United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

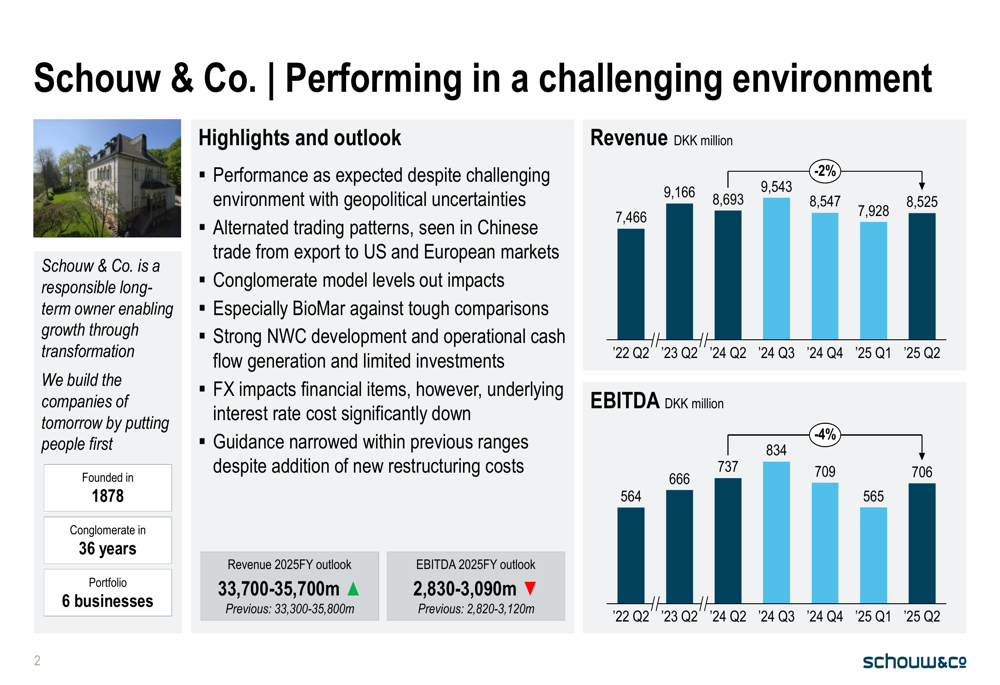

Schouw & Co. (CPH:SCHO) released its Q2 2025 interim report on August 15, 2025, revealing a mixed performance across its portfolio of six businesses. Despite narrowing its full-year guidance within previous ranges, the Danish conglomerate’s stock fell 6.26% to 599 DKK following the presentation, suggesting investors remain concerned about specific segments despite overall stability.

The company reported Q2 2025 revenue of 8,525 million DKK, down 2% year-over-year, while EBITDA reached 706 million DKK. The results come amid what management described as a "challenging environment" characterized by geopolitical uncertainties and shifting trade patterns.

Quarterly Performance Highlights

Schouw & Co.’s Q2 2025 results showed a recovery from Q1’s performance, when EBITDA had declined 13% year-over-year to 565 million DKK. The company highlighted strong net working capital development and operational cash flow generation, while noting that foreign exchange impacts affected financial items, though underlying interest rate costs decreased significantly.

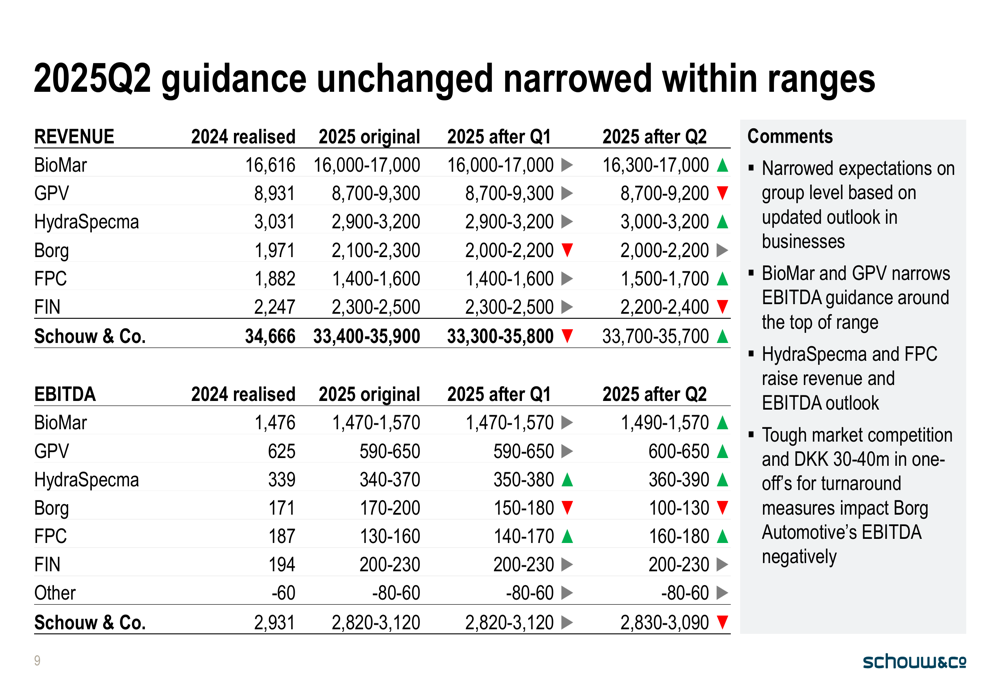

The conglomerate’s diversified business model appears to be providing some resilience, with management narrowing its full-year 2025 guidance to revenue of 33,700-35,700 million DKK (previously 33,300-35,800 million) and EBITDA of 2,830-3,090 million DKK (previously 2,820-3,120 million).

Portfolio Performance Analysis

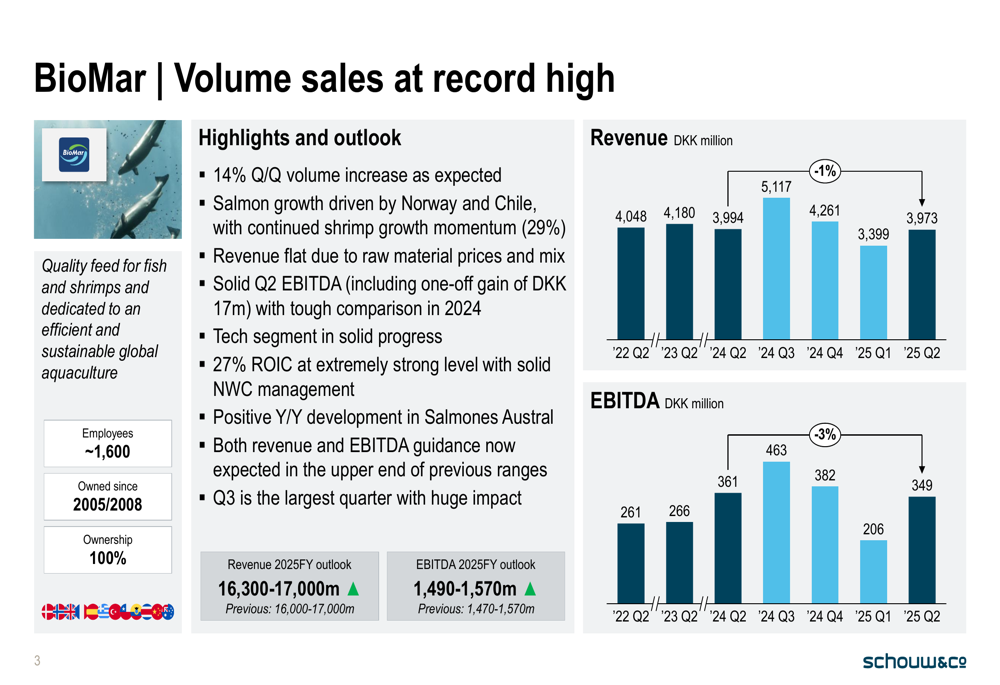

BioMar, Schouw’s aquaculture feed business, emerged as a bright spot with record-high volume sales and a 14% quarter-over-quarter volume increase. While revenue remained flat at 3,973 million DKK due to raw material prices and mix effects, EBITDA reached 349 million DKK, including a one-off gain of 17 million DKK. The company raised expectations for BioMar, now projecting results in the upper end of its guidance ranges.

The following chart illustrates BioMar’s performance metrics:

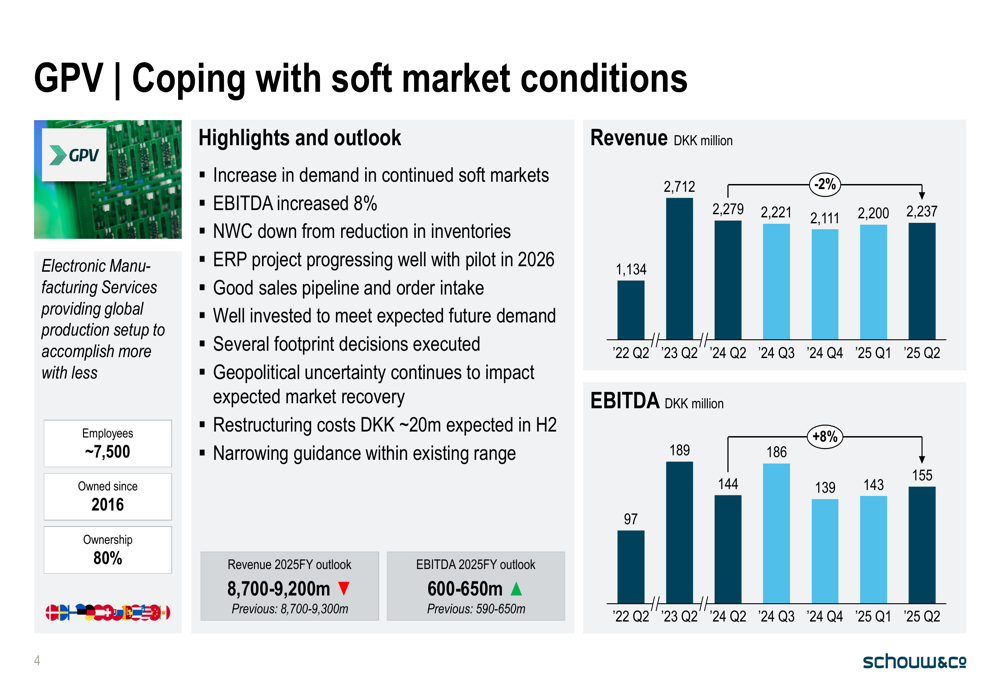

GPV, the electronics manufacturing business, showed resilience despite soft market conditions. The company reported a 2% revenue decline to 2,237 million DKK, but achieved an 8% increase in EBITDA to 155 million DKK. Management highlighted inventory reductions improving net working capital and noted progress on an ERP project with a pilot planned for 2026.

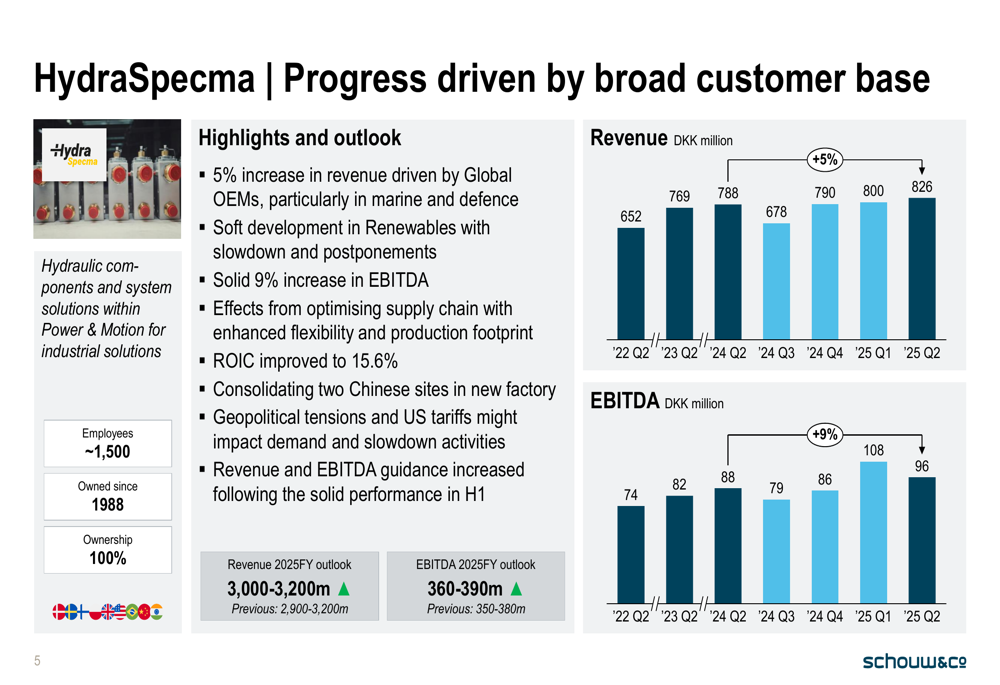

HydraSpecma delivered the strongest growth among portfolio companies with a 5% revenue increase to 826 million DKK, driven by global OEMs, and a solid 9% EBITDA improvement to 96 million DKK. The hydraulic solutions provider improved its ROIC to 15.6% and benefited from supply chain optimization efforts.

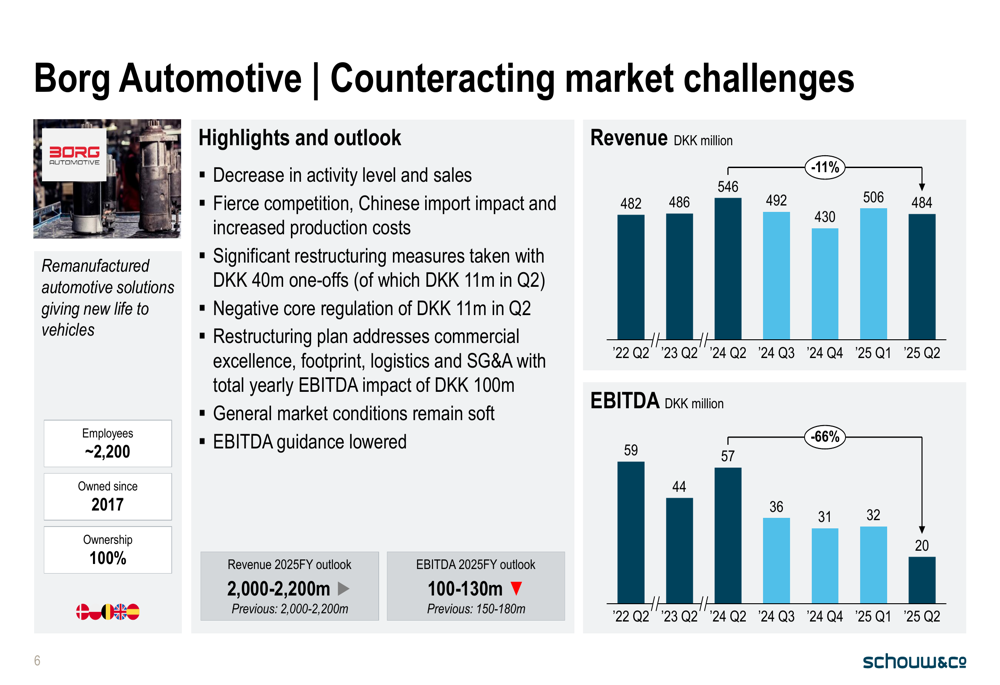

The most significant challenges were evident at Borg Automotive, where revenue declined 11% to 484 million DKK amid "fierce competition" and soft market conditions. EBITDA collapsed to just 20 million DKK, impacted by significant restructuring measures resulting in 40 million DKK of one-off costs and a negative core regulation of 11 million DKK. Consequently, Borg’s full-year EBITDA guidance was substantially reduced to 100-130 million DKK from the previous 150-180 million DKK.

Fibertex Personal Care reported a 13% revenue decline to 426 million DKK due to lower volumes, though EBITDA held relatively steady at 48 million DKK. Despite volume challenges, the company raised both revenue and EBITDA guidance, citing stable European markets and continued good development in its print business.

Fibertex Nonwovens maintained stable volumes with revenue of 581 million DKK, down 3% year-over-year. EBITDA remained nearly unchanged at 57 million DKK, with management noting that progress in US operations offset lower activity in other regions.

Guidance and Outlook

Schouw & Co.’s updated guidance reflects the divergent performance across its portfolio. While the overall guidance ranges were narrowed, the company maintained its full-year expectations, suggesting confidence in achieving its financial targets despite segment-specific challenges.

The detailed guidance comparison below shows how expectations have evolved throughout 2025:

The most notable guidance changes include:

- BioMar: Revenue now expected at 16,300-17,000 million DKK (previously 16,000-17,000 million)

- HydraSpecma: Both revenue and EBITDA guidance raised

- Fibertex Personal Care: Both revenue and EBITDA guidance raised

- Borg Automotive: EBITDA guidance significantly reduced due to restructuring costs

Market Reaction

Despite maintaining overall guidance, Schouw & Co.’s stock dropped 6.26% to 599 DKK following the presentation. This negative reaction likely reflects investor concerns about Borg Automotive’s significant underperformance and restructuring costs, which could indicate deeper structural issues in that business unit.

The stock decline also suggests the market may be focusing on near-term challenges rather than the company’s long-term positioning. Year-to-date, Schouw’s stock has traded between a 52-week low of 521 DKK and a high of 663 DKK, with today’s close representing a significant pullback from recent levels.

Investors appear particularly concerned about the sustainability of earnings in the automotive aftermarket segment, where Borg operates, and may be questioning whether the conglomerate structure provides sufficient value in the current economic environment despite management’s emphasis on being a "responsible long-term owner enabling growth through transformation."

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.