Street Calls of the Week

Introduction & Market Context

Service Corporation International (NYSE:SCI), North America’s largest provider of funeral and cemetery services, presented its first quarter 2025 financial results on May 1, 2025, highlighting significant year-over-year improvements in cash flow and earnings. Despite the strong performance metrics, SCI’s stock dropped 7.32% in premarket trading to $74.05, following a previous close of $79.90.

The company’s presentation focused primarily on non-GAAP financial measures, which SCI uses to evaluate operational performance and provide investors with additional insights beyond standard accounting metrics. The disconnect between the company’s positive financial results and the negative market reaction suggests investors may have had higher expectations or concerns about specific aspects of the outlook.

Quarterly Performance Highlights

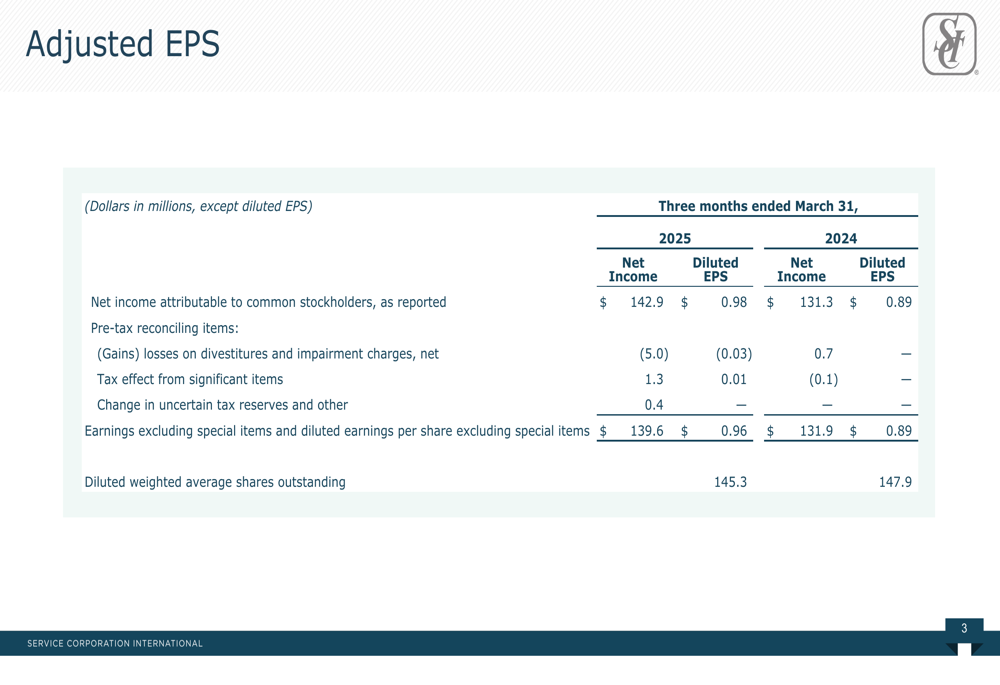

SCI reported net income of $142.9 million for Q1 2025, an 8.8% increase from $131.3 million in the same period last year. Diluted earnings per share rose to $0.98, up from $0.89 in Q1 2024, representing a 10.1% improvement. After adjusting for special items, the company’s adjusted EPS was $0.96, compared to $0.89 in the prior-year quarter.

As shown in the following reconciliation table:

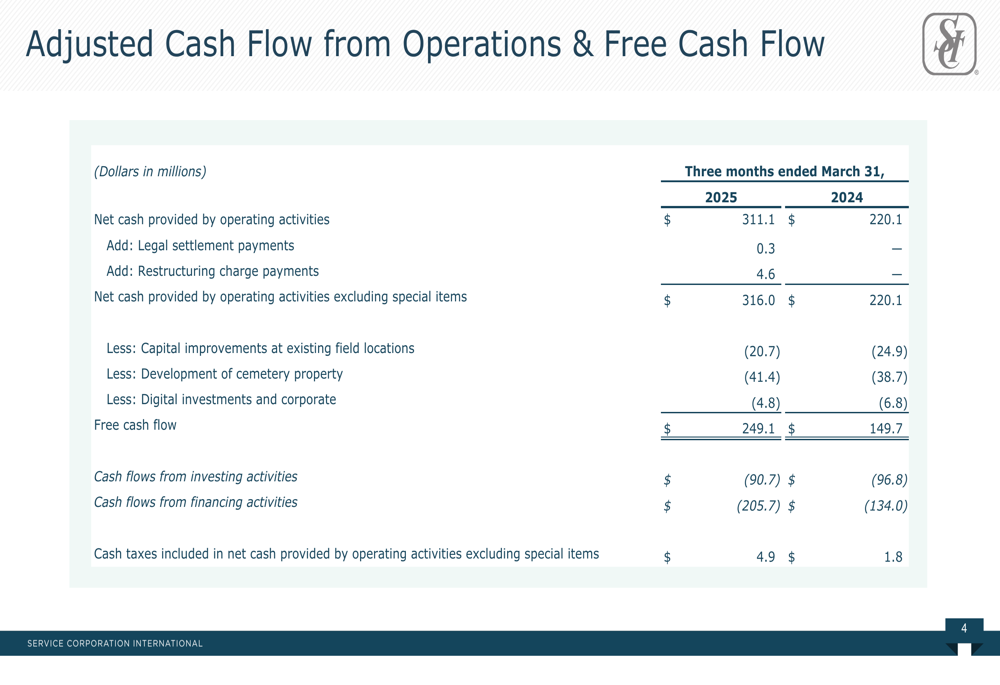

The most impressive aspect of SCI’s quarterly performance was its cash flow generation. Net cash provided by operating activities reached $311.1 million, a substantial 41.3% increase from $220.1 million in Q1 2024. After accounting for special items, adjusted cash flow from operations was $316.0 million, up 43.6% year-over-year.

Detailed Financial Analysis

The company’s free cash flow, which SCI defines as adjusted operating cash flow minus capital expenditures, showed even more dramatic improvement. Free cash flow surged to $249.1 million in Q1 2025, a 66.4% increase from $149.7 million in Q1 2024. This improvement came despite slightly higher cemetery property development costs of $41.4 million compared to $38.7 million in the prior year.

The following cash flow breakdown illustrates these improvements:

SCI’s capital allocation strategy appears to include ongoing share repurchases, as evidenced by the reduction in diluted weighted average shares outstanding from 147.9 million in Q1 2024 to 145.3 million in Q1 2025. This continues the company’s commitment to shareholder returns, which according to previous earnings information included $428 million returned to shareholders through dividends and share repurchases in 2024, along with an 11-year streak of consecutive dividend increases.

Cash taxes included in operating cash flow increased to $4.9 million from $1.8 million in the prior-year period, potentially reflecting higher profitability. However, the company is projecting a significant increase in cash taxes for the full year 2025.

Forward-Looking Statements

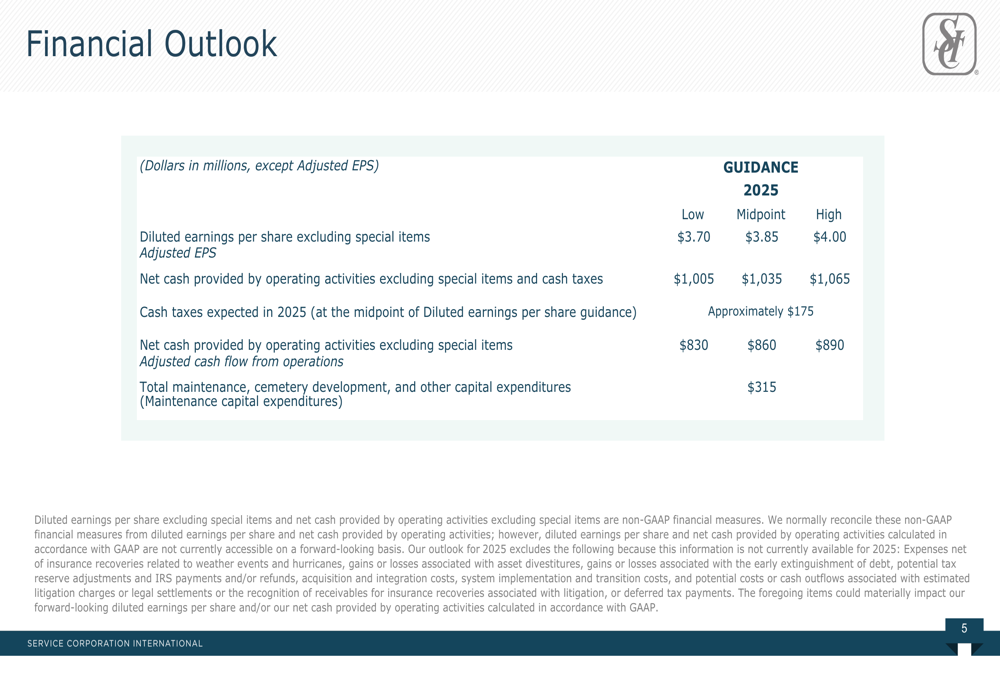

SCI maintained its previously announced 2025 guidance, projecting adjusted earnings per share in the range of $3.70 to $4.00, with a midpoint of $3.85. This guidance represents potential growth of 5-13% compared to 2024 results, aligning with the company’s long-term growth strategy.

The company expects net cash provided by operating activities (excluding special items and before cash taxes) to be between $1,005 million and $1,065 million for the full year. After accounting for projected cash taxes of approximately $175 million, adjusted operating cash flow is expected to range from $830 million to $890 million.

As detailed in the following outlook slide:

SCI plans to invest $315 million in total maintenance, cemetery development, and other capital expenditures during 2025. This represents a reduction from previous years, which could further enhance free cash flow generation if revenue and operating cash flow targets are met.

The company noted several items excluded from its outlook due to unpredictability, including impacts from weather events and hurricanes, gains or losses from divestitures, debt extinguishment effects, tax reserve adjustments, acquisition costs, system implementation expenses, and litigation settlements.

Market Reaction & Analyst Perspectives

The significant premarket decline in SCI’s stock price contrasts sharply with the positive financial metrics presented. Several factors may be contributing to this disconnect:

1. The substantial increase in projected cash taxes for 2025 ($175 million compared to much lower figures in Q1) could be weighing on investor sentiment.

2. While adjusted EPS improved year-over-year, the Q1 2025 figure of $0.96 represents just 25% of the midpoint of full-year guidance ($3.85), potentially raising concerns about the company’s ability to accelerate earnings in subsequent quarters.

3. As noted in previous earnings information, SCI is transitioning to insurance-funded preneed contracts, which may create short-term volatility in financial results despite potential long-term benefits.

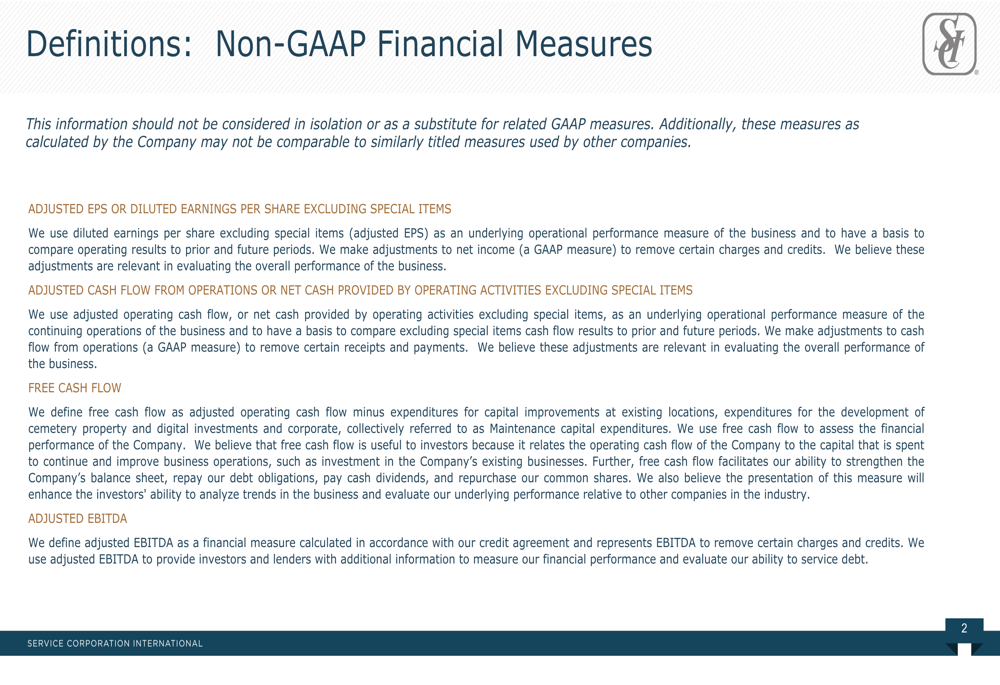

The company’s non-GAAP financial measures provide important context for understanding SCI’s operational performance, as explained in this definitions slide:

Despite the premarket selloff, SCI’s fundamentals appear solid based on the presentation data. The company’s ability to generate significantly higher cash flow year-over-year while maintaining its full-year outlook suggests operational improvements are taking hold. However, investors will likely seek additional clarity on the sustainability of these improvements and the company’s strategy for navigating the projected increase in cash taxes during upcoming earnings calls and investor presentations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.