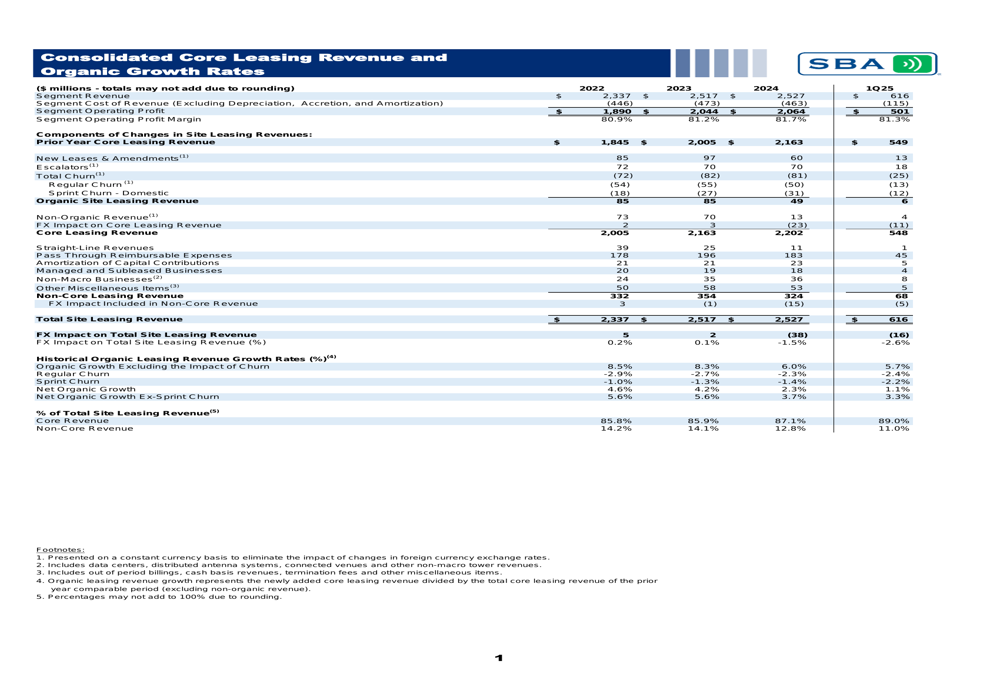

SBA Communications reported $616 million in segment revenue and $501 million in segment operating profit for Q1 2025. Core leasing revenue reached $548 million, accounting for 89.0% of total site leasing revenue, with an organic growth rate of 1.1% for the quarter.

As shown in the following consolidated core leasing revenue breakdown, the company has maintained relatively stable revenue growth despite various market pressures:

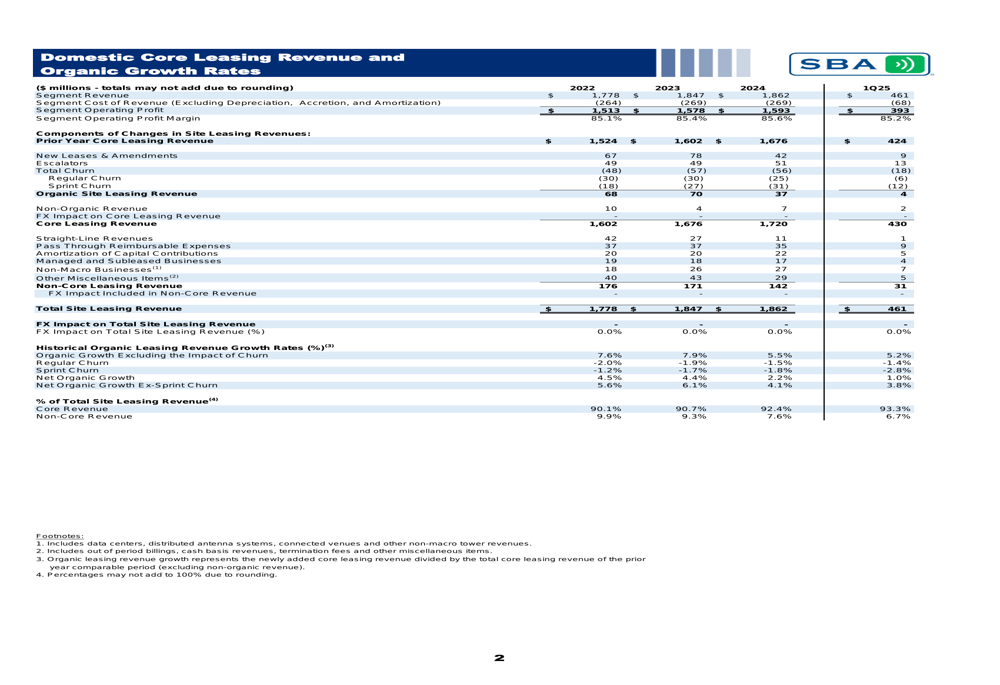

The domestic segment continued to show strength, with $461 million in segment revenue and $393 million in segment operating profit. Domestic core leasing revenue was $430 million, representing 93.3% of total domestic site leasing revenue, with an organic growth rate of 1.0%.

The detailed domestic performance metrics demonstrate the stability of SBA (LON:SBA)’s U.S. operations:

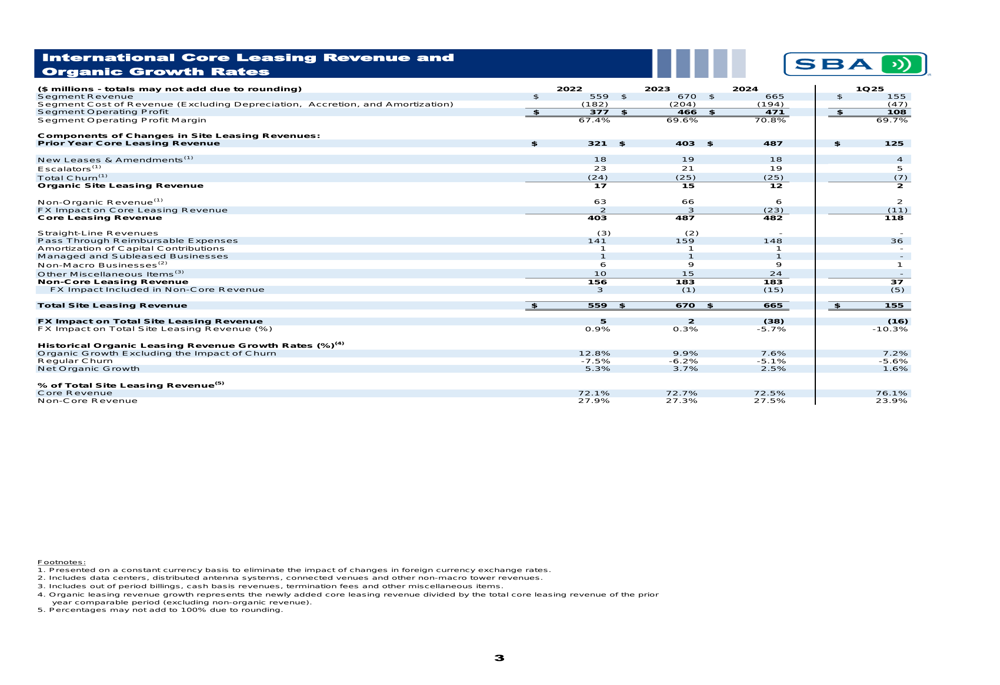

International operations generated $155 million in segment revenue and $108 million in segment operating profit. International core leasing revenue reached $118 million, accounting for 76.1% of total international site leasing revenue, with a slightly stronger organic growth rate of 1.6% compared to domestic operations.

The following chart illustrates the international segment’s performance metrics:

Detailed Financial Analysis

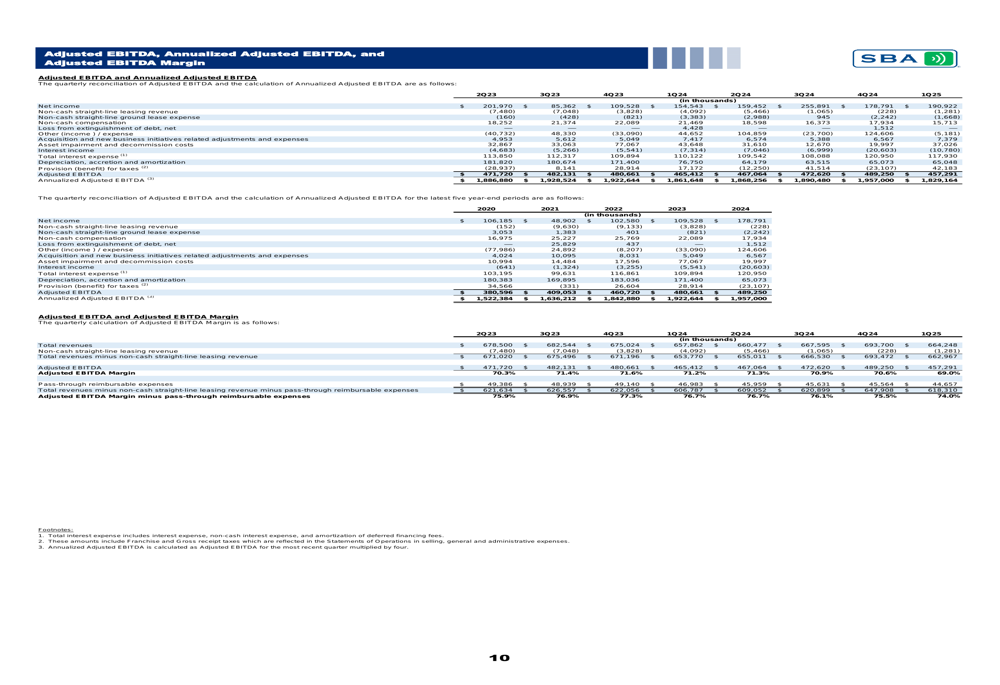

SBA Communications maintained strong financial metrics in Q1 2025, with a Tower Cash Flow Margin of 87.3% and an Adjusted EBITDA Margin of 74.0%. The company reported Adjusted Funds From Operations (AFFO) per share of $3.18 for the quarter.

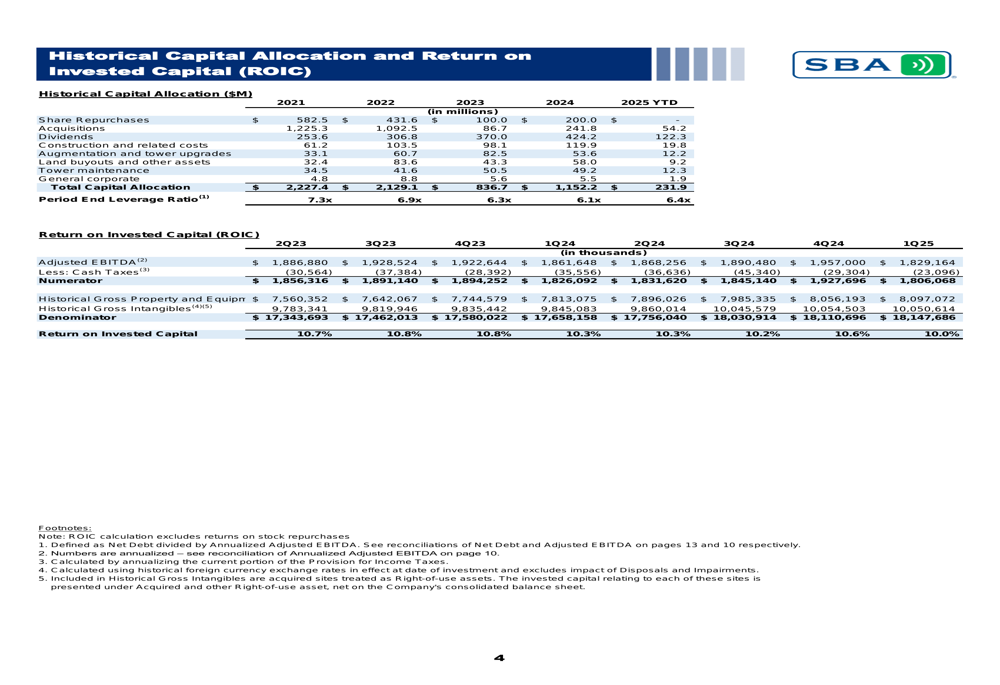

The company’s capital allocation strategy shows a disciplined approach to investments and shareholder returns. In 2025 YTD, SBA has allocated $54.2 million to acquisitions and $122.3 million to dividends, while maintaining a leverage ratio of 6.4x.

The historical capital allocation and return metrics provide insight into the company’s investment strategy:

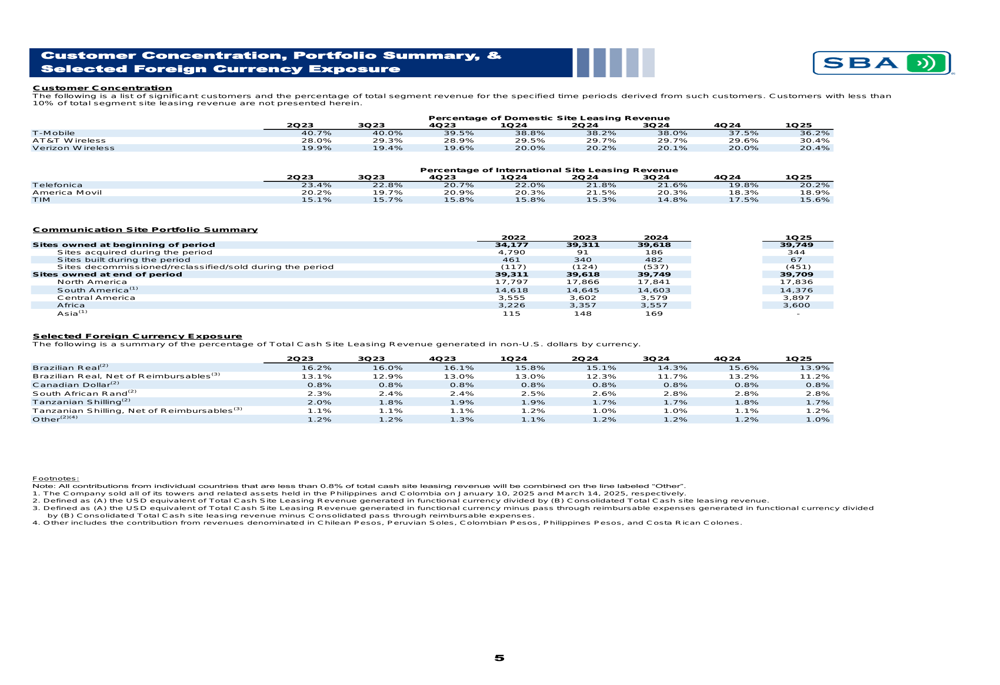

SBA’s customer base remains diversified across major telecommunications providers, with a portfolio of 39,709 sites at the end of Q1 2025. The company maintains geographic diversification across North America, South America, Central America, Africa, and Asia, with exposure to various currencies including the Brazilian Real, Canadian Dollar, South African Rand, and Tanzanian Shilling.

The following breakdown shows the company’s customer concentration and portfolio distribution:

SBA Communications’ debt profile shows a weighted average interest rate of 3.7%, with a calculated leverage ratio of 6.4x. The company maintains a Net Cash Interest Coverage Ratio of 4.9x, indicating adequate ability to service its debt obligations.

The debt maturity schedule and leverage metrics provide insight into the company’s financial structure:

Strategic Initiatives & Portfolio Management

SBA Communications has implemented strategic market exits in the Philippines and Colombia, as mentioned in the earnings call, reflecting a focus on optimizing its international portfolio. These exits appear to be part of a broader strategy to concentrate resources in markets with stronger growth potential and more favorable operating conditions.

The company’s capital allocation history shows a shift in 2025, with no share repurchases YTD compared to $200 million in 2024, suggesting a more conservative approach to capital deployment in the current environment. Instead, the focus appears to be on strategic acquisitions ($54.2 million YTD) and returning value to shareholders through dividends ($122.3 million YTD).

Forward-Looking Statements

According to the earnings call, SBA Communications has revised its full-year outlook upwards for site leasing revenue, tower cash flow, and adjusted EBITDA. The company expects increased U.S. leasing activity and potential for better international lease escalations.

CEO Brendan Cavanaugh expressed confidence in the company’s positioning, stating, "We are very well positioned," and noting that "The wireless ecosystem will continually evolve, providing new opportunities for those willing to take them."

However, the company faces several challenges, including high debt levels that could constrain future investments, potential impact from carrier consolidation in Brazil, and competitive pressures in the wireless infrastructure market. The recent market exits also suggest a recalibration of international growth strategies.

Despite these challenges, SBA Communications’ stable margins, disciplined capital allocation, and strategic portfolio management position it to navigate the evolving wireless infrastructure landscape while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.