Bitcoin price today: slips below $113k, near 6-wk low despite Fed cut bets

Scholastic Corporation (NASDAQ:SCHL) reported mixed fourth-quarter 2025 results on Thursday, July 24, with revenue growth offset by significant earnings per share declines and a substantial increase in debt. The company’s stock fell 4.56% during regular trading hours, with a modest 0.62% recovery in after-hours trading.

Quarterly Performance Highlights

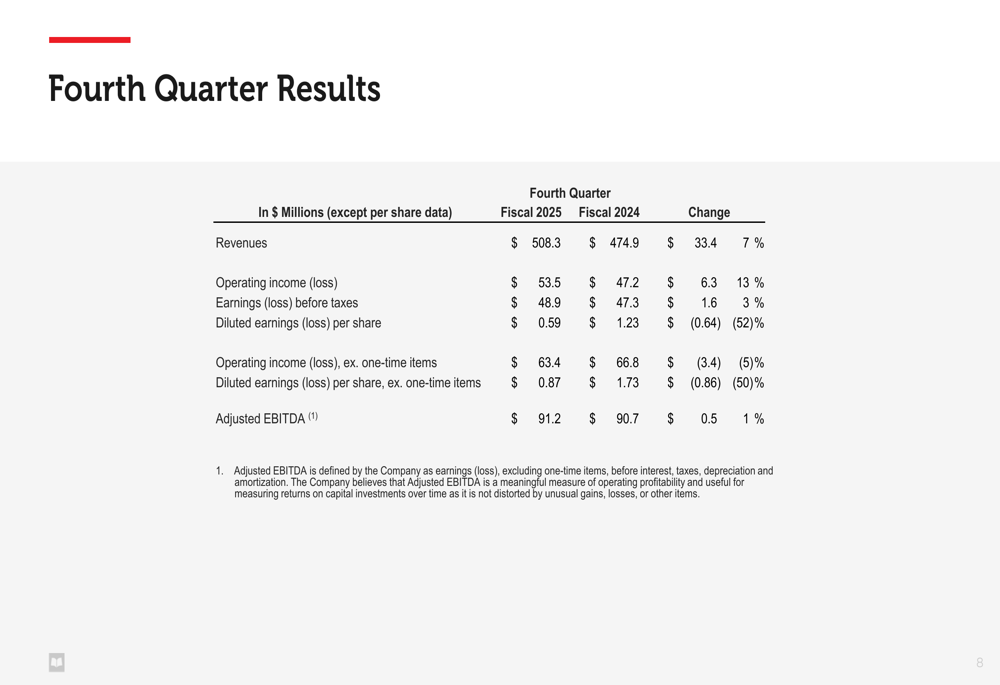

Scholastic delivered fourth-quarter revenue of $508.3 million, a 7% increase from $474.9 million in the same period last year. Operating income rose 13% to $53.5 million, while adjusted EBITDA showed a modest 1% improvement to $91.2 million. Despite these operational gains, diluted earnings per share fell sharply by 52% to $0.59, compared to $1.23 in the fourth quarter of fiscal 2024.

"We delivered strong financial and strategic results in the fourth quarter of fiscal 2025, with Adjusted EBITDA growing robustly in line with the original guidance range and Revenue growth in line with expectations," stated Peter Warwick, President and CEO of Scholastic, according to the presentation.

As shown in the following financial results table:

The company’s performance excluding one-time items showed similar patterns, with diluted EPS falling 50% to $0.87 from $1.73 in the prior year. This significant EPS decline came despite the revenue and operating income growth, suggesting margin pressures and potentially higher costs or tax impacts.

Segment Performance Analysis

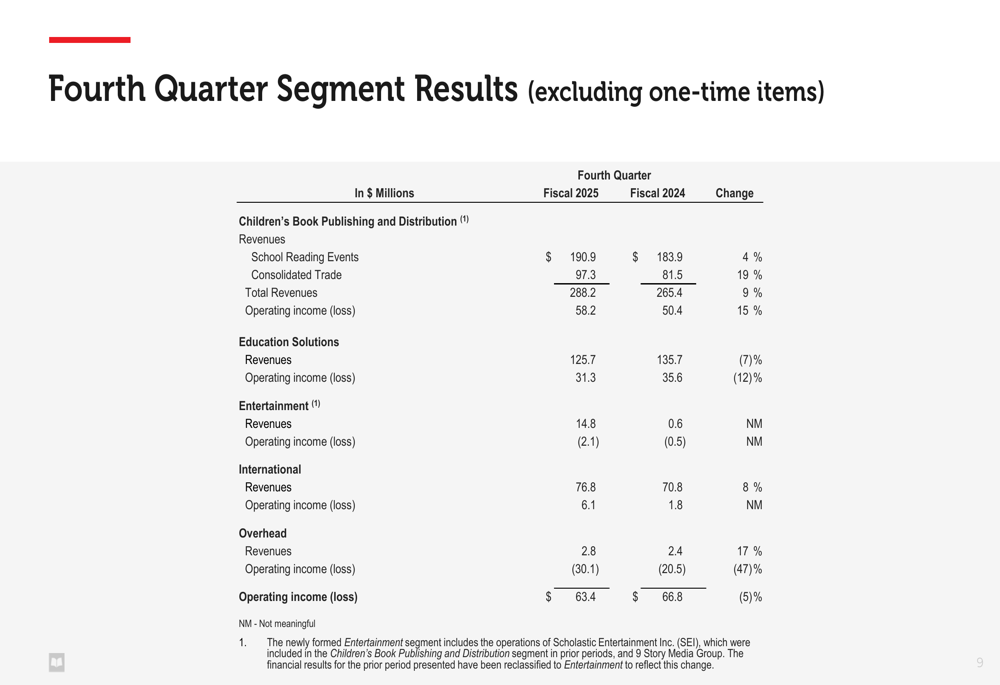

Scholastic’s performance varied significantly across business segments, with Children’s Book Publishing and Distribution showing strong results while Education Solutions faced challenges.

The Children’s Book Publishing and Distribution segment reported a 9% revenue increase to $288.2 million and a 15% jump in operating income to $58.2 million. This growth was driven by Trade Publishing success, particularly the launch of "Sunrise on the Reaping," and a 4% increase in Book Fair counts to over 100,000 fairs.

In contrast, the Education Solutions segment saw revenue decline 7% to $125.7 million and operating income fall 12% to $31.3 million, reflecting ongoing pressures in the supplemental curriculum market.

The following segment breakdown illustrates these contrasting performances:

The Entertainment segment showed significant revenue growth with the addition of 9 Story Media Group, while the International segment delivered 8% revenue growth and substantially improved operating income. However, overhead costs increased 47%, partially offsetting gains in the operating segments.

"We began executing on significant organizational changes to strengthen leadership, enhance growth, and improve efficiencies," noted Warwick in the presentation materials, addressing the company’s efforts to manage these overhead increases.

Balance Sheet and Cash Flow

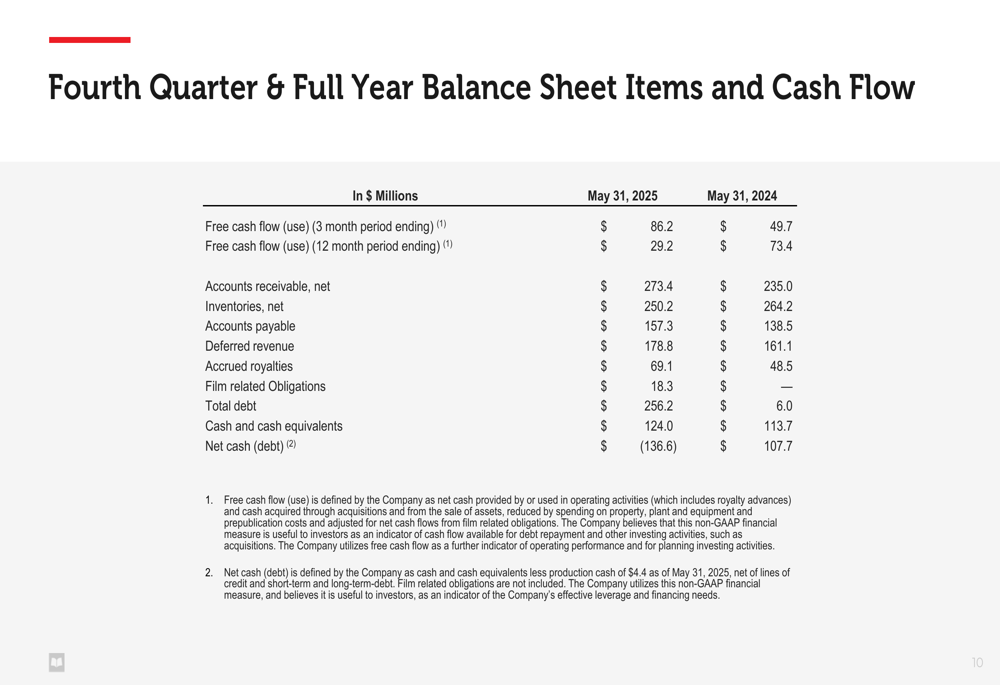

Scholastic’s balance sheet showed significant changes, with total debt increasing dramatically to $256.2 million as of May 31, 2025, compared to just $6.0 million a year earlier. This shift transformed the company’s net cash position of $107.7 million in fiscal 2024 to a net debt position of $136.6 million.

The company reported improved free cash flow of $86.2 million for the three-month period ending May 31, 2025, up from $49.7 million in the comparable period. However, full-year free cash flow declined substantially to $29.2 million from $73.4 million in fiscal 2024.

The following balance sheet and cash flow data highlights these significant changes:

Despite the increased debt load, Scholastic continued to return capital to shareholders, with $35 million in dividends and share repurchases in the fourth quarter alone, bringing the fiscal 2025 total to over $92 million.

Forward-Looking Statements

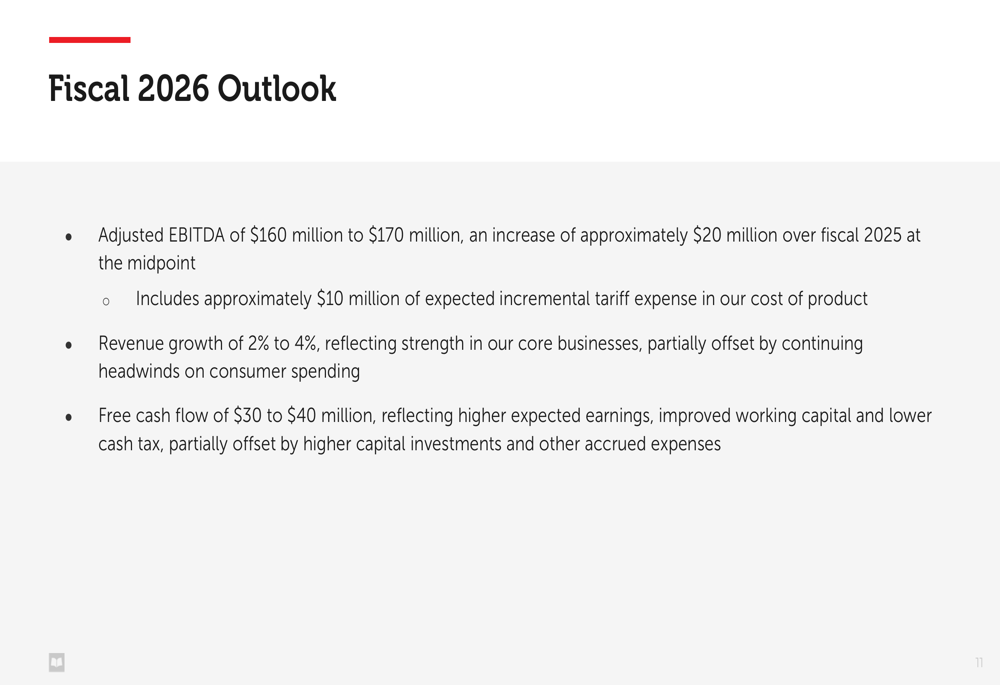

Looking ahead to fiscal 2026, Scholastic projects Adjusted EBITDA of $160-170 million, representing approximately 20% growth at the midpoint compared to fiscal 2025, despite anticipating about $10 million in incremental tariff expenses.

The company forecasts modest revenue growth of 2-4% for fiscal 2026, citing continuing headwinds on consumer spending. Management expects free cash flow of $30-40 million, reflecting higher expected earnings and improved working capital, partially offset by higher capital investments.

As shown in the fiscal 2026 outlook slide:

"We’re targeting strong Adjusted EBITDA growth of 20% at the midpoint of guidance, excluding $10M of anticipated tariff expense," stated Haji Glover, Chief Financial Officer and Executive Vice President.

The company’s growth strategy includes new releases from popular authors like Dav Pilkey, continued growth in Book Fair counts, Book Clubs revitalization, revenue growth resumption in Entertainment, repositioning the Education segment, and focused international growth.

These projections come after Scholastic beat EPS expectations in the third quarter of fiscal 2025, when it reported a loss of $0.13 per share versus an expected loss of $0.78, though revenue slightly missed forecasts at that time.

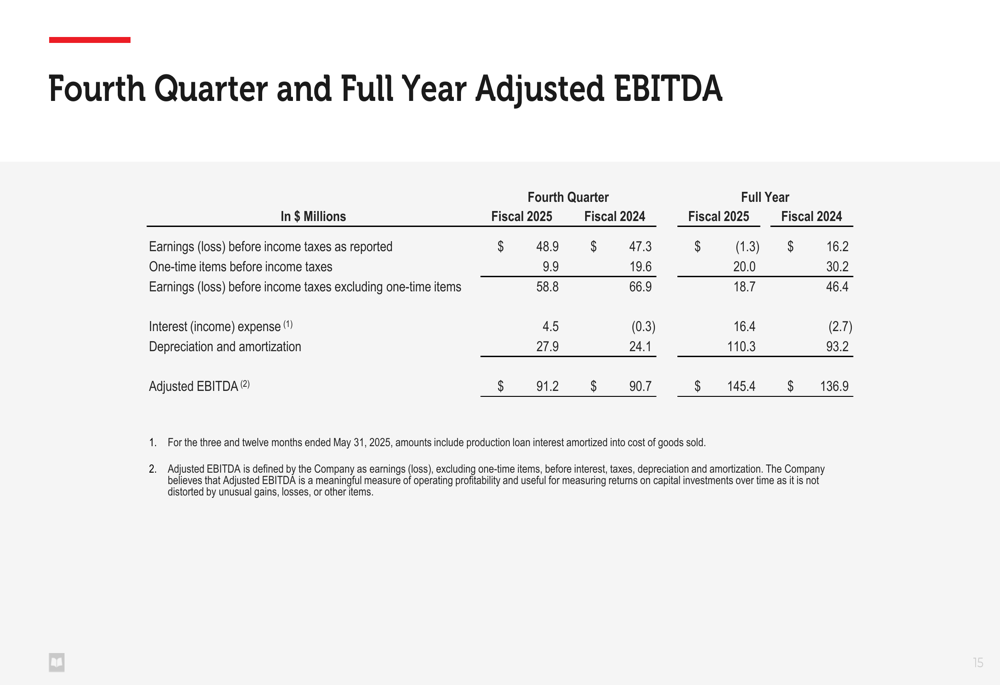

The fourth quarter and full year Adjusted EBITDA breakdown provides additional context for the company’s financial performance:

As Scholastic navigates fiscal 2026, investors will be watching closely to see if the company can deliver on its ambitious EBITDA growth targets while managing the significant debt increase and continuing challenges in consumer and educational spending.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.