Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Scholar Rock Holding Corp (NASDAQ:SRRK) presented its Q2 2025 business update on August 6, highlighting progress toward the anticipated U.S. launch of its lead candidate apitegromab for spinal muscular atrophy (SMA). Despite the company’s optimistic outlook, Scholar Rock’s stock fell 12.09% in premarket trading to $32.51, suggesting investors may have expected more from the quarterly update.

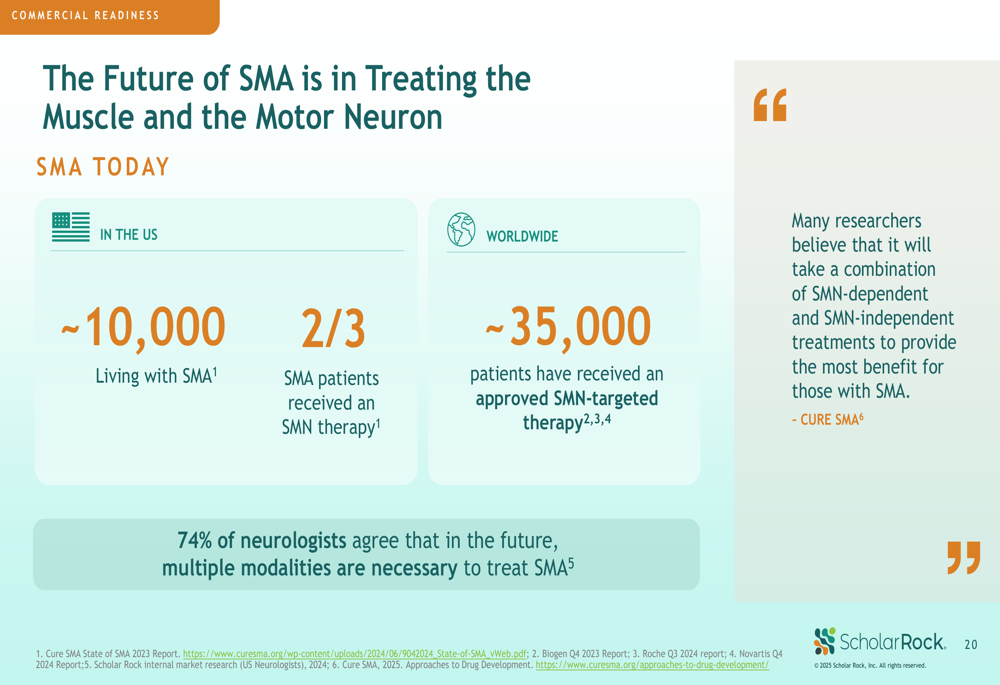

The company is positioning apitegromab as the first muscle-targeted treatment for SMA, complementing existing SMN-targeted therapies that address the underlying genetic cause of the disease. According to the presentation, approximately 10,000 people in the U.S. live with SMA, with about two-thirds having received an SMN therapy.

As shown in the following slide outlining the agenda for the earnings call, Scholar Rock’s leadership team presented a comprehensive overview of the company’s progress and strategic priorities:

Quarterly Performance Highlights

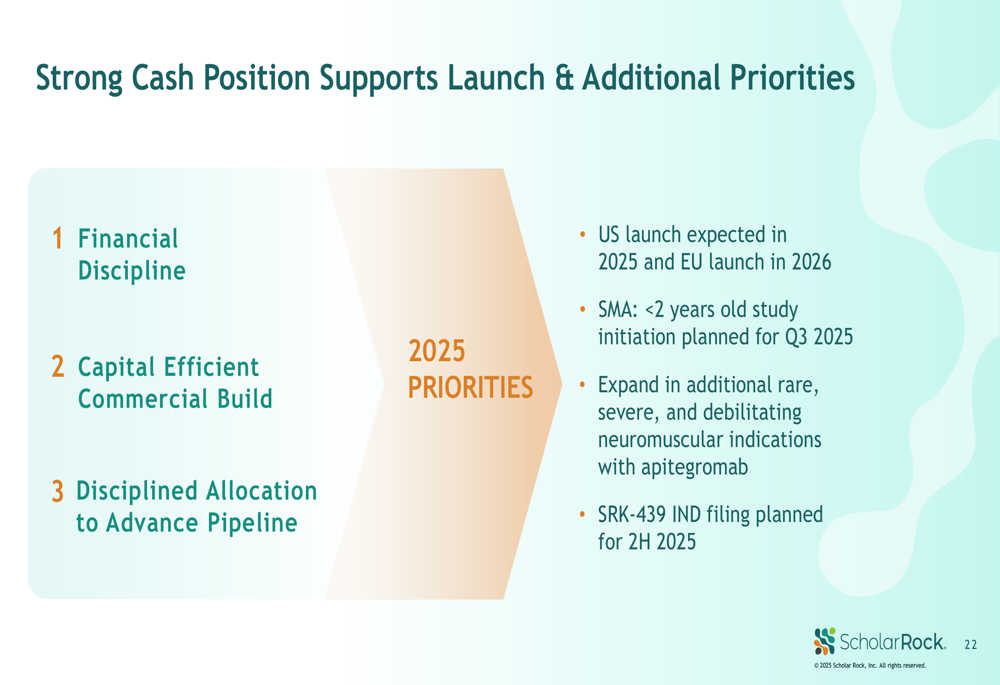

Scholar Rock reported $295 million in cash as of June 30, 2025, a significant decrease from the $364.4 million reported at the end of Q1 2025, indicating substantial cash utilization during the quarter as the company prepares for commercial launch.

The company’s key milestone achievements were summarized in the following slide, highlighting regulatory progress, pipeline developments, and corporate initiatives:

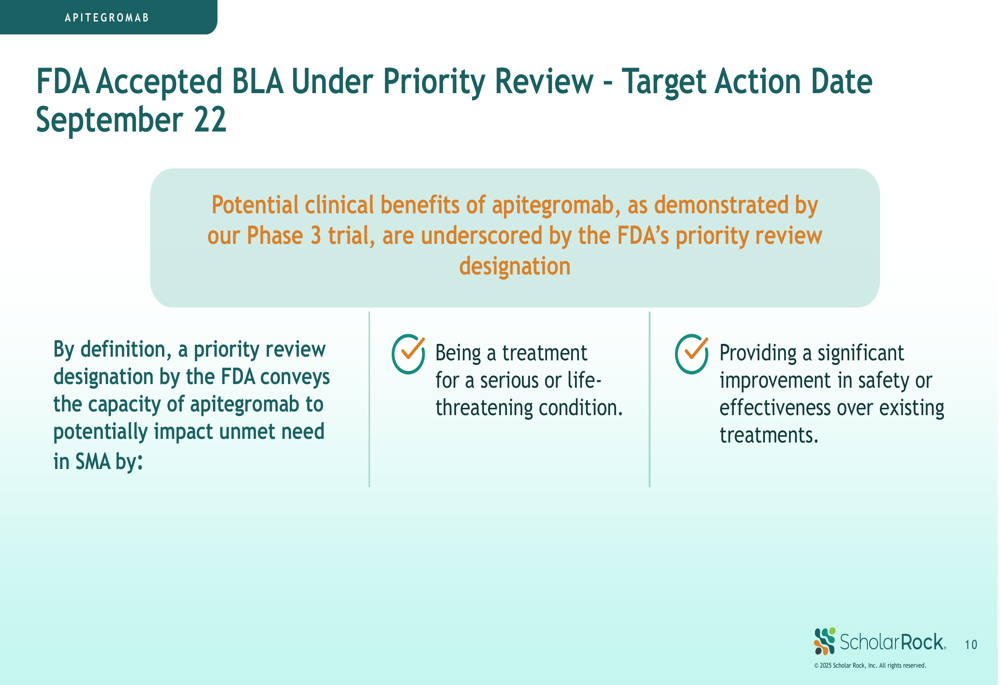

The most significant near-term catalyst is the FDA target action date of September 22, 2025, for apitegromab in SMA, following the agency’s acceptance of the Biologics License Application (BLA) under Priority Review. The European Medicines Agency (EMA) has validated the Marketing Authorization Application (MAA), with approval anticipated in 2026.

Clinical Development Progress

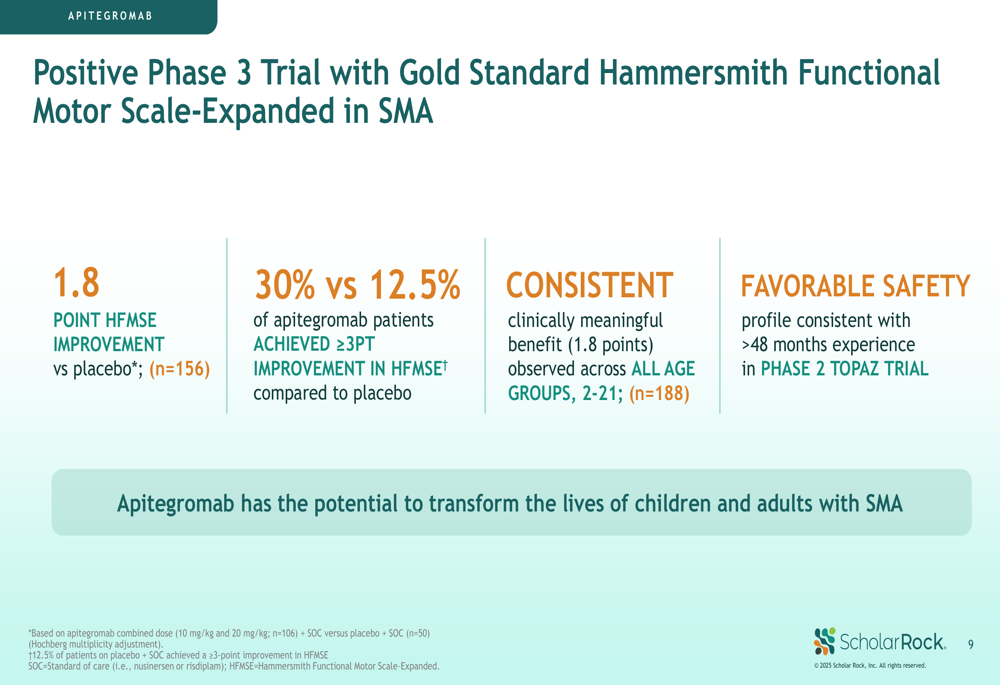

Scholar Rock’s confidence in apitegromab stems from positive Phase 3 trial results, which demonstrated meaningful improvements in motor function for SMA patients. The data, measured using the gold-standard Hammersmith Functional Motor Scale-Expanded (HFMSE), showed a 1.8-point improvement versus placebo and a higher percentage of patients achieving clinically meaningful benefits.

As illustrated in the following slide detailing the Phase 3 results, the drug demonstrated consistent benefits across all age groups and a favorable safety profile:

The FDA’s decision to grant Priority Review underscores the potential clinical significance of apitegromab, as this designation is reserved for treatments that address serious conditions and offer significant improvements over existing therapies.

Pipeline Expansion Strategy

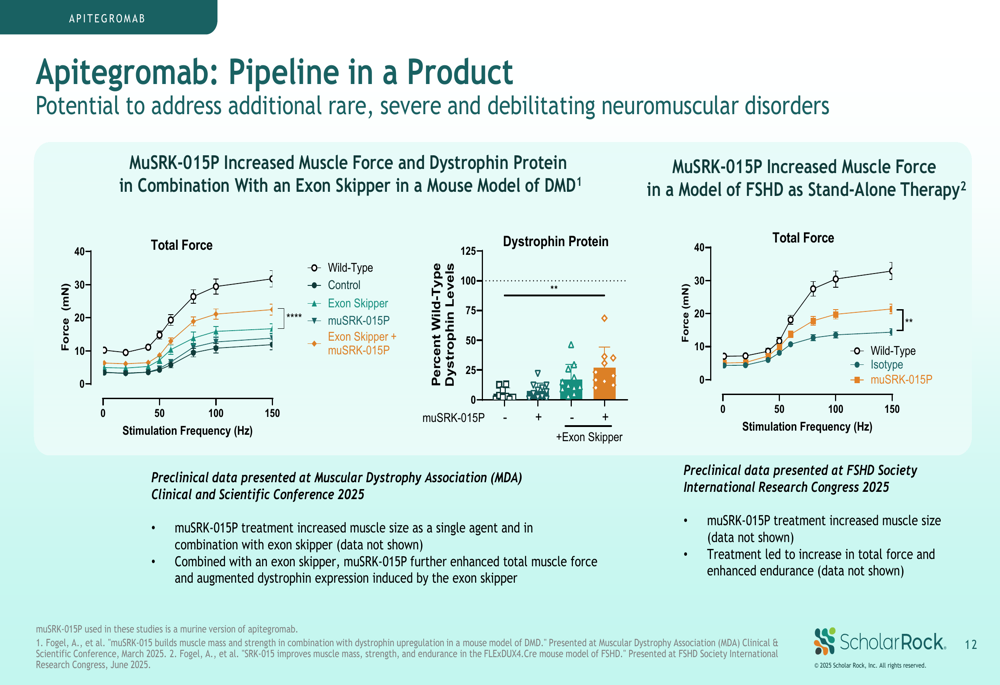

Beyond its lead SMA program, Scholar Rock is expanding apitegromab’s potential applications to other neuromuscular disorders. Preclinical data presented in the following slide demonstrates the drug’s potential in Duchenne muscular dystrophy (DMD) and facioscapulohumeral muscular dystrophy (FSHD):

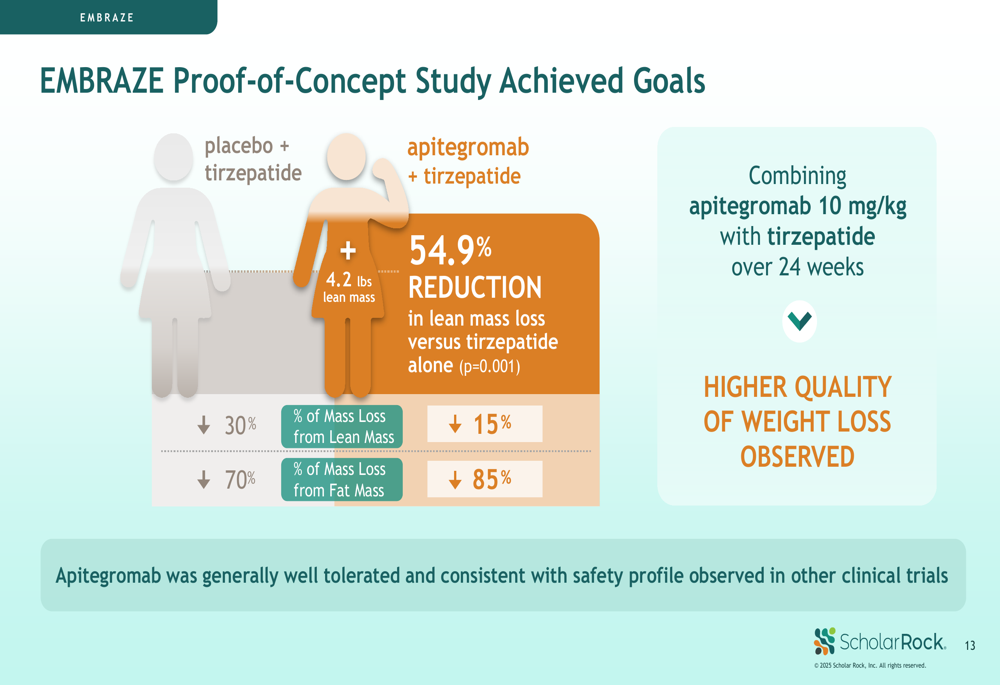

Additionally, the company reported positive results from its EMBRAZE proof-of-concept study, which evaluated apitegromab in combination with tirzepatide for obesity. The data showed that adding apitegromab resulted in higher quality weight loss, with a 54.9% reduction in lean mass loss compared to tirzepatide alone.

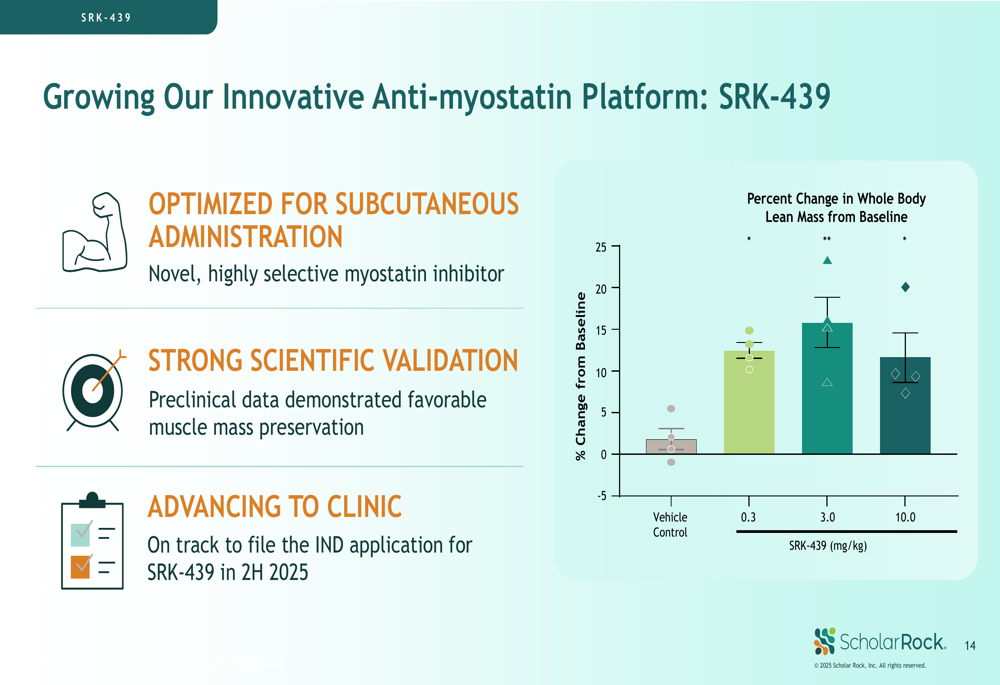

Scholar Rock is also advancing SRK-439, a novel myostatin inhibitor optimized for subcutaneous administration, with plans to file an Investigational New Drug (IND) application in the second half of 2025. Preclinical data showed significant increases in whole body lean mass at various dose levels:

Commercial Readiness

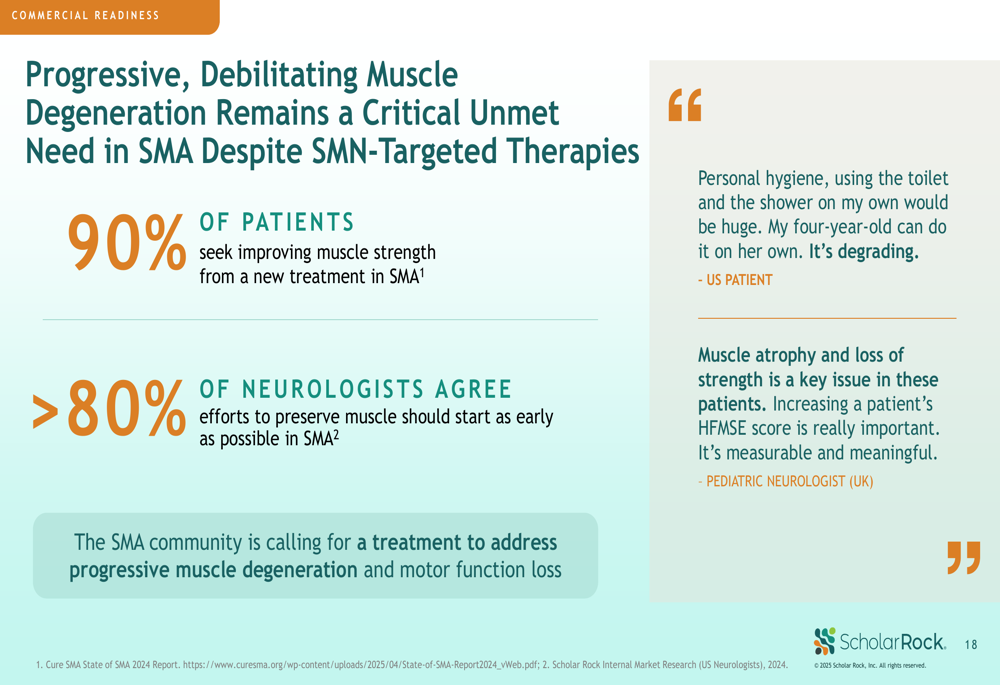

With the potential U.S. approval of apitegromab approaching, Scholar Rock is intensifying its commercial preparation efforts. The company emphasized the significant unmet need that remains in SMA despite existing therapies, with 90% of patients seeking improved muscle strength from new treatments.

The following slide highlights patient and physician perspectives on the continued challenges faced by SMA patients:

Scholar Rock’s commercial strategy recognizes the complementary role of apitegromab alongside existing SMN-targeted therapies, positioning it as part of a comprehensive approach to SMA treatment:

Financial Position

Scholar Rock reported $295 million in cash as of June 30, 2025, which the company believes will support its operations through the anticipated U.S. launch of apitegromab and other strategic priorities. The significant cash burn from Q1 to Q2 ($364.4 million to $295 million) reflects the company’s increased investment in commercial infrastructure and ongoing clinical development programs.

The company emphasized its disciplined approach to capital allocation, focusing on an efficient commercial build and phased investments to support future initiatives:

Forward-Looking Statements

Scholar Rock outlined its key priorities for 2025, which include executing a successful U.S. commercial launch of apitegromab (pending regulatory approval), advancing EU launch preparedness, and expanding into additional neuromuscular diseases:

Near-term catalysts include the FDA decision on apitegromab in September 2025, initiation of the Phase 2 OPAL trial in infants and toddlers with SMA in Q3 2025, and the IND filing for SRK-439 in the second half of 2025.

Despite the positive developments presented in the Q2 update, the significant premarket stock decline suggests investors may have concerns about the company’s accelerating cash burn rate or may have been expecting additional data or more specific commercial guidance ahead of the anticipated product launch.

As Scholar Rock approaches this critical inflection point with its lead program, the company’s ability to successfully navigate the regulatory process, execute an efficient commercial launch, and advance its broader pipeline will be crucial factors for investors to monitor in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.