Gold ticks up but remains pressured by Fed rate caution, easing trade fears

Introduction & Market Context

Schindler Holding AG presented its third-quarter 2025 results on October 24, revealing a company successfully navigating challenging market conditions through operational efficiency and strategic focus on high-growth segments. The Swiss elevator and escalator manufacturer demonstrated remarkable margin expansion despite topline pressure, particularly from China’s declining new installation market.

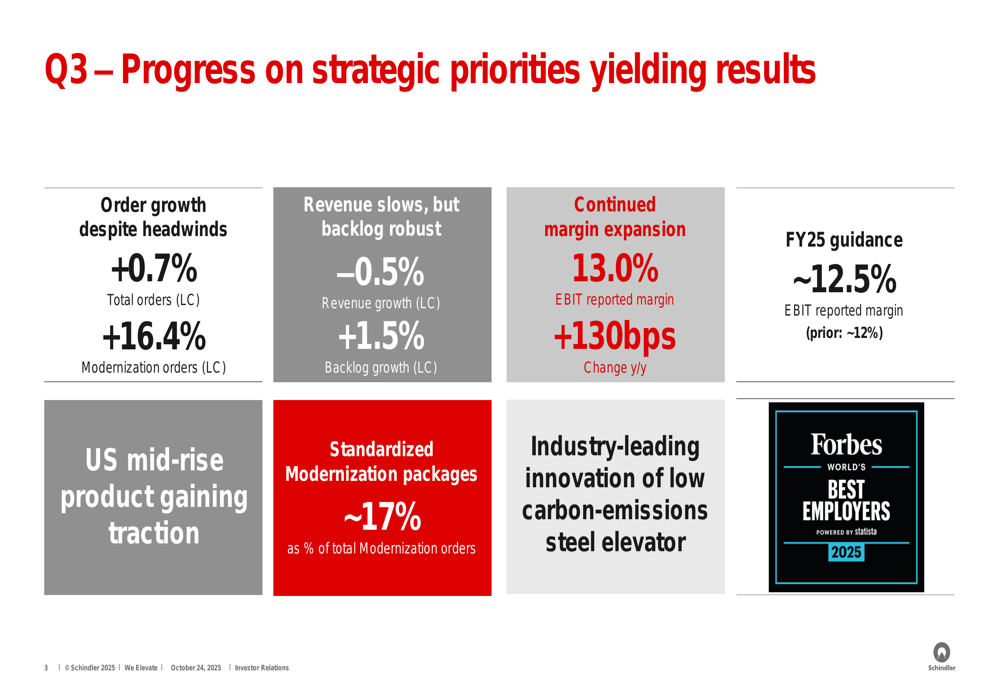

The company achieved a 130 basis point improvement in EBIT margin year-over-year, reaching 13.0% in Q3 2025, while upgrading its full-year guidance despite ongoing global economic uncertainties and regional market challenges.

Quarterly Performance Highlights

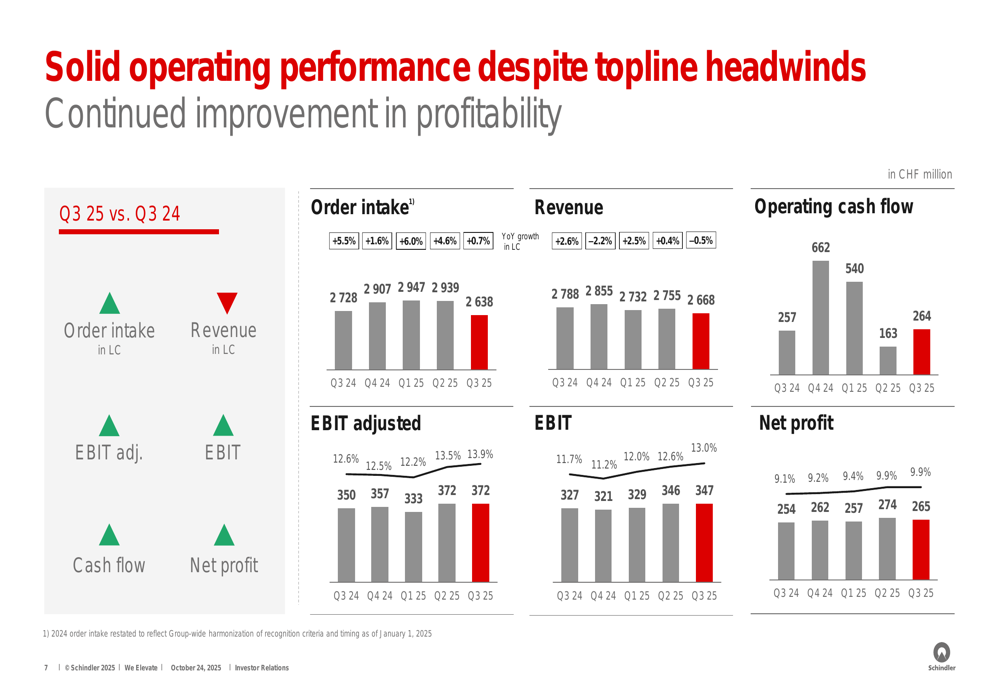

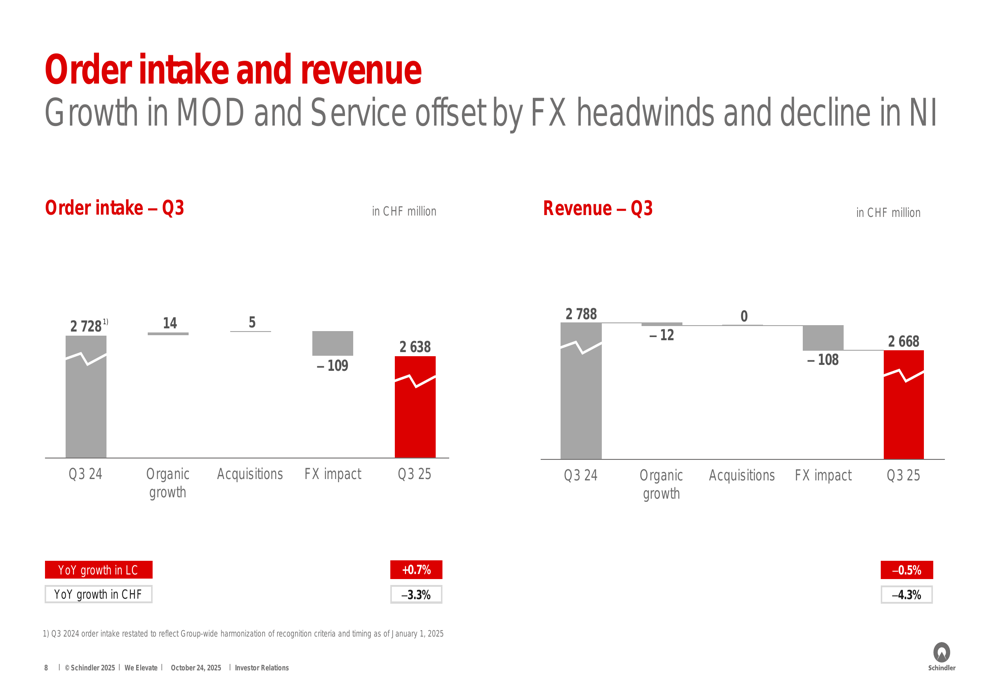

Schindler reported mixed financial results for Q3 2025, with order intake growing 0.7% in local currency to 2,638 million CHF, though this represented a 3.3% decline in Swiss franc terms due to currency effects. Revenue slightly decreased by 0.5% in local currency to 2,668 million CHF, translating to a 4.3% decline in CHF.

As shown in the following comprehensive overview of Q3 performance:

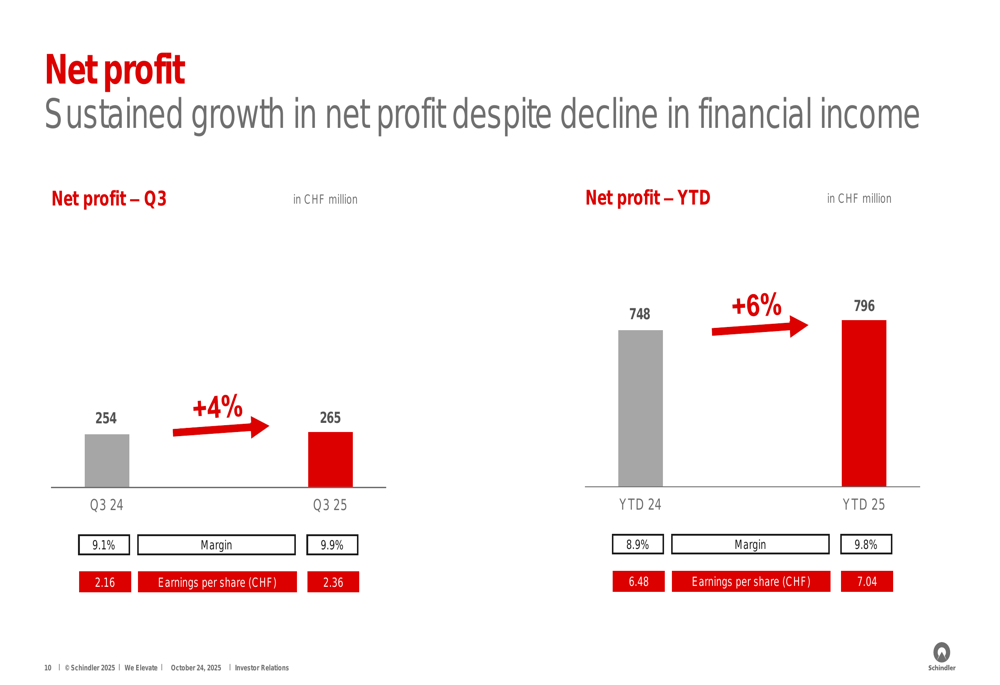

Despite the revenue challenges, Schindler’s profitability metrics showed impressive improvement. The company reported EBIT of 347 million CHF, up from 327 million CHF in Q3 2024, while adjusted EBIT reached 372 million CHF compared to 350 million CHF in the prior year. Net profit increased to 265 million CHF from 254 million CHF, representing a 4% year-over-year improvement.

The following chart illustrates this solid operating performance despite topline headwinds:

Operating cash flow remained strong at 264 million CHF for Q3, representing a 3% increase year-over-year. For the first nine months of 2025, operating cash flow reached 967 million CHF, up 4% compared to the same period in 2024, demonstrating Schindler’s continued focus on cash generation despite market challenges.

Detailed Financial Analysis

Schindler’s Q3 performance reflects the company’s ability to offset revenue pressures through operational efficiency. The order intake analysis reveals that organic growth contributed positively, but was partially offset by currency effects:

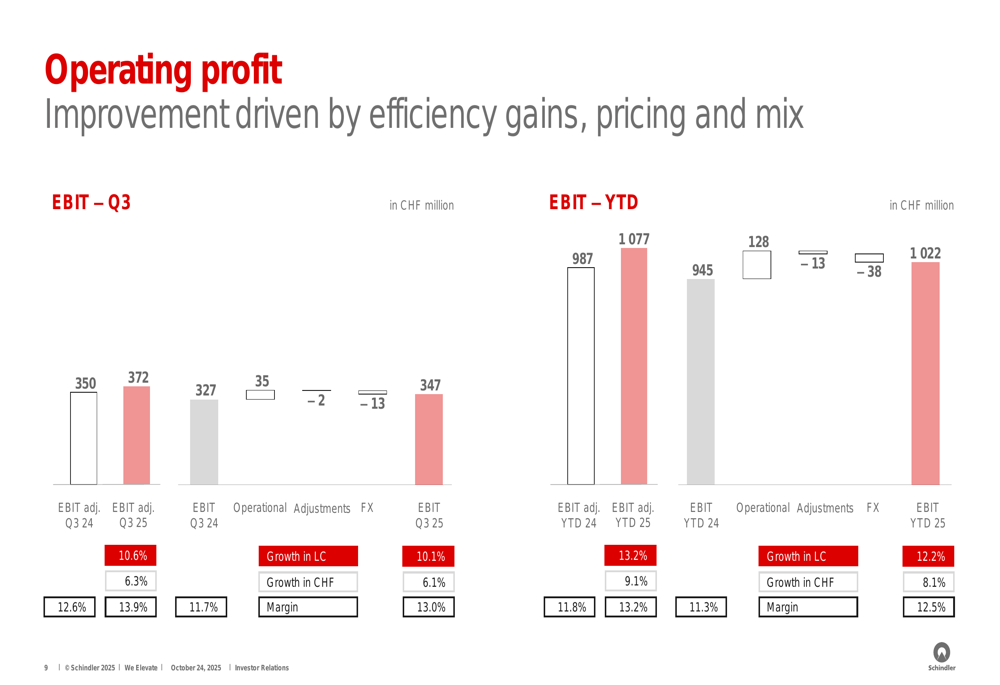

On the profitability front, Schindler continued to demonstrate margin expansion across both reported and adjusted EBIT metrics. The company’s EBIT margin of 13.0% represents a significant 130 basis point improvement compared to Q3 2024, highlighting successful cost management and operational efficiency initiatives.

The operating profit analysis shows consistent improvement in both quarterly and year-to-date figures:

Net profit also showed solid growth, reaching 265 million CHF for Q3 2025, a 4% increase from the previous year. For the first nine months of 2025, net profit grew 6% to 796 million CHF, reflecting Schindler’s ability to translate operational improvements into bottom-line results:

Regional Market Analysis

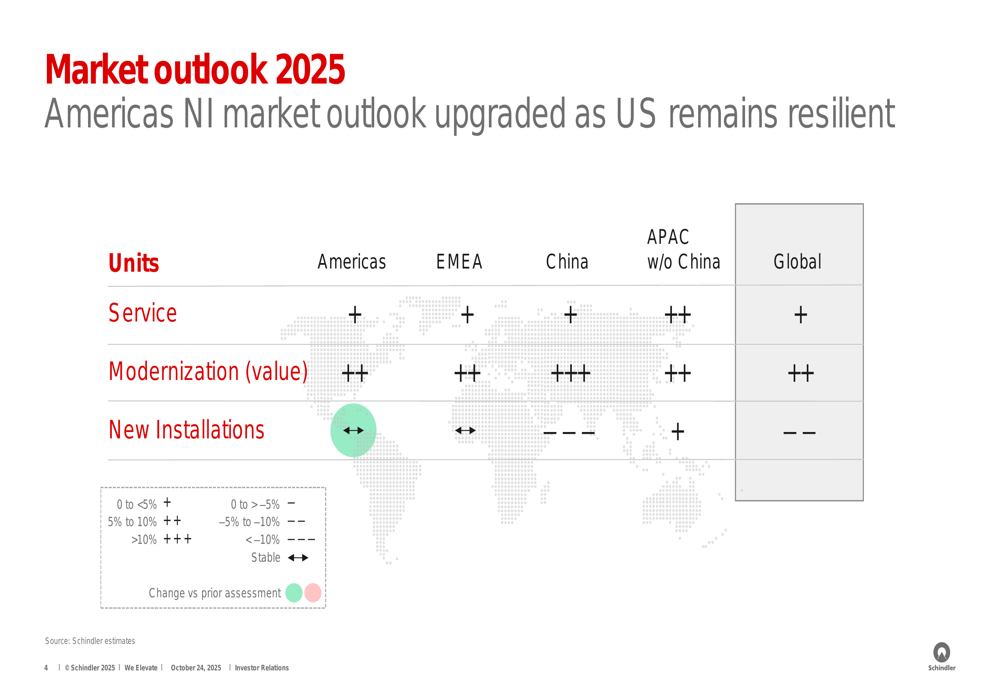

Schindler’s performance varied significantly across regions and product segments. The company provided a detailed market outlook for 2025, highlighting strong growth opportunities in modernization across all regions, while noting significant challenges in new installations, particularly in China:

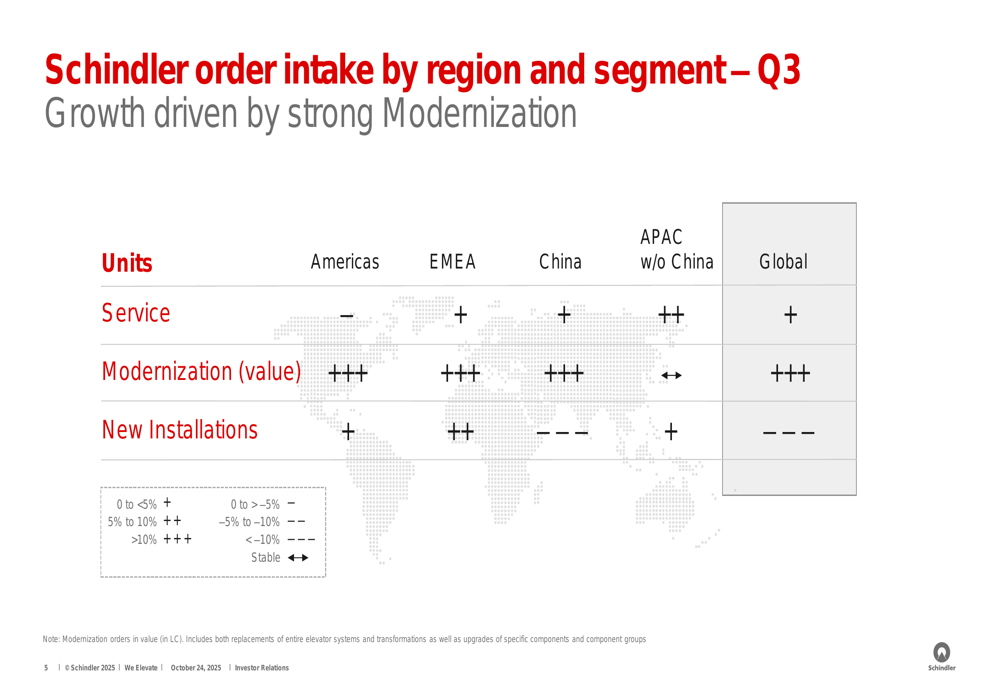

The company’s order intake reflected these market dynamics, with modernization orders showing exceptional strength (+16.4% in local currency) across most regions. Meanwhile, new installation orders faced significant headwinds in China, though other regions showed more resilience:

The contrasting performance between modernization and new installations segments underscores Schindler’s strategic shift toward higher-margin service and modernization business in response to changing market conditions, particularly in China where economic challenges continue to impact the construction sector.

Strategic Initiatives & Forward Outlook

Schindler highlighted several strategic initiatives driving its performance, including gaining traction in the US mid-rise market, standardized modernization packages (representing approximately 17% of total modernization orders), and the launch of an industry-leading low-carbon-emissions steel elevator, reinforcing the company’s commitment to sustainability.

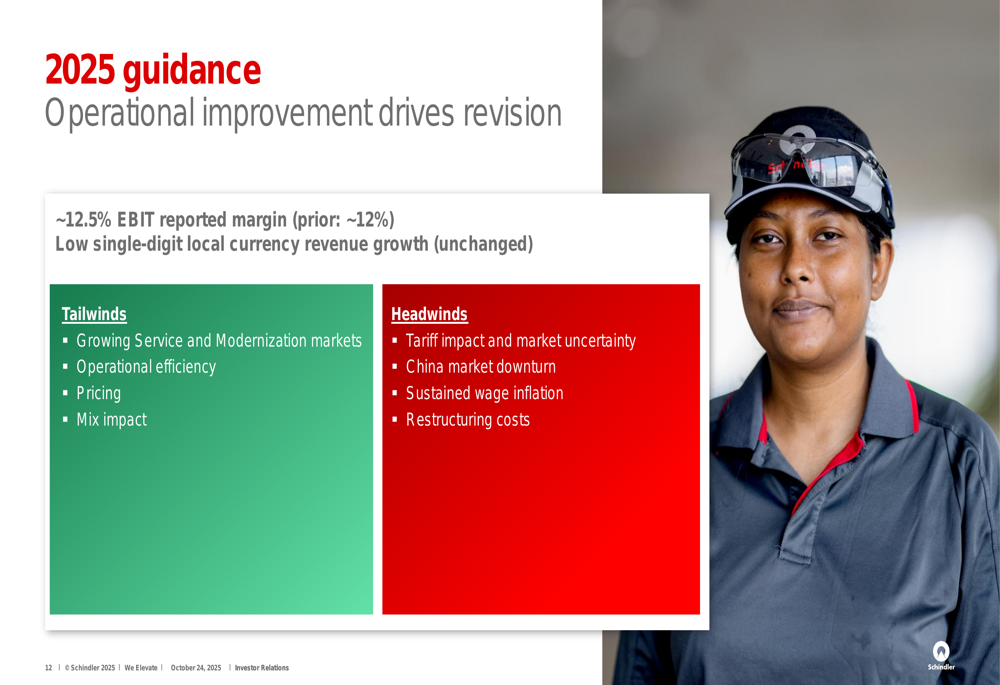

Based on its strong performance and strategic initiatives, Schindler upgraded its full-year 2025 EBIT margin guidance to approximately 12.5%, up from the previous guidance of approximately 12%, while maintaining its forecast for low single-digit local currency revenue growth.

The company’s guidance reflects both tailwinds and headwinds as illustrated in the following slide:

Tailwinds supporting Schindler’s outlook include growing service and modernization markets, continued operational efficiency improvements, favorable pricing, and positive mix impact. However, the company also faces significant headwinds, including tariff impacts and market uncertainty, the ongoing China market downturn, sustained wage inflation, and restructuring costs.

Competitive Industry Position

Schindler’s focus on innovation and sustainability positions it well against industry competitors. The company’s recognition as a Forbes Best Employer 2025 highlights its strong corporate culture and ability to attract talent in a competitive labor market.

The strategic emphasis on modernization and service segments provides Schindler with more stable revenue streams compared to the more cyclical new installations business, which is particularly important given the current challenges in the Chinese construction market.

The company’s ability to expand margins despite revenue challenges demonstrates effective cost management and operational discipline, which should help Schindler maintain its competitive position even in challenging market conditions.

In conclusion, Schindler’s Q3 2025 results demonstrate a company effectively navigating a complex global market environment through strategic focus on high-growth segments, operational efficiency, and innovation. While challenges remain, particularly in the Chinese new installations market, the company’s upgraded guidance reflects confidence in its ability to continue delivering margin improvement through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.